- Pharmaceuticals

- Dry Powder Inhaler Market

Dry Powder Inhaler Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Dry Powder Inhaler Market by Product (Single Dose Dry Powder Inhalers and Multi Dose Dry Powder Inhalers), Modality (Manually Operated Inhaler Devices and Digitally Operated Inhaler Devices), Application (Asthma, Chronic Obstructive Pulmonary Disease (COPD), Pulmonary Arterial Hypertension, Diabetes, Cystic Fibrosis, and Others) Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Regional Analysis from 2026 to 2033

Dry Powder Inhaler Market Share and Trend Analysis

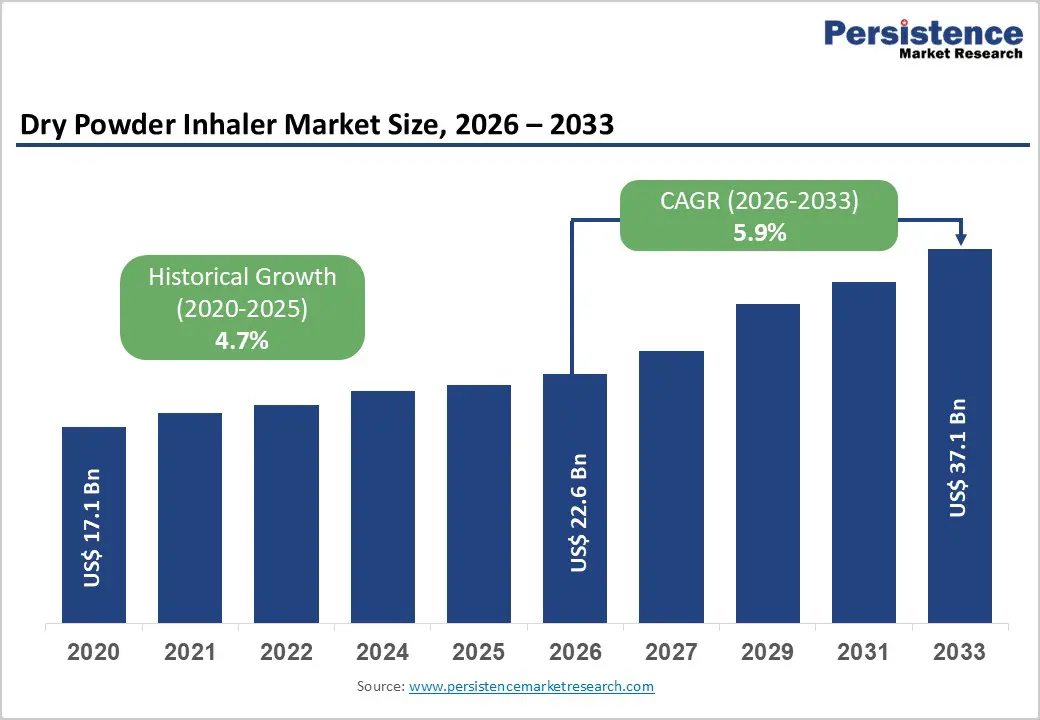

The global dry powder inhaler market size is estimated to grow from US$ 22.6 Bn in 2026 to US$ 37.1 Bn by 2033. The market is projected to record a CAGR of 5.9% during the forecast period from 2026 to 2033.

Global demand for dry powder inhalers is rising steadily, driven by the increasing prevalence of chronic respiratory conditions such as asthma, chronic obstructive pulmonary disease, cystic fibrosis, and other obstructive airway disorders, along with a growing shift toward patient-friendly, propellant-free inhalation therapies. Expanding use of dry powder inhalers across hospitals, specialty respiratory clinics, retail pharmacies, and home-care settings is supporting sustained market growth.

