- Specialty & Fine Chemicals

- Advanced Composites Market

Advanced Composites Market Size, Share, and Growth Forecast, 2026 - 2033

Advanced Composites Market by Product Type (Carbon Fiber Composite, Glass Fiber Composite, Others), Resin Type (Thermosetting, Thermoplastic, Others), Manufacturing Process, End-use Industry, and Regional Analysis for 2026 - 2033

Advanced Composites Market Size and Trends Analysis

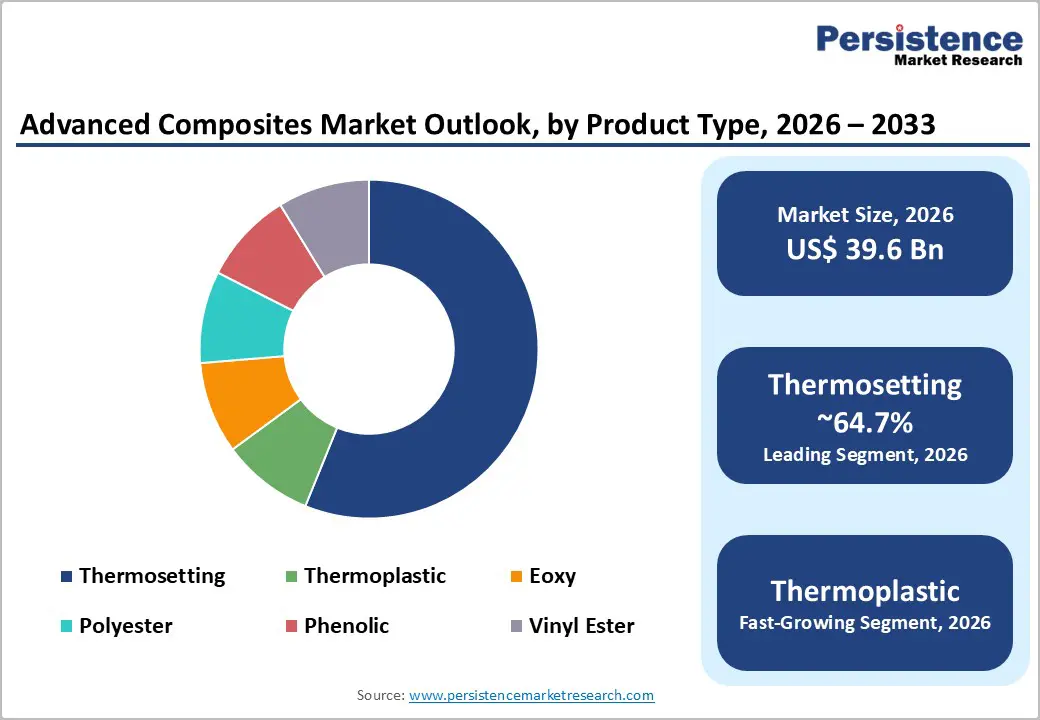

The global advanced composites market is likely to be valued at US$39.6 billion in 2026 and is expected to reach US$71.0 billion by 2033, growing at a CAGR of 8.7% between 2026 and 2033, driven by aviation fleet renewal, increasing lightweight material adoption in electric vehicle platforms, large-scale wind turbine blade manufacturing, and expanding defense procurement programs.

Carbon fiber composites dominate value share due to their high-performance characteristics, while thermoplastic systems and automated manufacturing technologies such as AFP/ATL and RTM are showing the fastest adoption rates. Market expansion remains concentrated in North America and the Asia Pacific, supported by strong industrial ecosystems and sustained capital investment.

Key Industry Developments:

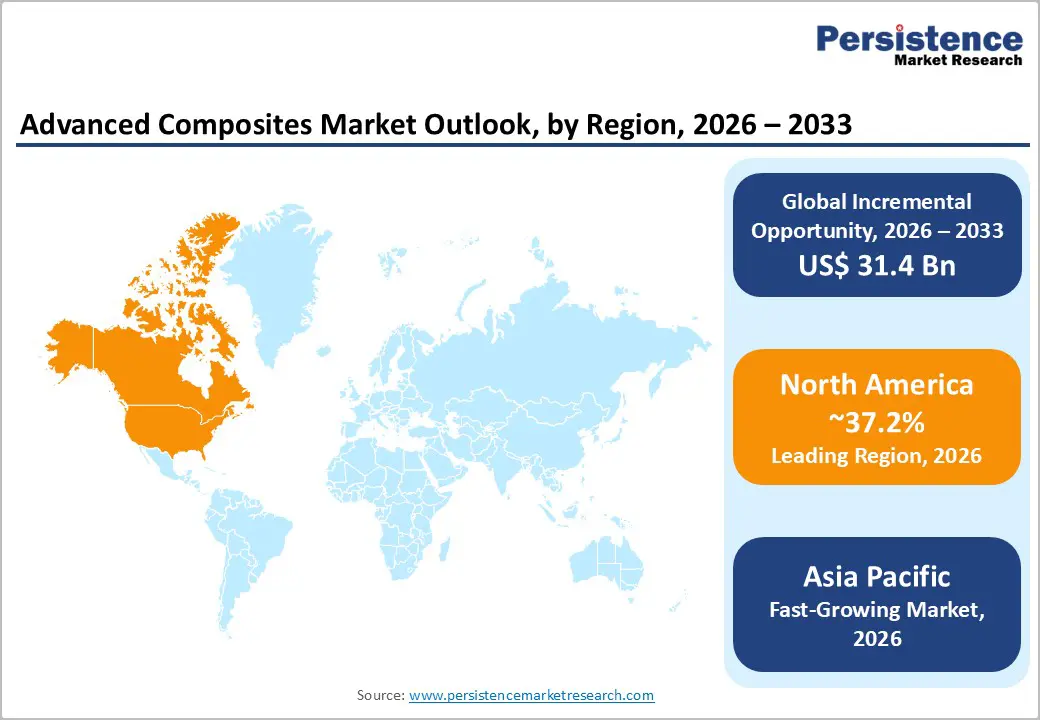

- Leading Region: North America is projected to account for approximately 37.2% of the global advanced composites market, supported by a mature aerospace and defense manufacturing base, strong OEM-supplier integration, and sustained investment in certified carbon fiber and thermoset composite systems.

- Fastest-growing Region: Asia Pacific, registering the highest regional growth rate through the forecast period, driven by large-scale wind energy manufacturing in China, rapid electric vehicle production expansion, and increasing automotive and sporting goods composite adoption across India and ASEAN economies.

- Investment Plans: Ongoing investments are concentrated in domestic carbon fiber capacity expansion, thermoplastic composite pilot lines, and automated manufacturing technologies (AFP/ATL, RTM), particularly in North America and Europe, aimed at supply-chain regionalization, recyclability, and high-rate production scalability.

- Dominant Product Type: Carbon fiber composites, anticipated to command approximately 64.7% of the market share, underpinned by strong demand from aerospace primary structures, premium automotive platforms, and long offshore wind turbine blade applications.

- Leading Resin Type: Thermosetting resins are expected to hold the largest market share, accounting for 58.7% in 2026, due to their widespread adoption in aerospace and defense applications, where thermal stability, fatigue resistance, and certified reliability are essential.

| Key Insights | Details |

|---|---|

| Advanced Composites Market Size (2026E) | US$39.6 Bn |

| Market Value Forecast (2033F) | US$71.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Aerospace and Defense Fleet Renewal and OEM Weight-Reduction Mandates

Global commercial and military aircraft manufacturers continue to increase composite content to reduce structural weight, improve fuel efficiency, and lower lifecycle operating costs. New-generation aircraft platforms and business jet upgrades allocate a significant share of primary and secondary structures to advanced composites, particularly carbon fiber-based systems. Aerospace applications account for a large share of the market value due to the high unit cost of certified composite components. Ongoing replacement cycles for narrow-body fleets, coupled with emerging regional and urban air mobility platforms, are creating sustained multi-year demand for prepregs, automated layup technologies, and high-performance resin systems. These factors collectively reinforce aerospace as the most value-intensive demand driver in the market.

Automotive Lightweighting, Electric Vehicle Adoption, and Thermoplastic Uptake

Automotive manufacturers are increasingly adopting advanced composites to meet regulatory emissions targets and improve electric vehicle driving range by reducing vehicle mass. Thermoplastic composite systems are gaining traction due to their faster processing cycles, recyclability, and compatibility with high-volume manufacturing. Structural carbon fiber components are expanding in premium EV models, while glass fiber-thermoplastic hybrids are being adopted in mass-market vehicles for cost-sensitive applications. This dual-material strategy enables automakers to balance performance and affordability. Continued investments by tier-one suppliers in thermoplastic processing technologies validate the long-term growth trajectory of composites within the automotive sector.

