- Specialty & Fine Chemicals

- Heat Transfer Fluids Market

Heat Transfer Fluids Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Heat Transfer Fluids Market by Product Type (Silicone Fluids, Aromatic Fluids, Mineral Oils, Glycol Based Fluids, Others), Application (Oil & Gas, Chemical Industry, CSP, Food & Beverages, Plastics, Pharmaceuticals, HVAC, Others), and Regional Analysis for 2025 - 2032

Heat Transfer Fluids Market Size and Trends Analysis

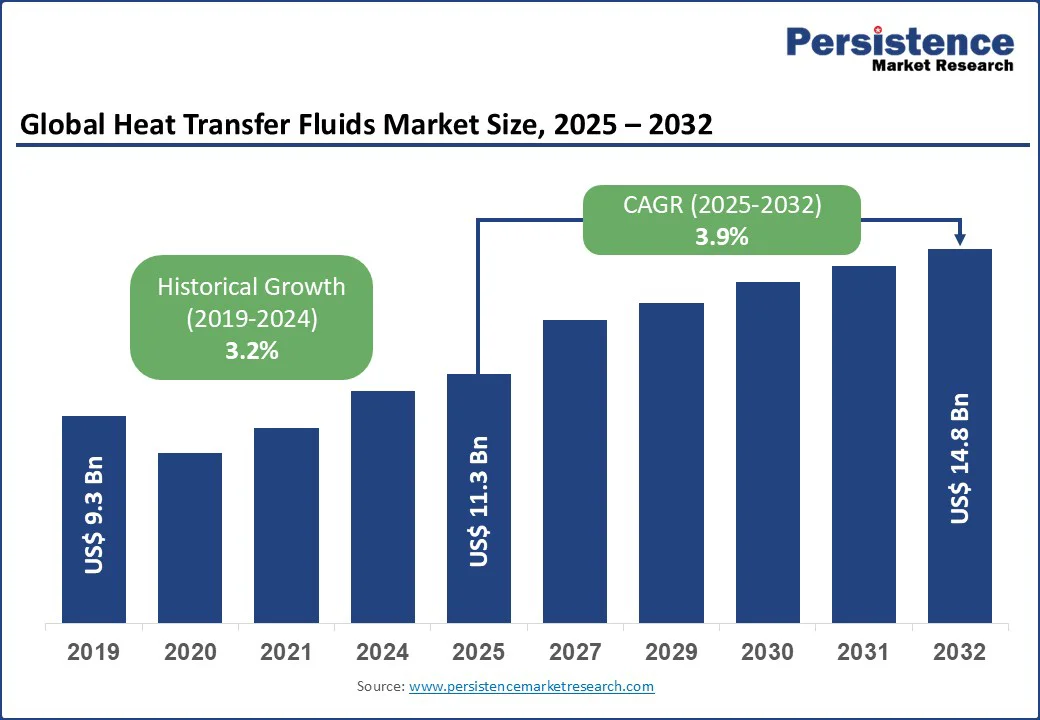

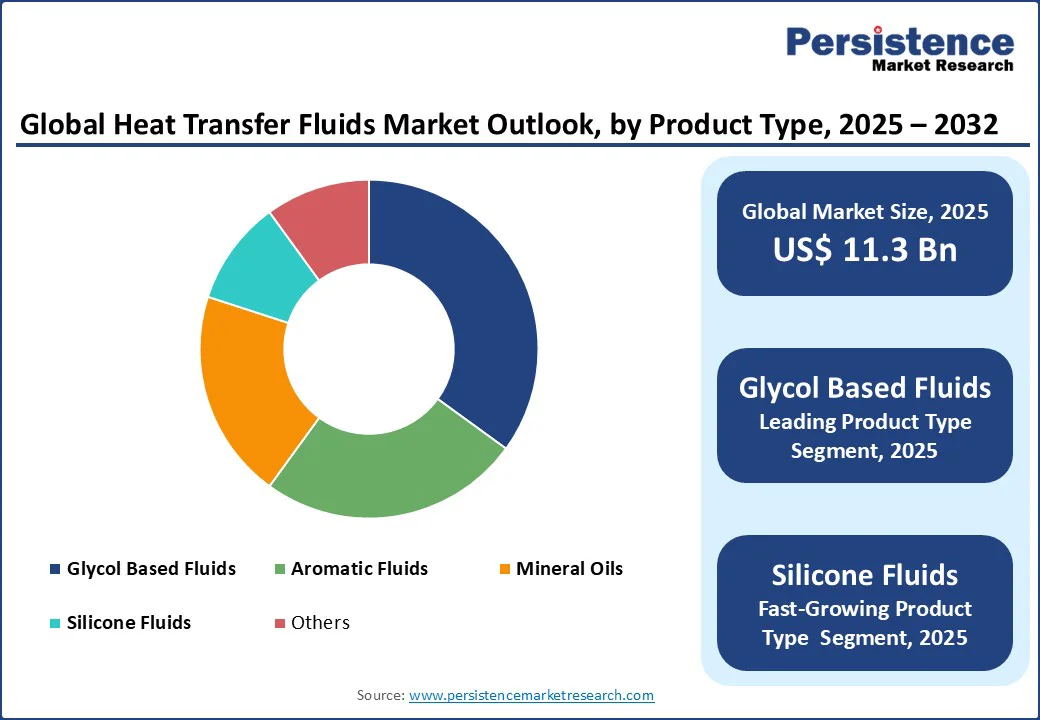

The global heat transfer fluids market size is likely to be valued at US$ 11.3 Bn in 2025, and is expected to reach US$ 14.8 Bn by 2032, growing at CAGR of 3.9% during 2025-2032.

The heat transfer fluids market is driven by increasing demand for efficient thermal management solutions across diverse industries, including chemicals, oil and gas, renewable energy, and HVAC systems. These fluids play a critical role in maintaining