- Specialty & Fine Chemicals

- Ferro Fluids Market

Ferro Fluids Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Ferro Fluids Market by Product Type (Oil-Based, Water-based Ferrofluids, Synthetic-Based Ferrofluids), Function (Sealing, Cooling / Heat Transfer, Damping & Vibration Control, Magnetic Positioning & Sensing), Application (Electronics, Industrial, Healthcare, Aerospace & Defense, Research, Others), and Regional Analysis, 2026 - 2033

Ferro Fluids Market Size and Trend Analysis

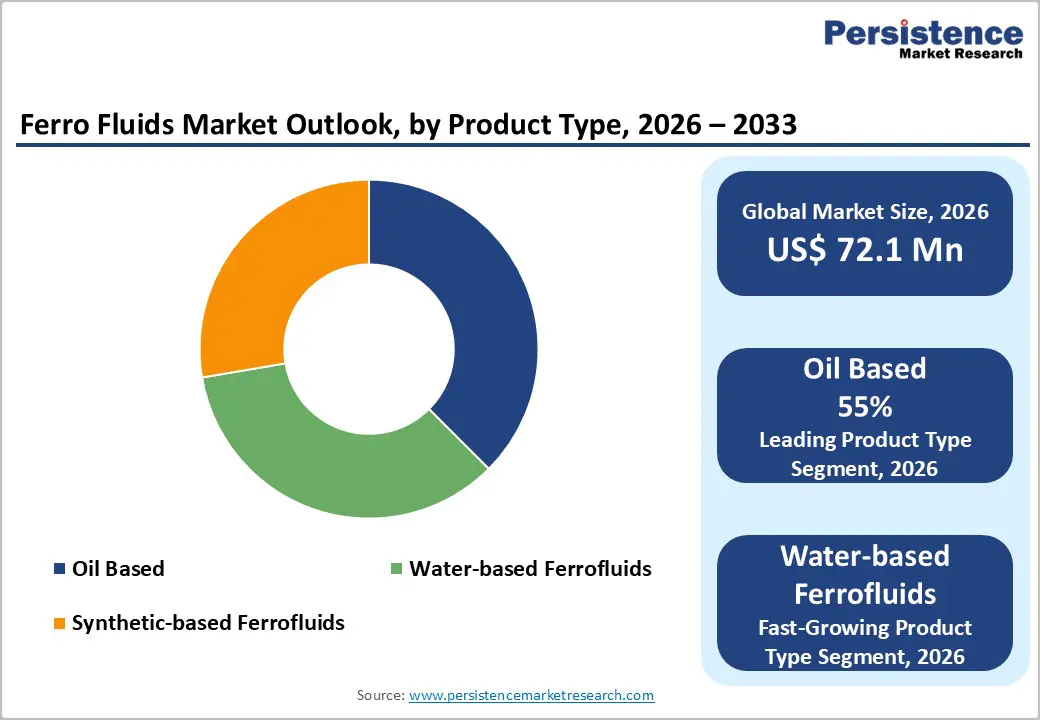

The global ferro fluids market size is expected to be valued at US$ 72.1 million in 2026 and projected to reach US$ 109.1 million by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

Growth is fueled by advancements in nanotechnology and increasing demand across electronics, healthcare, and industrial sectors. In electronics, ferrofluids improve heat dissipation in speakers and hard drives, supporting device miniaturization. In healthcare, their magnetic properties enable targeted drug delivery, with significant expansion expected in the U.S. sector. Industrial applications, including sealing and damping, benefit precision engineering, further driving market adoption globally.

Key Industry highlights:

