- Bulk Chemicals

- Drilling Fluids Market

Drilling Fluids Market Size, Share, and Growth Forecast 2025 - 2032

Drilling Fluids Market by Product Type (Water-based, Oil-based, Synthetic-based, Others), Application (Onshore, Offshore), and Regional Analysis for 2025 - 2032

Drilling Fluids Market Share and Trends Analysis

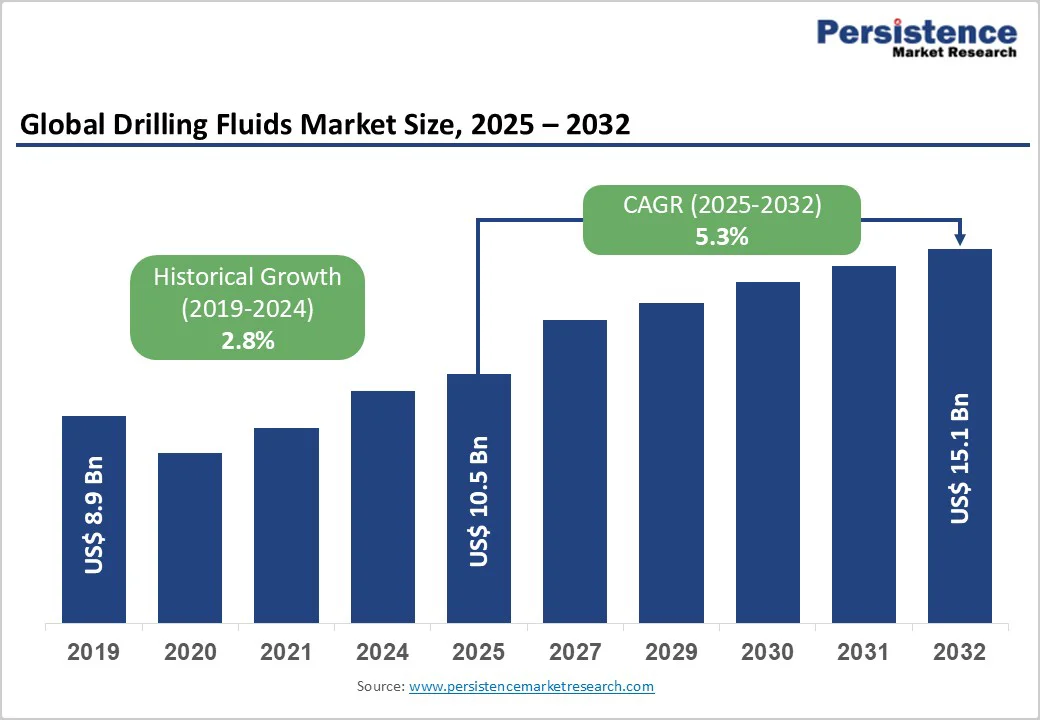

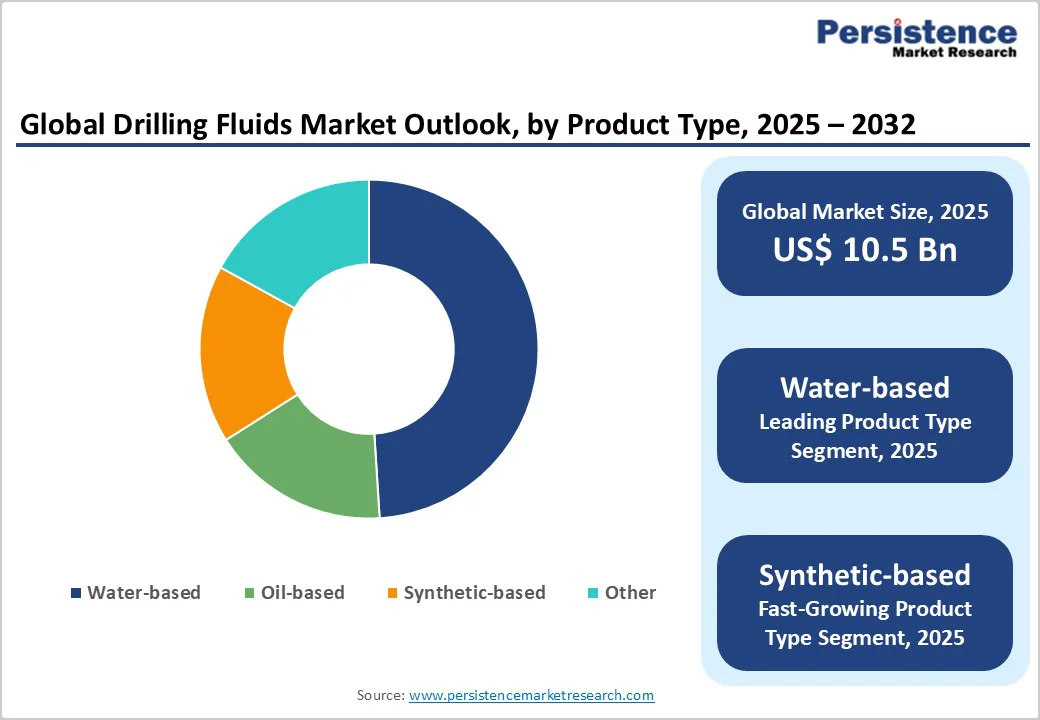

The global drilling fluids market size is likely to be valued at US$ 10.5 billion in 2025, and is projected to reach US$ 15.1 billion by 2032, growing at a CAGR of 5.3% during the forecast period 2025 - 2032.

Accelerating deepwater exploration activities in the Gulf of Mexico, North Sea, Persian Gulf, and South China Sea, where complex drilling operations demand advanced fluid systems, are primarily driving market expansion. Supporting this is the surge in unconventional resource extraction that has boosted drilling activities, as evidenced by increased rig counts and production efficiencies reported by energy agencies.

The U.S. Energy Information Administration (EIA) forecasts U.S. crude oil production to rise to 13.5 million barrels per day in 2025, up from 13.2 million barrels per day in 2024, fueled by increased rig counts and investments in shale plays.