consistent temperatures in processes such as chemical manufacturing, solar power generation, food processing, and industrial heating. Growing adoption of advanced technologies, rising focus on energy efficiency, and expansion of industrial and infrastructure projects are fueling market growth.

Key Industry Highlights:

- Leading Product: Glycol Based Fluids hold a 35% market share in 2025, driven by HVAC heat transfer fluids.

- Fast-growing Product: Silicone Fluids fueled by high-temperature heat transfer fluids for chemical processing.

- Dominant Application: Chemical Industry accounts for 30% market share, supported by industrial thermal oils.

- Leading Application: CSP application driven by heat transfer oils for solar power plants. It supports molten salts and thermal oils in renewable energy.

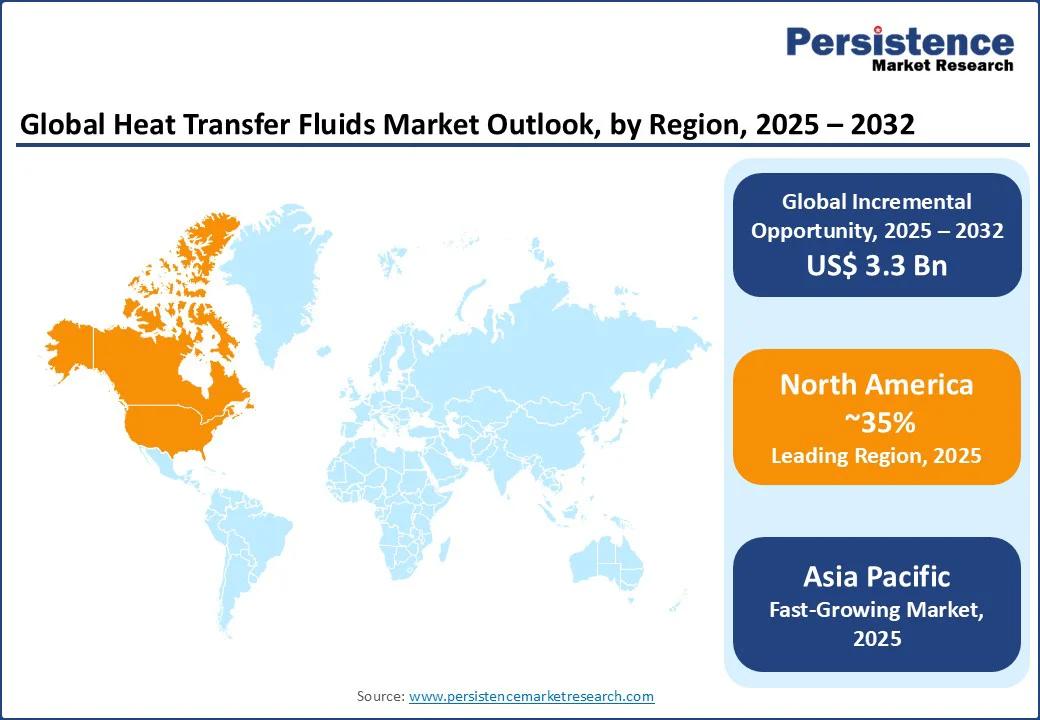

- Prominent Region: North America holds a 35% market share, with the U.S. leading in energy-efficient heat transfer systems.