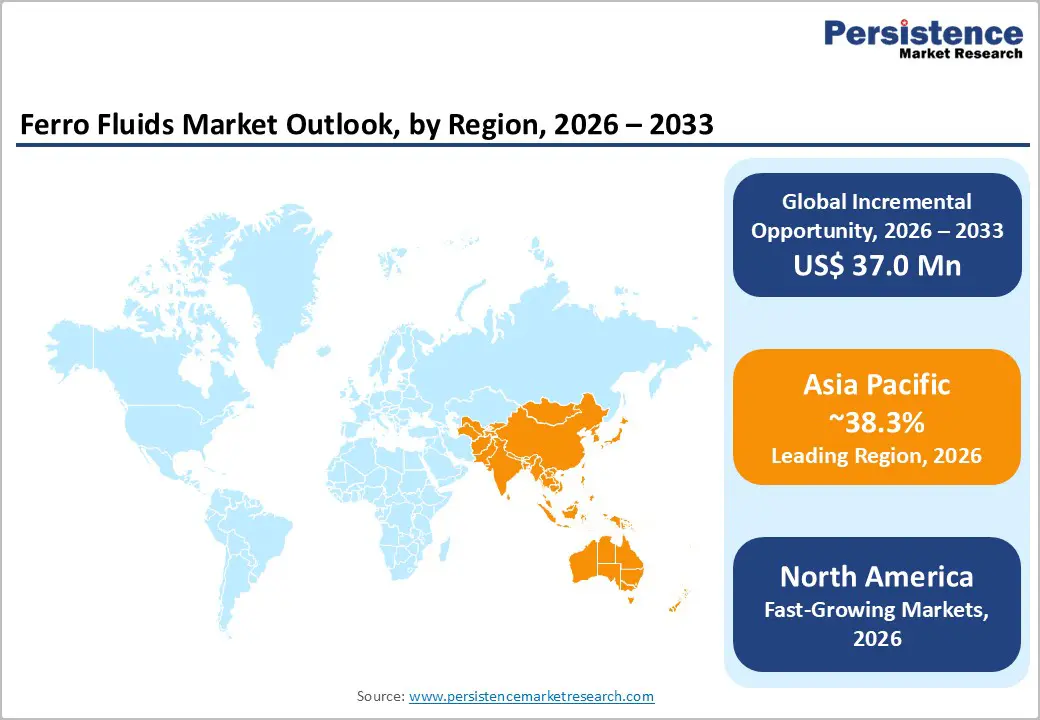

- Leading Region: Asia Pacific leads with 38.3% share, driven by large-scale manufacturing hubs in China, Japan, and rising electronics and EV production across emerging economies.

- Fastest-Growing Region: North America emerges as the fastest-growing region, driven by the United States due to its strong presence in aerospace, electronics, and advanced industrial manufacturing.

- Leading Product Category: Oil-based ferrofluids dominate the product landscape with ~55% share in 2025, owing to superior thermal stability, low viscosity, and widespread industrial and electronics use.

- Fastest-Growing Application: Healthcare represents the fastest-growing application area, fueled by advancements in magnetic drug delivery, diagnostics, and biocompatible ferrofluid formulations.

- Key Opportunity Area: Water-based ferrofluids present a major opportunity, particularly for sustainable and medical applications, due to improved biocompatibility, lower toxicity, and regulatory alignment.

| Key Insights | Details |

|---|---|

| Ferro Fluids Size (2026E) | US$ 72.1 million |

| Market Value Forecast (2033F) | US$ 109.1 million |

| Projected Growth CAGR (2026 - 2033) | 6.1% |

| Historical Market Growth (2020 - 2025) | 5.3% |

Market Dynamics

Drivers - Rising Use of Ferrofluids in Electronics and Healthcare

The proliferation of compact electronic devices has driven increased adoption of ferrofluids for thermal management and vibration damping. They improve heat dissipation in high-performance speakers, hard drives, and other precision components, addressing challenges posed by miniaturization. Growing consumer electronics demand, particularly in Asia Pacific, further fuels the need for advanced ferrofluid solutions.

In healthcare, ferrofluids are increasingly applied in magnetic drug delivery systems using biocompatible water-based variants. This allows precise targeting of therapeutic agents, minimizing side effects and improving treatment outcomes. Rising interest in such technologies continues to propel market growth, encouraging ongoing innovation in ferrofluid formulations for both electronics and healthcare applications.

Growing Industrial and Aerospace Applications of Ferrofluid Seals

Ferrofluid-based sealing solutions are gaining prominence in industrial machinery due to their ability to provide hermetic sealing in vacuum pumps, motors, and high-speed rotating equipment. Oil-based ferrofluids, like Ferrotec’s EMG series, reduce leakage, improve reliability, and extend operational life, making them ideal for precision engineering environments.

In aerospace, ferrofluids are used for vibration damping and control, outperforming conventional seals amid rising aircraft production. These applications demonstrate ferrofluids’ superior durability, minimal maintenance requirements, and efficiency benefits, reinforcing their role as a key growth driver in industrial and aerospace sectors.

Restraints - High Production Costs and Stability Limitations

The production of ferrofluids involves complex synthesis processes that rely on high-purity magnetic nanoparticles and specialized surfactants, significantly increasing manufacturing costs. Materials such as γ-Fe2O3 require precise particle size control and uniform surface coating to maintain magnetic responsiveness and fluid stability. Oil-based ferrofluids used in industrial environments demand strict quality measures to ensure performance consistency, further raising production expenses.