Higher diagnosis rates, improved physician awareness regarding long-term disease control, and rising patient preference for portable and easy-to-use inhalation devices are further accelerating adoption. In addition, increasing healthcare expenditure and broader access to maintenance respiratory therapies are enabling wider uptake across both developed and emerging markets. Continuous innovation in inhaler design, powder formulation stability, airflow optimization, and dose consistency is improving therapeutic efficacy, patient adherence, and treatment outcomes. The growing emphasis on home-based care, chronic disease self-management, and digitally connected inhalation platforms is further propelling global demand for dry powder inhalers.

Key Industry Highlights:

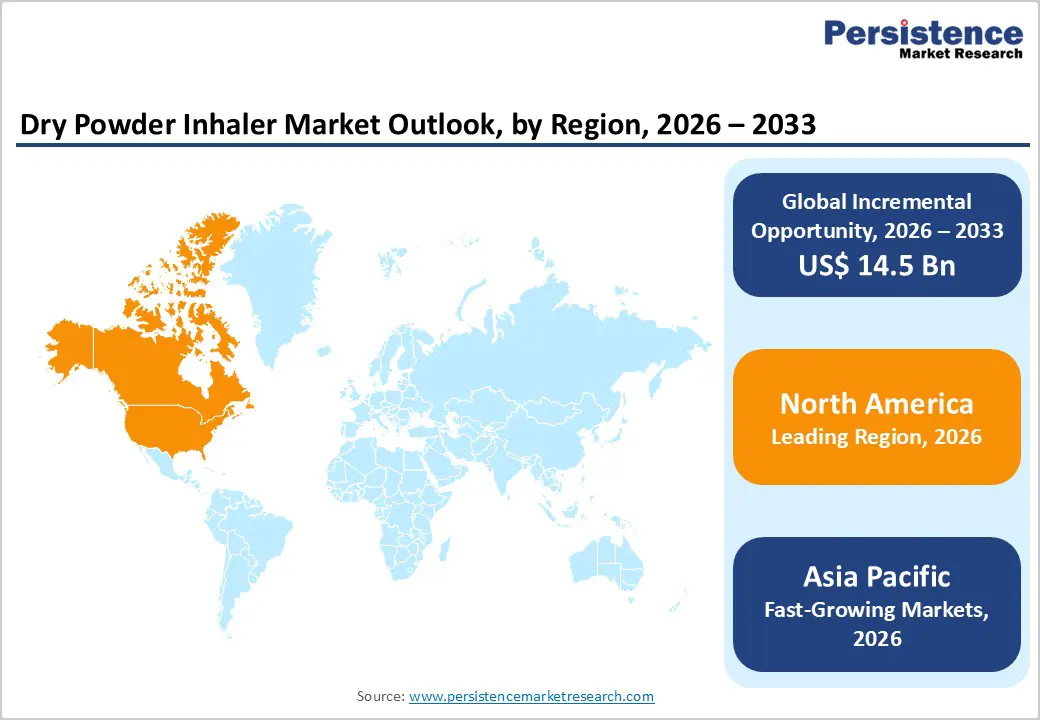

- Leading Region: North America holds the largest share at 46.7%, supported by a high burden of asthma and COPD, advanced healthcare infrastructure, strong adoption of maintenance inhalation therapies, early uptake of digitally enabled inhalers, and the presence of major pharmaceutical manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to large untreated respiratory patient populations, rising air pollution, improving healthcare access, and increasing investments in chronic disease management and inhalation therapy availability.

- Leading Product Segment: Single-dose dry powder inhalers dominate the market due to precise dose delivery, reduced contamination risk, and strong adoption for specialty and maintenance respiratory therapies.

- Fastest-Growing Product Segment: Multi-dose dry powder inhalers are expanding rapidly as demand increases for convenient, cost-effective solutions suited for long-term outpatient and home-based respiratory care.

