- Medical Devices

- IV Fluid Transfer Drug Devices Market

IV Fluid Transfer Drug Devices Market Size, Share, and Growth Forecast, 2026-2033

IV Fluid Transfer Drug Devices Market by Device Architecture (Infusion Pumps, Gravity Systems, IV Tubing & Sets, Connectors, Venous Access Devices), Therapeutic Application (Oncology, Autoimmune, Cardiovascular, Neurology, Blood Disorders, Aesthetic & Wellness IV Therapy), Delivery Setting (Hospital Care, Outpatient Centers, Home Healthcare, Long-Term Care), and Regional Analysis for 2026-2033

IV Fluid Transfer Drug Devices Market Share and Trends Analysis

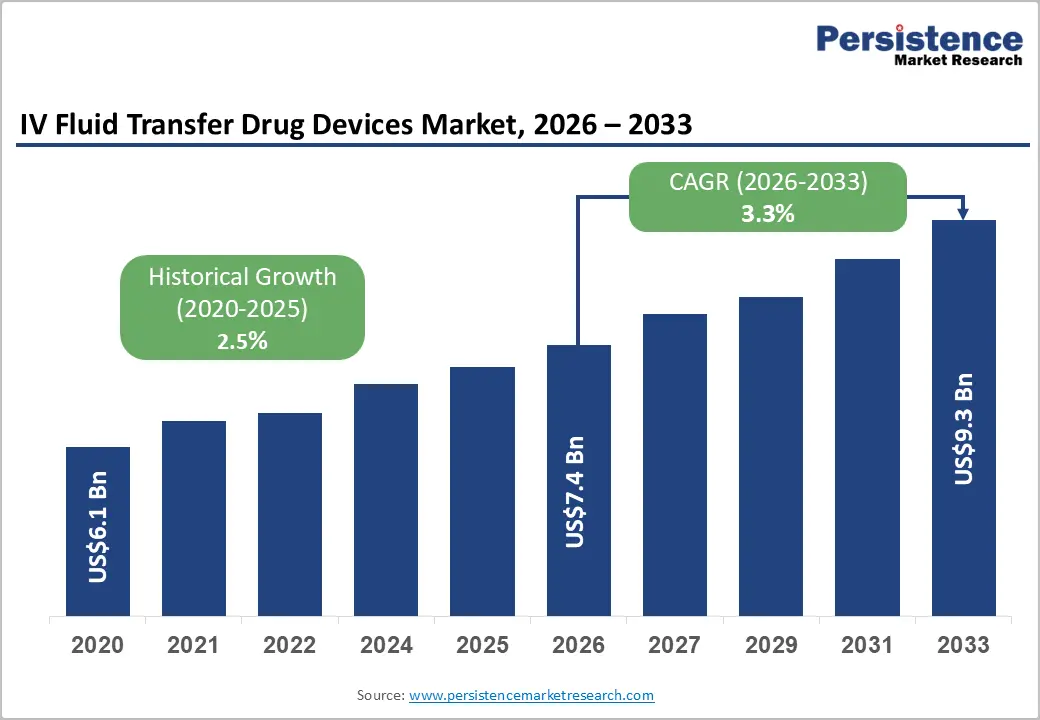

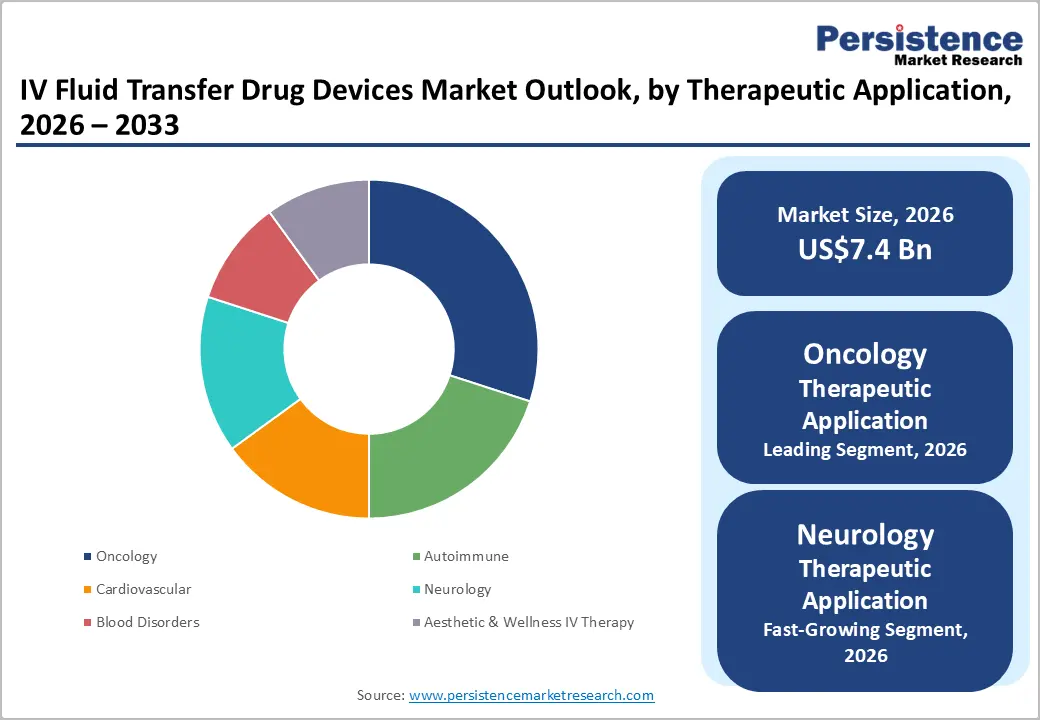

The global IV fluid transfer drug devices market size is likely to be valued at US$7.4 billion in 2026, and is projected to reach US$9.3 billion by 2033, growing at a CAGR of 3.3% during the forecast period 2026–2033. This market expansion is driven by the growing prevalence of chronic diseases, including cancer, cardiovascular disorders, autoimmune conditions, and neurological illnesses, which significantly increase the demand for intravenous (IV) therapy across hospitals, outpatient centers, and home healthcare settings.

Rising surgical volumes and complex treatment regimens further amplify the need for precise and reliable IV fluid transfer drug devices. Healthcare providers are actively investing in advanced drug delivery solutions and closed system transfer technologies, which enhance patient safety, reduce medication errors, and support efficient workflow management. Simultaneously, global improvements in healthcare infrastructure enable broader access and adoption of these devices, sustaining sustained market growth.

Key Industry Highlights

- Dominant Device Architecture: Infusion pumps are expected to command around 34% revenue share in 2026, while IV tubing & sets are likely to grow the fastest at 6.8% CAGR through 2033, driven by rising demand for infection-control-compliant components.

- Leading Therapeutic Application: Oncology is anticipated to lead with an estimated 30% share in 2026, while neurology applications are projected as the fastest-growing segment during 2026–2033, reflecting increasing incidence of chronic neurological disorders.

