- Advanced Materials

- Composite Pipes Market

Composite Pipes Market Size, Share, and Growth Forecast, 2026 - 2033

Composite Pipes Market by Diameter Type (Small Diameter (up to 6 inches), Medium Diameter (6 to 24 inches), Large Diameter (above 24 inches)), Application (Oil & Gas Transportation, Others), and Regional Analysis for 2026 - 2033

Composite Pipes Market Size and Trends Analysis

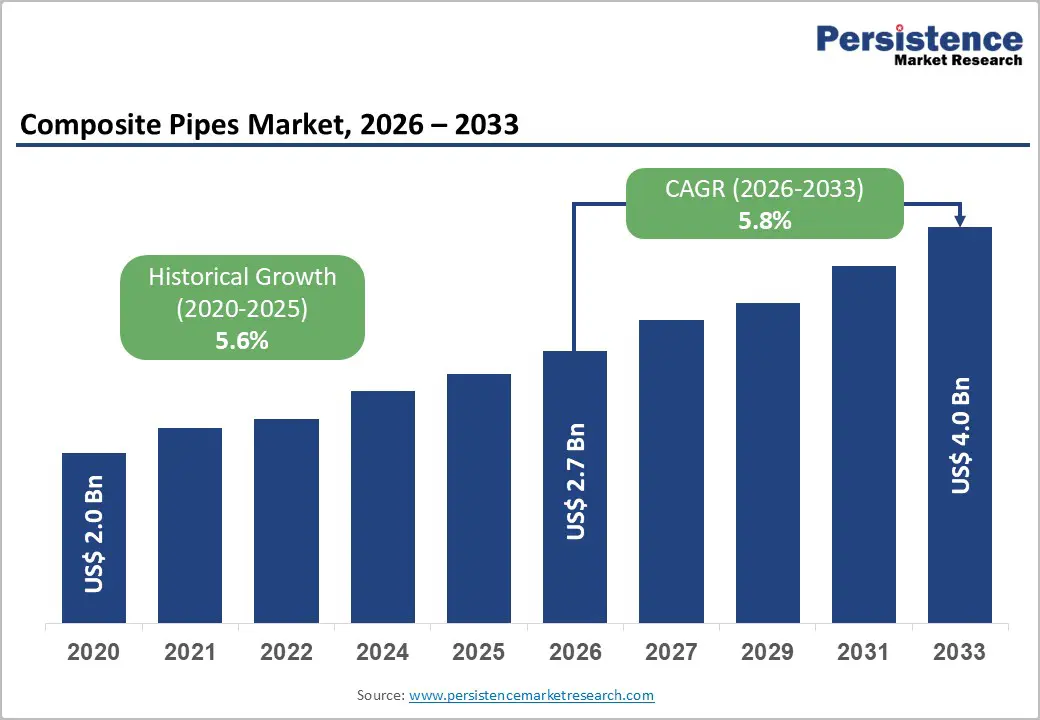

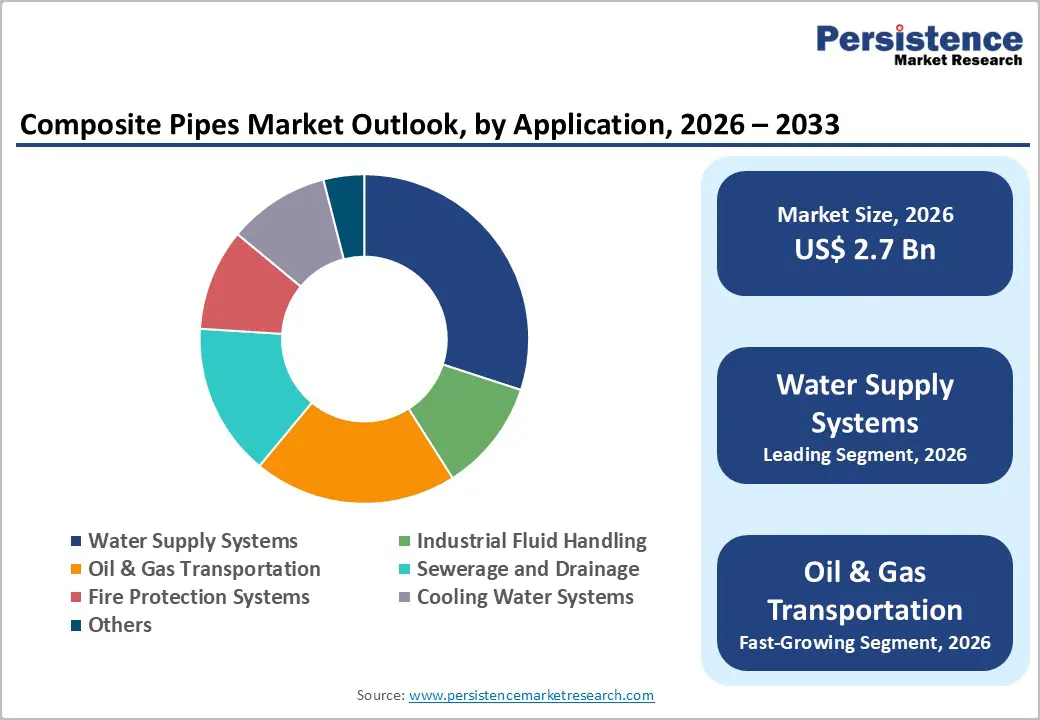

The global composite pipes market size is likely to be valued at US$2.7 billion in 2026 and is expected to reach US$4.0 billion by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033, driven by their superior corrosion resistance, longer service life, and lower lifecycle costs, particularly in water & wastewater infrastructure, oil & gas transportation, and industrial fluid handling.

