- Bulk Chemicals

- Deicing Fluid Market

Deicing Fluid Market Size, Share, and Growth Forecast, 2026-2033

Deicing Fluid Market by Fluid Type (Glycol-based, Acetate-based, Formate & Eco Blends, Others), Application (Aviation, Ground Transportation, Industrial & Infrastructure), End‑User (Airports & Airlines, Government, Industrial & Facility Management), and Regional Analysis for 2026-2033

Deicing Fluid Market Share and Trends Analysis

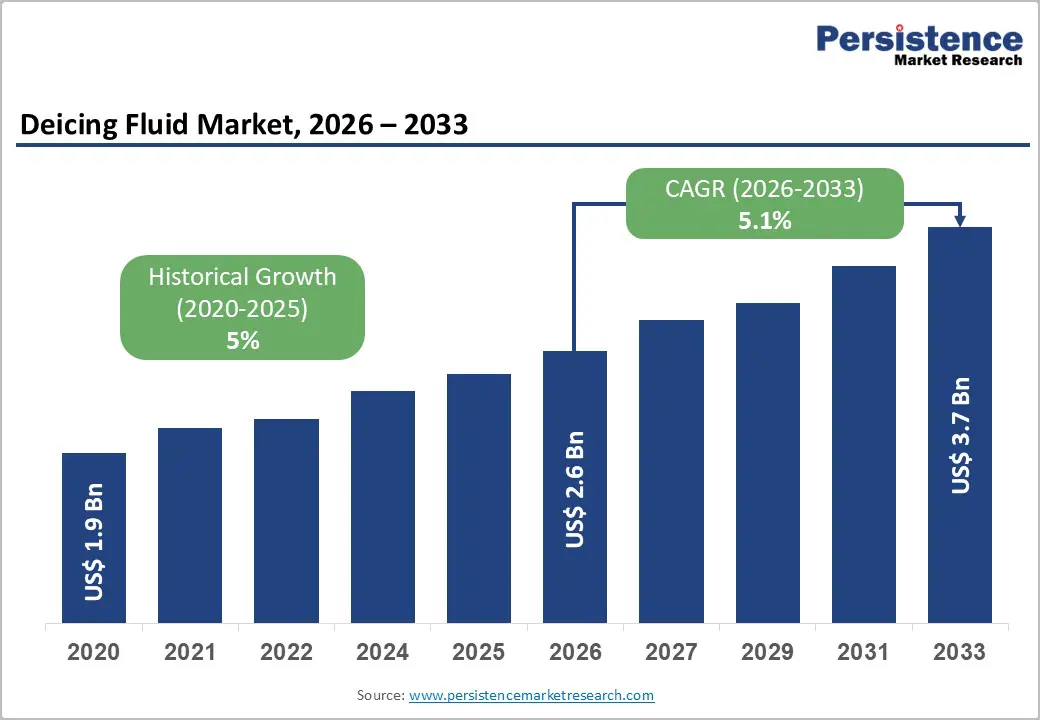

The global deicing fluid market size is likely to be valued at US$ 2.6 billion in 2026, and is projected to reach US$ 3.7 billion by 2033, growing at a CAGR of 5.1% during the forecast period 2026–2033. This growth is underpinned by expanding aviation activities, stringent safety standards for winter operations, and increasing investment in surface transportation safety infrastructure. Demand is bolstered by regulatory mandates that require extensive use of deicing fluids for aircraft and runway safety, as well as heightened public and private spending on road and industrial deicing solutions. Market demand exhibits seasonal sensitivity, with peak consumption during winter months in cold-weather regions, emphasizing the need for optimally blended fluid formulations that balance performance and environmental compliance.

Key Industry Developments

- Dominant Fluid Types: Glycol-based fluids are projected to command around 52% market share in 2026, while eco-blends are expected to register the fastest during 2026–2033, driven by environmental regulations and sustainability mandates.

