- Industrial Machinery

- Fluid Handling System Market

Fluid Handling System Market Size, Share, and Growth Forecast, 2026 – 2033

Fluid Handling System Market by Equipment Type (Pumps, Control Valves, Flow Meters), Pump Type (Centrifugal Pumps, Positive Displacement), Service Type, End-use Industry (Chemicals, Others), and Regional Analysis 2026 – 2033

Fluid Handling System Market Size and Trends Analysis

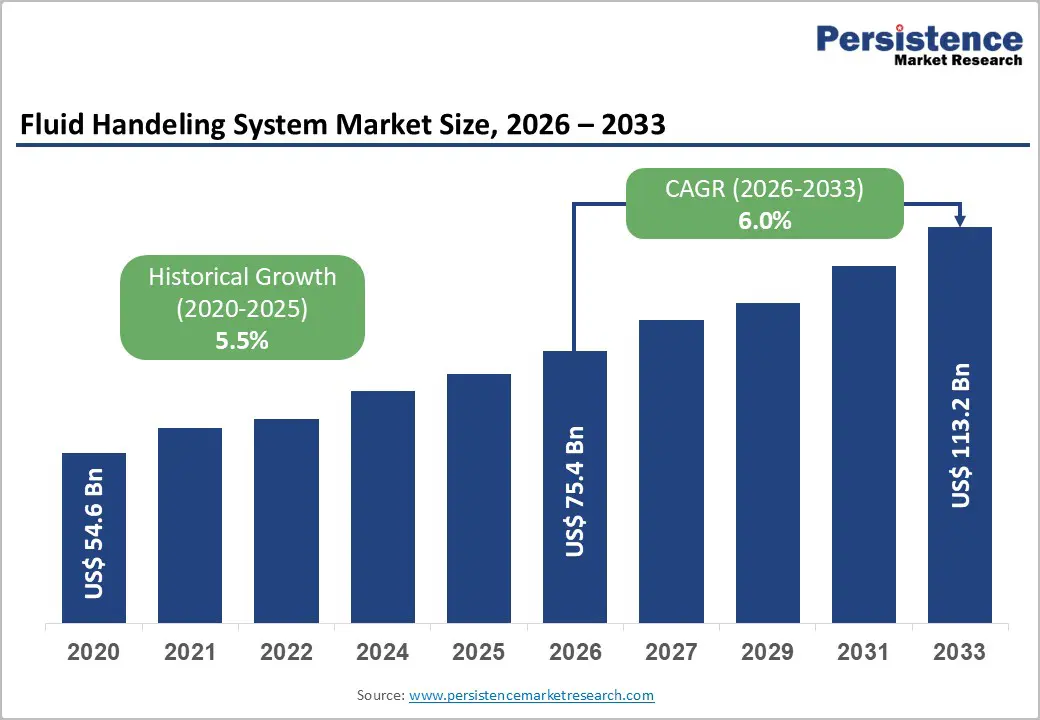

The global fluid handling system market size is likely to be valued at US$75.4 billion in 2026 and is expected to reach US$113.2 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by the rising demand in chemicals, oil & gas, and water treatment sectors, alongside automation and regulatory pressures for efficient fluid management.

The escalation in global wastewater treatment mandates, coupled with the expansion of chemical processing capacities in emerging economies, underpins this positive trajectory. The strategic pivot toward energy-efficient pumping systems to meet net-zero carbon goals is revitalizing demand across established industrial sectors.

Key Industry Highlights:

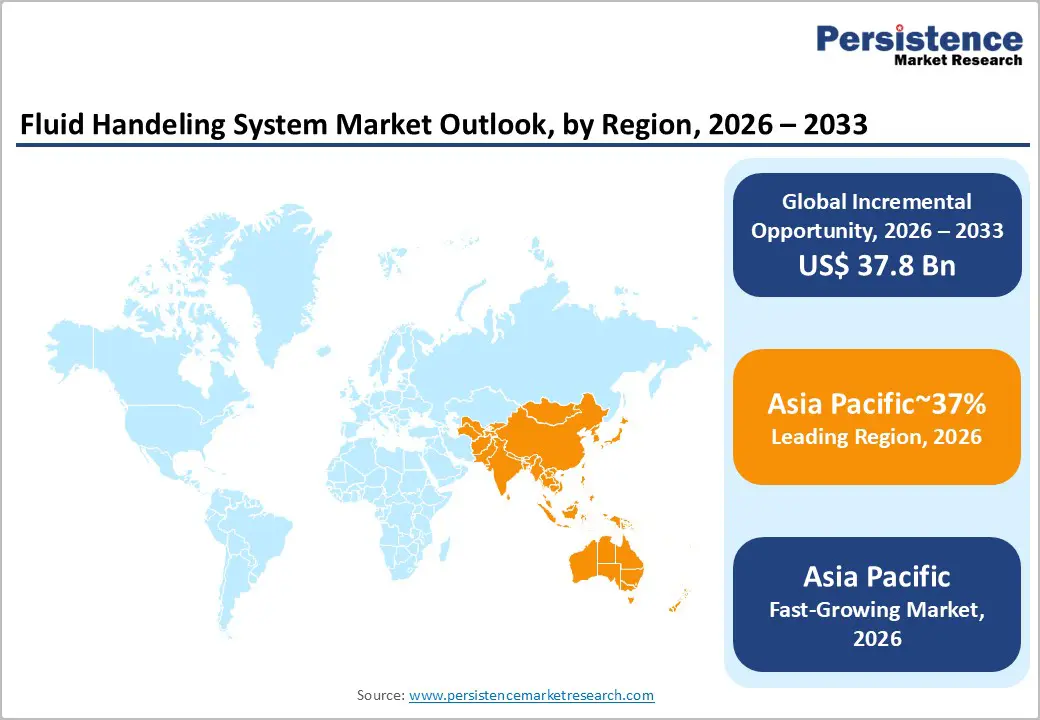

- Leading and Fastest-growing Region: Asia Pacific is projected to lead with approximately 37% share, supported by large-scale industrialization, infrastructure investments, and capacity expansions in chemicals, manufacturing, and water treatment across China and India.

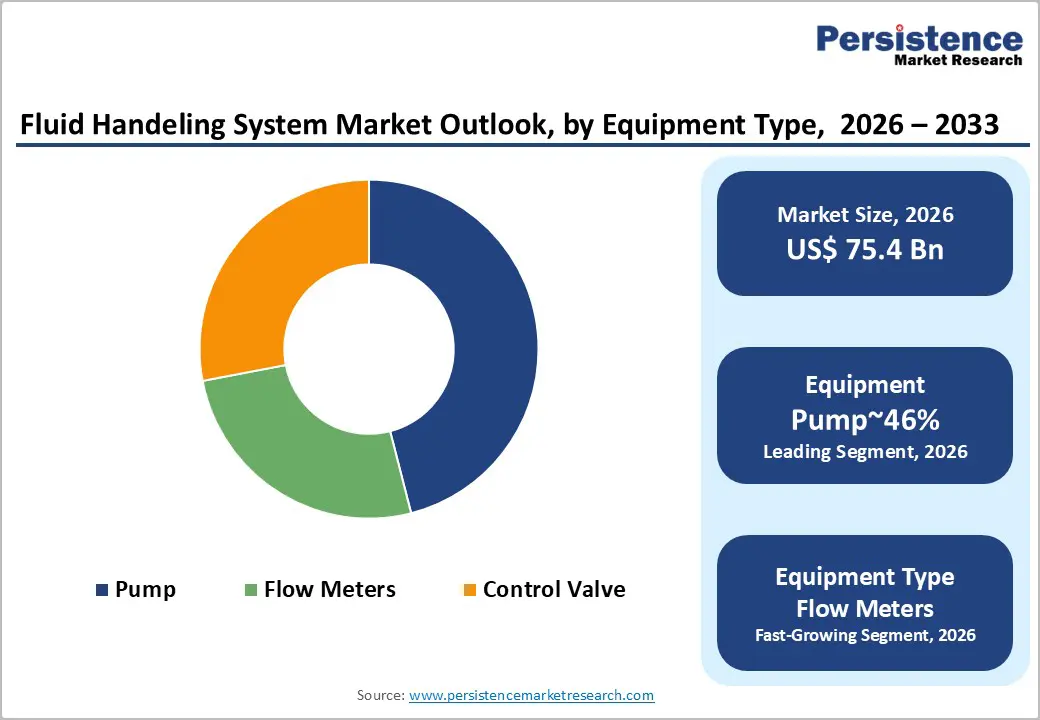

- Leading Equipment Type: Pumps are anticipated to lead, holding around 46% share, as they are fundamental to fluid transport across chemicals, oil and gas, power, and water treatment operations, with sustained demand from process industries and infrastructure projects.