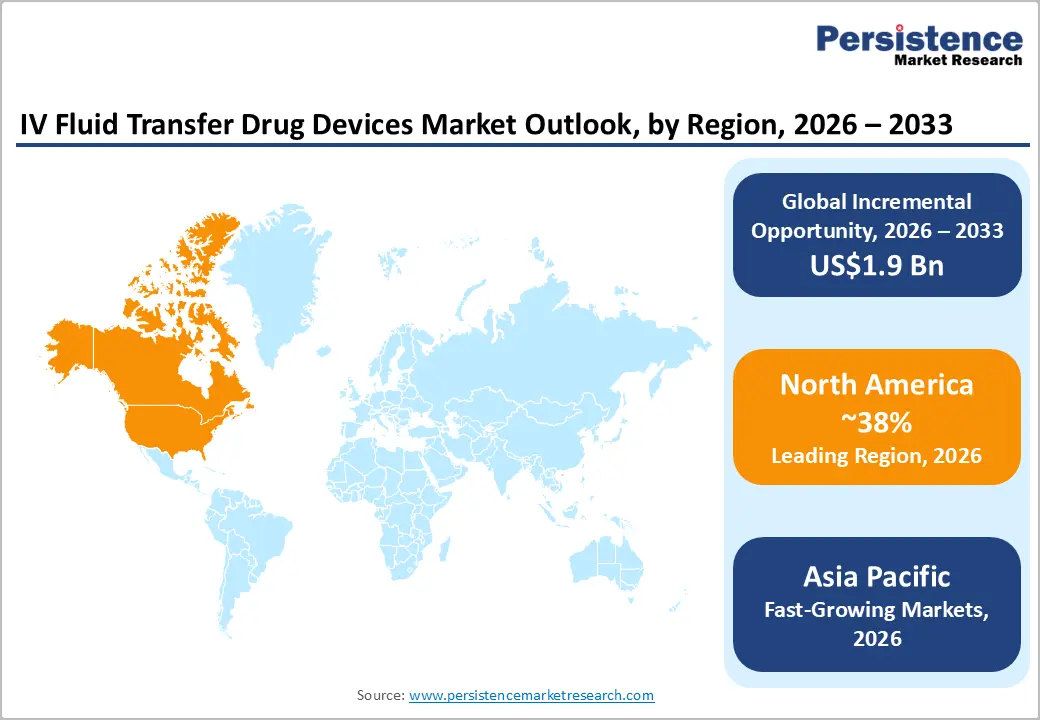

- Regional Leadership: North America is poised to dominate with an estimated 38% share in 2026, whereas Asia Pacific is projected to register the highest growth at 9.3% CAGR through 2033, driven by skyrocketing chronic disease prevalence.

- Competitive Environment: Key market dynamics include strategic product launches, facility expansions, and regional partnerships, enhancing innovation, supply chain resilience, and penetration into emerging markets such as India and China.

| Key Insights | Details |

|---|---|

| IV Fluid Transfer Drug Devices Market Size (2026E) | US$ 7.4 Bn |

| Market Value Forecast (2033F) | US$ 9.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Chronic Disease Burden and Increasing Demand for Intravenous Therapy

The global rise in chronic diseases, including cancer, cardiovascular disorders, autoimmune conditions, and neurological illnesses, has driven growing demand for IV fluid transfer drug devices. Intravenous therapy is essential for managing complex treatments, prompting the adoption of advanced infusion pumps, venous access devices, and connectors across hospital, outpatient, and home healthcare settings. Patients undergoing chemotherapy, long-term supportive care, or critical care rely on precise and reliable delivery systems to optimize outcomes and reduce complications. This demand is reinforced by ongoing investments in hospital infrastructure and increasing access to outpatient care facilities.

Heightened hospitalizations and treatment complexity are driving investment in closed system transfer technologies to enhance safety and minimize contamination. Policy shifts, such as the Non-Opioids Prevent Addiction in the Nation (NOPAIN) Act payment rule, expanding reimbursement for infusion pumps in ambulatory care starting in 2026, and further supporting device utilization. Simultaneously, aesthetic and wellness IV services are gaining traction worldwide. For example, REVIV offered Vitaglow drips backstage at New York Fashion Week 2026, as part of a beauty ritual alongside facials and skincare treatments, signaling luxury and experiential positioning of IV fluids in mainstream beauty culture. Also, Indian clinics in metropolitan cities report rapid uptake of “glow drips” for skin hydration, brightening, and wellness. These lifestyle applications broaden device use beyond clinical settings, contribute incremental device utilization, and support overall market growth.

Technological Advancements in IV Systems and Expansion of Ambulatory & Home Care Settings

Rapid innovation in IV infusion technologies is improving precision, safety, and usability, enabling clinicians to manage complex IV regimens with fewer errors. Smart infusion pumps with electronic safety controls, integrated alarms, and real-time connectivity support accurate dosing, while emerging connectors and safety-enhanced devices reduce infection risks and strengthen protocol compliance across hospital, outpatient, and home care settings. These advancements increase clinician confidence and adoption of advanced IV fluid transfer systems, while also enabling integration with hospital IT systems for analytics and workflow optimization.

The expansion of home healthcare and ambulatory infusion services is reshaping delivery models beyond traditional hospitals. Initiatives such as multi-year group purchasing agreements supporting outpatient clinic expansion highlight institutional investment in mobile and non-hospital care. Combined with patient-friendly device designs, caregiver training programs, remote monitoring integration, and the rise of cosmetic and wellness IV therapies in developed and developing regional markets. These collectively reinforce the market’s growth across both clinical and lifestyle care segments, creating opportunities for device manufacturers to diversify offerings and capture emerging revenue streams.

High Cost of Advanced IV Drug Transfer Systems

Despite significant technological improvements, advanced IV drug transfer devices, including smart infusion pumps and closed sterile systems, continue to carry high upfront costs that strain healthcare budgets. Smaller hospitals, clinics, and facilities in developing regions face budgetary limitations, making initial acquisition difficult. Ongoing maintenance, training, software updates, and calibration requirements further inflate lifecycle expenses. These financial barriers slow the adoption of advanced technologies in non-premium settings such as smaller outpatient centers and community health systems.

