- Energy Storage Solutions

- Fuel Cell for Data Center Market

Fuel Cell for Data Center Market Size, Share, and Growth Forecast, 2026 - 2033

Fuel Cell for Data Center Market by Technology Type (Solid Oxide (SOFC), Proton Exchange Membrane (PEM), Phosphoric Acid (PAFC)), Data Centre Type (Hyperscale, Colocation, Enterprise, Edge Data Centre), Power Rating (Up to 100 kW, 100-500 kW, 500 kW-1 MW, Above 1 MW), End-user (Cloud Service Providers, Telecom & Edge Networks, Enterprises (IT, Banking, Healthcare, Government), Hyperscale) and Regional Analysis for 2026 - 2033

Fuel Cell for Data Center Market Size and Trends Analysis

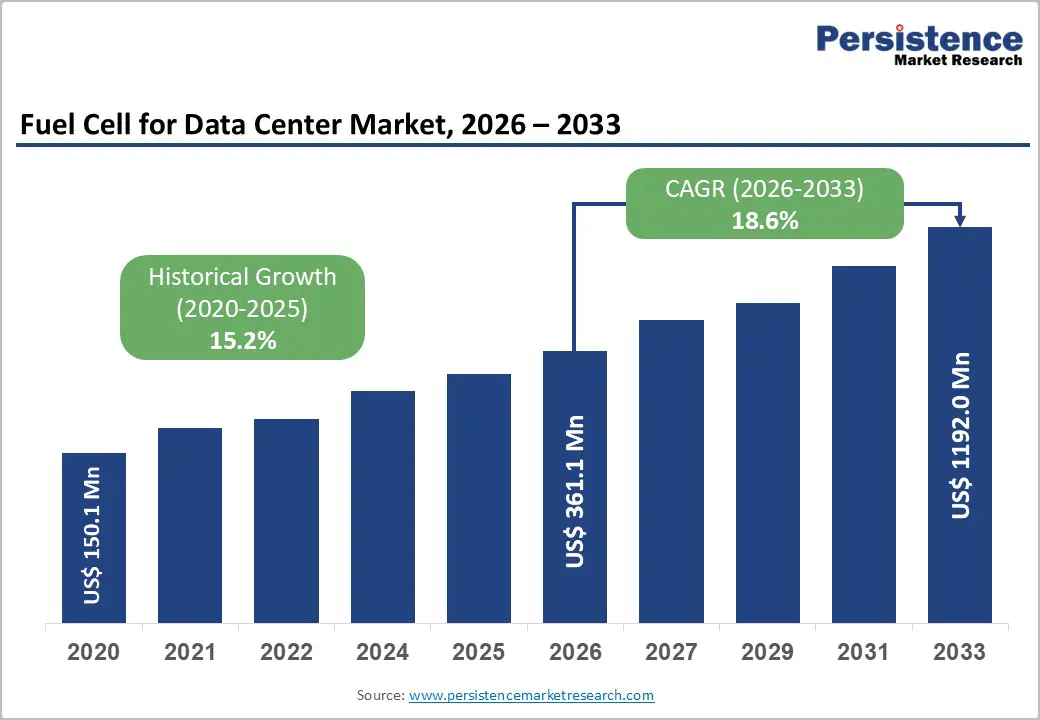

The global fuel cell for data center market size is likely to be valued at US$ 361.1 million in 2026 and is projected to reach US$ 1,192.0 million by 2033, growing at a CAGR of 18.6% between 2026 and 2033. This exceptional expansion trajectory reflects convergent macroeconomic imperatives such as exponential artificial intelligence workload growth driving data centre power demand toward 35 gigawatts of capacity announcement within five years, equivalent to over six times New York City's average annual energy consumption.

Regulatory mandates prioritizing decarbonization and zero-emission infrastructure within critical digital facilities and technological maturation enabling hydrogen fuel cell systems as viable alternatives to diesel backup generators and conventional grid connectivity.

Key Industry Highlights:

- AI and Hyperscale: Rapid expansion of AI workloads and hyperscale data centers is driving fuel cell adoption to meet high-performance, continuous power demands.

- Leading Technology: Solid oxide fuel cells dominate the market with 47.8% share in 2026, offering high efficiency and continuous baseload power for large-scale data centers.

- Fastest-Growing Technology: Proton exchange membrane fuel cells are the fastest-growing segment due to rapid start-up, responsive load-following, and auxiliary power applications.