Moreover, maintaining long-term colloidal stability remains a technical challenge, particularly under fluctuating temperatures and strong magnetic fields. Particle agglomeration and sedimentation can degrade performance, limiting suitability for demanding industrial applications. These stability concerns increase formulation complexity and testing requirements, constraining scalability and slowing broader market adoption.

Limited Awareness and Regulatory Barriers in Emerging Applications

Despite strong technical potential, the limited awareness of ferrofluid capabilities in emerging applications restricts market penetration. In biomedical uses such as magnetic hyperthermia and targeted drug delivery, commercialization is slowed by stringent regulatory approval processes. Extensive biocompatibility and toxicity testing lengthen development timelines, discouraging rapid adoption within healthcare systems.

Supply chain vulnerabilities related to specialized raw materials, including magnetic nanoparticles and surfactants, increase procurement risks and costs. Limited supplier availability and dependency on advanced manufacturing infrastructure further restrain expansion into new markets. These combined regulatory, awareness, and supply challenges continue to act as barriers to the widespread adoption of ferrofluids across emerging application areas.

Opportunity - Expansion of Water-Based Ferrofluids for Sustainable Applications

Water-based ferrofluids are gaining increasing attention due to their environmentally friendly profiles and suitability for sensitive applications. Their low toxicity and improved biocompatibility make them ideal for medical, environmental, and laboratory uses where safety and sustainability are critical. Ongoing research into biodegradable surfactants and greener synthesis methods further enhances their appeal, supporting compliance with tightening environmental regulations.

In medical applications, water-based ferrofluids enable advanced targeted therapies and diagnostic techniques by offering controlled magnetic responsiveness with reduced risk. Manufacturing strength in East Asia, combined with cost-efficient production capabilities, is accelerating adoption across multiple industries. These factors create strong opportunities for market players to expand sustainable product portfolios and address growing demand for eco-conscious ferrofluid solutions.

Rising Opportunities in Aerospace, Defense, and Advanced Thermal Management

The aerospace and defense sectors present significant opportunities for ferrofluids due to their ability to support precision sensing, vibration control, and efficient heat transfer. Ferrofluids are particularly valuable in zero-gravity environments, where they enable controlled fluid positioning and thermal regulation in space systems. This functionality supports increasing investment in advanced aerospace technologies.

Strong research ecosystems and defense innovation initiatives, especially in the United States, continue to drive the development of high-performance ferrofluid solutions. Beyond aerospace, emerging applications in electric vehicle thermal management further expand the potential. As global electrification accelerates, ferrofluids offer promising solutions for managing heat and enhancing system efficiency across advanced mobility platforms.

Category-wise Analysis

Product Type Insights

Oil-based ferrofluids dominate the product type landscape, accounting for around 55% market share in 2025, driven by their superior thermal stability, electrical insulation, and compatibility with demanding industrial environments. Their low viscosity makes them well-suited for high-speed applications such as loudspeakers, rotating seals, and automotive components. Established product lines, including Ferrotec’s EMG series, have reinforced adoption across electronics and precision machinery, supporting their continued leadership.

Water-based ferrofluids are emerging as the fastest-growing product type, primarily due to rising demand from healthcare, laboratory, and environmentally sensitive applications. Improved biocompatibility, reduced toxicity, and ongoing innovation in surfactant chemistry are expanding their usability. Growing focus on sustainable materials and regulatory compliance further accelerates the adoption of water-based formulations across new application areas.

Function Insights

Sealing remains the leading functional segment, holding approximately 40% share in 2025, supported by widespread use in hermetic rotary seals for pumps, compressors, and electric motors. Ferrofluids enable magnetic containment that prevents leakage at rotational speeds exceeding 10,000 RPM, ensuring reliable performance in harsh and vacuum environments. Their ability to reduce wear and maintenance requirements strengthens dominance in industrial and manufacturing settings.

Cooling and thermal management represent the fastest-growing functional area as systems become more compact and thermally sensitive. Ferrofluids are increasingly explored for efficient heat dissipation in electronics, electric vehicles, and aerospace components. Their dual capability to manage heat while maintaining magnetic control positions them as attractive alternatives to conventional cooling methods in advanced engineering applications.

Application Insights

Electronics leads the application landscape with around 35% market share in 2025, driven by extensive use of ferrofluids in speakers, hard disk drives, and precision electronic components. They enhance damping, reduce friction, and improve heat dissipation, addressing challenges posed by device miniaturization. Strong demand from consumer electronics and audio equipment manufacturers continues to support this segment’s leadership.