Recent healthcare policy debates and tariff developments have heightened cost pressures on device pricing. For example, renewed tariffs on medical device imports have caused concerns that hospital providers will encounter higher costs for critical devices and components, with industry leaders warning that these trade measures could propagate cost increases through supply chains. This economic constraint can delay adoption in both home healthcare and long-term care facilities. As a result, providers may defer purchases of high-cost infusion systems, slowing overall market expansion of sophisticated drug transfer technologies globally.

Regulatory and Supply Chain Challenges

Stringent regulatory requirements in major markets such as the U.S. and Europe extend time-to-market and compliance costs for IV fluid transfer devices. Manufacturers must undertake comprehensive safety testing, documentation, and quality audits to meet U.S. Food & Drug Administration (FDA), European CE, and other global standards, which can delay product launches and increase device pricing. Ongoing changes in regulatory frameworks, including new quality management rules, continue to shape compliance complexity. These hurdles require significant investment from manufacturers and can discourage smaller players from entering the market.

On the supply side, government monitoring and shortage reporting efforts highlight persistent vulnerabilities. In early 2025, the U.S. FDA finalized guidance under Section 506J of the FD&C Act, requiring device manufacturers to notify the agency of potential manufacturing interruptions that could disrupt the supply chain, a clear indication of ongoing supply risk monitoring. These disruptions, compounded by logistic constraints, increased demand for medical components, and regional production delays, introduce operational risk for manufacturers and healthcare providers alike. These regulatory hurdles and supply chain vulnerabilities act as key restraints on faster market adoption and long-term growth trajectories worldwide.

Expansion in Burgeoning Healthcare Markets and Digital Infrastructure

High-growth healthcare markets in Asia Pacific, Latin America, and the Middle East & Africa present significant opportunities for IV fluid transfer drug devices. Rapid increases in healthcare spending, expanding hospital capacity, and rising per capita income are driving demand for modern drug delivery solutions. Governments in these regions are actively expanding healthcare infrastructure and digital health systems, increasing access to quality care and strengthening critical care delivery. For example, the India Digital India Health Mission and Ayushman Bharat initiatives are accelerating telemedicine, unified health records, and digital health IDs nationwide, significantly improving access to remote care and clinical data exchange.

Regional policies aimed at improving healthcare access are boosting infrastructure investments and capacity expansions. In 2026, major digital health summits such as Smart Health Asia 2026 are bringing together policymakers, healthcare providers, and technology innovators to advance digital health ecosystems across Asia Pacific, reinforcing regional collaboration and investment in connected care technologies. Growing awareness of chronic disease management and critical care requirements in emerging markets further positions IV fluid devices as essential tools. These developments pave the way for broader adoption of IV fluid transfer systems in both urban and underserved areas, offering manufacturers opportunities in high-growth emerging markets.

Telehealth Integration, Sterile Systems, and Emerging Lifestyle Applications

The convergence of telehealth, connected medical technologies, and real-time data analytics is creating powerful opportunities for IV systems that support remote monitoring and integrated care delivery. Healthcare systems are accelerating digital transformation to improve access, efficiency, and patient outcomes, particularly in chronic disease management and outpatient care. In the Asia Pacific, a growing shift toward digital-first healthcare models is evident, with providers and policymakers increasingly adopting connected solutions that enhance remote care coordination and resource utilization.

Government initiatives are also enabling digital health advancements and faster technology adoption. In late 2025, the U.S. FDA finalized guidance allowing broader use of real-world evidence (RWE) from digital sources to support regulatory decision-making for medical devices, including software-enabled and connected care products. Meanwhile, wellness and aesthetic clinics are increasingly adopting IV fluids and nutrient drips for hydration, vitamin therapy, and anti-aging applications, highlighting a growing lifestyle and beauty market segment. Digital health conferences and technology partnerships are accelerating collaboration between healthcare providers and innovators, creating a fertile ecosystem for patient-centric care models that span both clinical and wellness applications.