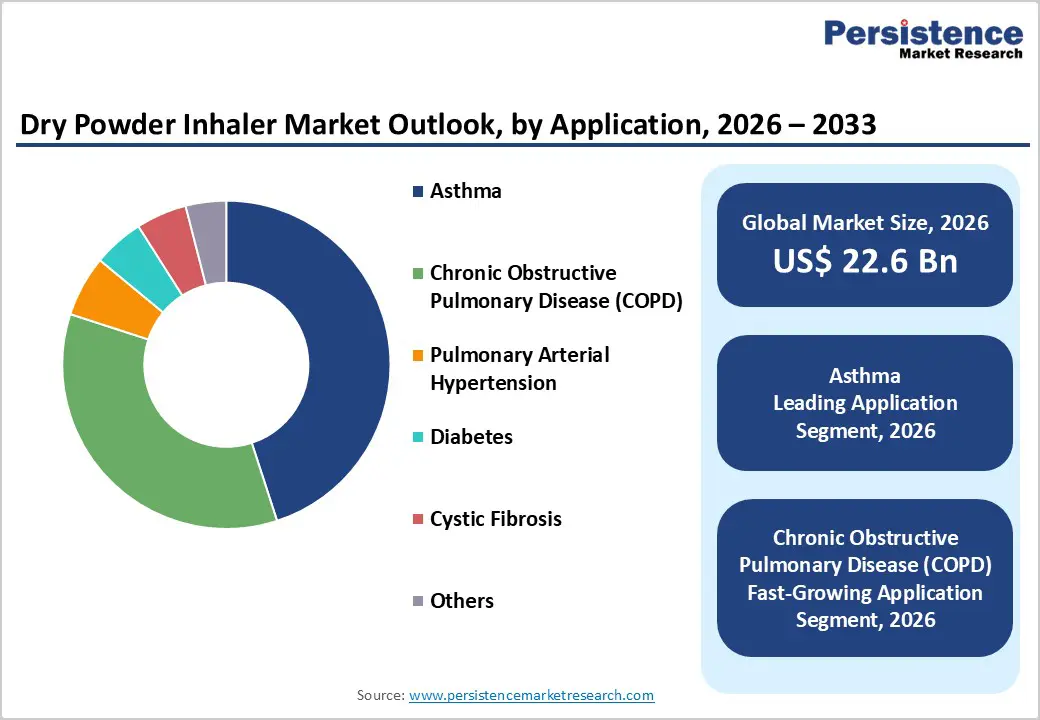

- Leading Application Segment: Asthma remains the top application, driven by high global prevalence and the widespread use of dry powder inhalers for long-term disease control and symptom management.

- Fastest-Growing Application Segment: Chronic obstructive pulmonary disease is scaling quickly due to aging populations, rising smoking rates, and increased reliance on maintenance inhalation therapies for disease management.

| Key Insights | Details |

|---|---|

| Dry Powder Inhaler Market Size (2026E) | US$ 22.6 Bn |

| Market Value Forecast (2033F) | US$ 37.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Dynamics

Driver - Growing Burden of Chronic Respiratory Diseases and Preference for Propellant-Free Inhalation

Increasing incidence of chronic respiratory conditions is a primary force accelerating adoption of dry powder inhalers globally. Asthma and chronic obstructive pulmonary disease are rising steadily due to aging populations, urbanization, smoking habits, and prolonged exposure to air pollutants. As long-term disease management becomes central to respiratory care, inhalation therapy remains the most effective route for targeted pulmonary drug delivery. Dry powder inhalers are increasingly favored because they are breath-actuated, portable, and eliminate the need for propellants, aligning with both clinical and environmental priorities.

Healthcare providers are emphasizing patient adherence and ease of use, driving demand for inhalers that reduce coordination errors common with pressurized devices. DPIs support consistent dosing and are well suited for maintenance therapies, particularly in outpatient and home-care settings. Expanding diagnosis rates, improved access to respiratory care, and rising awareness of disease control further increase prescription volumes. Additionally, environmental regulations aimed at reducing greenhouse gas emissions from medical devices are encouraging a gradual shift away from propellant-based inhalers. Continuous improvements in inhaler design, airflow optimization, and powder dispersion efficiency reinforce adoption, sustaining strong demand across developed and emerging healthcare systems.

