- Hardware & Software IT Services

- Sales Analytics Software Market

Sales Analytics Software Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Sales Analytics Software Market by Application (Sales Forecasting & Demand Planning, Pipeline Management & Opportunity Analysis, Lead Scoring & Customer Segmentation, Pricing & Discount Optimization, Sales Performance Management, Revenue Intelligence & Deal Intelligence, Others), by Organization Size (Small & Medium Enterprises, Large Enterprises), Industry, Pricing Model, by Regional Analysis, 2026 - 2033

Sales Analytics Software Market Size and Trend Analysis

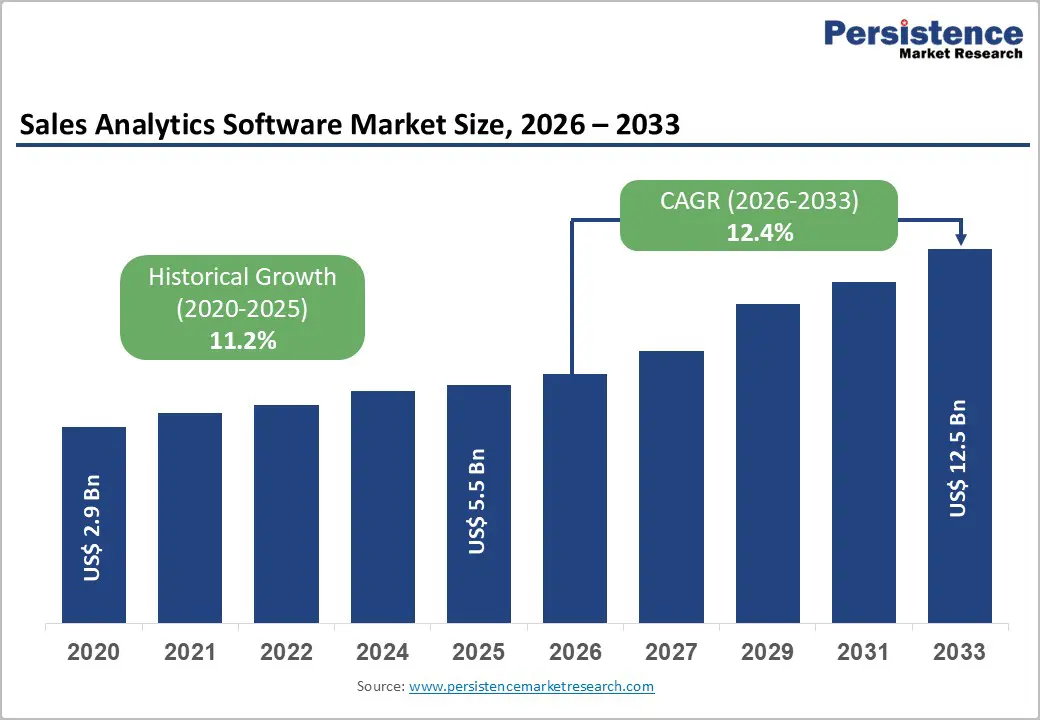

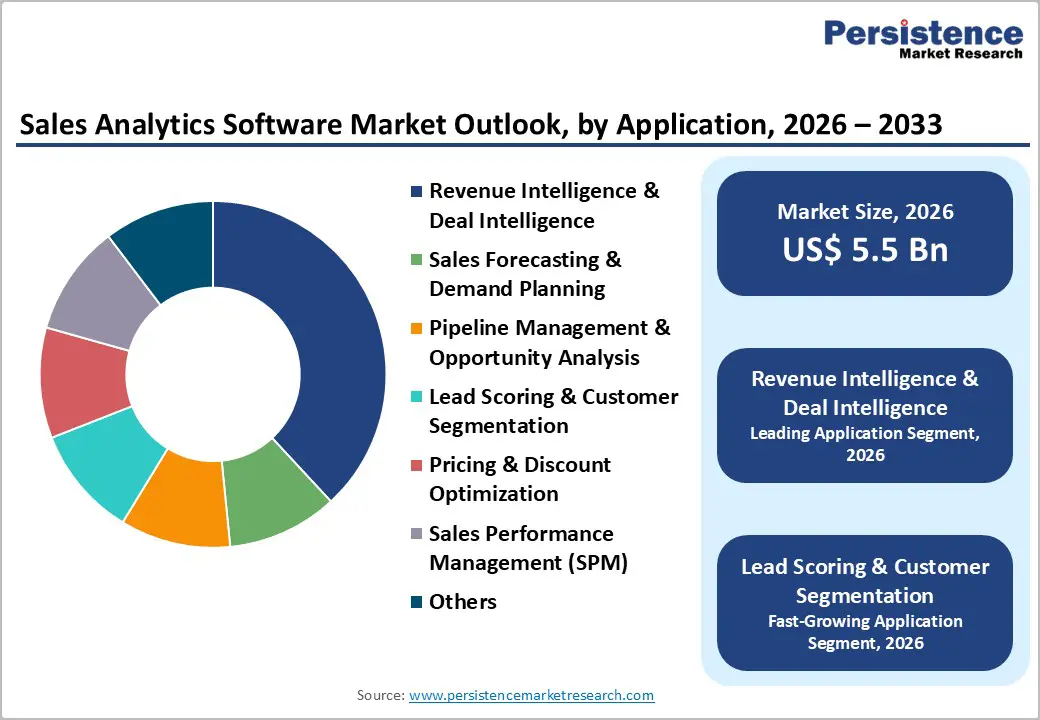

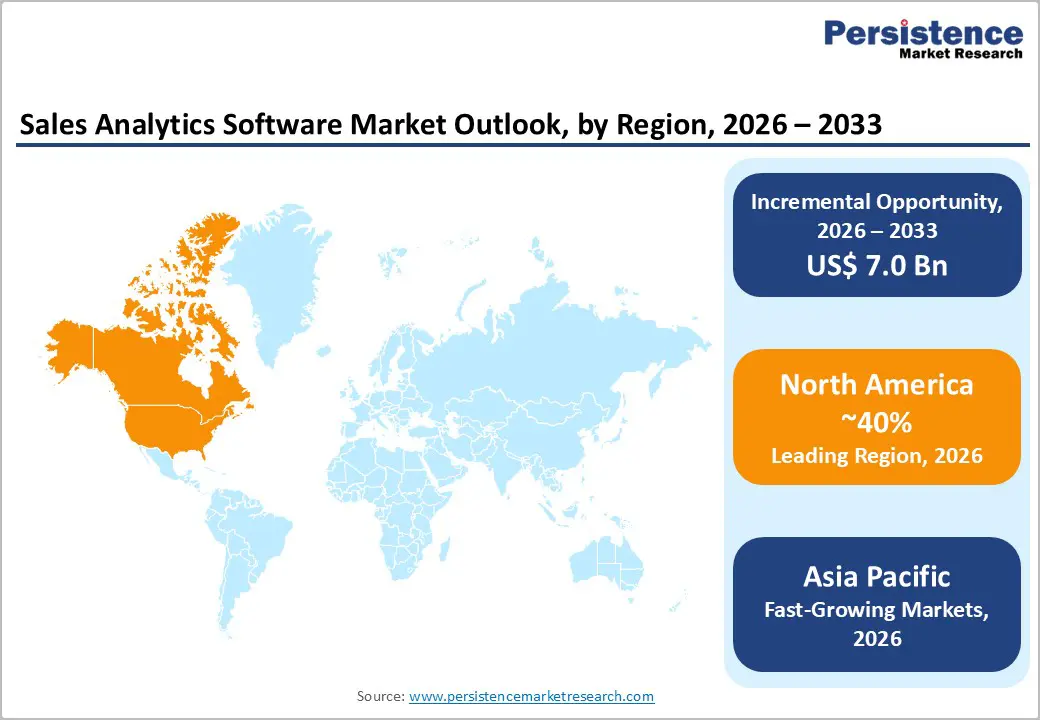

The global sales analytics software market size is expected to be valued at US$ 5.5 billion in 2026 and projected to reach US$ 12.5 billion by 2033, growing at a CAGR of 12.4% between 2026 and 2033.