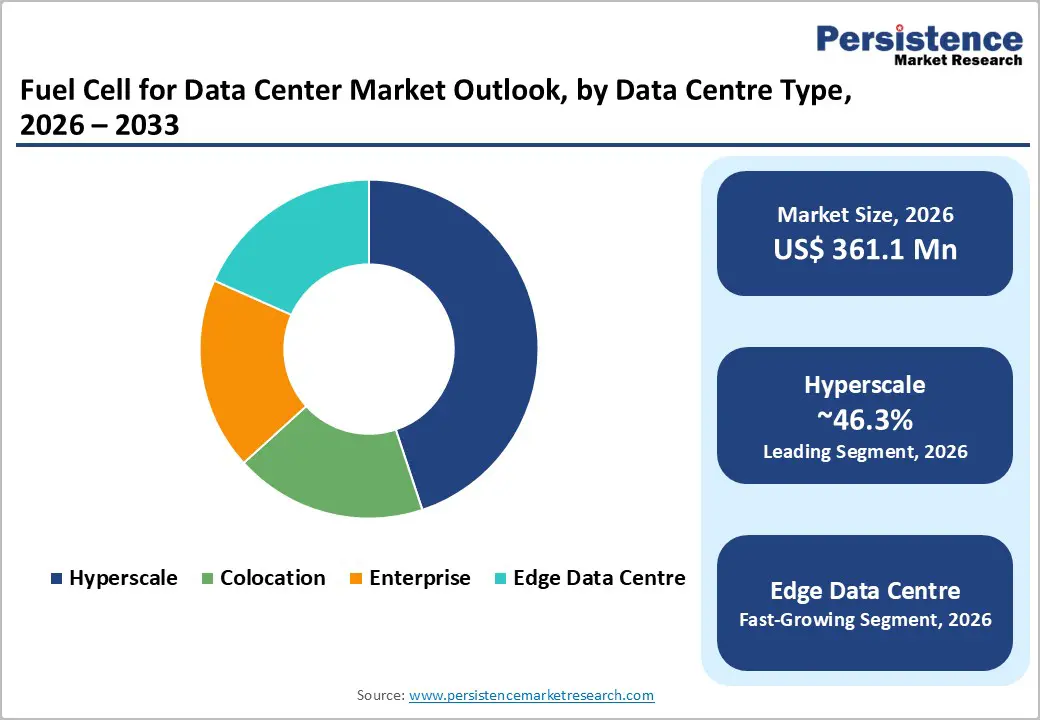

- Dominant Data Center Type: Hyperscale data centers lead with 46.3% market share in 2026, driven by multi-megawatt AI and cloud computing infrastructure investments.

- Fastest-Growing Data Center Type: Edge data centers are expanding rapidly, creating modular, resilient fuel cell deployment opportunities for distributed computing and 5G networks.

