- Power Generation, Transmission, & Distribution

- U.S. Diesel Exhaust Fluid (DEF) Market

U.S. Diesel Exhaust Fluid (DEF) Market Size, Share, and Growth Forecast, 2025 - 2032

U.S. Diesel Exhaust Fluid (DEF) Market by Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Component (Catalysts, Tanks, Injectors, Sensors, Others), Application (Construction Equipment, Agricultural Tractors, Others), and Regional Analysis for 2025 - 2032

U.S. Diesel Exhaust Fluid (DEF) Market Share and Trends Analysis

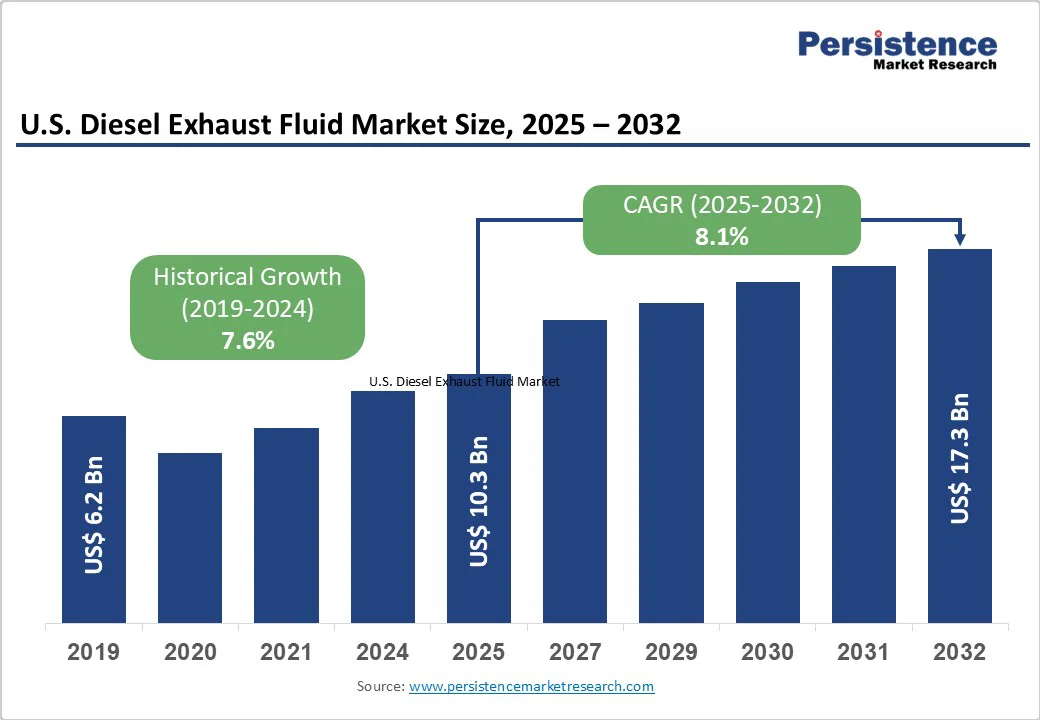

The U.S. diesel exhaust fluid (DEF) market size is likely to be valued at US$10.3 billion in 2025, and is projected to reach US$17.3 billion by 2032, growing at a CAGR of 8.1% during the forecast period 2025-2032. This promising growth trajectory reflects the nation's commitment to stringent emission control regulations and the widespread adoption of selective catalytic reduction (SCR) technology across commercial and industrial vehicle fleets.

Key drivers include the U.S. Environmental Protection Agency (EPA)’s rigorous enforcement of Tier 3 and Tier 4 emission standards, which mandate SCR systems in heavy-duty trucks, commercial vehicles, and off-road equipment. The expanding commercial transportation sector, fueled by e-commerce growth and logistics demand, continues to boost DEF consumption. In contrast, infrastructure investments in the construction and agriculture sectors drive adoption across off-highway applications. Market opportunities are amplified by the integration of IoT-enabled monitoring systems for real-time DEF tracking, advancements in freeze-resistant formulations for cold climates, and the establishment of robust retail and bulk distribution networks that ensure nationwide supply accessibility.

Key Industry?Highlights

- Vehicle Segmentation Leadership: Heavy commercial vehicles are set to command around 35.6% market share in 2025, driven by mandatory SCR adoption and high-DEF consumption rates in long-haul trucking fleets.