Rising investments in urban water supply, sewerage networks, desalination plants, and district cooling systems are significantly increasing demand, especially in emerging economies. Technological advancements in resin systems (vinyl ester, epoxy) and fiber reinforcements (glass and carbon fibers) are enhancing pressure tolerance, chemical resistance, and installation efficiency, accelerating adoption across chemical processing and power generation industries.

Key Industry Highlights:

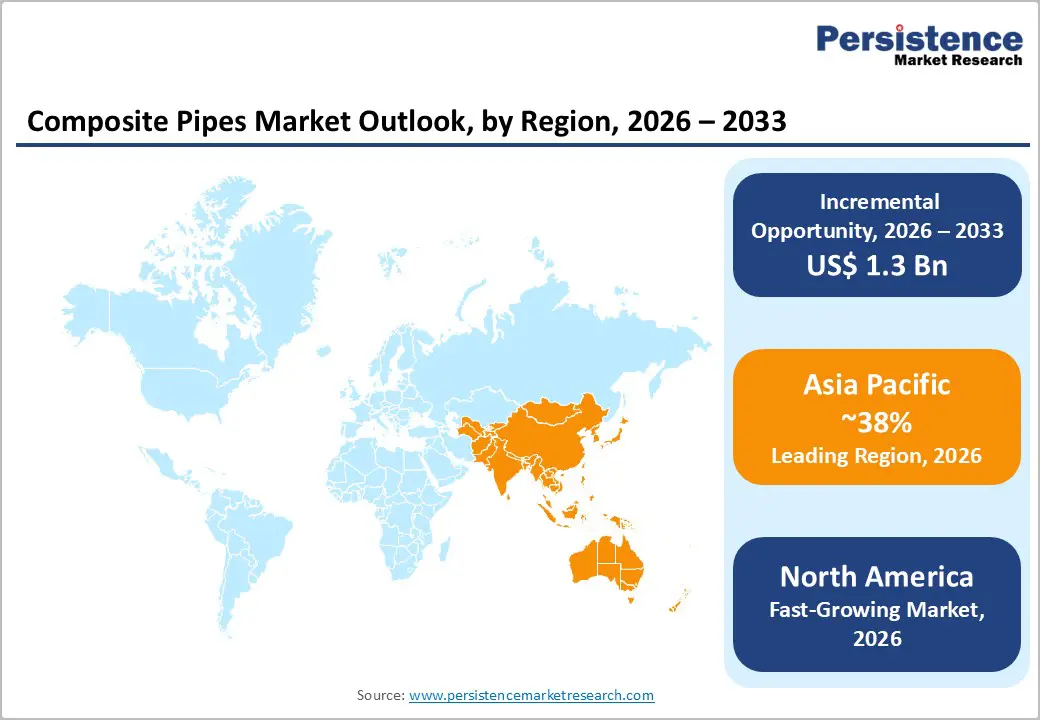

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by rapid urbanization, large-scale water and wastewater infrastructure development, and expanding oil & gas and power generation projects in sustainable piping solutions across China, India, and Japan.