- Leading Pump Type: Centrifugal pumps are projected to remain the leading pump type, holding around 68% share, due to their suitability for high-flow, low-viscosity fluid applications across water treatment, chemicals processing, and general industrial operations.

| Key Insights | Details |

|---|---|

| Fluid Handling System Market Size (2026E) | US$ 75.4 Bn |

| Market Value Forecast (2033F) | US$ 75.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Integration of Industrial IoT (IIoT) and Smart Pumping Systems

The integration of Industrial IoT (IIoT) into fluid handling systems is driving a shift from reactive maintenance to condition-based and predictive models. By embedding connectivity, edge sensing, and digital control into pumps, valves, and meters, process industries gain continuous visibility into flow, pressure, temperature, and fluid characteristics. This digitalization transforms equipment from passive assets to data-generating nodes within plant-wide automation systems. As a result, maintenance strategies are increasingly optimized using real-time diagnostics and failure prediction, enhancing asset utilization, stabilizing throughput, and reducing process variability in critical sectors such as chemicals, oil and gas, water treatment, and power generation.

The rise of smart sensors and connected devices boosts demand for precision measurement and control components, especially advanced flow meters and intelligent control valves. This accelerates the replacement of legacy mechanical meters and drives the retrofitting of brownfield assets with digital interfaces. Smart pumping systems and IIoT integration shift fluid handling from hardware procurement to lifecycle performance optimization, promoting higher attach rates for connected components and service-based revenue models, ultimately enhancing value across the entire supply chain.

Expansion of Chemical Processing Capacity in Emerging Manufacturing Hubs

The relocation and expansion of chemical manufacturing in cost-competitive, consumption-driven regions is a key demand driver for advanced fluid handling systems. As global producers scale polymer, petrochemical, and specialty chemical output for growing domestic and export markets, plants need high-performance pumping, metering, and control systems to manage complex and hazardous fluid streams. Chemical production environments demand strict materials compatibility, sealing integrity, corrosion resistance, and operational reliability, positioning the chemicals sector as the leading end-user for fluid handling equipment due to the continuous-duty nature of processes and the high cost of unplanned downtime or contamination.

From a market perspective, capacity expansions in chemicals and related industries fuel demand for precision positive displacement pumps, automated control valves, and accurate flow measurement systems. As plants seek higher throughput, tighter control, and safer handling of aggressive media, procurement shifts from generic centrifugal pumps to application-specific, engineered systems with enhanced containment and automation. This industrial growth increases system complexity and performance requirements, driving faster replacement cycles for legacy equipment, boosting aftermarket service revenues, and reinforcing the strategic importance of reliability-focused, leak-tight fluid handling solutions in large-scale process operations.

Barrier Analysis – Elevated Maintenance Burden in Corrosive and Abrasive Process Environments

High maintenance intensity in corrosive and abrasive operating conditions represents a structural restraint for the fluid handling systems market, particularly across chemical processing and hydrocarbon value chains. Pumps, valves, seals, and flow control components in these environments are continuously exposed to aggressive chemicals, slurries, particulates, and high-temperature media that accelerate material degradation. The resulting wear mechanisms, including erosion, corrosion fatigue, seal hardening, and cavitation damage, shorten service intervals and increase the frequency of unplanned interventions. For operators, this translates into persistent expenditure on spare parts, consumables, and specialized maintenance labor, eroding the total economic advantage of advanced system upgrades.

Frequent shutdowns for inspection, component replacement, and recalibration impose opportunity costs through lost production, process instability, and compliance risk in tightly regulated process industries. This creates a conservative procurement posture, where asset owners prioritize proven, serviceable configurations over newer, higher-specification systems perceived to carry uncertain durability profiles under harsh duty cycles. Consequently, elevated lifecycle costs dampen upgrade velocity, slow penetration of premium materials and digitally enabled systems in high-corrosion applications, and shift spending toward incremental retrofits and maintenance contracts rather than full-scale system modernization.