Restraints - Patient Technique Dependency, Cost Pressure, and Limited Suitability Across Populations

Despite strong clinical adoption, several factors continue to limit broader utilization of dry powder inhalers. Effective DPI use depends heavily on a patient’s inspiratory flow, making these devices less suitable for very young children, elderly patients with severe airflow limitation, or individuals experiencing acute exacerbations. Inadequate inhalation technique can compromise dose delivery, reducing therapeutic effectiveness and impacting clinical outcomes. This dependency necessitates patient education and repeated training, increasing the burden on healthcare providers.

Cost considerations also restrain adoption, particularly in price-sensitive markets. Compared with some generic pressurized inhalers, DPIs especially branded or digitally enabled versions often carry higher unit costs. Limited reimbursement coverage in certain regions can shift expenses to patients, affecting long-term adherence. Additionally, formulation complexity and moisture sensitivity of dry powders increase manufacturing and packaging costs. Supply chain disruptions and dependence on specialized formulation technologies further add to pricing pressure. Regulatory requirements related to device-drug combination approvals can extend development timelines, delaying market entry. These clinical, economic, and operational challenges collectively moderate growth, particularly in low-resource settings where affordability and simplicity remain key decision factors.

Opportunity - Expansion of Smart Inhalers, Emerging Markets, and Sustainable Respiratory Care

Evolving healthcare priorities present significant growth opportunities for dry powder inhaler manufacturers. Integration of digital technologies into inhaler platforms is gaining momentum, enabling dose tracking, adherence monitoring, and real-time patient feedback. Smart DPIs support data-driven disease management and align with the broader adoption of connected healthcare and remote patient monitoring solutions. As payers and providers increasingly focus on outcome-based care, digitally enabled inhalers offer measurable clinical and economic value.

Emerging markets represent another major opportunity as respiratory disease prevalence rises alongside healthcare infrastructure development. Expanding insurance coverage, growing middle-class populations, and increasing availability of generic DPIs are improving access to inhalation therapies in Asia-Pacific, Latin America, and parts of the Middle East. Environmental sustainability initiatives further strengthen opportunity potential, as DPIs are viewed as eco-friendly alternatives to propellant-based devices. Ongoing innovation in low-resistance inhalers, multi-dose platforms, and combination therapies broadens the patient base. Strategic collaborations between pharmaceutical companies, device developers, and digital health firms are expected to accelerate product differentiation and market penetration, positioning DPIs for sustained long-term growth.

Category-wise Analysis

By Product, Single-Dose Dry Powder Inhalers Lead Due to Dose Precision and Reduced Cross-Contamination Risk

The single-dose dry powder inhalers segment is projected to dominate the global dry powder inhaler market in 2026, capturing a revenue share of 60.0%. This leadership is driven by precise dose delivery, lower risk of moisture exposure, and minimal cross-contamination, making single-dose DPIs particularly suitable for sensitive formulations and specialty therapies. These devices are widely adopted in hospital and home-care settings where accurate dosing and hygiene are critical. Single-dose formats are commonly preferred for patients with variable inspiratory flow, as they ensure consistent powder dispersion and reliable drug delivery. Their simple design supports ease of use, especially among elderly and pediatric populations. In addition, pharmaceutical companies favor single-dose DPIs for niche respiratory and systemic indications due to formulation stability and regulatory flexibility. Rising demand for controlled dosing, increasing use in emerging therapeutic applications, and ongoing improvements in capsule and blister-based delivery mechanisms continue to reinforce the dominance of this segment globally.