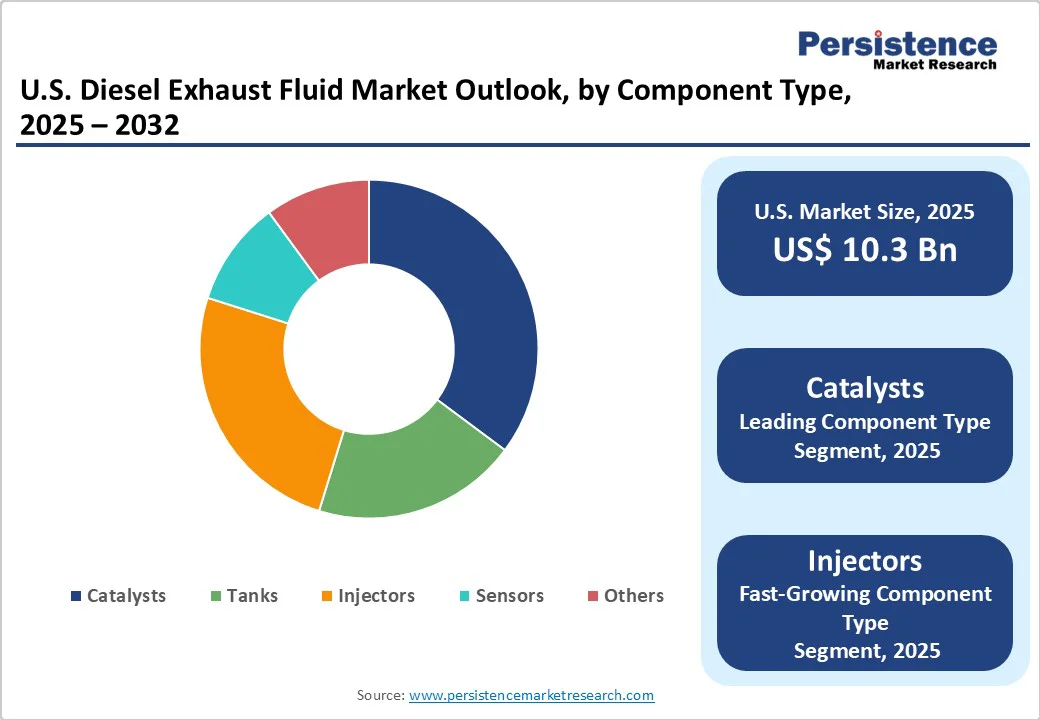

- Dominant Component: Catalysts are likely to dominate with about 39.3% share in 2025, underscoring their critical role in SCR systems for NOx conversion.

- Fastest-growing Component: Injectors are the fastest-growing component for 2025-2032, driven by advancements in precision dosing technologies and the integration of electronic controls for optimized DEF delivery and reduced emissions.

- Application Focus: Construction equipment is expected to hold approximately 43.4 of % diesel exhaust fluid market revenue share in 2025, owing to widespread diesel engine use and extended duty cycles in heavy-duty operations.