- Rapid Growing Market: Asia Pacific commands 20%, driven by global demand for thermal heat transfer fluids.

|

Global Market Attribute |

Key Insights |

|

Heat Transfer Fluids Market Size (2025E) |

US$ 11.3 Bn |

|

Market Value Forecast (2032F) |

US$ 14.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.2% |

Market Dynamics

Driver - Growth in Renewable Energy and Industrial Activities

The heat transfer fluids market is propelled by the growth in renewable energy and expanding industrial activities, driving demand for heat transfer oil, glycol fluids, and industrial heat fluids. In 2025, global concentrated solar power (CSP) capacity reached 7 GW, with a 10% annual growth rate, boosting heat transfer oils for solar power plants by 15%. High-temperature heat exchange fluids for chemical processing saw 20% adoption in 2025, driven by the global chemical industry’s output of US$ 4.7 Tn. The rise in energy-efficient heat transfer systems, with 25% of industrial facilities adopting closed-loop heating fluids, supports industrial thermal oils and corrosion-resistant heat carrier fluids for efficient heat exchange.

HVAC thermal transfer fluids grew by 12% in 2025, driven by 30% growth in global HVAC installations. Eastman Chemical Company reported 10% revenue growth in 2025 from thermal oils for process heating. The global push for net-zero emissions, with US$ 500 Bn in renewable energy investments by 2030, positions heat transfer medium for industrial systems and energy conservation fluids for sustained growth, particularly in CSP and chemical industry applications.

Restraint - High Costs and Environmental Concerns

The heat transfer fluids market faces challenges due to high costs and environmental concerns associated with industrial process fluids and thermal heat fluids. Producing high-temperature heat carrier fluids for chemical processing and molten salts and thermal oils costs US$ 500–US$ 2000 per ton, limiting adoption in cost-sensitive markets. Disposal of industrial thermal oils, with 20% classified as hazardous waste, increases compliance costs by 15%, impacting closed-loop heating fluids. Environmental regulations, such as REACH in Europe, restricted 30% of aromatic fluids in 2025, affecting heat exchangers and fluids. These constraints slower adoption of corrosion-resistant thermal transfer fluids in emerging regions, where 25% of manufacturers face regulatory compliance issues, particularly in oil & gas and plastics applications.

Opportunity - Advancements in Eco-Friendly and High-Performance Fluids

Advancements in eco-friendly and high-performance energy conservation fluids and corrosion-resistant thermal transfer fluids present significant opportunities for the heat transfer fluids market, driving demand for thermal oils for process heating and heat transfer oils for solar power plants. In 2025, the global green chemicals market reached US$ 150 Bn, with a 7% CAGR, boosting glycol fluids and silicone fluids by 15% for their biodegradability. Molten salts and thermal oils, with 20% improved thermal efficiency, support heat transfer medium for industrial systems in CSP applications. Emerging markets, with US$ 100 Bn in renewable energy investments in 2025, offer potential for energy-efficient heat transfer systems in HVAC and pharmaceuticals. BASF SE reported 8% growth in 2025 from corrosion-resistant thermal transfer fluids, positioning the market for expansion in chemical industry and food & beverages applications.

Category-wise Analysis

Product Type Insights

Glycol based fluids account for 35% share in 2025, driven by HVAC heat carrier fluids. They ensure efficient heat transfer in HVAC and food & beverages. Propylene glycol and ethylene glycol are commonly used due to their superior thermal properties, non-corrosive nature, and ability to operate effectively in both heating and cooling cycles. These characteristics make them ideal for closed-loop systems that require stable performance under varying temperatures.

Silicone fluids are fueled by high-temperature heat carrier fluids for chemical processing. They support industrial thermal oils in chemical industry applications. These fluids offer exceptional thermal stability, low viscosity variation, and superior resistance to oxidation and thermal degradation, making them indispensable in processes requiring consistent heat transfer under extreme conditions. Industries such as chemicals, pharmaceuticals, and plastics processing rely on silicone fluids for heating and cooling reactors, condensers, and distillation units, where precise temperature control is critical to maintaining product integrity and process efficiency.

Application Insights

Chemical industry commands a 30% market share in 2025, driven by industrial thermal oils. It relies on high-temperature thermal transfer fluids for chemical processing, with 15% growth in chemical production. This growth directly translates to increased consumption of heat exchange fluids. Energy efficiency regulations and the push for sustainable solutions are further encouraging chemical manufacturers to adopt advanced synthetic fluids that offer superior heat stability, oxidation resistance, and extended fluid life.

CSP fueled by heat transfer oils for solar power plants. It supports molten salts and thermal oils in renewable energy. Thermal oils are particularly valued for their excellent heat stability and ability to withstand continuous high-temperature operations without degradation. The integration of molten salts further enhances heat storage capacity, supporting power generation even during periods without sunlight. This capability aligns with the global shift toward sustainable energy solutions and grid stability, positioning CSP as a vital technology for decarbonization efforts.