Renewable Energy Expansion and Large-Format Composite Demand

The global expansion of onshore and offshore wind energy is driving demand for large-format composite structures, particularly turbine blades. Increasing rotor diameters require materials with high stiffness-to-weight ratios, leading to greater use of carbon fiber reinforcements alongside glass fiber for cost efficiency. Wind energy contributes significantly to volume demand and supports investments in resin transfer molding, automated pultrusion, and filament winding processes. These manufacturing advancements enable the economical production of very large components, creating a durable and diversified demand base for advanced composites beyond transportation sectors.

Barrier Analysis - High Raw Material Costs and Carbon Fiber Price Volatility

Carbon fiber and high-performance resin systems remain significantly more expensive than conventional metallic materials. Volatility in energy prices and precursor feedstocks can materially affect production costs, compress margins, and delay adoption in cost-sensitive applications. Periodic supply constraints and pricing adjustments have led some OEMs to postpone composite substitution in favor of traditional materials. In high-volume applications, component costs can increase by 10-20% during periods of elevated carbon fiber pricing, limiting near-term penetration outside premium segments.

Recycling, End-of-Life Management, and Regulatory Pressures

While thermoplastic composites offer improved recyclability, thermoset-based systems continue to face end-of-life challenges. Regulatory frameworks emphasizing extended producer responsibility and circular economy principles increase lifecycle compliance costs for composite-intensive products. The lack of scaled, economically viable recycling infrastructure for thermoset composites risks constraining adoption in highly regulated markets. Uncertainty around recycling economics can add an estimated 2-6% to total lifecycle costs in certain applications, particularly in automotive and consumer-facing industries.

Opportunity Analysis - Thermoplastic Composites in High-Volume Automotive Platforms

As automakers transition toward modular electric vehicle architectures, thermoplastic composites present an opportunity to replace metal-intensive body-in-white and structural components. Their fast cycle times and potential for part consolidation support efficient large-scale manufacturing. If thermoplastic composite penetration reaches 5-7% of mid-segment vehicle structural material spend by 2030, the resulting opportunity would be in the low-single-digit billions of U.S. dollars during the 2026 - 2033 period. Suppliers with validated recycling solutions and proven processing capabilities are positioned to secure preferred supplier status.

Composite Recycling and Circular Supply Chains

Advances in chemical, thermal, and mechanical recycling technologies are enabling the recovery and reuse of composite materials, particularly carbon fiber. Reclaimed fibers retaining 70-80% of original mechanical properties are suitable for non-primary structural and industrial applications. Successful scale-up of these technologies could create a multi-hundred-million-dollar secondary materials market by the early 2030s. Investment in recycling infrastructure offers both cost stabilization benefits and regulatory compliance advantages, creating defensible competitive differentiation.

Category-wise Analysis

Product Type Insights

Carbon fiber composites are anticipated to account for approximately 64.7% market share in 2026, driven by their exceptional strength-to-weight ratio, fatigue resistance, and premium pricing structure. Demand remains heavily concentrated in aerospace primary and secondary structures, including fuselage sections, wings, empennages, and interior components, where weight reduction directly translates into fuel efficiency and lower operating costs.

Premium automotive platforms, particularly electric and high-performance vehicles, increasingly deploy carbon fiber for structural tubs, body panels, and battery enclosures, while sporting goods continue to leverage its performance advantages. Expanding use in longer offshore wind turbine blades further reinforces carbon fiber’s leadership. Ongoing capacity expansions focus on higher-temperature resin compatibility, faster cure prepregs, and recyclable fiber chemistries, enabling penetration into broader industrial and mobility applications.

Glass fiber composites represent the fastest-growing product segment by volume, supported by their cost efficiency, scalable manufacturing, and adequate mechanical performance for non-critical structural applications. Growth is strongly driven by onshore and offshore wind energy, where glass fiber remains the preferred reinforcement for blades, nacelles, and structural shells due to favorable cost-to-performance economics.