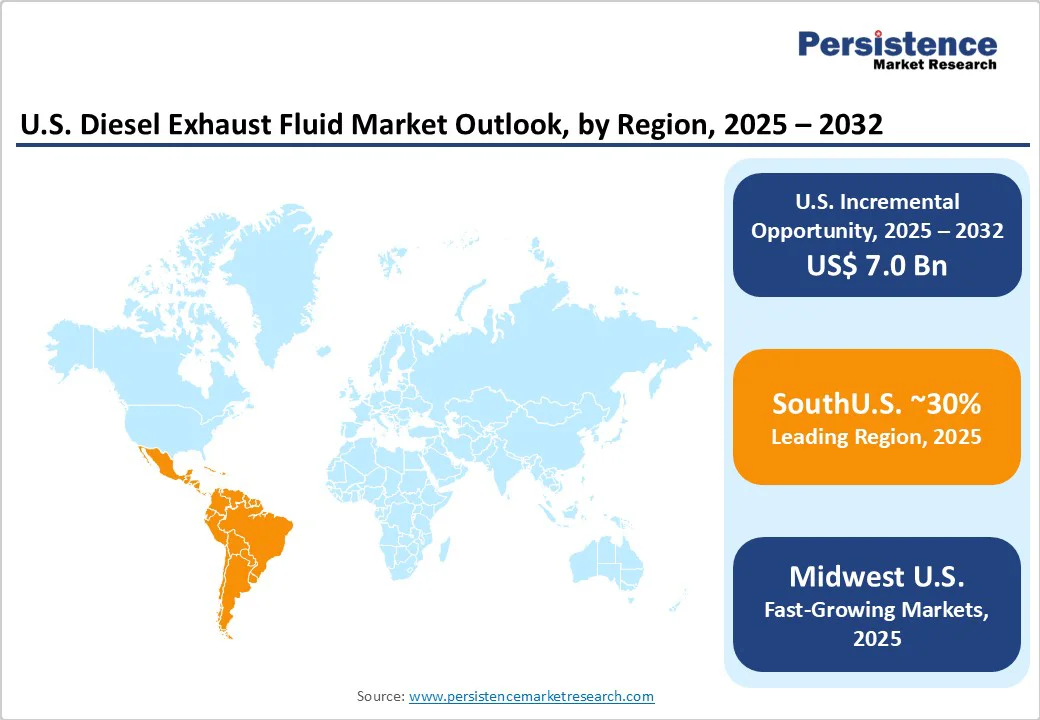

- Regional Dynamics: The South region is slated to lead with an estimated 35% share (valued at US$3.6 billion) in 2025, supported by extensive oil and gas operations, freight corridors, and commercial transport fleets.

- Strategic Consolidation: Market consolidation accelerates as Yara International’s US$150 million capacity expansion and Old-World Industries’ US$85 million acquisition program strengthen supply chain integration, enhance market coverage, and boost regional distribution efficiency.

- Technology Integration: Shell–Cummins partnerships in advanced SCR systems and BASF’s next-generation catalyst formulations reflect ongoing industry innovation toward integrated emission control solutions, higher fuel efficiency, and enhanced system durability.

| Key Insights | Details |

|---|---|

|

U.S. Diesel Exhaust Fluid (DEF) Market Size (2025E) |

US$10.3 Bn |

|

Market Value Forecast (2032F) |

US$22.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

30.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

27.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Stringent EPA Emission Regulations and Compliance Requirements

The U.S. Environmental Protection Agency (EPA)'s implementation of increasingly strict emission standards represents the primary growth catalyst for the DEF market. EPA Tier 4 Final regulations, which took full effect in 2015, mandate significant reductions in nitrogen oxide (NOx) emissions from diesel engines, requiring the adoption of SCR technology across heavy-duty vehicles and off-road equipment. According to EPA data, these regulations have resulted in NOx emission reductions of up to 90% compared to pre-2010 levels. The regulatory framework extends beyond on-highway applications to include construction equipment, agricultural machinery, and marine vessels, creating comprehensive market demand. Compliance costs associated with non-conforming equipment can exceed US$37,500 per unit in penalties, driving proactive adoption of DEF-enabled SCR systems across commercial fleets.

At the same time, major infrastructure investment programs, including the Infrastructure Investment and Jobs Act's US$1.2 trillion allocation, drive substantial demand for construction and agricultural equipment requiring DEF compliance. Off-road equipment applications, including excavators, bulldozers, and agricultural tractors, typically consume diesel exhaust fluid at higher rates than highway vehicles due to extended operating cycles and higher engine loads. The agricultural sector's modernization toward precision farming techniques further increases demand for DEF-compliant machinery that meets Tier 4 emission standards.

Raw Material Price Volatility and Supply Chain Dependencies

DEF production relies heavily on urea pricing, which is highly volatile due to fluctuations in natural gas costs and global supply chain disruptions. Urea accounts for 32.5% of DEF composition, making the fluid susceptible to commodity market pressures that can increase manufacturing costs by 15-25% annually. Supply chain constraints, particularly during peak agricultural seasons when urea demand for fertilizer applications rises, create periodic shortages that affect DEF availability and pricing stability. The concentration of urea production facilities in specific geographic regions compounds vulnerability to localized disruptions, potentially constraining market growth during supply shortages.

Establishing a comprehensive DEF distribution infrastructure requires substantial capital investment, particularly in rural and remote areas where construction and agricultural equipment operate. Distribution terminals, specialized storage tanks, and dispensing equipment can cost 500,000-US$2 million per facility, creating barriers for new market entrants. Temperature-sensitive storage requirements and shelf-life considerations further complicate distribution logistics, requiring climate-controlled facilities and the management of inventory rotation. The geographic dispersion of end-users, particularly in agricultural and construction sectors, increases transportation costs and delivery complexity compared to centralized fuel distribution networks.