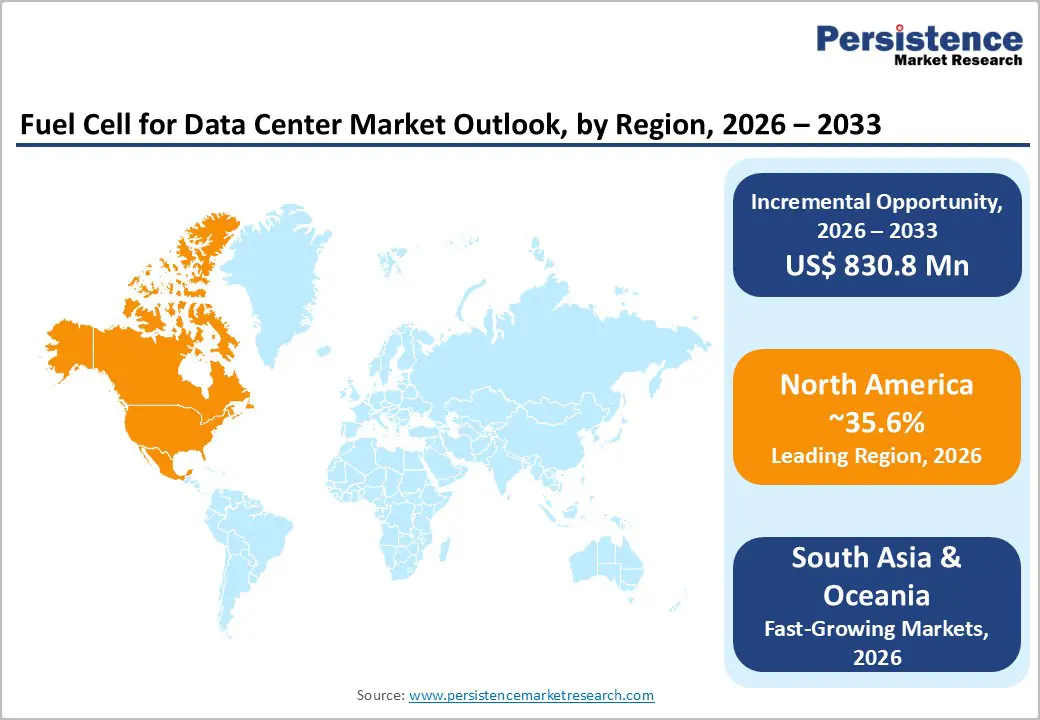

- Leading Region: North America accounts for 35.6% of market value, supported by advanced AI data centers, government incentives, and major partnerships like Bloom Energy-Oracle.

- Emerging Opportunities: Fuel cells enable data centers to participate in grid services, demand-side management, and distributed power architectures, unlocking new revenue streams while supporting decarbonization mandates.

| Key Insights | Details |

|---|---|

| Fuel Cell for Data Center Market Size (2026E) | US$ 361.1 Mn |

| Market Value Forecast (2033F) | US$ 1,192.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 18.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 15.2% |

Market Dynamics

Drivers - Artificial Intelligence Infrastructure Expansion and Hyperscale Data Center Power Requirements

Artificial intelligence workload acceleration constitutes the primary structural driver of the Fuel Cell for Data Center Market, where unprecedented computational intensity and continuous availability requirements necessitate innovative power infrastructure solutions exceeding traditional grid capacity and connection timelines. Global data center electricity consumption reached approximately 1 percent of total electricity demand in 2022, with projections exceeding 10 percent by 2030 absent interventions, reflecting exponential growth trajectories aligned with artificial intelligence model training, large language model deployment, and generative AI application proliferation across enterprise computing environments.

Bloom Energy's 2025 Data Center Power Report documents industry recognition that 35 gigawatts of data center capacity will be announced within five years, representing data center operators' acknowledgement that grid interconnection delays impose competitive and economic constraints necessitating onsite power generation alternatives.

The Fuel Cell for Data Center Market responds directly to this infrastructure requirement through rapid-deployment capabilities: Bloom Energy's July 2024 Oracle partnership enables 90-day deployment cycles, providing scalable, ultra-reliable power for large-scale artificial intelligence workloads, while FuelCell Energy's July 2025 Memorandum of Understanding with Inuverse targeting 100 megawatts deployment at AI Daegu Data Center exemplifies commercial-scale commitments to fuel cell-powered hyperscale infrastructure.

Bloom Energy's November’24 procurement agreement with American Electric Power for up to 1 gigawatt of fuel cells, the largest commercial fuel cell order in history, confirms that industry capital allocation prioritises onsite power generation solutions addressing grid capacity constraints, economic imperative for independent operations, and sustainability mandates limiting diesel generator deployment in environmentally sensitive jurisdictions.

Environmental Regulatory Transition and Decarbonization Mandates

Government decarbonization policies and emissions reduction frameworks establish a regulatory imperative driving Fuel Cell for Data Center Market adoption, particularly through increasingly stringent environmental compliance requirements restricting traditional diesel backup generator deployment in mission-critical infrastructure.

The European Union's Green Deal commits to climate neutrality by 2050, complemented by the Clean Hydrogen Strategy, establishing policy frameworks supporting hydrogen infrastructure development and deployment incentives within industrial sectors, including data centers. The Climate Neutral Data Centre Pact mandates 75 percent renewable energy utilisation by 2025 and 100 percent by 2030, creating operational imperatives for data center operators to transition toward zero-emission power sources that fuel cells enable while maintaining service reliability through dispatchable, on-demand generation capabilities.

The United States Department of Energy's H2@Scale initiative supports fuel cell research and commercial deployment through dedicated funding programs, exemplified through the November 2021 collaboration between Ballard Power Systems, Caterpillar, and Microsoft, demonstrating 1.5-megawatt hydrogen fuel cell backup power systems for data centers as documented proof of concept, validating technological feasibility and performance characteristics. Bloom Energy's fuel cell solutions deliver 34 percent lower CO2 emissions compared to displaced marginal generation resources while virtually eliminating sulfur dioxide and nitrogen oxides emissions when operating on natural gas, directly supporting data center operators' compliance obligations under increasingly stringent environmental regulatory frameworks establishing emissions thresholds and reporting requirements. The Market benefits from this regulatory transition as environmental compliance costs associated with traditional diesel generators amplify adoption economics, favouring zero-emission fuel cell systems despite higher capital requirements.