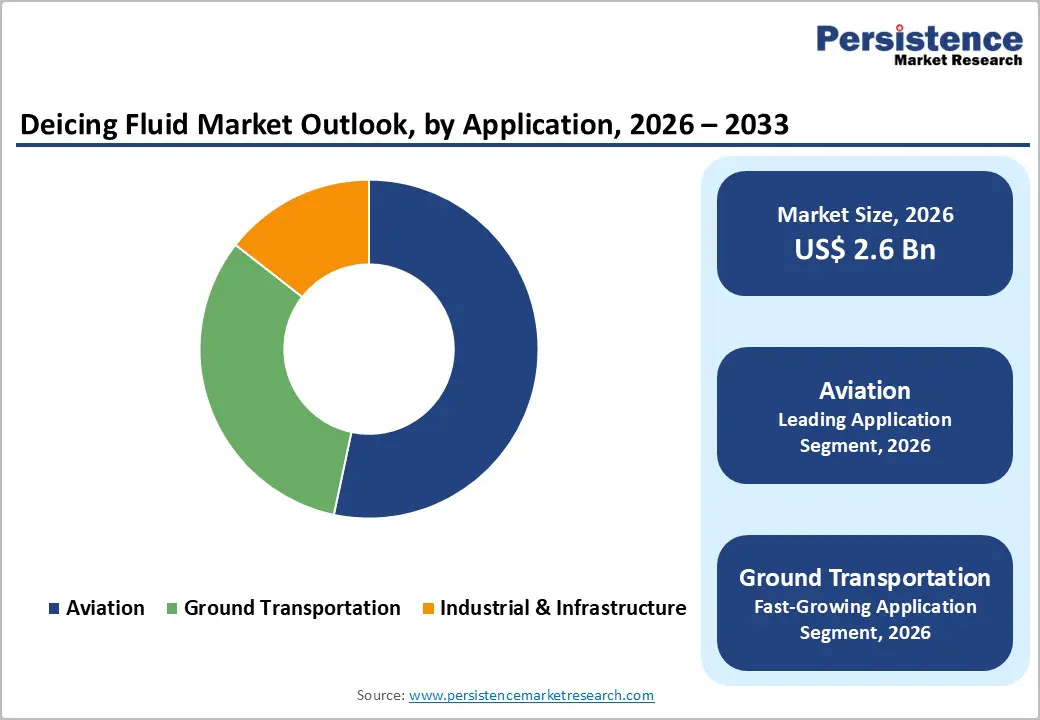

- Leading Applications: Aviation deicing is anticipated to lead with approximately 48% revenue share in 2026, while ground transportation deicing is likely to grow the fastest at a CAGR of 5.8%, owing to strong winter road safety initiatives.