Opportunity Analysis – Energy Transition and Decarbonization-Led Infrastructure Upgrades

The accelerating energy transition is driving new demand in the fluid handling sector as energy systems shift toward lower-carbon fuels and alternative energy carriers. The rise of hydrogen value chains and expanded liquefied gas infrastructure requires significant upgrades to legacy pipelines, terminals, storage, and process units. Unlike conventional hydrocarbons, hydrogen and liquefied gases present unique engineering challenges for pumps, valves, seals, and metering systems. Cryogenic service demands resistance to extreme thermal gradients and material embrittlement, while hydrogen service requires handling permeation, leakage, and compatibility issues that surpass the capabilities of many existing assets. This drives the need for high-integrity, purpose-built systems over retrofitting conventional equipment.

From a market perspective, decarbonization initiatives are fueling long-term investments in new builds and brownfield conversions across production, liquefaction, transport, storage, and downstream usage. This expands opportunities beyond traditional oil and gas into hydrogen hubs, gas-to-power systems, and industrial decarbonization. The demand for cryogenic pumps, vacuum-jacketed valves, advanced seals, and precision flow control systems is set to grow, aligned with the structural shift in global energy infrastructure. For instance, Alfa Laval’s 2026 partnership with Ariane-Group to develop a specialized liquid hydrogen pump highlights the emerging market for decarbonized mobility solutions.

Retrofitting and Modernization of Aging Infrastructure

Across developed economies, a large installed base of water, wastewater, and industrial fluid handling assets is approaching the end of its engineered service life, creating a sustained replacement and modernization cycle. Utilities and plant operators face mounting reliability risks, rising leakage losses, and declining energy efficiency from legacy pumps, valves, and control systems that were not designed for current operating profiles or efficiency expectations. Full network replacement is economically and operationally disruptive, which elevates demand for “drop-in” retrofit solutions that can be deployed within existing piping envelopes and footprint constraints.

From a commercial standpoint, retrofit-led modernization aligns with asset life-extension strategies that prioritize incremental efficiency gains, resilience improvements, and compliance with evolving performance benchmarks. Modular retrofit kits, variable-speed drives, high-efficiency impellers, and sensor-enabled control packages allow operators to extract measurable energy and reliability gains while preserving sunk capital in existing infrastructure. Vendors with strong installed-base penetration, standardized retrofit portfolios, and field service capabilities are positioned to capture disproportionate share in mature markets, where procurement cycles increasingly favor low-disruption upgrades over greenfield capacity expansion.

Category-wise Analysis

Equipment Type Insights

Pumps are expected to dominate, accounting for approximately 46% share in 2026, underpinned by their entrenched role as the primary energy-transfer component across municipal water, oil and gas, chemicals, and power generation workflows. Adoption remains anchored by throughput reliability, pressure stability, and lifecycle cost efficiency, with operators prioritizing standardization and scale economics in high-duty environments. Vendors such as Flowserve, Grundfos, and Xylem are expanding portfolios with platforms such as Flowserve’s canned-motor hydrogen pumps and Grundfos’ intelligent circulators to secure long-term service contracts. This combination of mature infrastructure, ecosystem lock-in, and predictable maintenance demand sustains the segment’s leadership within structured industrial deployments.

Flow meters are anticipated to be the fastest-growing segment, driven by rising accuracy requirements and the limitations of periodic manual measurement across energy transition, utilities, and process automation use cases. Growth is being catalyzed by advanced sensing technologies such as Coriolis, ultrasonic, and electromagnetic designs, which materially improve measurement precision, diagnostics, and total cost of ownership. Accelerating adoption is supported by IIoT connectivity, edge analytics, and self-verification features that reduce commissioning friction and downtime for first-time adopters. Companies, including Emerson, Endress+Hauser, and ABB, are scaling platforms such as Rosemount Criolis and Proline smart meters to capture early-cycle demand and embed switching costs.