Technological Integration and Smart Fleet Management

The convergence of diesel exhaust fluid systems with telematics and IoT technologies presents significant growth opportunities for value-added services and efficiency optimization. Advanced monitoring systems enable real-time DEF level tracking, consumption optimization, and predictive maintenance scheduling, creating differentiation opportunities for suppliers. Integration with fleet management platforms allows operators to minimize operational costs while ensuring regulatory compliance through automated reporting and documentation. The smart DEF management market segment is projected to reach US$500 million by 2030, driven by fleet operators seeking operational efficiency gains.

Furthermore, the transition toward hybrid diesel-electric powertrains in commercial vehicles creates new applications for DEF technology beyond traditional diesel engines. Marine applications, including commercial fishing vessels and recreational boats, represent an underserved market segment facing growing regulatory pressure to comply with emissions standards. Power generation equipment, including backup generators and stationary engines, increasingly requires DEF compliance under EPA regulations, expanding the addressable market beyond transportation applications. These emerging segments collectively represent approximately $800 million in additional market opportunity through 2032.

Category-wise Analysis

Vehicle Type Insights

Heavy commercial vehicles are expected to dominate the U.S. DEF market, with around 35.6% share in 2025, driven by mandatory SCR adoption and high consumption in long-haul trucking operations. Class 8 trucks, including tractor-trailers and heavy-duty delivery vehicles, consume DEF at rates ranging from 2% to 6% of diesel fuel consumption, creating substantial demand for DEF. The segment benefits from established distribution infrastructure at truck stops and commercial fueling stations nationwide. Major fleet operators, including FedEx, UPS, and Walmart, maintain comprehensive DEF supply contracts supporting consistent market demand.

Component Insights

Catalysts are poised to capture an estimated 39.3% of the U.S. diesel exhaust fluid market share in 2025, serving as the critical component enabling SCR system functionality through NOx reduction chemistry. These ceramic honeycomb structures, coated with precious metals such as platinum, palladium, and vanadium, require replacement every 150,000-300,000 miles, creating recurring aftermarket demand. The segment benefits from technological advancements, improving catalyst efficiency and durability while reducing precious metal content requirements. Partnerships between original equipment manufacturers (OEMs) and catalyst manufacturers ensure consistent supply chain integration and compliance with quality standards.

Injectors represent the fastest-growing component segment through 2032, aided by technological advancement toward precision dosing systems and electronic control integration. Modern DEF injectors use advanced spray patterns and electronic timing control to optimize urea distribution within exhaust streams, improving emission-reduction efficiency. The segment benefits from increasing adoption of closed-loop control systems that adjust DEF injection rates based on real-time NOx sensor feedback. Replacement cycles typically range from 100,000 to 150,000 miles, creating substantial aftermarket opportunities as vehicle fleets age.

Application Insights

Construction equipment is slated to hold about 43.4% of the U.S. DEF market share in 2025, reflecting the sector's large diesel engine population and extended operating cycles requiring continuous DEF consumption. Excavators, bulldozers, and other earthmoving equipment typically operate 2,000-3,000 hours annually at high engine loads, resulting in proportionally higher DEF consumption than highway vehicles. The segment benefits from infrastructure investment programs, driving equipment utilization and replacement cycles. Major equipment manufacturers, including Caterpillar, Komatsu, and John Deere, have standardized SCR technology across their Tier 4 Final product lines.

Agricultural tractors demonstrate the fastest growth rate within application types, fueled by farm modernization toward precision agriculture and equipment replacement cycles. Modern agricultural equipment that incorporates GPS guidance, variable-rate application, and data analytics requires Tier 4 Final compliance, which mandates DEF consumption. The segment benefits from favorable financing programs and tax incentives supporting equipment upgrades. Seasonal usage patterns create predictable demand cycles aligned with planting and harvesting seasons, enabling suppliers to optimize inventory management and distribution strategies.

Regional Insights

South U.S. Diesel Exhaust Fluid (DEF) Market Trends

The South region is expected to maintain its market leadership position, with approximately 35% of the U.S. diesel exhaust fluid market share in 2025. Texas leads regional consumption, driven by extensive oil and gas drilling operations, agricultural production, and transportation corridor activity, which support high diesel fuel and DEF usage. The region benefits from established petroleum refining infrastructure, facilitating DEF production and distribution through existing fuel terminal networks. Major ports in Houston, New Orleans, and Savannah generate substantial demand for marine applications and cargo-handling equipment that require emission compliance.