Category-wise Analysis

Device Architecture Insights

Infusion pumps are projected to lead with about 34% of the IV fluid transfer drug devices market revenue share in 2026, reflecting critical reliance on precise fluid and drug delivery in chemotherapy, pain management, parenteral nutrition, and complex fluid regimens. Hospitals and specialty care centers prioritize pumps with integrated safety alarms and programmable dosing to minimize errors and improve patient outcomes. Real-world developments underscore this leadership. In late 2025, for instance, the NOPAIN Act final rule added multiple electronic infusion pumps to the list of devices eligible for separate Medicare payment in ambulatory surgical centers (ASCs) and outpatient settings, strengthening outpatient therapy adoption beginning in 2026. This regulatory support highlights infusion pumps’ central role in both traditional and evolving care delivery models.

IV tubing & sets are expected to grow at an estimated 6.8% CAGR through 2033, driven by rising demand for sterile, disposable accessories that enhance infection control across hospitals, outpatient centers, and home infusion settings. Frequent replacement cycles and stringent hygiene standards create stable recurring demand, while the shift toward ambulatory and home-based therapies accelerates adoption of single-use tubing and connectors. In 2025, the Centers for Medicare & Medicaid Services (CMS) expanded separate Medicare reimbursement for qualifying infusion pumps under the NOPAIN Act, highlighting broader support for infusion systems and their components in outpatient and ambulatory care. This policy indirectly encourages the integration of complete IV therapy solutions, including consumable tubing & sets, into standard clinical practice.

Therapeutic Application Insights

The oncology segment is expected to capture roughly 30% of the therapeutic application revenue in 2026, driven by the increasing prevalence of cancer and heavy reliance on intravenous therapies for chemotherapy and supportive care. Complex multi-drug protocols delivered via IV systems require precision and safety, making advanced delivery technologies essential in hospitals and outpatient clinics. Supporting this trend, the U.S. FDA in early 2026 granted full first-line approval to a new targeted lung cancer therapy, signaling ongoing emphasis on expanding effective cancer treatment regimens that often depend on structured infusion delivery protocols. Such regulatory momentum reinforces oncology’s dominant influence on IV device utilization across care settings.

The neurology segment is forecast to grow at approximately 7.2% CAGR from 2026 to 2033, supported by the rising incidence of neurological and neurodegenerative conditions, such as multiple sclerosis and chronic neuropathic disorders that increasingly require intravenous or infusion-linked drug delivery as part of standard care. These therapies are being adopted across hospitals and outpatient neurology clinics where connected monitoring and dosing precision enhance long-term management. The regulatory actions, such as the FDA approval of an injectable version of an Alzheimer’s drug that facilitates less frequent clinic visits highlights both therapeutic demand and evolving care pathways, underscoring the value of adaptable infusion technologies in neurology practice.

Regional Insights

North America IV Fluid Transfer Drug Devices Market Trends

At approximately 38%, North America is anticipated to claim the largest portion of the IV fluid transfer drug devices market share in 2026, anchored by advanced healthcare infrastructure, widespread adoption of smart infusion systems, and robust procedural volumes in oncology, critical care, and chronic disease management. The United States leads regional performance, supported by precision drug delivery priorities, healthcare digitization, and a strong payer landscape that supports innovative therapy delivery models in both hospitals and ambulatory settings. The CMS expansion of reimbursement in 2025 for select infusion therapies and home infusion services under the NOPAIN Act continues to accelerate adoption of integrated IV solutions outside traditional inpatient environments.

Supply chain investments and manufacturing growth further strengthen the region’s outlook. For example, BD committed over US$ 30 million to expand U.S. production of IV lines and catheter products, enhancing local availability of critical components. Expansion of hybrid care models and integration with electronic medical records supports clinician workflows and patient safety. Regulatory focus on device quality and interoperability also enables continued penetration of advanced IV technologies, enhancing treatment accuracy and reinforcing North America’s role as a high-value, innovation-driven market with sustained growth potential.

Europe IV Fluid Transfer Drug Devices Market Trends

Europe is poised to account for an estimated 28% share of the global market for IV fluid transfer drug devices in 2026, driven by well-established healthcare systems, strong clinical adoption of safety-enhanced devices, and collaborative regulatory frameworks under the European Medicines Agency (EMA). Germany, the U.K., France, and Spain represent major demand centers, with broad utilization of precision infusion systems, closed sterile connectors, and advanced fluid transfer technologies in oncology, emergency care, and acute care settings. Alignment of device safety standards across the European Union supports seamless clinical implementation and encourages suppliers to innovate within harmonized regulatory requirements.