- Fastest-growing Region: North America is likely to be the fastest-growing region for composite pipes in 2026, driven by strong demand from the oil & gas and water management sectors, major infrastructure upgrades, stringent environmental regulations, advanced technological adoption, and sustained investments in sustainable wastewater and utility projects.

- Leading Diameter Type: The medium diameter segment (6 to 24 inches) is projected to represent the leading diameter type in 2026, accounting for 35% of the revenue share, driven by its extensive use in municipal water supply and industrial fluid handling applications.

- Leading Application: Water supply systems are anticipated to be the leading application type, accounting for over 30% of the revenue share in 2026, owing to increasing investments in sustainable urban water infrastructure and the need for corrosion-resistant piping solutions.

| Key Insights | Details |

|---|---|

|

Composite Pipes Market Size (2026E) |

US$2.7 Bn |

|

Market Value Forecast (2033F) |

US$4.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Demand in Water and Wastewater Management

Governments and utilities worldwide focus on upgrading aging water infrastructure and expanding access to safe drinking water. Rapid urbanization, population growth, and industrial expansion are placing significant pressure on existing water distribution and sewage networks, leading to higher investment in durable piping solutions. Composite pipes are increasingly preferred in water and wastewater applications due to their excellent corrosion resistance, long service life, low leakage rates, and reduced maintenance requirements compared to traditional metal pipes. Their lightweight nature also lowers transportation and installation costs, making them suitable for large-scale municipal projects and underground installations.

The emphasis on water conservation, wastewater reuse, and desalination is accelerating the adoption of composite piping systems. Stricter environmental regulations and sustainability mandates are encouraging utilities to replace deteriorating pipelines that contribute to water losses and contamination. Composite pipes offer superior resistance to aggressive wastewater chemicals, biofouling, and fluctuating pressures, ensuring consistent performance over decades. Their ability to support high flow efficiency further enhances operational reliability in treatment plants, pumping stations, and transmission networks, making them a critical component in modern water and wastewater infrastructure development.

Need for Specialized Installation Expertise

Composite pipes require more advanced handling and installation practices compared to conventional metal or plastic alternatives. Composite pipes often involve specific joining methods, such as adhesive bonding, mechanical couplings, or filament-wound connections, which demand trained technicians and strict adherence to installation standards. Inadequate installation can compromise pressure resistance, joint integrity, and long-term performance, increasing the risk of leaks or premature failure. This creates hesitation among project developers, particularly for municipal and industrial projects operating under tight budgets and timelines.

The reliance on skilled labor, specialized tools, and certified installation procedures raises upfront project costs, limiting adoption in cost-sensitive and emerging markets. Smaller contractors and rural infrastructure projects may lack access to trained installers or technical support, further restricting market penetration. While composite pipes deliver lower lifecycle costs through reduced maintenance and corrosion resistance, the initial complexity of installation can delay decision-making and extend project schedules. Despite their long-term operational benefits, the requirement for specialized installation expertise continues to challenge widespread adoption, especially in regions with limited technical training infrastructure.

Growth in Chemical Processing and Oil & Gas

Oil & gas industries increasingly operate in highly corrosive, high-pressure, and high-temperature environments. Conventional metal pipes are prone to corrosion, scaling, and fatigue, leading to frequent maintenance and costly shutdowns. Composite pipes, with their excellent chemical resistance, high strength-to-weight ratio, and superior fatigue performance, provide a reliable alternative for handling aggressive chemicals, hydrocarbons, sour gas, and saline fluids. These characteristics make them particularly suitable for refineries, petrochemical complexes, offshore platforms, and onshore transmission networks.

Rising energy demand, expansion of petrochemical capacities, and increased investments in offshore and unconventional oil & gas projects are accelerating the need for durable and low-maintenance piping solutions. Regulatory emphasis on operational safety and environmental protection is further encouraging the adoption of composite pipes, which offer reduced leakage risk and longer service life. In chemical processing plants, composite piping systems support continuous operations by minimizing corrosion-related failures and downtime. The increasing focus on efficiency, safety, and lifecycle cost reduction in chemical and oil & gas infrastructure is expected to drive strong adoption of composite pipes across upstream, midstream, and downstream applications.