The regulatory environment emphasizes federal EPA compliance while providing state-level incentives for emission reduction technologies through programs such as the Texas Emissions Reduction Plan, which has allocated over US$1.2 billion for clean transportation initiatives. The competitive landscape features both national suppliers and regional distributors leveraging established relationships with fleet operators and equipment dealers. Investment trends focus on expanding storage capacity and distribution terminals to serve growing demand from shale oil production and agricultural modernization.

Midwest U.S. Diesel Exhaust Fluid (DEF) Market Trends

The Midwest region represents an estimated 28% of the U.S. DEF market share in 2025, with projected growth to US$4.8 billion by 2032, driven by extensive agricultural operations and manufacturing activity. Illinois, Iowa, and Minnesota lead regional consumption through large agricultural equipment fleets and transportation networks supporting grain movement and industrial production. The market here benefits from proximity to urea production facilities and established agricultural supply chains, facilitating cost-effective DEF distribution. Chicago serves as a major distribution hub with multiple DEF terminals supporting regional supply chains.

Primary growth drivers include agricultural modernization toward precision farming techniques that require Tier 4 Final-compliant equipment, manufacturing sector expansion driving demand for material handling equipment, and transportation infrastructure supporting intermodal freight operations. The regulatory environment emphasizes EPA compliance while providing state-level programs that support clean transportation initiatives, including renewable fuel standards and emission-reduction grants. The competitive landscape features agricultural cooperatives, fuel distributors, and specialized DEF suppliers serving diverse customer segments. Investment trends focus on expanding seasonal storage capacity and enhancing the rural distribution network to serve dispersed agricultural customers who require a reliable DEF supply during critical operating periods.

Competitive Landscape

The U.S. diesel exhaust fluid market structure exhibits moderate concentration with leading players maintaining significant market positions through established distribution networks and strategic partnerships. Yara International holds approximately 25% market share through its Air1® brand and comprehensive supply chain infrastructure, while CF Industries Holdings Inc. commands 18% share leveraging domestic urea production capabilities. BASF SE, Shell PLC, and Cummins Inc. maintain strong positions through technology integration and OEM partnerships. Market concentration analysis reveals opportunities for strategic consolidation as smaller regional players seek scale advantages and national market access.

Key Industry Developments

- In August 2025, Tartan Oil LLC expanded its diesel-exhaust-fluid (DEF) terminal network to three new sites in North America, specifically in Kingman, Arizona; Camilla, Georgia; and Staunton, Virginia, aiming to meet the growing demand for DEF across the transportation sector. The move bolsters Tartan’s capacity and geographic reach, reinforcing its role as a wholesale marketer of refined products, DEF and lubricants to over 10,000 locations throughout 48 states and five Canadian provinces.

- In August 2025, the U.S. EPA issued new guidance for diesel engines in vehicles and equipment using SCR systems and DEF. The updated guidance relaxes the so-called “inducement” requirements, such as immediate engine speed or torque derates that kick in when DEF levels are too low or system sensors fail, so that operators such as farmers, truckers and construction equipment users will face fewer abrupt power losses. From model-year 2027 onward, new on-road diesel trucks must be engineered to avoid sudden and severe performance losses when DEF is depleted, and existing equipment will be eligible for software updates, allowing more time for fault resolution.

- In June 2025, Rislone launched a super? Concentrated version of its Diesel DEF Treatment, designed for commercial, governmental, and agricultural fleets. The 33-ounce bottle treats up to 55 gallons of DEF, while a six-bottle case can treat a full 330 gallons. gallon IBC tote, allowing fleets to protect multiple vehicles efficiently. The formula stabilizes DEF, prevents AdBlue®/DEF crystallization, and enhances SCR system efficiency, safeguarding components such as the tank, pump, heater, injector, lines, and mixer.

Companies Covered in U.S. Diesel Exhaust Fluid (DEF) Market

- Total Energies

- Shell

- BASF SE

- Sinopec

- Cummins Filtration

- CF Industries Holdings, Inc.

- Dyno Nobel

- Agrium Inc.

- Honeywell International Inc.

- Faurecia SE

Frequently Asked Questions

The U.S. diesel exhaust fluid (DEF) market is estimated to reach US$ 10.3 billion in 2025.

The key demand driver for the market is the stringent emission regulations mandating selective catalytic reduction (SCR) technology adoption across on-road and off-road diesel vehicles.

The market is poised to witness a CAGR of 8.1% from 2025 to 2032.

The convergence of diesel exhaust fluid systems with telematics and IoT technologies presents significant growth opportunities for value-added services and efficiency optimization.

Some of the key market players are Total Energies, Shell, BASF SE, Sinopec and Cummins Filtration.