By Application, Asthma Leads Due to High Global Prevalence and Long-Term Maintenance Therapy

The asthma segment is expected to lead the global dry powder inhaler market in 2026, accounting for a 45.0% revenue share. This dominance is driven by the high global burden of asthma across both pediatric and adult populations and the widespread use of DPIs for long-term disease management. Dry powder inhalers are extensively prescribed for asthma due to their breath-actuated mechanism, portability, and suitability for maintenance and rescue therapies. Growing awareness of asthma control, increasing diagnosis rates, and improved access to inhalation therapies have expanded treatment adoption worldwide. Clinical guidelines in multiple regions increasingly favor DPIs because they eliminate coordination challenges associated with pressurized inhalers. Additionally, the availability of combination therapies and corticosteroids in DPI form supports consistent usage. Rising urbanization, air pollution, and allergen exposure further increase asthma incidence, sustaining demand. Continuous innovation in patient-friendly inhaler designs and digital adherence tools strengthens asthma’s position as the leading application segment.

By Distribution Channel, Hospital Pharmacies Lead Due to Prescription Volume and Structured Treatment Pathways

Hospital pharmacies are projected to dominate the global dry powder inhaler market in 2026, capturing a 55.0% revenue share. Hospitals remain the primary point of initiation for inhalation therapy, particularly for newly diagnosed asthma and COPD patients, severe cases, and acute exacerbations. Hospital pharmacies benefit from high prescription volumes, standardized treatment protocols, and strong physician oversight, ensuring consistent demand for dry powder inhalers. These settings play a critical role in patient education, device selection, and therapy optimization, which drives preference for hospital-dispensed DPIs. In addition, hospitals manage complex respiratory cases requiring combination therapies and specialty inhalers, further strengthening channel dominance. Long-term supplier contracts, formulary inclusion, and centralized procurement systems support recurring sales. Increasing hospital admissions related to respiratory disorders, expansion of pulmonary departments, and integration of inhaler therapy into inpatient and discharge care pathways ensure sustained leadership of hospital pharmacies globally.

Regional Insights

North America Dry Powder Inhaler Market Trends

North America is expected to dominate the global dry powder inhaler market in 2026, accounting for a 46.7% value share, primarily driven by the United States. The region benefits from a high prevalence of asthma and COPD, strong disease awareness, and early adoption of advanced respiratory therapies. Well-established healthcare infrastructure and widespread access to pulmonologists support consistent DPI prescriptions across both hospital and outpatient settings. Favorable reimbursement policies for inhalation therapies and strong insurance coverage encourage patient adherence and long-term use. North America also leads in the adoption of digitally enabled DPIs that support dose tracking and adherence monitoring.

The presence of major pharmaceutical and inhaler manufacturers accelerates product innovation and commercialization. Additionally, stringent regulatory standards promote high-quality device design and formulation reliability. Growing emphasis on preventive respiratory care, increasing elderly population, and sustained investments in chronic disease management programs collectively reinforce North America’s leadership in the dry powder inhaler market.

Europe Dry Powder Inhaler Market Trends

Europe’s dry powder inhaler market is expected to grow steadily in 2026, supported by aging demographics, rising prevalence of chronic respiratory diseases, and strong adherence to guideline-based treatment. Countries such as Germany, the U.K., France, Italy, and the Nordic region demonstrate robust adoption due to universal healthcare coverage and structured respiratory care pathways. Dry powder inhalers are widely preferred across Europe because of environmental concerns related to propellant-based inhalers, accelerating the shift toward DPIs. Regulatory focus on sustainability and patient safety further supports this transition. Hospitals, primary care clinics, and retail pharmacies actively prescribe DPIs for asthma and COPD maintenance therapy.

Europe is also witnessing gradual uptake of smart inhalers to improve adherence and outcomes. Standardized treatment protocols, strong clinician training programs, and favorable reimbursement structures sustain consistent demand. Continued innovation in low-resistance inhalers and patient-centric designs supports stable long-term growth across the region.