Pump Type Insights

Centrifugal pumps are projected to dominate, accounting for approximately 68% share, underpinned by their entrenched role as the default choice for high-flow, low-viscosity transfer across municipal water, power generation, desalination, and process industries. Adoption remains anchored by mechanical simplicity, hydraulic efficiency, and favorable lifecycle economics, with operators prioritizing standardization and scalability in high-throughput environments. Ongoing platform evolution, including variable speed drive integration, edge-enabled condition monitoring, and CFD-optimized impeller design, is reinforcing replacement cycles and utilization intensity. The combination of mature infrastructure, interoperability, and predictable demand sustains centrifugal pumps’ leadership across large-scale fluid transport workflows.

Positive displacement pumps are anticipated to be the fastest-growing segment, driven by unmet needs in handling high-viscosity, shear-sensitive, and abrasive fluids across EV battery manufacturing, biopharma processing, and specialty chemicals. Growth is being catalyzed by advances in progressive cavity, diaphragm, and peristaltic architectures that materially improve dosing accuracy, contamination control, and performance under variable pressure. Companies including Graco, IDEX, and NETZSCH are scaling specialized platforms for slurry handling, precision metering, and low-shear transfer to capture early-cycle demand and embed switching costs. As industrial validation and operator familiarity improve, this segment is likely to outpace overall market growth.

Regional Insights

Asia Pacific Fluid Handling System Market Trends

Asia Pacific is set to maintain its dominant position in the fluid handling market, expected to account for around 37% of market share during the forecast period. This leadership is driven by the region's role as the global manufacturing hub and ongoing infrastructure development. The presence of dense clusters of chemical processing, electronics manufacturing, power generation, and municipal water projects in China and India will further solidify demand. Continuous capacity additions in refining, petrochemicals, food processing, and urban utilities will drive the adoption of centrifugal pumps, control valves, and smart flow systems at scale.

Regional production depth also plays a crucial role, with established manufacturers such as Ebara, Kirloskar Brothers, Shanghai Kaiquan, and Shimadzu maintaining strong local manufacturing, service networks, and application-specific portfolios. This enables faster project execution and lower supply chain friction for large infrastructure and industrial clients.

Asia Pacific is also anticipated to be the fastest-growing regional market, fueled by accelerated industrialization, urban expansion, and the localization of global manufacturing in China and India. Multinational suppliers such as Alfa Laval, Flowserve, and Grundfos are expanding their regional manufacturing and engineering capabilities, while domestic players such as Ebara and Kirloskar Brothers are broadening their portfolios to include smart pumping, energy-efficient systems, and predictive maintenance solutions. This combination of localized manufacturing, increasing end-use demand, and strong regional brands is expected to support Asia Pacific’s continued growth.

North America Fluid Handling System Market Trends

North America is positioned as a technology-centric and compliance-driven market for fluid handling systems, anchored by early adoption of smart pumping, advanced flow control, and digitally enabled monitoring across energy, chemicals, water, and process industries. Market demand is shaped by the modernization of legacy infrastructure rather than capacity-led expansion, with procurement priorities centered on reliability, cybersecurity-ready control architectures, and lifecycle efficiency. The regional ecosystem is supported by strong OEM and systems integrator presence, including Flowserve, Xylem, Emerson, ITT, Pentair, Crane, SPX Flow, Parker Hannifin, and Dover, alongside a dense service and aftermarket network that sustains long-term asset performance across municipal utilities, refineries, and large industrial facilities.

The growth profile is underpinned by reinvestment cycles in domestic manufacturing, energy infrastructure, and utility systems, with sustained replacement demand for compliant, high-efficiency pumps, valves, and metering platforms. The U.S. chemicals, refining, and midstream segments continue to prioritize sensorized equipment, predictive maintenance, and remote asset management, reinforcing demand for integrated hardware-software solutions from vendors such as Emerson, Flowserve, and Xylem. Investment flows into municipal water rehabilitation and industrial retrofitting programs support steady equipment turnover, while CCS-oriented upgrades in refineries and heavy industry sustain demand for corrosion-resistant pumps, high-integrity valves, and precision flow control.