Key Industry Highlights

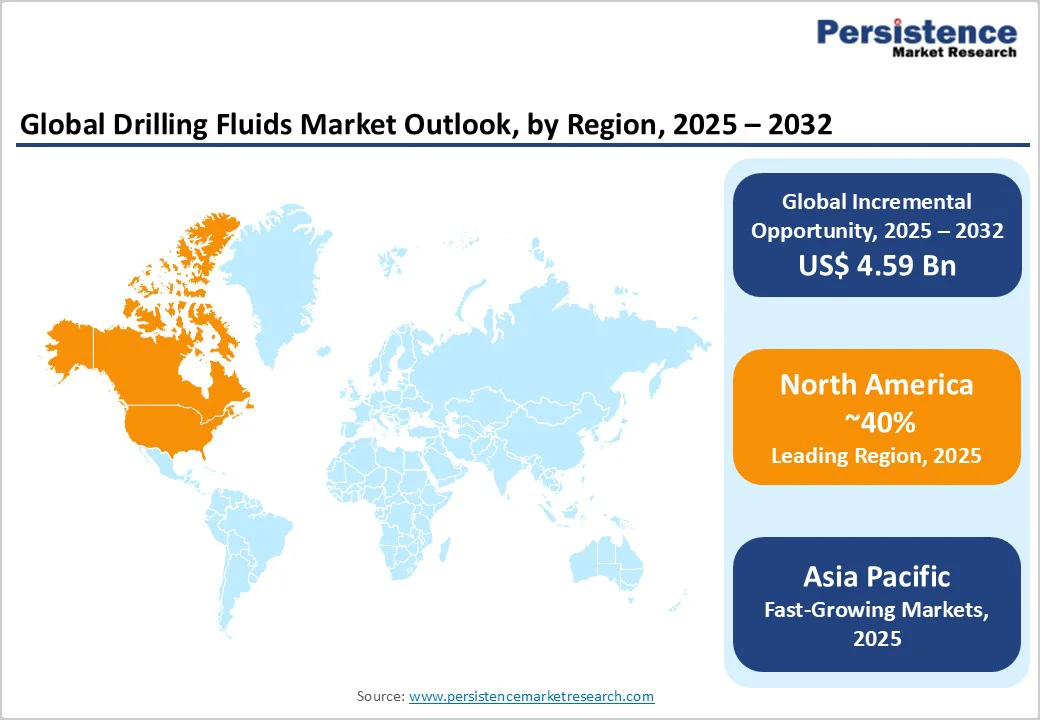

- Regional Leader: North America leads the market with a 40% share, due to U.S. shale dominance and efficient onshore drilling operations.

- Fastest-growing Regional Market: Asia Pacific is set to be the fastest-growing regional market, propelled by booming energy exploration activities of India and China.

- Leading Application: Onshore drilling dominates applications, capturing 60% of the revenue share in 2025, fueled by unconventional resource extraction and accelerated adoption in shale gas recovery.

- Fastest-growing Product Type: Water-based fluids are likely to be the fastest-growing segment, due to their cost-effectiveness and eco-compatibility in routine drilling.

- Growth Opportunities: Deepwater exploration offers a key opportunity, unlocking vast reserves with specialized fluids, supported by technological advancements and policy incentives for sustainable offshore ventures.

| Key Insights | Details |

|---|---|

| Drilling Fluids Market Size (2025E) | US$ 10.5 Bn |

| Market Value Forecast (2032F) | US$ 15.1 Bn |

| Projected Growth CAGR (2025 - 2032) | 5.3% |

| Historical Market Growth (2019 - 2024) | 2.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Global Energy Demand and Exploration Activities

The drilling fluids market is expanding steadily, driven by soaring energy demand worldwide, fueled by industrialization and population growth. Increasing drilling activity in ultra-deep waters and advanced reservoir conditions necessitates specialized fluids that maintain stability under extreme pressure and temperature.

Innovations such as nanotechnology additives improve fluid performance, reduce operational downtime, and lower costs, supporting extraction from challenging formations. The U.S. onshore rig count growth and global upstream investments further reinforce demand for advanced drilling fluids.

Technological advancements such as horizontal drilling and hydraulic fracturing increase the need for versatile fluids that guarantee operational efficiency and wellbore stability. High-pressure, high-temperature scenarios require robust formulations to minimize non-productive time.

As exploration extends into previously uneconomical reserves, smart fluid management and digital optimization systems become critical for project success. This dynamic market is essential within the broader oil and gas industry’s efforts to meet growing global energy requirements sustainably and cost-effectively.

Stringent Environmental Regulations

Regulatory frameworks significantly impact the drilling fluids market growth by imposing strict environmental compliance requirements, such as the U.S. Environmental Protection Agency (EPA)'s toxicity limits under the 40 CFR 435.15 standards, which demand water-based fluids meet stringent 96-hour LC50 thresholds.

These regulations prohibit or restrict the use of oil-based fluids in sensitive offshore areas, driving operators to adopt costlier, eco-friendly alternatives. While essential for protecting marine and groundwater ecosystems, these rules increase operational costs, delay project timelines, and complicate fluid supply chains, thereby challenging market growth and fluid innovation.

Furthermore, fluctuating crude oil prices directly influence drilling activity and budget allocations, affecting drilling fluid demand. The U.S. EIA forecasts a decline in oil prices to around US$ 62 per barrel in late 2025, leading to reduced rig counts and cautious exploration spending, especially in marginal fields.

Geopolitical instability and global supply imbalances further exacerbate market uncertainty, hindering investment and slowing the pace of technological advancement and market expansion. Despite these challenges, ongoing innovation in environmentally compliant drilling fluids and monitoring technologies offers opportunities to sustain market viability and efficiency.

Expansion in Deepwater and Ultra-Deepwater Exploration

The deepwater and ultra-deepwater drilling fluids space is rapidly expanding as energy companies focus on exploring reserves located beyond 15,000 feet underwater, requiring fluids that endure extreme pressures and temperatures.