Asia Pacific Dry Powder Inhaler Market Trends

Asia Pacific dry powder inhaler market is projected to register a higher CAGR of around 8.0% between 2026 and 2033, driven by rapid healthcare expansion and increasing respiratory disease burden. Large populations in China, India, Japan, and South Korea, combined with rising air pollution and smoking prevalence, are significantly increasing asthma and COPD cases. Improving access to healthcare services, expansion of private hospitals, and growing awareness of inhalation therapy are accelerating DPI adoption. Government initiatives focused on chronic disease management, insurance expansion, and local manufacturing support market growth. Cost-effective DPI devices are gaining traction in high-volume and resource-constrained settings.

Global manufacturers are expanding regional presence through partnerships and localized production to improve affordability and supply. Increasing physician training, availability of generic DPIs, and gradual uptake of digital health solutions further strengthen adoption, positioning Asia Pacific as the fastest-growing regional market.

Competitive Landscape

The global dry powder inhaler market is highly competitive, with strong participation from Boehringer Ingelheim International GmbH, CHIESI Farmaceutici S.p.A., Cipla, GSK plc., Hovione, OPKO Health Inc., and Teva Pharmaceutical Industries Ltd. These players leverage extensive global distribution networks, strong brand equity, and continuous innovation in inhaler device engineering, powder formulation technology, dose consistency, airflow optimization, and patient-centric ergonomics to address a broad spectrum of respiratory therapeutic needs.

Rising prevalence of asthma and COPD, growing exposure to air pollution, and increasing preference for propellant-free, portable inhalation therapies are driving innovation in the market. Manufacturers are focusing on smart and digitally enabled DPIs, improved drug delivery efficiency, enhanced patient adherence, and sustainable device designs, while strengthening hospital and pharmacy partnerships, expanding footprint in emerging markets, and sustaining R&D investments to deliver reliable, effective, and user-friendly inhalation solutions.

Key Industry Developments:

- In January 2026, MannKind Corporation announced that the U.S. Food and Drug Administration (FDA) approved an updated label for insulin human (Afrezza) inhalation powder, providing revised starting-dose guidance for patients with type 1 diabetes transitioning from multiple daily injections or insulin pump mealtime therapy; supported by phase 4 INHALE-3 trial data.

- In September 2024, PureIMS received a grant of €41,028.58 to initiate development of a next-generation dry powder inhaler (DPI) featuring an innovative dispersion mechanism designed to enable effective delivery of antibiotics, vaccines, and biologics; unlike existing devices, the new DPI is intended to be highly user-friendly and suitable for vulnerable populations, including children and elderly patients.

Companies Covered in Dry Powder Inhaler Market

- Boehringer Ingelheim International GmbH

- CHIESI Farmaceutici S.p.A.

- Cipla

- GSK plc.

- Hovione

- OPKO Health Inc

- Teva Pharmaceutical Industries Ltd.

- Molex®

- Otsuka Pharmaceutical Co., Ltd.

- Respira Therapeutics Inc.

- MannKind Corporation.

- Aptar.com

- Iconovo

- Harro Höfliger Verpackungsmaschinen GmbH

- Others

Frequently Asked Questions

The global dry powder inhaler market is projected to be valued at US$ 22.6 Bn in 2026.

Rising global prevalence of asthma and COPD, increasing air pollution, and growing adoption of patient-friendly inhalation therapies are driving demand for dry powder inhalers.

The global dry powder inhaler market is poised to witness a CAGR of 5.9%between 2026 and 2033.

Rapid adoption of smart/digital DPIs and expanding access to respiratory care in emerging economies create strong growth opportunities.

Boehringer Ingelheim International GmbH, CHIESI Farmaceutici S.p.A., Cipla, GSK plc., Hovione, OPKO Health Inc., and Teva Pharmaceutical Industries Ltd. are some of the key players in the dry powder inhaler market.