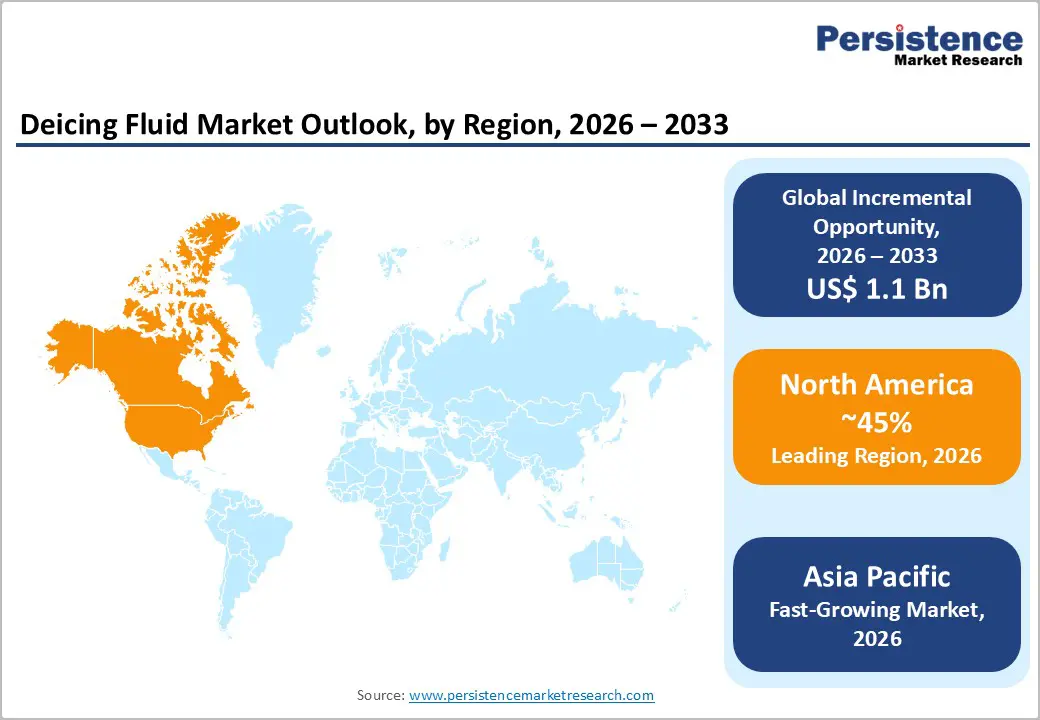

- Regional Leadership: North America is poised to dominate with an estimated 45% share in 2026, while Asia Pacific is expected to exhibit the fastest growth at a CAGR of 7.1%, benefiting from rapid airport expansion and industrial infrastructure investments.

- Industry Trends: Market expansion is driven by eco-friendly formulation adoption, deployment of digital and IoT-enabled deicing technologies, and regional capacity investments.

| Key Insights | Details |

|---|---|

| Deicing Fluid Market Size (2026E) | US$ 2.6 Bn |

| Market Value Forecast (2033F) | US$ 3.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of Global Air Travel and Evolving Safety Regulations

The rapid expansion of global air travel continues to directly boost demand for deicing fluids, particularly where sustained sub-zero conditions and heavy snowfall are recurrent. Aircraft deicing remains indispensable for flight safety, with regulatory authorities enforcing vigorous protocols to prevent ice accretion that compromises lift and control. Recent updates to Holdover Time (HOT) guidance by the U.S. Federal Aviation Administration (FAA) for the 2025–2026 winter season included revised fluid-specific tables, reflecting regulatory alignment with evolving deicing chemistries. The FAA also expanded winter weather operational support through funding for deicing infrastructure, reinforcing industry responsiveness to seasonal safety requirements.

This regulatory momentum correlates with aircraft deicing accounting for nearly half of total fluid consumption worldwide. As commercial flights increase, airports and airlines have invested in dedicated deicing pads, automated spray systems, and storage solutions to maintain operational efficiency. At major aviation hubs in North America and Europe, fluid use aligns tightly with seasonal flight schedules, underscoring the direct relationship between air traffic growth, safety compliance, and expanded fluid demand. These developments exemplify how regulatory evolution and capacity enhancements together drive market expansion in aviation deicing applications.

Government Winter Infrastructure Investment and Eco-Friendly Formulation Adoption

Public infrastructure investment in winter safety continues to be a key market driver, significantly benefiting ground transportation and industrial deicing fluid segments. Governments and municipal agencies are allocating increasing budgets for winter maintenance, enhanced roadway safety, and economic risk mitigation through strategic deployment of deicing solutions. Traditional chloride-based salts are often supplemented or replaced by potassium acetate and formate blends, responding to both safety and environmental considerations. A recent environmental analysis published in Eco-Environment & Health underscored the ecological impact of road deicer runoff, highlighting soil and water quality risks that reinforce the need for lower-toxicity chemistries.

Simultaneously, innovation in eco-friendly formulations is reshaping market dynamics. Emerging solutions, including bio-based glycol alternatives, calcium magnesium acetate blends, and lower-toxicity eco blends, are gaining adoption as regulatory frameworks increasingly favor products that reduce chemical runoff and environmental exposure. This trend was spotlighted in a Feb 2026 news report on winter deicing innovation, which discussed municipal interest in advanced formulations to reduce corrosion and environmental damage. Strategic R&D partnerships and expanded product portfolios now serve broader operational needs across aviation, surface transport, and industrial sectors.

Environmental and Regulatory Constraints

The use of traditional glycol-based deicing fluids continues to raise environmental concerns, particularly regarding water and soil contamination. Glycol runoff increases biochemical oxygen demand (BOD) in local water bodies, harming aquatic life and necessitating expensive recovery and treatment systems at airports, roads, and industrial sites. Stricter environmental regulations now mandate compliance with effluent limits, adding operational and capital costs for entities handling deicing operations.