The market is experiencing exceptional acceleration driven by three critical catalysts: transformative integration of artificial intelligence and machine learning algorithms enabling predictive forecasting accuracy improvements of 25-30%, growing demand for cloud-based subscription-based pricing models reducing upfront capital expenditure by 40-60% compared to traditional license fees, and pervasive digital transformation initiatives requiring real-time visibility into sales pipeline management and revenue intelligence capabilities.

Key Industry Highlights:

- Leading Region: North America remains the leading region, capturing 40% of the sales analytics software market in 2025, driven by strong enterprise software investment, advanced innovation ecosystems, and a deep organizational focus on SalesOps and digital transformation.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market, expanding at a 17.2% CAGR through 2033, driven by growth in China and India, rapid industrialization, digital infrastructure expansion, and large-scale modernization initiatives.

- Dominant Segment: Revenue Intelligence & Deal Intelligence is the dominant segment, holding a 38% share in 2025, enabling real-time pipeline visibility, predictive risk assessment, deal scoring, and enhanced sales leadership oversight.

- Fastest Growing Segment: Lead Scoring & Customer Segmentation is the fastest-growing segment, rising at 16.0% CAGR through 2033 as ML-driven behavioral analysis and automated scoring models deliver 10-20% conversion improvements.

- Key Market Opportunity: AI-powered Sales Performance Management offers the strongest market opportunity, set to grow at 15% CAGR as organizations prioritize quota optimization, compensation accuracy, and unified revenue visibility across global sales operations.

| Key Insights | Details |

|---|---|

| Sales Analytics Software Market Size (2026E) | US$ 5.5 Billion |

| Market Value Forecast (2033F) | US$ 12.5 Billion |

| Projected CAGR (2026 - 2033) | 12.4% |

| Historical Market Growth (2020 - 2025) | 11.2% |

Market Dynamics

Drivers - Widespread Digital Transformation and Cloud-Based Adoption Driving Enterprise Software Investment

Enterprise organizations across global markets are prioritizing digital transformation initiatives with an estimated 3.5% annual growth in enterprise IT investments through 2030, according to World Bank forecasts, creating substantial expansion opportunities for cloud-based sales analytics solutions. Organizations transitioning from on-premises infrastructure to cloud-based solutions benefit from subscription-based pricing models with 27% CAGR adoption among SMEs from 2025 - 2030, eliminating substantial upfront capital expenditure and enabling rapid deployment across global operations.

SalesOps market expansion reflects an organizational recognition that integrated cloud-based SalesOps solutions offering real-time analytics, seamless CRM integration, and AI-driven insights more effectively enhance forecasting accuracy and sales productivity than fragmented point solutions. Government incentives, including tax credits, subsidies, and innovation grants, further accelerate adoption, particularly among cost-sensitive SME segments that recognize return-on-investment potential within 12-18-month deployment horizons.

