- Plastics, Polymers & Resins

- Biocomposites Market

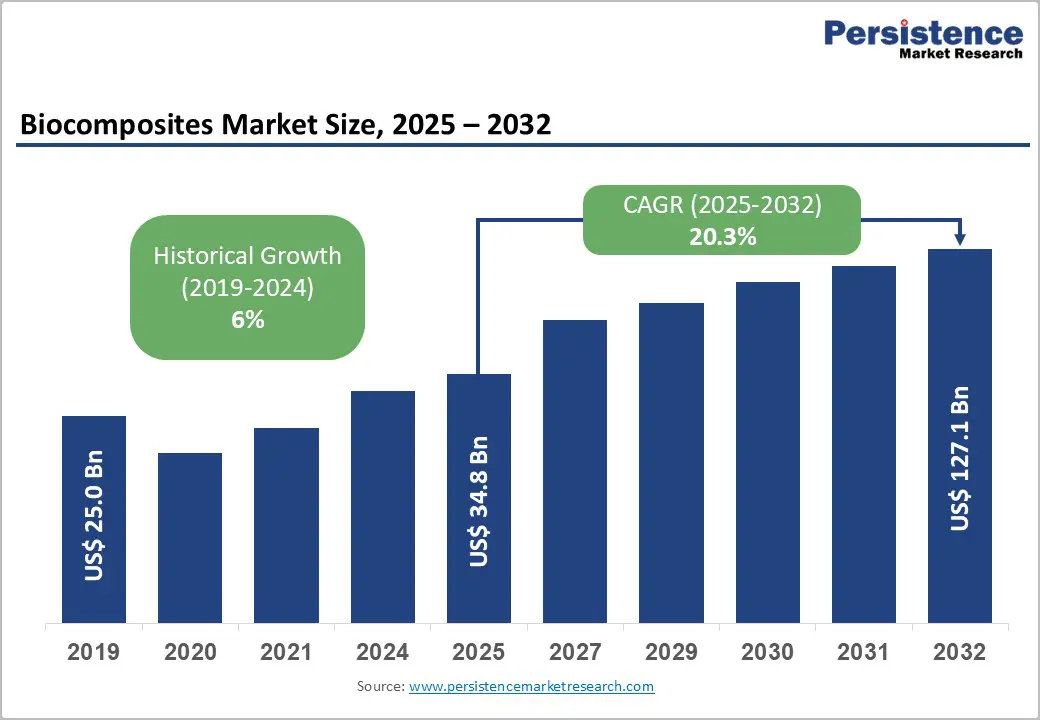

Biocomposites Market Size, Share, and Growth Forecast, 2025 - 2032

Biocomposites Market By Fiber Type (Wood Fiber, Non-Wood Fiber), Product Type (Wood Plastic Composites (WPCs), Hybrid Biocomposites), End-user Industry (Building & Construction, Automotive, Consumer Goods, Electrical & Electronics, Packaging, Others), and Regional Analysis for 2025 - 2032

Biocomposites Market Share and Trends Analysis

The global biocomposites market size is likely to be valued at US$34.8 Billion in 2025, and is estimated to reach US$127.1 Billion by 2032, growing at a CAGR of 20.3% during the forecast period 2025 - 2032, driven by increasing demand for advanced bio-based composite materials in the transportation, building & construction, and consumer goods sectors.

Market growth is driven by stricter environmental regulations, advances in natural fiber processing, and rising demand for sustainable materials. The automotive sector increasingly uses biocomposites for lightweighting and emissions compliance, while the building and construction segment grows rapidly under tighter energy efficiency standards.

Key Industry Highlights

- Leading End-user: The automotive sector is set to be the leading end-user, capturing about 38.5% revenue share in 2025, backed by a focused adoption of lightweight biocomposites.

- Leading & Fastest-growing Fiber Types: Wood fiber composites are slated to be market leaders with an estimated 68.7% share in 2025, while non-wood fibers are the fastest-growing segment through 2032.

- Dominant & Fastest-growing Product Types: Wood plastic composites are likely to hold nearly 72% market share in 2025, with hybrid biocomposites growing the fastest from 2025 to 2032.

- Dominant Region & Fastest-growing Regional Market: North America is expected to dominate with a 50.4% market share in 2025, supported by advanced R&D and regulatory incentives; Asia Pacific is the fastest-growing regional market for 2025 - 2032.

- Key Challenges: Industry challenges involve high initial capital costs and supply chain complexities that demand investment in integration and quality control to sustain growth.

- February 2025: UPM Biochemicals partnered with Bilfinger to provide comprehensive maintenance services for a pioneering biorefinery in Leuna, Germany, which uses sustainably sourced hardwood to produce biochemicals.

| Key Insights | Details |

|---|---|

| Biocomposites Market Size (2025E) | US$34.8 Bn |

| Market Value Forecast (2032F) | US$127.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 20.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Shift to Lightweight Biocomposites in the Automotive Sector

The gradual transition of the automotive industry to lightweight materials for improved fuel efficiency and emission reduction serves as a major growth engine for the market. Government regulations globally, such as the U.S. Corporate Average Fuel Economy (CAFE) standards and the European Union (EU)’s CO2 emission targets, are mandating significant reductions in vehicle weight and tailpipe emissions.