These regulatory pressures were highlighted in early 2026 when the Minnesota Pollution Control Agency (MPCA) reported the completion of 78 enforcement cases covering wastewater and chemical runoff violations. This example reflects the broader trend of enhanced oversight across municipal and industrial operations, illustrating how regulatory compliance costs and environmental constraints continue to slow adoption of some high-performance deicing chemistries, especially in sensitive regions. Compliance planning, monitoring, and reporting requirements further increase administrative burdens and necessitate specialized operational protocols.

Seasonal Demand Volatility

The demand for deicing fluids is subject to seasonal variability, peaking in winter months and dropping sharply during warmer periods. This cyclical pattern causes revenue fluctuations, complicates supply chain and inventory management, and challenges accurate production planning. Manufacturers and distributors must balance peak-season availability with off-season storage, often incurring higher carrying costs or temporary underutilization of production facilities.

Recent winter disruptions further emphasize this volatility. In February 2026, severe snowstorms led to thousands of flight cancellations across major U.S. airports, demonstrating how unpredictable winter weather affects fluid consumption and airport operations. Such seasonal uncertainty creates structural constraints for consistent market growth, requiring agile planning and risk mitigation strategies by suppliers and end users. Extreme winter events may trigger sudden spikes in demand, straining logistics and regional supply chains during peak periods.

Expansion in Emerging Cold Climate Markets

Emerging cold climate regions, particularly in Asia Pacific, including China, and parts of India, are witnessing substantial investment in airport and transportation infrastructure, creating strong growth avenues for deicing solutions. Rapid expansion of commercial flight networks and airport capacities in Northeast Asia and South Asia is increasing operational demand for modern winter support systems. Major airport expansion projects, including a new passenger terminal with dedicated aircraft stands and deicing space at Budapest Airport, underscore the scale of infrastructure investment underway globally.

Simultaneously, persistent extreme winter weather events continue to highlight the strategic importance of reliable cold climate operations. The 2025–26 European windstorm and heavy snowfall season resulted in extensive travel disruptions and infrastructure impacts across Northern and Western Europe, reinforcing the need for enhanced winter preparedness at critical transport nodes. These global climate pressures, paired with long-term infrastructure development, position cold climate and emerging markets as key drivers of sustainable expansion for deicing fluid demand through the forecast period.

Technological Innovation and Industrial Applications

Technological integration and advanced solutions are reshaping how deicing functions are delivered, offering productivity, cost, and environmental benefits. Airports and transportation authorities are increasingly piloting hybrid and electric snow and ice removal technologies. For example, Kodiak Technologies’ collaboration with Gerald R. Ford International Airport to test hybrid-electric heavy-duty snow and ice removal equipment in 2026 directly supports the shift toward cleaner, more efficient winter operations.

In addition to aviation, industrial and infrastructure applications are gaining traction as sectors broaden the use of deicing fluids beyond traditional routes. Utility grids, critical industrial facilities, and cold storage environments face severe weather stresses, as evidenced by widespread ice accumulation and infrastructure impact during early 2026 winter storms in North America. Specialized fluid formulations with low corrosion and low environmental impact are gaining preference in these contexts, supporting industrial freeze protection, asset continuity, and risk mitigation strategies. This fusion of innovation and diversified end-use demand reinforces long-term opportunity potential in both core and adjacent markets.

Category-wise Analysis

Fluid Type Insights

Glycol-based deicing fluids are expected to hold the largest market share at around 52% in 2026, due to their proven performance in aviation and ground transportation. Propylene glycol blends are widely adopted for their effective freezing point depression and lower toxicity, ensuring compliance with safety and operational protocols at airports and municipal winter programs. These fluids are extensively stocked for peak winter conditions, especially in cold-climate regions where reliability affects flight schedules and surface safety. A practical example is the deployment of 51,000 gallons of liquid and 174,000 pounds of pellets at Houston’s Bush Intercontinental and Hobby airports in January 2026, highlighting large-scale operational readiness and reinforcing glycol fluids’ market dominance under stringent regulatory and performance demands.