Europe Fluid Handling System Market Trends

Europe is a sustainability-driven market for fluid handling systems, defined by advanced engineering practices and a strong focus on the circular economy. The demand is centered on energy-efficient pumps, precision flow control, and durable system architectures, with key sectors including industrial processing, utilities, and energy transition. Germany and the U.K. lead in industrial demand, backed by mature OEM ecosystems and a network of system integrators, EPC firms, and component suppliers. The region's stability is further supported by European manufacturers such as KSB, Sulzer, Verder, Wilo, and Grundfos, whose portfolios emphasize lifecycle efficiency, low-emission operation, and digital performance optimization across various applications.

Europe's market remains resilient, driven by continuous replacement cycles of legacy equipment and tightening performance standards in industrial and public infrastructure. Germany continues to be the hub for high-precision pumps and engineered systems. The region’s sustainability focus is reinforced by investments in recyclable materials, modular designs, and extended product lifecycles. Companies such as KSB, Sulzer, Wilo, Verder, and Grundfos are expanding service networks, digital diagnostics, and refurbishment programs to enhance long-term asset efficiency and support circular economy models across industrial and utility sectors.

Competitive Landscape

The global fluid handling system market is moderately fragmented, with leaders such as Flowserve, Emerson, Alfa Laval, and Xylem shaping technology standards and procurement preferences through broad product portfolios and global service networks. Their ability to supply pumps, valves, and sensing technologies at scale makes them preferred partners for complex industrial and municipal projects. While major OEMs dominate, the market remains competitive, with regional manufacturers and specialized vendors maintaining fragmentation across applications and regions.

Competitive positioning is driven by integrated fluid management solutions, where leaders combine hardware with controls, monitoring, and lifecycle services for reliability and performance. Smaller players differentiate through niche expertise, customized designs, and regional pricing. Industry trends show a shift towards technology differentiation, digital monitoring, and service-led models, signaling consolidation at the equipment level while competition intensifies in aftermarket services and specialized applications.

Key Industry Highlights:

- In December 2025, Alfa Laval launched the FCM LNG Fuel Supply System. As the maritime industry shifts to LNG to meet IMO 2030 emission targets, this product provides the necessary infrastructure for handling fluids at extreme sub-zero temperatures safely.

- In December 2025, Beckman Coulter launched the Biomek i3 benchtop liquid handler. Traditionally, high-precision fluid automation required massive floor space. This compact product allows smaller labs (SMEs) to compete in genomics, tapping into a previously unserved market segment.

- In January 2025, Tecan Unveiled Veya, an AI-enhanced liquid handling platform. Revolutionizes lab precision by integrating AI into the workflow, it moves fluid handling from "pre-programmed" to "adaptive," reducing human error in complex multiomics research, a high-margin sector.

Companies Covered in Fluid Handling System Market

- Alfa Laval AB

- Flowserve Corporation

- Graco Inc.

- Ingersoll Rand Inc.

- Xylem Inc.

- Grundfos Holding A/S

- Crane Co.

- Parker Hannifin Corporation

- IDEX Corporation

- Emerson Electric Co.

- Sulzer Ltd.

- KSB SE & Co. KGaA

- Dover Corporation

- ITT Inc.

- Endress+Hauser Group

- SPX FLOW, Inc.

- Ebara Corporation

Frequently Asked Questions

The global fluid handling system market is projected to be valued at US$75.4 billion in 2026 and is expected to reach US$113.2 billion by 2033, driven by rising demand from chemical processing, water treatment, and the integration of smart, energy-efficient systems.

IIoT integration turns pumps, valves, and meters into connected assets, enabling predictive maintenance and precise control. This shift from reactive to condition-based management reduces downtime, boosts efficiency, and drives demand for advanced, digitally-enabled components in process industries.

The fluid handling system market is forecast to grow at a CAGR of 6.0% from 2026 to 2033, reflecting sustained investment in industrial automation, capacity expansions, and infrastructure modernization.

Asia Pacific is the leading regional market, accounting for approximately 37% share, supported by large-scale industrialization, massive infrastructure investments, and its role as the global manufacturing hub for chemicals, power, and water treatment sectors.

The fluid handling system market is moderately fragmented, with global leaders such as Flowserve, Emerson, Alfa Laval, and Xylem dominating. These companies compete with comprehensive portfolios and integrated solutions, while specialized and regional players such as Grundfos, KSB, and Sulzer hold strong positions in niche applications and specific regions.