Biocomposites, combining natural fibers such as flax and hemp with bio-based polymers, facilitate tangible weight reductions compared to traditional composites while maintaining mechanical performance.

Major original equipment manufacturers (OEMs) and Tier 1 suppliers, supported by R&D collaborations and government incentives, are integrating biocomposites into interior door panels, dashboards, and underbody shields to comply with sustainability mandates. This transition is being further accelerated by increasing consumer environmental awareness and electrification trends, fostering the demand for high-performance, lightweight components.

High Initial Investment and Supply Chain Complexities

The market growth faces notable challenges stemming from high initial capital expenditure and intricate supply chain requirements. The production of biocomposites involves raw material variability, especially in non-wood fibers, which complicates quality control and consistency across batches, leading to increased R&D and processing costs.

Investments in specialized processing equipment, including injection molding and extrusion lines compatible with natural fibers, can be 10-15% higher than those for traditional composites. Supply chain fragmentation, with raw materials sourced from agricultural residues and emerging fiber crops, poses risks related to feedstock availability, seasonal fluctuations, and logistical inefficiencies. Regulatory frameworks, while supportive, also require compliance verification that adds operational overhead.

Expansion of Bio-Based Polymers in Packaging

The packaging sector is emerging as a lucrative growth opportunity for stakeholders in the biocomposites market, driven by tightening regulatory bans on single-use plastics and surging consumer preference for biodegradable alternatives. Governments worldwide, such as the EU with its Single-Use Plastics Directive and China’s Packaging Law, are instituting stringent restrictions and incentivizing sustainable packaging.

The biocomposite packaging market expansion is being fed by advancements in bio-based polymers such as polylactic acid (PLA) and polyhydroxyalkanoates (PHA) that are being increasingly blended with natural fibers to achieve compostable yet mechanically robust packaging solutions.

This sector addresses unmet needs for renewable, easily recyclable packaging materials suitable for food, cosmetics, and consumer electronics industries. Market participants investing in R&D are developing cost-competitive, scalable solutions integrating agro-waste fibers such as rice husk and coconut coir, capitalizing on circular economy models.

Category-wise Analysis

Fiber Type Insights

Wood fiber composites are set to dominate with an estimated 68.7% of the biocomposites market revenue share in 2025, aided by widespread industrial availability of wood by-products such as sawdust and flour. Their robust mechanical properties, ease of integration with various polymer matrices, and compatibility with existing processing technologies support their dominance. Wood fibers are also favored due to regulatory incentives promoting sustainable forestry and waste utilization.

The non-wood fiber segment is expected to display the fastest annual growth between 2025 and 2032. This rapid ascent is propelled by growing cultivation and commercial use of alternative natural fibers such as hemp, flax, kenaf, and bamboo, especially in Asia Pacific and Europe.

These fibers offer superior biodegradability and lower density, aligning with rising environmental consciousness and circular economy initiatives. Growing upstream supply chain maturity and government subsidies further empower the non-wood fiber segment, expanding applications in lightweight automotive interiors, packaging, and consumer electronics.

Product Type Insights

Wood plastic composites (WPCs) are slated to lead with an estimated 72% share of the market revenue in 2025. These composites are preferred for their durability, resistance to moisture and UV exposure, and aesthetic wood-like appearance, making them ideal for decking, fencing, automotive interiors, and consumer goods. The popularity of WPCs is reinforced by the incorporation of recycled polymers, further enhancing sustainability credentials and reducing environmental impact.

Hybrid biocomposites are likely to be the fastest-growing product category through 2032. Hybrid composites combine natural fibers with synthetic reinforcements such as glass or carbon fibers to achieve enhanced mechanical strength and thermal stability, essential for high-performance applications in aerospace, automotive structural parts, and electronic devices. These hybrids allow customization of composite properties, balancing biodegradability with superior performance metrics.

End-user Industry Insights

The automotive and transportation sector is anticipated maintains its position as the principal end-user, capturing a significant 38.5% of the biocomposites market sales in 2025. This dominance stems from the stringent implementation of fuel economy standards and emissions regulations across several jurisdictions that have compelled manufacturers to adopt lightweight materials to improve vehicle efficiency and lower environmental impact.

The inherent benefits of biocomposites, including noise reduction, recyclability, and cost-effective manufacturing, make them attractive for interior components, underbody shields, and semi-structural parts in passenger vehicles, commercial trucks, and electric vehicles (EVs).

The building & construction segment is projected to expand the fastest between 2025 and 2032. Sustainable building codes and certifications such as LEED and BREEAM are driving demand for biocomposites in applications including insulated panels, cladding, flooring, and window frames.

Biocomposites offer resistance to moisture, pests, and fire, enabling compliance with stringent building standards. Urbanization and infrastructure development in emerging economies are further sustaining growth. These sectoral dynamics imply tailored approaches for manufacturers, balancing material performance with regulatory compliance and cost-efficiency.