AI and Machine Learning Integration: Delivering Quantifiable Performance Improvements

Artificial intelligence and machine learning algorithms are fundamentally transforming sales performance metrics, with organizations implementing AI-driven forecasting engines achieving 95% forecast accuracy compared to approximately 70% accuracy using traditional statistical approaches, representing a transformative 25-percentage-point improvement. Advanced deep learning models and convolutional neural networks enable the detection of complex sales patterns and anomalies invisible to conventional rule-based systems, with 90% of companies using Clari’s AI-powered platform reporting 25% average improvement in sales pipeline visibility. Companies leveraging revenue intelligence experience a 25% increase in deal-closure rates, a 30% reduction in sales cycle time, and a 35% higher win rate, creating measurable financial returns that justify enterprise-wide software investments. Advanced predictive analytics platforms that incorporate machine learning algorithms are increasingly embedded in enterprise CRM systems, including Salesforce Einstein, Microsoft Dynamics 365 Copilot, and SAP Analytics Cloud, enabling widespread AI adoption without requiring specialized data science expertise.

Restraints - Complex Implementation Requirements and High Total Cost of Ownership Limiting Adoption

Despite compelling financial justification, adoption of sales analytics software faces substantial barriers related to implementation complexity and escalating total cost of ownership, with integration projects frequently requiring external consultants to connect sales platforms to ERP, finance, and customer-service systems, inflating deployment costs that can exceed annual license fees. Small and medium-sized enterprises face particular adoption friction when upfront implementation services rival or exceed yearly subscription fees, extending payback periods to 18-36 month timelines that exceed organizational approval thresholds for discretionary technology spending. Integration challenges with existing legacy systems, data quality issues, and the need for ongoing system maintenance create persistent operational burdens that deter cost-sensitive manufacturers and regional distributors lacking a dedicated IT infrastructure. Data migration complexity, the need for specialized workforce training, and the requirement for continuous system optimization to extract maximum analytics value create sustained demands on IT resource capacity that many organizations struggle to meet.

Data Security, Privacy Regulation Compliance, and Cybersecurity Vulnerabilities Constraining Adoption

Escalating regulatory compliance requirements, including GDPR enforcement in Europe, CCPA implementation in California, and fragmented national cybersecurity standards, create substantial compliance burdens for organizations deploying cloud-based sales analytics solutions across geographically dispersed customer bases. Organizations must navigate complex data residency requirements, encryption standards, and audit trail documentation protocols while simultaneously addressing growing cybersecurity vulnerabilities associated with expanded cloud connectivity and data exposure. Data privacy concerns, combined with the scarcity of skilled professionals proficient in data analytics and AI implementation, create significant barriers that prevent an estimated 40-50% of potential organizations from deploying advanced analytics solutions. Implementation delays stemming from regulatory compliance validation timelines, security assessments, and internal approval processes often extend software deployment to 6-12-month cycles, discouraging time-sensitive organizations that require rapid capability deployment.

Opportunity - Exceptional Growth Opportunity in AI-Powered Sales Performance Management and Real-Time Analytics Integration

Sales Performance Management (SPM) applications combined with AI-powered predictive analytics represent exceptional growth opportunities for solution providers, driven by organizations’ escalating focus on quota management accuracy, compensation optimization, and revenue visibility across complex global sales organizations. Incentive & Performance Management applications are experiencing robust expansion as enterprises recognize that AI-driven analytics enable real-time performance measurement, dynamic quota allocation based on predictive capacity modeling, and automated compensation calculations, reducing disputes and administrative overhead. This market segment is projected to expand at a CAGR of 15% through 2033, substantially exceeding the overall software market's growth rate and attracting significant venture capital investment in specialized revenue intelligence platforms, including Clari, Salesloft, Outreach, and emerging AI-native platforms that combine conversational intelligence with revenue orchestration capabilities.

Category-wise Analysis

Application Insights

Revenue Intelligence & Deal Intelligence remains the leading application segment, capturing roughly 38% of the global market in 2025 as enterprises prioritize real-time visibility into pipeline health, deal progression, and forecast accuracy. These platforms leverage conversational intelligence, call analysis, and behavioral anomaly detection to identify at-risk opportunities early, strengthen deal qualification discipline, and enhance coaching effectiveness across distributed sales teams. Organizations adopting revenue intelligence solutions report a 25-30% improvement in forecasting precision, enabling finance leaders to allocate resources confidently and supporting sales executives in setting more realistic quarterly targets informed by predictive analytics rather than manual judgment.