Category-wise Analysis

Diameter Type Insights

The medium-diameter composite pipes segment (6 to 24 inches) is expected to lead the composite pipes market, accounting for approximately 35% of total revenue in 2026, driven by its wide applicability across municipal water supply, wastewater networks, and industrial fluid-handling systems. These pipes offer an optimal balance between flow capacity, pressure handling, and installation flexibility, making them the preferred choice for urban and industrial infrastructure projects. Their corrosion resistance and long service life significantly reduce leakage losses and maintenance costs compared to traditional metal pipes. For example, municipal water distribution networks, where medium-diameter composite pipes are extensively used for transmission and distribution lines, ensure reliable performance under varying pressure conditions.

The large-diameter composite pipes segment (above 24 inches) is likely to be the fastest-growing in 2026, driven by rising demand from large-scale infrastructure projects requiring high-volume fluid transmission. Growth is supported by increasing investments in long-distance water transfer, sewerage systems, desalination plants, and oil & gas transportation networks, where large-diameter pipelines are essential. Composite pipes in this category offer superior strength, corrosion resistance, and lightweight advantages, enabling easier installation compared to steel alternatives. For example, desalination and bulk water transmission projects, where large-diameter composite pipelines are used to transport treated water over long distances with minimal pressure loss and reduced maintenance.

Application Insights

The water supply systems segment is projected to lead the market, capturing around 30% of the total revenue share in 2026, driven by continuous investments in drinking water infrastructure and pipeline replacement programs. Aging metal pipelines are increasingly being replaced with composite alternatives due to their resistance to corrosion, biofouling, and chemical degradation, thereby improving water quality and reducing non-revenue water losses. Composite pipes also offer longer service life and lower lifecycle costs, making them economically attractive for municipalities. For example, urban water distribution upgrades, where composite pipes are widely used to modernize old networks and meet growing demand from expanding cities.

The oil & gas transportation segment is likely to be the fastest-growing application in 2026, driven by increasing exploration activities, pipeline expansion, and the need for durable materials in harsh operating environments. Composite pipes offer high-pressure tolerance, excellent resistance to hydrocarbons, and superior performance in corrosive and offshore conditions compared to conventional steel pipes. These properties reduce maintenance frequency and improve operational safety. For example, offshore oil and gas pipelines, where composite pipes are increasingly deployed to handle corrosive fluids and dynamic loads while reducing installation weight and costs.

Regional Insights

North America Composite Pipes Market Trends

North America is likely to be the fastest-growing region in 2026, driven by infrastructure renewal and performance requirements, particularly in water & wastewater and oil & gas sectors, as utilities and industries increasingly replace aging steel and concrete pipelines with corrosion-resistant composite solutions. Municipal water authorities across states such as California, Texas, and Florida are awarding a growing share of pipeline contracts to composite pipes due to their long service life and lower lifecycle costs, with utilities focusing on reducing leakage and maintenance expenses in existing networks. Smart monitoring and fiber-reinforced technologies are also being integrated into new installations, improving real-time performance tracking and predictive maintenance, which supports demand for high-value composite solutions in urban infrastructure projects.

Leading manufacturers are actively innovating to capitalize on regional demand, with companies such as Enduro Composites expanding their product portfolios to offer high-pressure, corrosion-resistant FRP pipe systems designed specifically for North American industrial and energy applications. These advancements help manufacturers comply with stringent environmental and safety regulations, particularly in oil and gas transportation and chemical processing. Ongoing investments in infrastructure modernization and regulatory compliance are expected to continue driving demand across municipal and industrial sectors.

Europe Composite Pipes Market Trends

Europe is likely to be a significant market for composite pipes in 2026, due to strict environmental regulations, aging infrastructure replacement, and the adoption of sustainable materials. EU initiatives such as the Green Deal and circular economy policies are encouraging investments in water distribution, wastewater management, and industrial piping systems that prioritize durability and environmental performance. Regulatory frameworks, including the EU’s drinking water directive, support the use of long-life, low-maintenance piping solutions, making composite pipes an attractive choice for municipal and industrial networks.

The increasing use of composite pipes in offshore energy and subsea applications, where robust, corrosion-resistant materials are critical. REHAU Group, a leading European manufacturer, has expanded its portfolio of FRP and multilayer composite pipes specifically for water and industrial applications, highlighting the shift toward high-performance, sustainable piping solutions. Innovations in composite formulations and installation techniques are enabling tailored solutions for complex infrastructure projects, reinforcing Europe’s position as a market focused on quality, compliance, and sustainability.