Eco-blend deicing fluids are projected to be the fastest-growing segment with an estimated CAGR of 6.2% through 2033, driven by rising environmental regulations and demand for sustainable solutions. These fluids are increasingly used for runway, roadway, and sensitive infrastructure applications in Europe and North America, where low-chloride and low COD products are incentivized. Adoption is supported by corporate sustainability initiatives and government policies. For instance, Spain’s 2025–2026 winter road maintenance campaign deployed over 254,000 tons of deicing material, reflecting operational scale where eco-friendly blends are gaining traction. Continued technological improvements and regulatory incentives position these blends as a high-growth alternative to traditional glycol-based fluids.

Application Insights

Aviation is likely to capture roughly 48% of the deicing fluid market revenue share in 2026, on account of strict safety requirements and large fluid volumes per aircraft. Deicing ensures operational safety and schedule adherence, particularly at cold-climate hubs. Airports invest in automated spray systems, dedicated deicing pads, and storage to maintain peak winter readiness. During the January 23–27, 2026 North American winter storm, over 9,000 flight cancellations occurred, with extensive pre-treatment operations highlighting aviation’s critical demand for deicing fluids. Regulatory oversight and seasonal operational needs continue to reinforce aviation as the dominant fluid consumer globally.

Ground transportation, including roads and rail, is projected to be the fastest-growing application with an estimated CAGR of 5.8% through 2033, driven by infrastructure spending, safety regulations, and wider adoption of advanced deicing solutions. Municipal and state agencies deploy pre-treatment programs, salt, and brine to reduce winter hazards. In February 2026, Pennsylvania’s Department of Transportation mobilized 60,000 tons of salt and 170 trucks ahead of a major blizzard, exemplifying large-scale operational reliance on deicing for safe roadways. The segment’s growth is reinforced by rising winter maintenance budgets, regulatory focus on commuter safety, and increased awareness of infrastructure resilience.

Regional Insights

North America Deicing Fluid Market Trends

North America is expected to capture an approximate 45% of the deicing fluid market share in 2026, supported by harsh winter conditions across the United States and Canada and being to some of the world’s busiest aviation networks. The region’s demand is rooted in federal safety requirements and municipal winter maintenance programs that prioritize fluid supply and runway readiness. For example, the Airports Council International – North America highlighted proactive snowstorm preparations in January 2026, with airports stage-setting snow removal and deicing equipment and coordinating with airlines and federal partners to maintain safe operations in challenging weather.

Winter weather impacts are further evidenced by extensive system-wide disruptions during the 2025–26 North American winter, which saw major storms through January and February 2026 that grounded flights, stressed airport weather response systems, and intensified roadway deicing programs across multiple states and provinces. These events underscore why airports and transportation authorities invest in centralized deicing pads, automated application infrastructure, and fluid recovery systems to maintain operational efficiency. Regulatory frameworks from the U.S. FAA and the Environmental Protection Agency (EPA) continue to shape procurement and environmental compliance trends, reinforcing North America’s dominant regional position and driving modernization investments in deicing technology and infrastructure.

Europe Deicing Fluid Market Trends

Europe represents the second-largest market for deicing fluids, with Germany, the U.K., France, and Spain among key contributors, driven by frequent severe winter weather and substantial aviation and ground transport activities. Operational pressures in early 2026 illustrate this: heavy snowfall and freezing conditions across the continent led to significant flight disruptions at major hubs such as Amsterdam Schiphol, Paris Charles de Gaulle, and Heathrow, in some instances forcing cancellation of thousands of flights over several days as crews struggled to clear runways and de-ice aircraft amid intense weather.

In one notable case, airline warnings and operational bottlenecks due to deicing fluid shortages at Schiphol highlighted the operational complexities and scale of European winter demand, with carriers seeking additional supplies from regional partners to maintain service levels. Harmonized regulatory standards across the EU further encourage coordinated procurement and sustainability criteria for fluids used in aviation and ground operations. Infrastructure investments and public winter preparedness programs across high-traffic corridors ensure ongoing fluid usage for runways, road networks, and cross-border transport, reinforcing the region’s mature market status while sustaining long-term growth amid evolving environmental and safety mandates.