Organization Size Insights

Large Enterprises dominate the market with an estimated 62-68% share in 2025, reflecting significant investment capacity and the need for advanced analytics to manage complex global sales structures. Multinational corporations rely on these platforms to streamline forecasting cycles, enhance pipeline visibility across regions, and improve quota attainment through AI-driven insights. A 10% CAGR through 2033 is driven by automation initiatives aimed at reducing manual reporting workloads and cutting forecasting time by up to 70%, while supporting scalable sales operations across thousands of users with consistent data governance and performance measurement frameworks.

Industry Insights

BFSI leads the end-use landscape with approximately 32% market share in 2025, driven by stringent regulatory requirements, demand for transparent sales documentation, and the need for advanced revenue forecasting to support financial planning cycles. Banks and financial institutions increasingly adopt AI-powered analytics to optimize lead prioritization, assess customer lifetime value, and automate compliance-ready reporting. These capabilities deliver an estimated 30% improvement in sales efficiency by accelerating qualification processes and enabling data-driven decision-making for customer engagement, cross-selling, and pricing strategies aligned with profitability and retention expectations.

Pricing Model Insights

Subscription-based pricing models dominate the market, with a 72% share in 2025, as organizations shift from capital-heavy perpetual licenses to flexible SaaS deployments that offer predictable budgeting and continuous feature updates. This model is projected to grow at 16.5% CAGR through 2033, supported by widespread cloud migration, scalable user licensing, and reduced dependency on internal IT infrastructure. Subscription frameworks enable rapid adoption, seamless upgrades, and improved vendor support, making them particularly attractive for enterprises undergoing digital transformation and seeking consistent access to evolving analytics and AI capabilities without large upfront spending.

Regional Insights

North America Sales Analytics Software Market Trends

North America maintains its leadership in the global sales analytics software market with an estimated 40% share in 2025, supported by strong enterprise software spending and the presence of advanced innovation clusters across the United States. The region benefits from mature cloud adoption, a robust venture capital ecosystem, and widespread digital transformation initiatives prioritizing SalesOps efficiency, revenue intelligence deployment, and AI-driven forecasting accuracy. Large enterprises are rapidly modernizing their sales technology stacks to address persistent pipeline visibility challenges and enhance quota attainment consistency through integrated analytics platforms.

Continued migration from legacy on-premises systems to cloud-native architectures is strengthening demand for unified sales performance tools and predictive models that optimize decision-making across distributed sales organizations. Market growth at 10.5% CAGR through 2033 is further reinforced by the expansion of e-commerce, which surpassed US$1 trillion in the U.S., intensifying the need for real-time analytics, demand forecasting, and automated sales planning capabilities.

Europe Sales Analytics Software Market Trends

Europe accounts for approximately 24% of global market share in 2025, shaped by stringent regulatory frameworks such as GDPR that significantly influence technology procurement, data governance priorities, and cloud adoption strategies. Organizations increasingly prefer regional cloud infrastructure and privacy-compliant analytics platforms that ensure data residency, auditability, and strict access controls. Germany anchors regional leadership due to its strong enterprise software ecosystem and high adoption rates across manufacturing, automotive, and finance.

The United Kingdom is seeing rising adoption of advanced sales analytics to remain competitive in a digitally mature marketplace, while France, Spain, and the Nordic economies are accelerating investment through national digitalization programs and EU-supported innovation initiatives. Europe’s projected CAGR of 11.8% through 2033 is driven by regulatory harmonization and emerging frameworks like the Data Governance Act, which create standardized requirements compelling enterprises to modernize analytics infrastructure and adopt platforms built on privacy-by-design and secure data-management principles.