Restraint- Hydrogen Infrastructure Immaturity and Fuel Supply Constraints

Hydrogen infrastructure development lags demand trajectory, with limited availability of competitively priced clean hydrogen supply constraining widespread fuel cell deployment, particularly in regions lacking established hydrogen production, distribution, and refuelling infrastructure. Hydrogen supply chain establishment requires sustained capital investment in electrolysis facilities, production capacity development, and distribution pipeline infrastructure, with cost-competitive hydrogen availability remaining elusive in most geographic markets despite government support programs.

Data center operators require guaranteed hydrogen supply agreements supporting 24/7 continuous operations, necessitating long-term contracts and infrastructure development commitments beyond individual facility requirements, creating collective action challenges limiting adoption scaling until regional hydrogen economies achieve threshold mass supporting competitive pricing and reliable supply.

Opportunity - Edge Data Center Proliferation and Distributed Power Architectures

Edge data center expansion supporting Internet of Things, 5G telecommunications infrastructure, and localised computing creates specialised opportunities for fuel cell deployment, providing independent, resilient power solutions where grid connectivity remains unavailable, unreliable, or economically prohibitive. Telecommunications infrastructure resilience requirements reflected in India's telecom sector, supporting 1.21 billion subscribers, 979 million internet connections, and expanding 5G networks, contributing nearly 25 percent of wireless data usage by FY25, drive demand for distributed backup power solutions supporting critical communication network reliability throughout network outages and operational disruptions.

The fuel cell for data center market expansion into edge data centers addresses unmet customer needs for modular, rapidly deployable power solutions supporting decentralised computing architectures aligned with next-generation 5G infrastructure, autonomous vehicle control systems, and smart city digital platforms requiring local processing and immediate response capabilities incompatible with centralised hyperscale data center models.

SFC Energy AG's June 2025 deployment of 235 kilowatts of hydrogen fuel cell capacity for telecommunications infrastructure supporting fibre-optic point-of-presence stations exemplifies a practical edge data center application addressing critical network infrastructure reliability through clean, zero-emission backup power solutions compatible with environmental regulations and sustainability objectives. Government initiatives supporting distributed renewable energy systems, including India's BharatNet project targeting optical fibre connectivity for 42,000 uncovered Gram Panchayats and rural fibre connection expansion, create complementary infrastructure investments positioning fuel cells as complementary technology supporting energy-resilient digital platforms.

Grid Services and Demand-Side Management Revenue Models

Hydrogen fuel cells enable data centers to participate in advanced grid services and demand-side management programs, transforming facilities from energy consumers into grid-supporting resources capable of providing frequency regulation, voltage support, and load-balancing services, generating additional revenue streams justifying fuel cell capital investment. Bidirectional power flow capabilities enable energy storage during low-cost renewable generation periods and power injection during high-cost peak demand periods, creating virtual power plant architectures that enhance grid stability while monetising excess generation capacity through demand response markets.

The fuel cell for data center market opportunity encompasses emerging business models where data center operators partner with utilities and grid operators to provide frequency regulation, voltage stability, and peak-load management services, with fuel cell systems providing dispatchable generation capability supporting grid resilience during peak demand periods or renewable generation shortfalls. Microsoft's documented green hydrogen pilot projects and Bloom Energy's grid-support capability integration exemplify emerging operational models where data centers function as grid assets rather than passive consumers, creating stakeholder value alignment between data center operators, utilities, and renewable energy providers supporting broader energy transition objectives aligned with climate change mitigation requirements.

Category-wise Analysis

Technology Type Insights

Solid oxide fuel cells maintain market leadership at 47.8% share in 2026, reflecting technology maturity, exceptional efficiency characteristics, and proven commercial deployment record, establishing SOFC as the preferred technology for large-scale data center applications requiring continuous baseload power and thermal integration supporting cooling system requirements.

Solid oxide fuel cell technology operates at elevated temperatures, enabling fuel flexibility encompassing hydrogen, natural gas, ammonia, biogas, methanol, and syngas operation, allowing data center operators to adapt fuel sourcing to regional availability and economic dynamics while maintaining long-term capability for renewable hydrogen transition as hydrogen infrastructure develops. Stack-level electrical efficiency reaching 75 percent, combined with 90 percent total system efficiency through integrated combined heat and power systems, delivers operational cost advantages compared to conventional backup generators and alternative fuel cell technologies, with waste heat recovery systems enabling comprehensive data center energy optimisation through absorption chilling, rack cooling, and facility climate control integration.