Asia Pacific Composite Pipes Market Trends

The Asia Pacific region is expected to be the leading region, accounting for 38% in 2026, driven by rapid urbanization, extensive infrastructure development, and rising industrial investments in China and India. Rapid expansion of municipal water supply, sewerage networks, and industrial fluid handling infrastructure is increasing demand for corrosion-resistant and long-lasting composite pipes. Governments in countries such as China and India are rolling out large-scale pipeline initiatives to modernize water distribution and wastewater systems, which supports strong uptake of composite piping solutions over traditional materials due to their durability and lower lifecycle costs.

The growing use of advanced composite technologies in energy and offshore applications, where lightweight and high-strength pipes are increasingly required for oil & gas transportation and deepwater projects. In the Asia Pacific region, Strohm’s partnership with Malaysia’s Petronas Technology Ventures demonstrates increasing commercial adoption of thermoplastic composite pipes (TCPs), where the companies have collaborated to qualify and deploy TCP technology for oil & gas flowlines in Sarawak waters, highlighting the shift toward corrosion-resistant, low-weight composite solutions in regional energy infrastructure.

Competitive Landscape

The global composite pipes market exhibits a moderately fragmented structure, driven by the presence of both large multinational manufacturers and specialized regional players investing in innovation, expanded production capacity, and application-specific solutions to meet rising demand across water & wastewater, oil & gas, and industrial sectors. This structure is influenced by the capital-intensive nature of composite material production, stringent quality and certification requirements, and the need for strong distribution networks to support infrastructure projects.

With key players such as TechnipFMC, National Oilwell Varco (NOV), Baker Hughes, Future Pipe Industries (FPI), and Amiblu Holding (Flowtite), the competitive landscape is shaped by companies that capitalize on strong R&D capabilities, integrated supply chains, and strategic partnerships to secure large-scale contracts across energy, water management, and industrial sectors. Competition centers on innovation in materials and manufacturing technologies, including advanced composite solutions, along with the expansion of regional production capacities, strategic collaborations, and enhanced service offerings. These strategies enable companies to differentiate their portfolios while addressing growing customer demands for durability, performance, and sustainability in composite piping systems.

Key Industry Developments:

- In January 2025, Strohm, a leading provider of Thermoplastic Composite Pipes (TCP), launched TCP Designer™, a web-based tool that simplifies TCP system design. It enabled engineers to quickly assess water depth, pressure, temperature, and installation requirements, and generate datasheets with size, weight, stiffness, and bend radius. The tool reduced the design time, supported the adoption of lightweight, corrosion-resistant TCP solutions, and allowed independent pipeline design with access to Strohm’s engineering support, accelerating TCP use in offshore, oil & gas, water, and industrial projects.

- In November 2024, Composite Piping Technology (CPT) launched a new state-of-the-art facility in Kilgore, Texas, to produce MaxDR™, the world’s first large-diameter, high-pressure fusible composite HDPE pipe. The plant can manufacture up to 300 miles of 12”-24” pipes with operating pressures of 350, 550, and 750 psi, offering two to three times higher pressure capacity than conventional HDPE. MaxDR™ provides cost-effective, high-performance solutions for oil & gas, industrial, mining, water, and wastewater applications, while generating local employment and supporting infrastructure growth.

Companies Covered in Composite Pipes Market

- KiTEC

- Vasitars

- Jindal Pex Tubes

- Akiet

- KISAN

- Cerro Flow Product

- Furukawa Electric

- Cambridge-Lee

- SH Copper

- Wieland-Werke

Frequently Asked Questions

The global composite pipes market is projected to reach US$2.7 billion in 2026.

The composite pipes market is driven by increasing demand for corrosion-resistant, durable, and low-maintenance piping solutions across water, wastewater, oil & gas, and industrial sectors.

The composite pipes market is expected to grow at a CAGR of 5.8% from 2026 to 2033.

Key market opportunities include expanding chemical processing activities, increased oil and gas transportation requirements, rising investments in desalination and wastewater management projects, and the development of large-scale industrial and infrastructure facilities.

KiTEC, Vasitars, Jindal Pex Tubes, Akiet, KISAN, and Cerro Flow Products are the leading players.