Regional Insights

North America Heat Transfer Fluids Market Trends

North America holds a 35% global market share in 2025, valued at US$ 3.96 Bn, with the U.S. leading due to advanced industrial and renewable energy sectors. The U.S. market generating US$ 3.05 Bn in 2025 driven by energy-efficient heat transfer systems and heat transfer oils for solar power plants. In 2025, 40% of U.S. CSP plants adopted molten salts and thermal oils, supported by 20% growth in renewable energy capacity, reaching 200 GW. The chemical industry, with US$ 800 Bn in output, boosts high-temperature thermal transfer fluids for chemical processing by 15%. Eastman Chemical Company holds a 12% regional share, leveraging industrial thermal oils. Investments in energy conservation fluids, reaching US$ 50 Bn by 2025, drive closed-loop heating fluids in HVAC and pharmaceuticals.

Europe Heat Transfer Fluids Market Trends

Europe accounts for a 30% global share, valued at US$ 3.39 Bn in 2025, led by Germany, the UK, and France, driven by stringent environmental regulations and industrial growth. Germany’s market grows at a CAGR of 3.8%, generating US$ 1.36 Bn in 2025, propelled by industrial process fluids and corrosion-resistant Heat exchange fluids. The chemical sector, contributing €550 Bn to the economy, saw 35% of manufacturers adopt thermal oils for process heating in 2025, driven by REACH regulations. The UK market is driven by HVAC heat carrier fluids, with 30% adoption in 2025. France’s market grows at 7%, fueled by heat transfer medium for industrial systems, with €100 Mn in CSP investments. BASF SE leads with energy conservation fluids, capturing 10% of the market.

Asia Pacific Heat Transfer Fluids Market Trends

Asia Pacific is the fastest-growing with a CAGR of 4.2%, valued at US$ 3.39 Bn in 2025, led by China, Japan, and India, driven by industrial expansion and renewable energy adoption. China holds a 50% regional share, fueled by US$ 200 Bn in industrial and renewable energy investments, boosting global demand for thermal transfer heat. In 2025, 45% of Chinese CSP plants adopted heat transfer oils for solar power plants. India’s market driven by 25% growth in chemical production, with 40% adoption of industrial thermal oils. Japan’s market sees 8% growth, with 35% adoption of energy-efficient heat transfer systems for HVAC. HPCL captures 10% of the regional market with thermal heat fluids.

Competitive Landscape

The global Heat Transfer Fluids Market is highly competitive, with Hindustan Petroleum Corporation Ltd. (HPCL), Delta Western, Inc. (DWI), British Petroleum (BP), Huntsman Corporation, Royal Dutch Shell Plc, Eastman Chemical Company, Phillips 66, Chevron Co., BASF SE, Exxon Mobil, DowDuPont Chemicals, Dalian Richfortune Chemicals Ltd., GJ Chemical, Radco Industries Inc., LANXESS AG, and Schultz Chemicals focusing on heat transfer oil, glycol fluids, and industrial heat fluids. Companies leverage high-temperature industrial heat fluids for chemical processing and heat transfer oils for solar power plants to gain market share. Strategic R&D investments in energy conservation fluids and partnerships drive heat transfer medium for industrial systems, addressing corrosion-resistant thermal transfer fluids needs.

Key Developments

- In August 2025, Thermal fluid specialist, Global Heat Transfer, has launched a new synthetic heat transfer fluid, Globaltherm® DBT, designed for use in the liquid phase within closed, forced circulation heat transfer systems. Suitable for a wide range of industrial process applications, including chemical and plastics applications - the fluid offers a reliable, high-performance solution for managing temperature.

- In May 2023, ORLEN Po?udnie announced the completion of the first operational year of its BioPG plant, involving the conversion of glycerol into renewable propylene glycol. BASF provided its BioPG technology for the purpose, while Air Liquide Engineering & Construction contributed with the licensing, proprietary equipment, and basic engineering services.

Companies Covered in Heat Transfer Fluids Market

- Hindustan Petroleum Corporation Ltd.

- Delta Western, Inc.

- British Petroleum

- Huntsman Corporation

- Royal Dutch Shell Plc

- Eastman Chemical Company

- Phillips 66

- Chevron Co.

- BASF SE

- Exxon Mobil

- DowDuPont Chemicals

- Dalian Richfortune Chemicals Ltd.

- GJ Chemical

- Radco Industries Inc.

- LANXESS AG

- Schultz Chemicals

- Others

Frequently Asked Questions

The heat transfer fluids market is projected to reach US$ 11.3 Bn in 2025, driven by heat transfer oil and glycol fluids.

Global CSP capacity of 7 GW in 2025 and chemical industry output of US$ 4.7 Tn fuel industrial heat fluids.

The heat transfer fluids market grows at a CAGR of 3.9% from 2025 to 2032, reaching US$ 14.8 Bn by 2032.

Eco-friendly energy conservation fluids, with 20% improved efficiency, offer growth in heat transfer medium for industrial systems.

Key players include HPCL, Eastman Chemical Company, BASF SE, Exxon Mobil, and DowDuPont Chemicals.