Proton exchange membrane fuel cells represent the fastest-expanding technology segment, driven by rapid start-up capability, responsive load-following performance, and suitability for dynamic power delivery applications supporting variable artificial intelligence workload profiles characteristic of modern data center operations. Proton exchange membrane fuel cells operate at lower temperatures, enabling faster system response to load changes, quick-start capabilities supporting uninterruptible power system integration, and flexibility compatible with diverse backup power and supplementary generation applications requiring instantaneous response to operational demand fluctuations.

Plug Power's November 2025 initial data center sector entry through letters of intent for backup and auxiliary power solutions exemplifies emerging market focus on proton exchange membrane technology, with operational strategy emphasising auxiliary power applications and backup system roles supporting market penetration in facility segments valuing quick-start capabilities and responsive performance over continuous baseload operation requirements characteristic of hyperscale primary power applications dominated by SOFC technology.

Data Centre Type Insights

Hyperscale data centers command 46.3% market share in 2026, reflecting infrastructure capital intensity, sophisticated power management architecture, and strategic importance supporting artificial intelligence computation and cloud computing services, where fuel cell deployment addresses grid connectivity constraints and economic imperatives for independent operations.

Hyperscale data center operators, including Amazon Web Services, Microsoft Azure, Google Cloud, and Alibaba Cloud, drive a substantial portion of the fuel cell market value through multi-megawatt procurement commitments, proven procurement volume enabling supply chain development, and strategic partnerships establishing reference deployments validating technology viability for industry peers.

The hyperscale segment benefits from established regulatory relationships, procurement sophistication enabling technology risk assessment and mitigation, and sufficient capital resources supporting fuel cell infrastructure investment despite premium pricing relative to conventional diesel alternatives.

Edge data centers represent the fastest-expanding segment, driven by Internet of Things proliferation, 5G telecommunications infrastructure deployment, and distributed computing architectures requiring independent, resilient power solutions where grid connectivity remains unavailable, unreliable, or economically prohibitive. Edge data center power requirements ranging from sub-kilowatt applications in remote sensor networks to multi-megawatt telecommunications data centers supporting 5G baseband processing create diverse market opportunities across equipment scales supported by modular fuel cell system architecture enabling scalable deployment from 200 kilowatts to multi-megawatt installations.

Regional Insights and Trends

North America Fuel Cell For Data Center Market Trends

North America is a dominant market accounting for 35.6% of global value, characterized by advanced data center infrastructure, sophisticated technology procurement capabilities, and policy environments supporting hydrogen technology development and fuel cell deployment incentives. The United States market reflects corporate sustainability commitments among hyperscale cloud operators, government support through U.S. Department of Energy H2@Scale initiatives, and state-level incentives in California and New York, encouraging low-carbon distributed generation systems through regulatory credits and fiscal benefits supporting clean energy transition objectives.

Major technology partnerships anchor regional market leadership: Bloom Energy and Brookfield's $5 billion strategic partnership establishing preferred onsite power status for global AI factories, Bloom Energy and Oracle Cloud Infrastructure's 90-day rapid deployment partnership, and Bloom Energy's American Electric Power procurement agreement for 1 gigawatt capacity deployment targeting AI data centers demonstrate concentrated capital deployment toward fuel cell infrastructure within the region. Ballard Power Systems, Caterpillar, and Microsoft's three-year hydrogen fuel cell demonstration project, supported by U.S. Department of Energy funding, exemplified commitment to technology validation and commercial pathway development.

East Asia Fuel Cell For Data Center Market Trends

East Asia accounts for 28% of the global fuel cell for data center market value, driven by China's digital economy expansion, South Korea's hydrogen technology focus, and Japan's clean energy policy framework supporting fuel cell infrastructure development. South Korea emerges as a regional technology leadership center, with Doosan Fuel Cell's mass production commencement using Ceres Power's solid oxide technology at a dedicated South Korea facility, representing major manufacturing capacity expansion supporting regional deployment scaling. FuelCell Energy's July’25 Memorandum of Understanding with Inuverse targeting 100 megawatt deployment at AI Daegu Data Center, combined with Doosan Fuel Cell and SK Ecoplant partnership for hydrogen fuel cell-based power solutions, emphasising integrated baseload power, gas engine load-following, and waste-heat cooling integration, establishes Korea as an accelerating market for fuel cell technology adoption, supporting AI infrastructure expansion.