The U.S. Gulf of Mexico is a key growth region, with production expected to increase significantly in 2025, boosted by the deployment of advanced drilling technologies that use synthetic-based fluids for enhanced thermal stability. Innovations such as subsea tiebacks and 3D seismic imaging have unlocked vast offshore hydrocarbons, augmenting the demand for high-performance fluids that support extended reach and complex reservoir conditions.

Simultaneously, growing regulatory emphasis on eco-friendly and biodegradable drilling fluids creates new opportunities amid rising sustainability mandates. Industry initiatives led by organizations such as the International Association of Oil & Gas Producers (IOGP) have been encouraging green alternatives that meet environmental and operational standards.

AI-powered fluid formulations and advanced products, such as high-performance mud motors, are improving efficiency in harsh environments. These technological advancements enable companies to tap into emerging offshore markets, reduce environmental impact, and gain competitive advantage by aligning with evolving green regulations and energy demand trends.

Category-wise Analysis

Product Type Insights

Water-based fluids dominate the product type category, commanding approximately 49% of the drilling fluids market revenue share in 2025. Their leadership originates from inherent cost-effectiveness and environmental compatibility, making them ideal for a wide array of drilling scenarios, especially in onshore shale operations where simplicity and low toxicity are paramount. Their lower toxicity and biodegradability aligns with EPA standards that mandate minimal ecological impact, as seen in their widespread adoption across onshore projects, globally.

Industry research statistics indicate water-based systems reduce operational costs by 20-30% compared to alternatives, making them ideal for shallow wells where shale stability is less critical. This dominance is further reinforced by regulatory preferences in regions such as North America, where EPA guidelines favor less hazardous options, ensuring their widening deployment in routine and extended-reach drilling.

Application Insights

Onshore applications command the leading position, capturing about 70% revenue share in 2025. This dominance mainly attributable to the proliferation of unconventional resource extraction, particularly in shale-rich basins. The EIA reports onshore rigs were employed for most of the oil & gas drilling operations in the U.S. in 2024, fueled by shale discovery that prioritizes fluids for horizontal drilling efficiency.

Onshore drilling is also being supported by the reduced logistics costs and favorable regulations, enabling faster deployment in regions such as the Permian Basin, where onshore production accounts for nearly three-fifths of U.S. crude. This focus on cost-optimized, high-volume drilling in mature regions solidifies the position of the onshore segment, with its prospects additionally bolstered by infrastructure advantages that minimize deployment challenges and enhance recovery economics.

Regional Insights

North America Drilling Fluids Market Trends

North America spearheads with an estimated 40% of the drilling fluids market share, backed by U.S. dominance in shale production, wherein innovative fluid technologies drive efficiency in the Permian and Bakken formations. The EIA reports a steady rise in crude output, fueled by multi-well pad drilling that demands versatile, high-performance fluids to manage complex hydraulics.

Regulatory frameworks from the Bureau of Ocean Energy Management (BOEM) enforce eco-standards for offshore ops, promoting synthetic-based variants that reduce environmental risks in the Gulf of Mexico. This ecosystem fosters R&D, with companies advancing high pressure, high temperature (HPHT) fluids to tackle deep shale challenges, ensuring sustained leadership amid energy independence goals.

Regional innovation thrives via collaborations between operators and fluid specialists, optimizing formulations for reduced water usage and enhanced lubricity. Recent BOEM assessments highlight how these advancements have cut drilling times, strengthening the region's role in global supply while integrating with the associated markets for seamless subsea integrations.

The blend of technological prowess and policy support positions North America as a context-setter for resilient, low-impact drilling practices.

Europe Drilling Fluids Market Trends

In Europe, the drilling fluids market expansion is contingent on the energy exploration projects around the North Sea, led by Germany, the U.K., and France, where harmonized regulations prioritize sustainable practices.

The North Sea Transition Authority (NSTA) of the U.K. notes a decline in well numbers but improved success rates, with only a limited number of development wells completed in 2020 amid HPHT challenges. Performance in U.K. fields relies on synthetic-based fluids for deepwater, aligning with European Union (EU) directives on marine pollution reduction.