Asia Pacific Sales Analytics Software Market Trends

Asia Pacific represents the fastest-growing regional market, expected to expand at approximately 17.2% CAGR through 2033, driven by rapid industrialization, expanding digital infrastructure, and strong government support for enterprise technology modernization in China, India, Japan, South Korea, and Southeast Asia. China remains the largest growth engine, driven by nationwide digital transformation strategies that emphasize automation, AI adoption, and data-driven manufacturing optimization.

India demonstrates exceptional momentum, with analytics adoption growth exceeding 35%, supported by large-scale modernization across BFSI, retail, telecommunications, and IT services. Japan continues to invest heavily in advanced analytics, AI integration, and robotics-enabled sales optimization. At the same time, South Korea’s globally connected supply chain network drives demand for sophisticated revenue planning and performance management tools. Southeast Asian economies-including Vietnam, Indonesia, Thailand, and the Philippines-are emerging as manufacturing and BPO hubs, attracting multinational enterprises requiring standardized CRM systems, sales intelligence platforms, and real-time performance visibility across regional operations.

Competitive Landscape

The global sales analytics software market exhibits moderate consolidation, with a relatively small group of platform-centric vendors holding a substantial share due to their integrated ecosystems that combine CRM, analytics, cloud infrastructure, and enterprise applications. The market structure is defined by continuous expansion of end-to-end revenue platforms, where vendors compete through embedded AI capabilities, unified data models, and cross-suite workflow integration that lock customers into long-term ecosystems.

Mid-tier providers and niche innovators play an important role by offering specialized revenue intelligence, sales engagement, or AI-native analytics tools that cater to SMEs and high-growth digital-first organizations. Business strategies across the competitive landscape increasingly emphasize vertical integration of sales, marketing, and customer success analytics, alongside expansion of AI-driven automation for forecasting, pipeline visibility, and sales performance optimization. Market dynamics are further shaped by mergers, acquisitions, and strategic partnerships aimed at strengthening product breadth, accelerating AI adoption, and expanding global distribution channels.

Key Market Developments

- April 2024: Salesforce announced expanded Einstein Copilot integration within Sales Cloud incorporating advanced AI-driven forecast automation, opportunity scoring, and predictive pipeline analytics enabling 95%+ forecast accuracy for enterprise customers implementing integrated revenue cloud solutions.

- February 2024: Microsoft released Copilot for Sales, embedding generative AI directly within Dynamics 365 Sales and Outlook, enabling sales representatives to automate call transcription, opportunity analysis, and deal guidance without leaving productivity tools used daily by sales teams.

- March 2025: SoftwareOne opened new Digital Sales Hubs in Bogotá and São Paulo in collaboration with Microsoft to extend AI-driven sales support to SMEs across Americas and Europe, democratizing enterprise-grade sales analytics capabilities for cost-sensitive organizations previously priced out of premium solutions.

Companies Covered in Sales Analytics Software Market

- Salesforce

- Microsoft

- SAP

- Oracle

- IBM

- SAS Institute

- Tableau Software

- Qlik

- Zoho Corporation

- HubSpot

- Adobe

- Infor

- Teradata

- MicroStrategy

- Domo

- Clari

- Salesloft

- Outreach

- Gong

Frequently Asked Questions

The sales analytics software market is expected to reach US$ 12.5 billion by 2033, up from US$ 5.5 billion in 2026 at a 12.4% CAGR.

Adoption is driven by AI-enabled accuracy gains, cloud-based cost reductions, digital transformation needs, and sales productivity improvements.

Revenue Intelligence & Deal Intelligence leads with 38% share due to strong demand for predictive scoring and real-time pipeline visibility.

North America leads with 40% share, supported by strong enterprise software spending and advanced innovation ecosystems.

AI-powered Sales Performance Management is a major opportunity, growing at 15% CAGR.

Leading companies include Salesforce, Microsoft, SAP, Oracle, IBM, and specialized platforms including HubSpot, Clari, Salesloft, and Outreach.