Japan's 5G expansion and artificial intelligence computing workload growth drive data center fuel cell adoption, with government subsidies for clean energy and Japan's hydrogen-first energy roadmap providing policy support for technology investment. China's digital ecosystem expansion to 1.108 billion internet users, extensive 5G infrastructure deployment, and dual carbon policy emphasising decarbonization across industrial sectors create market opportunity for fuel cell technology deployment within data center and distributed power generation applications.

Europe Fuel Cell For Data Center Market Trends

Europe represents 18% of the global market, characterized by stringent environmental regulations, high electricity costs supporting onsite power generation economics, and policy frameworks emphasizing hydrogen infrastructure development and decarbonization targets. The European Union's Green Deal, establishing a climate neutrality objective by 2050, combined with the Clean Hydrogen Strategy, providing policy frameworks and investment incentives, creates a regulatory environment supporting fuel cell technology adoption within data centre infrastructure aligned with decarbonization mandates.

Key consuming countries, including Germany, the Netherlands, France, and the Nordic region, demonstrate regional technology leadership through policy support, hydrogen infrastructure investment, and data center operator engagement with fuel cell technology. The Climate Neutral Data Centre Pact mandates 75 percent renewable energy utilisation by 2025 and 100 percent by 2030, establishing operational imperatives driving data center operators toward fuel cell adoption, supporting sustainability compliance while maintaining service reliability through dispatchable generation.

Competitive Landscape

The global fuel cell for data center market is largely consolidated and oligopolistic, dominated by a few key players such as Bloom Energy, FuelCell Energy, Plug Power Inc., Ballard Power Systems, Doosan Fuel Cell, and SFC Energy AG. These companies lead through technological expertise, reliable and scalable fuel cell solutions, and strategic partnerships with hyperscale cloud providers and enterprises.

High entry barriers, including capital intensity and regulatory requirements, limit new competitors, keeping the market concentrated. Innovations in SOFC, PEM, and PAFC fuel cells allow differentiation in efficiency and uptime. While smaller regional players exist, they hold minimal market share, focusing on niche applications like edge data centers.

Key Developments:

- In July 2025, FuelCell Energy signed a strategic Memorandum of Understanding (MOU) with Inuverse to explore deploying up to 100 MW of fuel cell-based power at the AI Daegu Data Center in Korea. The collaboration aims to integrate FuelCell Energy’s clean, high-efficiency fuel cell platforms with thermal energy for advanced rack cooling and absorption chilling, reducing operational costs and improving energy efficiency. This initiative highlights the company’s rapid deployment capabilities and reinforces its role in supporting hyperscale and AI-focused data centers while advancing sustainable, low-emission digital infrastructure in the region.

- In October 2025, Bloom Energy announced a $5 billion strategic partnership with Brookfield to become the preferred onsite power provider for Brookfield’s global AI factories. The collaboration will deploy Bloom Energy’s advanced fuel cell technology to deliver reliable, scalable, and clean power for AI-focused data centers, addressing the growing compute and energy demands of the AI era. This partnership underscores the critical role of fuel cells in enabling rapid deployment, grid-independent operation, and sustainable digital infrastructure for hyperscale and enterprise AI data centers worldwide.

Companies Covered in Fuel Cell for Data Center Market

- Bloom Energy

- FuelCell Energy

- Plug Power Inc.

- Ballard Power Systems

- Doosan Fuel Cell

- SFC Energy AG

- Ceres Power Holdings plc

Frequently Asked Questions

The global Fuel Cell for Data Center Market is projected to be valued at US$ 1.3 Mn in 2026.

The Hyperscale segment is expected to account for approximately 46.3% of the global Fuel Cell for Data Center Market by Data Centre Type in 2026.

The market is expected to witness a CAGR of 18.6% from 2026 to 2033.

The Fuel Cell for Data Center Market is primarily driven by the rapid expansion of AI workloads and hyperscale data centers, coupled with decarbonization mandates and the need for reliable, on-site, zero-emission power solutions.

Key opportunities in the Fuel Cell for Data Center Market lie in edge data center expansion and distributed power architecture, enabling resilient, zero-emission local power, and participation in grid services and demand-side management for additional revenue streams.

Key players in the Fuel Cell for Data Center Market include Bloom Energy, FuelCell Energy, Plug Power Inc., Ballard Power Systems, Doosan Fuel Cell, and SFC Energy AG.