Regulatory harmonization via the European Chemicals Agency pushes low-toxicity water-based systems, cutting environmental risks in mature basins. In Germany and France, trends favor digital monitoring to optimize fluids, supporting a rebound in Central North Sea drilling.

Asia Pacific Drilling Fluids Market Trends

The Asia Pacific drilling fluids market is anticipated to surge through 2032, leveraging manufacturing advantages in India, China, and ASEAN nations for cost-competitive production. China's state-backed exploration in the Bohai Bay has ramped up onshore shale activities, demanding robust fluids for tight formations.

National statistics show drilling depths increasing by 10% annually. In India, the push for energy self-sufficiency, under initiatives such as the Hydrocarbon Exploration and Licensing Policy, has boosted fluid needs for onshore and offshore drilling projects, with a special emphasis on affordable water-based options.

ASEAN dynamics highlight offshore expansions, where synthetic fluids handle tropical geologies efficiently. Manufacturing hubs in China and India enable rapid scaling, intertwining with the Wellhead Components Market for integrated solutions amid rising urbanization-driven energy demand.

Competitive Landscape

The global drilling fluids market landscape exhibits a consolidated structure, dominated by a handful of multinational giants through extensive R&D and global footprints. Leaders pursue expansion via strategic mergers and joint ventures, targeting emerging deepwater segments, while channeling investments into sustainable formulations to counter regulations.

Key differentiators include proprietary additives for HPHT stability and digital monitoring integrations, enhancing client efficiencies. Emerging models emphasize service-integrated solutions, such as fluid management contracts, alongside trends in bio-based fluids for eco-compliance, fostering innovation amid consolidation.

Key Industry Developments

- In November 2025, Condor Energies successfully drilled its first horizontal well in Uzbekistan’s Andakli field, reaching a total depth of 3,775 meters with the longest lateral drilled to date at 1,007 meters. The well has started initial gas flowback and is expected to enter production in December. Encouraged by promising reservoir quality and strong flows from related wells, Condor plans to drill up to 12 more wells in 2026 to expand production.

- In November 2025, Drilling Specialties launched NanoSlide™, an advanced drilling fluid lubricant designed to reduce wear and friction on drill pipes under extreme downhole conditions. The lubricant uses a blend of micronized graphene, proprietary additives, and CPChem’s Synfluid® PAO to create a protective tribofilm, enhancing drilling efficiency and equipment longevity. Field trials in the Bakken Formation demonstrated significant reductions in pipe wear and drill time, positioning NanoSlide™ as a cost-effective innovation that improves operational performance.

- In April 2025, ADNOC Drilling Company PJSC secured a US$ 1.63 billion, five-year integrated drilling services contract from ADNOC Offshore, covering directional drilling, drilling fluids, cementing, and technical support for offshore wells. The deal strengthens ADNOC Drilling’s position as a regional energy services leader and adds revenue stability, supporting financial targets through 2025 and 2026. ADNOC Drilling also plans to expand regionally and enhance efficiency by deploying advanced, AI-enabled rigs.

Companies Covered in Drilling Fluids Market

- Schlumberger Ltd.

- Halliburton Inc.

- Newpark Resources, Inc.

- Baker Hughes

- TETRA Technologies, Inc.

- CES Energy Solutions Corp.

- NOV Inc.

- Imdex Limited

- Weatherford

- Chevron Phillips Chemical Company LLC

- Scomi Group Bhd

- Flotek Industries, Inc.

- China Oilfield Services Limited

Frequently Asked Questions

The global drilling fluids market is projected to reach US$ 10.5 billion in 2025.

Rising global energy needs and technological advancements in drilling, such as HPHT systems, fuel demand, with unconventional resources such as shale boosting fluid requirements for efficient operations.

The market is poised to witness a CAGR of 5.3% from 2025 to 2032.

Deepwater exploration offers to open up new and attractive opportunities, as these operations necessitate the use of specialized eco-friendly fluids that can enable access to untapped reserves as well as align with sustainable energy transition goals.

Prominent players in the market include Schlumberger Ltd., Halliburton Inc., and Baker Hughes.