Regional Insights

North America Biocomposites Market Trends

North America is the global leader in the development and adoption of biocomposites, predicted to account for roughly 50.4% of the market share in 2025, led by the U.S. The regional market benefits from the BioPreferred Program of the U.S., which mandates increased federal procurement of bio-based products, spurring domestic demand and supplier development.

The mature automotive, aerospace, electronics, and construction sectors of North America have integrated sustainability targets aligned with governmental policies such as the Clean Air Act and various state-level renewable material incentives.

Its innovation ecosystem has been even more strengthened by the robust presence of world-class research institutions and extensive R&D funding from both public and private sectors. Competitive dynamics reflect vertically integrated supply chains and collaborative partnerships between raw material suppliers, OEMs, and technology firms.

Europe Biocomposites Market Trends

Europe is poised to hold around 24% of the biocomposites market share in 2025. Regulatory harmonization across Germany, the U.K., France, and Spain supports a cohesive bioeconomy agenda that encourages bio-based product development through subsidies, tax benefits, and green public procurement policies.

Germany, in particular, leads technological adoption with its automotive and construction sectors benefiting from government industrial bioeconomy strategies and innovation cluster investments. Collaborative efforts between universities, research centers, and industry accelerate material innovation and commercial deployment.

The EU’s stringent single-use plastics directives and circular economy transition policies have expanded the demand for biocomposites beyond automotive and construction into packaging and consumer goods. The market is projected to grow at a notable CAGR through 2032, supported by a deepening emphasis on lifecycle sustainability and eco-labeling standards that facilitate market acceptance and consumer confidence.

Asia Pacific Biocomposites Market Trends

Asia Pacific is slated to be the fastest-growing regional market for biocomposites with an estimated 13% CAGR during the 2025 - 2032 forecast period. Regional market growth is underpinned by the abundant availability of natural fibers, including jute, hemp, bamboo, and kenaf, combined with competitive manufacturing costs and expanding industrial capacity in China, India, Japan, and ASEAN countries.

National strategies promoting bioeconomy and pollution control reinforce governmental support through funding, pilot projects, and regulatory incentives aimed at reducing plastic waste and fostering renewable materials. The regional competitive landscape is characterized by both local enterprises and multinational corporations establishing production facilities and joint ventures.

Competitive Landscape

The global biocomposites market exhibits a moderately concentrated structure with a blend of large multinational corporations and numerous specialized small-to-medium enterprises (SMEs). The leading players collectively hold approximately 37% of the market, reflecting oligopolistic tendencies in key sub-segments such as wood fiber composite production and bio-based polymer supply.

Major companies, including Stora Enso, UPM Biocomposites, and UFP Industries, leverage vertically integrated operations spanning raw material sourcing, composite manufacturing, and customer partnerships, enhancing their competitiveness in cost management and innovation speed.

Strategic alliances and joint ventures are prevalent, enabling players to address feedstock variability challenges and improve product standardization. The market remains dynamic with continuous reinvestment in R&D and expanding capacity, fostering gradual consolidation amid rising barriers to entry imposed by technological complexity and capital intensity.

Key Industry Developments

- In September 2025, the European Composites Industry Association (EuCIA) welcomed Bremen-based Circular Structures, uniting Greenboats and Greenlander, to its Technical Section to advance European flax and hemp fiber composites through engineering expertise, performance validation, supply chain integration, and sustainable material education.

- In July 2025, Ecotechnilin opened a new production line near Warsaw, Poland, boosting capacity for flax, hemp, glass fiber, and polypropylene composites to meet automotive demand with sustainable, lightweight materials such as non-wovens and sandwich panels for high-performance, eco-efficient transportation applications.

- In June 2025, Bcomp announced that its flax-based natural fiber composites will feature in future BMW Group production cars, replacing carbon fiber components to cut CO2 emissions by about 40%. Building on motorsport success, the materials enable scalable manufacturing via RTM and prepreg processes while enhancing performance and sustainability.

Companies Covered in Biocomposites Market

- Stora Enso

- UPM Biocomposites

- UFP Industries, Inc.

- Natural Fibre Technologies

- RBT BioComposites

- FiberWood

- Bcomp Ltd

- Jelu-Werk J.Ehrler GmbH

- Hemka

- Norske Skog Saugbrugs

- FlexForm Technologies

- Trex Company

- Meshlin Composites ZRT

- Tecnaro GmbH

- Nanjing Jufeng Advanced Materials Co., Ltd.

Frequently Asked Questions

The global biocomposites market is projected to reach US$34.8 Billion in 2025.

Increasing demand for advanced bio-based composite materials in the transportation, building & construction, and consumer goods sectors, and regulatory pressures targeting reductions in carbon emissions and plastic waste are driving the market.

The biocomposites market is poised to witness a CAGR of 20.3% from 2025 to 2032.

Advancements in natural fiber processing technologies, rising consumer demand for sustainable, eco-friendly materials, and aggressive adoption of biocomposites by automakers to achieve weight reduction are key market opportunities.

Stora Enso, UPM Biocomposites, and UFP Industries are some of the key market players.