The European Commission (EC) approved € 403 million in targeted public funding to accelerate medical device innovation, including digital and AI-enabled platforms, pointing to broader momentum in clinical technologies that support infusion and drug delivery solutions across member states. Emphasis on reducing hospital-acquired infections supports adoption of needleless and closed system components. While differing reimbursement policies and budgetary pressures exist across European health systems, continued investments in outpatient services, device interoperability, and infection control strengthen overall market resilience and mid-to-high growth prospects.

Asia Pacific IV Fluid Transfer Drug Devices Market Trends

Asia Pacific is projected to be the fastest-growing regional market for IV fluid transfer drug devices, with a projected CAGR of approximately 9.3% through 2033. Growth is propelled by rapidly expanding healthcare infrastructure, increasing chronic disease burdens, rising middle-class demand for quality medical care, and expanding outpatient and home care delivery. Markets such as China, India, Japan, and ASEAN are scaling hospital and specialized care capacity, enabling broader clinical deployment of advanced infusion systems and connected therapy platforms across diverse care settings. These shifts are supported by national healthcare modernization strategies that emphasize access, quality, and efficiency.

Real-world developments illustrate this acceleration: at the India MedTech Expo 2025, the country showcased significant expansion of its domestic medical device ecosystem, reinforcing India’s evolution as a manufacturing and innovation hub for clinical and infusion devices. Governments are prioritizing local production, critical care enhancements, and supply chain resilience, reducing reliance on imports while expanding device availability. Investments in infection control practices and outpatient infusion programs further contribute to Asia Pacific’s dynamic market environment, presenting sustained high-volume opportunities for global manufacturers targeting emerging growth corridors.

Competitive Landscape

The global IV fluid transfer drug devices market structure is moderately consolidated, with leading players such as BD (Becton Dickinson), Baxter International, B. Braun, Smiths Medical, and ICU Medical together accounting for over 50% of market revenue. These established companies leverage strong hospital and healthcare provider relationships, regulatory expertise, and integrated device ecosystems spanning infusion pumps, IV tubing & sets, connectors, and closed system transfer devices. Heavy investment in R&D, clinical safety, and digital integration allows them to maintain technological leadership in smart infusion systems, remote monitoring, and error-reduction technologies.

Regional and niche players, including Terumo, Fresenius Kabi, Nipro, and Mindray, are focusing on specialized segments such as oncology-specific devices, home healthcare solutions, and emerging markets. Regulatory compliance, safety standards, and complex device integration create high barriers for new entrants, while growing digitalization and connected care trends enable software-driven platforms to enter via compatibility and remote monitoring solutions. Market consolidation is likely to increase as global leaders pursue strategic acquisitions, regional expansion, and technology partnerships, while analytics and connected-care providers continue collaborating to enhance device interoperability and patient safety outcomes.

Key Industry Developments

- In December 2025, InfuSystem announced that two electronic ambulatory infusion pumps used in its pain management services will receive separate Medicare reimbursement under the NOPAIN Act starting January 1, 2026. The decision by the CMS applies to pumps such as CADD-Solis and Sapphire.

- In August 2025, Terumo India launched Terufusion Advanced Infusion Systems, a connected infusion platform designed to improve precision and safety in intensive care units (ICUs). The system integrates a smart syringe pump, volumetric infusion pump, and pump monitoring software to enable accurate drug dosing, remote monitoring, and streamlined clinical workflows.

- In April 2025, Hydration Room introduced the “Glow & Go” IV drip for skin health using collagen and biotin. The expansion to 50+ clinics reflects growing adoption of IV therapy in the beauty and wellness segment.

Companies Covered in IV Fluid Transfer Drug Devices Market

- B. Braun Medical

- Baxter International

- ICU Medical

- Hospira

- Advance Medical Designs

- Unilife Corporation

- Amedra Pharmaceuticals

- Biogen Idec

- Sanofi

- Q.I. Medical

- Merit Medical Systems

- Terumo Corporation

- Smiths Medical

- Medtronic plc

Frequently Asked Questions

The global IV fluid transfer drug devices market is projected to reach US$ 7.4 billion in 2026.

Rising prevalence of chronic diseases, adoption of advanced IV therapy devices, and expansion of home healthcare drive the market.

The market is poised to witness a CAGR of 3.3% from 2026 to 2033.

Emerging markets, telehealth integration, and rising adoption of closed sterile transfer systems present strong growth opportunities.

BD, Baxter International, B. Braun, Smiths Medical, and ICU Medical are some of the leading market players.