Asia Pacific Deicing Fluid Market Trends

Asia Pacific stands out as the fastest-growing market for deicing fluids, with an estimated CAGR of 6.1% during the 2026-2033 forecast period, propelled by expanding aviation networks, rapid transportation modernization, and increasing winter weather preparedness in China, Japan, India, and parts of ASEAN. Regional aviation activity experienced notable operational strain in early 2026, with widespread flight delays and cancellations reported across key hubs including Tokyo Haneda, Ho Chi Minh City, and other major airports, reflecting both growth in air travel and emerging winter weather vulnerability in diverse climate zones.

In East Asia, winter flight disruptions along Japan–China corridors exposed structural challenges in balancing peak operations with weather impacts, leading to cascading schedule delays and highlighting the need for robust winter operational strategies, including effective deicing and ground handling systems. Investments in airport modernization, including automated deicing systems, optimized logistics, and enhanced infrastructure, are increasing operational efficiency and creating new opportunities for fluid suppliers and technology partners. Local manufacturing expansion and cross-regional procurement partnerships with global suppliers further support scaling deicing solutions, positioning Asia Pacific as the key growth engine in the global market.

Competitive Landscape

The global deicing fluid market structure is moderately consolidated, with leading players such as Kost Chemical, Ecolab, Clariant, BASF, and Solvay controlling a significant portion of revenue, estimated at over 50% of global market share in 2026. These established companies leverage long-standing relationships with airports, municipalities, and industrial clients, while maintaining compliance with stringent environmental and aviation safety regulations. Investment in R&D enables them to develop high-performance, low-toxicity, and eco-friendly formulations, as well as improve application technologies such as automated spray systems and closed-loop fluid recovery.

Regional and niche competitors, including Aviation Chemicals, Cryotech, and SnowEx, focus on specialized geographic markets or unique formulations, targeting eco blends, formate-based solutions, and industrial freeze protection applications. Market entry barriers, such as regulatory compliance, complex fluid recovery infrastructure, and environmental permitting, limit new entrants. However, digitalization and smart deicing technologies are enabling partnerships with IoT and AI-driven solution providers. Market consolidation is expected to rise gradually, with leading companies acquiring regional players to expand their geographic footprint and product portfolio, while innovation partnerships continue to drive growth in sustainable and efficient deicing solutions.

Key Industry Developments

- In January 2026, Amcor introduced a portfolio of rigid and flexible packaging solutions for de-icing products, including containers, jerry cans, trigger spray bottles, and moisture-resistant bags designed for safe storage, handling, and transport in harsh conditions. The solutions incorporate recyclable materials and post-consumer recycled (PCR) plastics to support sustainability goals across the de-icing supply chain.

- In December 2025, researchers at the University of York developed supramolecular gel additives that significantly enhance aircraft anti-icing fluids, allowing treated surfaces to remain ice-free for more than twice as long as conventional formulations. The gels self-assemble from low-cost compounds and improve the fluid’s “holdover time,” while breaking down naturally during aircraft takeoff to maintain aerodynamic performance.

- In July 2025, Ice Shield partnered with Boeing in a strategic master distribution agreement to supply deicing solutions across Boeing’s business and general aviation networks. This deal expanded global distribution reach and enhanced logistical capabilities for deicing products, strengthening market access and operational reliability.

Companies Covered in Deicing Fluid Market

- Dow Chemical Company

- Clariant AG

- BASF SE

- Kilfrost Group PLC

- E. I. du Pont de Nemours

- Cargill, Incorporated

- Univar Inc.

- Chemco Inc.

- Proviron

Frequently Asked Questions

The global deicing fluid market is projected to reach US$ 2.6 billion in 2026.

Surging aviation traffic, winter road safety spending, and regulatory demand for environmentally compliant fluids are driving market growth.

The market is poised to witness a CAGR of 5.1% from 2026 to 2033.

Expansion in emerging cold-climate regions and adoption of eco-friendly and digital deicing technologies offer major opportunities.

Kost Chemical, Ecolab, Clariant, BASF, and Solvay are among the key market players.