In automotive manufacturing, glass fiber composites are increasingly used to replace metals in underbody shields, front-end modules, leaf springs, and structural panels, particularly in mass-market vehicles. Infrastructure and construction applications, including corrosion-resistant panels, pipes, and reinforcement elements, further support demand. While carbon fiber leads the market in value, glass fiber composites underpin volume-led expansion and cost-sensitive adoption across industrial sectors.

Resin Type Insights

Thermosetting resins are projected to hold the largest share of 58.7% in the advanced composites market in 2026, led by epoxy systems used extensively in aerospace and defense applications. Their superior thermal stability, fatigue resistance, and long-term structural integrity make them essential for certified aircraft structures, rotor blades, and high-load components.

Prepreg-based thermoset systems dominate aerospace manufacturing due to their compatibility with established qualification standards, autoclave processing, and predictable mechanical performance. Robust partnerships among resin formulators, prepreg manufacturers, and aircraft OEMs continue to reinforce the value leadership of thermosets. Although they involve longer curing cycles, ongoing advancements in out-of-autoclave and fast-curing epoxy technologies are maintaining thermosets’ relevance in wind energy, marine, and high-performance industrial sectors.

Thermoplastic resins constitute the fastest-growing resin segment, propelled by rising automotive demand for recyclability, shorter cycle times, and high-volume manufacturing compatibility. Advanced thermoplastics such as PEEK, PEKK, PPS, and PA-based systems are increasingly adopted in electric vehicles, consumer products, and select aerospace secondary structures.

Innovations in reactive thermoplastics, thermoplastic RTM, and hybrid processing methods are reducing tooling and processing costs and enabling broader structural applications. Regulatory emphasis on circular economy principles and end-of-life recyclability further accelerates adoption, particularly in automotive body structures, battery housings, and consumer electronics enclosures. These factors position thermoplastic composites as a critical growth lever through the forecast period.

Regional Insights

North America Advanced Composites Market Trends - Aerospace-Driven Demand with Defense, EV, and Wind Energy Reinforcement

North America is projected to lead the market with approximately 37.2% share, supported by its deep-rooted aerospace manufacturing ecosystem, defense spending, automotive innovation, and sustained wind energy investment. The U.S. anchors regional demand, driven by the presence of major aircraft OEMs such as Boeing, tier-one suppliers, and defense contractors that rely heavily on carbon fiber and high-performance thermoset composites for primary and secondary structures. Composite material suppliers, including Hexcel, Toray Advanced Composites, and Solvay, maintain strong manufacturing and R&D footprints across the region, reinforcing supply chain resilience and technological leadership.

The regulatory environment favors certified thermoset systems for aerospace and defense while increasingly supporting innovation in recyclable thermoplastics and low-VOC resin chemistries. Federal initiatives promoting domestic manufacturing and critical material security have accelerated investments in U.S.-based carbon fiber capacity, automated fiber placement (AFP), and out-of-autoclave processing technologies.

In parallel, the automotive sector, led by electric vehicle platforms, continues to expand the use of thermoplastic composites for lightweighting, battery enclosures, and structural reinforcements. Wind energy remains a steady demand driver, particularly for glass and carbon fiber composites used in larger, more efficient turbine blades. Strategic acquisitions and private equity participation in composite fabricators and material suppliers reflect ongoing consolidation and regionalization of supply chains, as OEMs seek tighter control over quality, lead times, and certification-critical materials. Collectively, these factors position North America as a mature yet innovation-driven market with strong value retention.

Europe Advanced Composites Market Trends - Regulation-Led Innovation Anchored by Aerospace and Offshore Wind

Europe represents the second-largest regional market for advanced composites, underpinned by its strong aerospace capabilities, offshore wind leadership, and increasingly harmonized regulatory framework. Countries such as Germany, France, and the U.K. remain central to aerospace composite demand through the extensive supply chains supporting Airbus commercial aircraft, defense platforms, and space programs. European automotive manufacturers, including premium and performance-focused OEMs, continue to integrate advanced composites into lightweight vehicle architectures, particularly for electric and hybrid platforms.

Europe’s leadership in offshore wind energy significantly shapes regional composite demand. Wind turbine manufacturers such as Vestas and Siemens Gamesa rely heavily on glass and carbon fiber composites for longer blades and high-load components, with manufacturing hubs across Northern and Southern Europe. Spain and other Southern European countries play a key role in blade manufacturing and composite component fabrication, benefiting from established industrial infrastructure and skilled labor.