Healthcare is emerging as the fastest-growing application segment, supported by increasing research into magnetic drug delivery, diagnostics, and therapeutic technologies. Advances in biocompatible ferrofluids enable controlled magnetic manipulation with minimal side effects. Expanding interest in precision medicine and non-invasive treatment methods continues to unlock new opportunities for ferrofluid adoption in medical applications.

Regional Insights

North America Ferro Fluids Market Trends

North America holds a significant share of around 34.6% in 2025, led primarily by the United States due to its strong presence in aerospace, electronics, and advanced industrial manufacturing. Ferrofluids are widely used in vibration control, thermal management, and precision sealing, supported by applications in space programs and high-end defense systems. Adoption is reinforced by established players and early integration of advanced materials technologies.

The region also benefits from a robust research and development ecosystem, with universities and research institutions actively advancing ferrofluid formulations, including biocompatible variants. Continuous innovation, coupled with high-value industrial demand, supports steady expansion across emerging applications such as medical devices and next-generation electronics.

Europe Ferro Fluids Market Trends

Europe demonstrates steady growth in the ferrofluids market, driven by strong industrial and automotive manufacturing bases. Countries such as Germany lead adoption in precision engineering and automotive sealing applications, supported by harmonized regulatory frameworks like REACH. The region is projected to grow at a moderate CAGR of around 5.8%, reflecting stable demand across industrial and medical segments.

The United Kingdom and France are advancing ferrofluid use in medical imaging, diagnostics, and research applications, while sustainability-focused policies encourage innovation in eco-friendly formulations. A well-established industrial ecosystem, combined with growing emphasis on green technologies, continues to support ferrofluid adoption across diverse European end-use industries.

Asia Pacific Ferro Fluids Market Trends

Asia Pacific accounts for the largest share of approximately 38.3% in 2025, driven by strong manufacturing capabilities in China and Japan and rapidly expanding electronics production across the region. Ferrofluids are extensively used in speakers, hard drives, and precision components, benefiting from large-scale consumer electronics manufacturing and export-oriented industries.

Emerging economies such as India and ASEAN countries are witnessing increased adoption, supported by cost advantages and expanding electronics, semiconductor, and electric vehicle manufacturing. Rising investments in advanced manufacturing infrastructure and growing demand for thermal management solutions position the Asia Pacific as a key growth engine for the global ferrofluids market.

Competitive Landscape

The ferrofluids market is moderately consolidated, with a limited number of established players holding strong positions due to specialized manufacturing capabilities and proprietary formulations. Competition is largely driven by continuous research and development aimed at improving magnetic responsiveness, thermal stability, and application-specific performance. Leading participants focus on developing customized solutions to meet precise industrial, electronics, and medical requirements, reinforcing long-term customer relationships.

Strategic collaborations, technology partnerships, and product customization remain key competitive strategies. Companies increasingly emphasize tunable viscosity, enhanced stability, and environmentally responsible formulations to differentiate offerings. Growing focus on sustainability and advanced material engineering is shaping next-generation ferrofluid products and influencing competitive positioning across global markets.

Key Developments:

- In March 2025, Yale University developed ferrofluid-based microfluidic systems for rapid pathogen detection, improving diagnostic precision and sensitivity. This advancement highlights the growing role of ferrofluids in biomedical research and next-generation diagnostic technologies.

- In 2024, Ferrotec enhanced its oil-based ferrofluid series for electric vehicle cooling applications, improving thermal efficiency and heat dissipation. The development supports the rising demand for advanced thermal management solutions in electric mobility and power electronics.

Companies Covered in Ferro Fluids Market

- Ferrotec Holdings Corporation

- Liquids Research Limited

- FerroLabs Inc.

- American Elements

- MoreTec Group

- EMG International

- Sigma-Aldrich (Merck Group)

- BASF SE

- Chemicell GmbH

- DOWA Electronics Materials Co., Ltd.

- Eagle Industry Co., Ltd.

- Ocean NanoTech

- Reade International Corp.

- Nanogap Sub-Nano Powder

- Shenzhen Magpower Magnetic Materials Co., Ltd.

Frequently Asked Questions

The global ferro fluids market is expected to reach US$ 72.1 million in 2026.

Key drivers include electronics thermal management and healthcare drug delivery, with the Asia Pacific manufacturing surge.

North America leads with ~34.6% market share in 2025, driven by U.S. innovation in aerospace, electronics, and advanced industrial applications.

Water-based ferrofluids offer a major opportunity due to the rising demand for sustainable and biocompatible solutions in medical and environmental applications.

Leading companies include Ferrotec Holdings Corporation, LORD Corporation, and Liquids Research Limited.