Regulatory harmonization under EU circular economy and sustainability directives strongly influences material selection, driving R&D in recyclable resins, bio-based composites, and lower-emission manufacturing processes. Public-private research initiatives, often supported through EU-level funding mechanisms, facilitate cross-border collaboration between material suppliers, OEMs, and research institutes. These efforts are accelerating innovation while maintaining Europe’s competitive position in high-value, regulation-intensive composite applications.

Asia Pacific Advanced Composites Market Trends - High-Volume Manufacturing Growth Fueled by Wind Energy and EV Expansion

Asia Pacific is the fastest-growing regional market for advanced composites, driven by large-scale wind energy manufacturing, rapid electric vehicle production growth, and expanding aerospace assembly activity. China leads the region in volume manufacturing, supported by its dominant position in wind turbine production, where glass fiber composites are extensively used for blades, nacelles, and structural components. Chinese material suppliers and fabricators benefit from manufacturing scale, vertically integrated supply chains, and strong domestic demand.

Japan occupies a strategic position at the high end of the value chain, with companies such as Toray Industries recognized globally for advanced carbon fiber and prepreg technologies used in aerospace, defense, and premium industrial applications. Japanese expertise in material science and process control continues to influence global standards for high-performance composites.

India and ASEAN countries are emerging as important growth hubs, supported by expanding automotive manufacturing, infrastructure development, and sporting goods production. Automotive lightweighting initiatives and rising EV adoption are driving demand for both thermoset and thermoplastic composites, while favorable industrial policies and cost advantages are attracting foreign investment in composite part manufacturing. Collectively, Asia Pacific’s combination of scale, cost efficiency, and policy support positions the region as the primary growth engine for the advanced composites market over the forecast period.

Competitive Landscape

The global advanced composites market is concentrated at the raw material level, particularly among carbon fiber and specialty resin producers, while downstream component manufacturing remains fragmented. Vertically integrated players with certification expertise hold competitive advantages in aerospace and defense applications. Consolidation activity is increasing, particularly among automotive-focused composite suppliers seeking scale and geographic reach.

Key developments include investments in composite recycling technologies, strategic partnerships with automotive OEMs, capacity expansions aligned with aerospace demand, and private equity-led acquisitions targeting automotive composite platforms. These actions reflect a broader industry shift toward sustainability, automation, and supply-chain resilience.

Leading companies emphasize vertical integration, manufacturing automation, sustainability initiatives, and long-term OEM partnerships. Certification expertise, co-development capabilities, and lifecycle cost optimization are key differentiators shaping competitive positioning.

Key Industry Developments

- In March 2025, Huntsman Corporation and Advanced Material Development Ltd entered a partnership to develop carbon nanotube-integrated functional composite materials in the U.S., targeting electrically enhanced solutions for defense and aerospace applications.

- In March 2025, Hexcel and FIDAMC formed a strategic collaboration to explore digitalization, AI, and advanced manufacturing techniques across aerospace, automotive, and other industries, driving innovation and sustainability in composite material performance.

Companies Covered in Advanced Composites Market

- Toray Industries

- Hexcel Corporation

- Teijin Limited

- SGL Carbon

- Mitsubishi Chemical Group

- Solvay

- Gurit

- Owens Corning

- Jushi Group

- Huntsman Corporation

- Toray Advanced Composites

- Teijin Automotive Technologies

- Zoltek Corporation

- Formosa Plastics Corporation

- Hyosung Advanced Materials

- Park Aerospace

- Axiom Materials

- Cytec Solvay Group

Frequently Asked Questions

The global composites market is valued at US$39.6 billion in 2026.

By 2033, the composites market is expected to reach US$71.0 billion.

Key trends include increasing carbon fiber penetration in aerospace and EVs, rapid adoption of thermoplastic composites for recyclability and faster cycle times, expansion of automated manufacturing technologies (AFP/ATL, RTM), and growing emphasis on circular materials and composite recycling solutions.

Carbon fiber composites are the leading segment, anticipated to account for approximately 64.7% of total market value, due to their superior strength-to-weight ratio and high usage in aerospace, premium automotive, and wind energy applications.

The advanced composites market is projected to grow at a CAGR of 8.7% between 2026 and 2033.

Major players include Toray Industries, Hexcel Corporation, Teijin Limited, SGL Carbon, and Mitsubishi Chemical Group.