- Advanced Materials

- Metal Matrix Composite Market

Metal Matrix Composite Market Size, Share, and Growth Forecast 2026 - 2033

Metal Matrix Composite Market by Matrix Material (Aluminum, Magnesium, Copper, Titanium, Others), by Reinforcement Type (Continuous Fiber, Discontinuous Fiber, Particulates, Others), by Reinforcement Material (Silicon Carbide, Carbon Fiber, Alumina, Others), by Production Technology, by End-Use Industry, by Regional Analysis, 2026 - 2033

Metal Matrix Composite Market Size and Trend Analysis

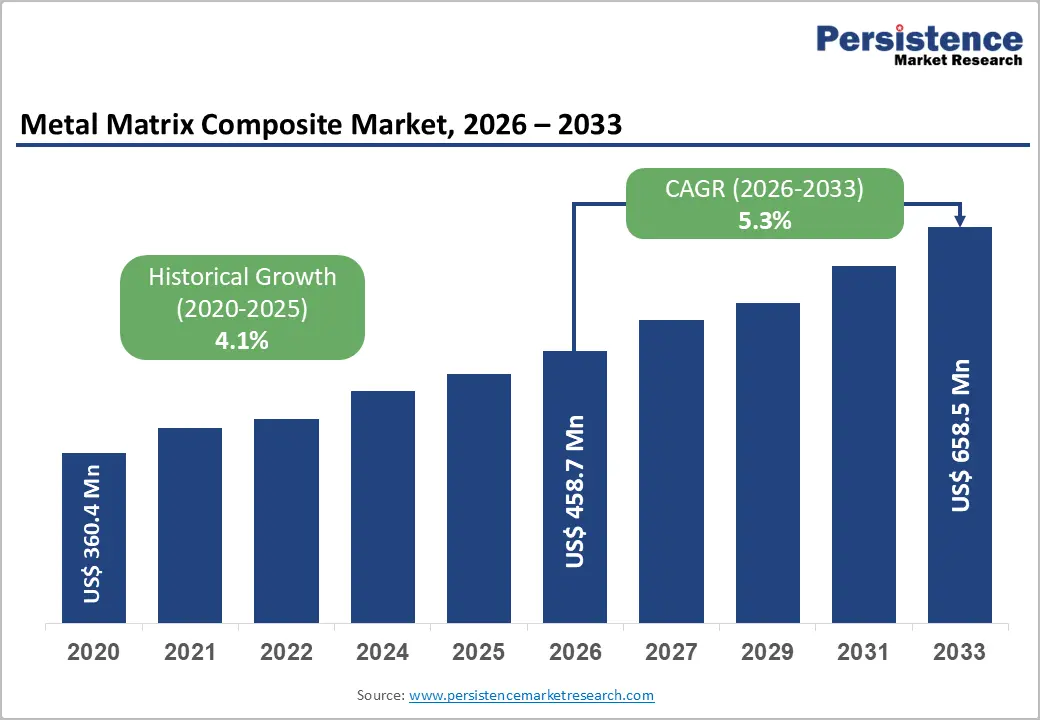

The global metal matrix composite market size is likely to be valued at US$ 458.7 Million in 2026 and is expected to reach US$ 658.5 Million by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033.

The market outlook is underpinned by the adoption of lightweight, high-strength materials in automotive, aerospace & defence, and electronics applications to meet stricter fuel-efficiency and performance norms.

Key Market Highlights

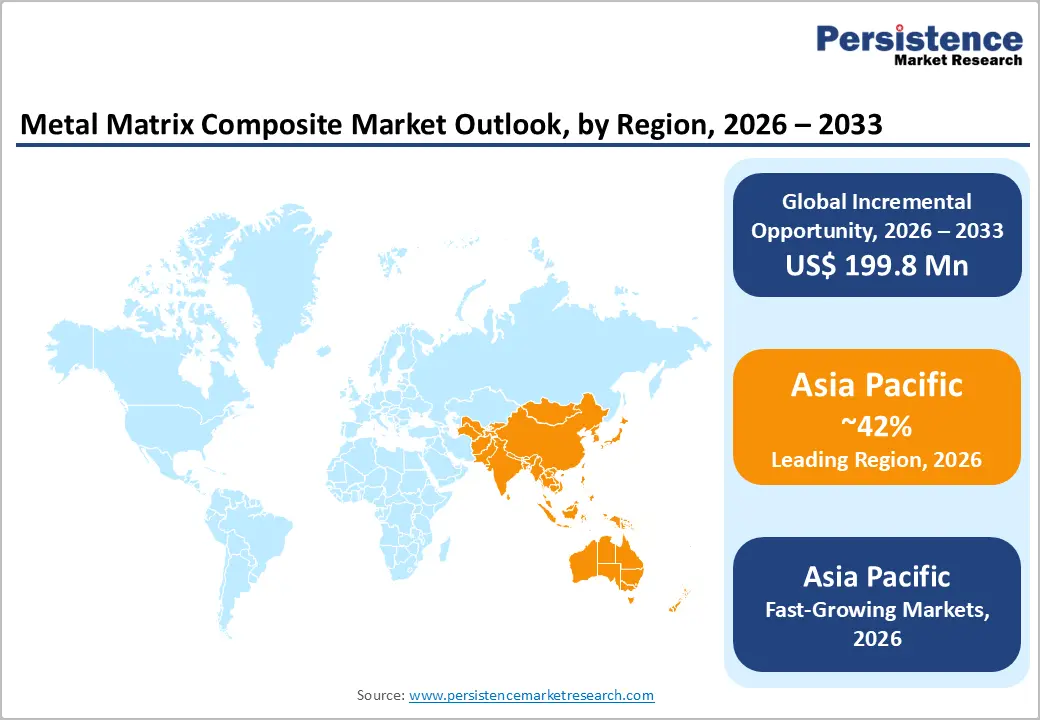

- Leading Region: Asia Pacific currently represents the leading regional market for metal matrix composites, supported by strong industrial bases in China, Japan, and India, large-scale automotive and electronics production, and competitive manufacturing ecosystems that encourage adoption of lightweight materials.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market with a rising CAGR of 7.3%, where rapid industrialization, EV adoption, and investments in aerospace and advanced manufacturing drive above-average growth rates in metal matrix composite demand across multiple end-use industries.

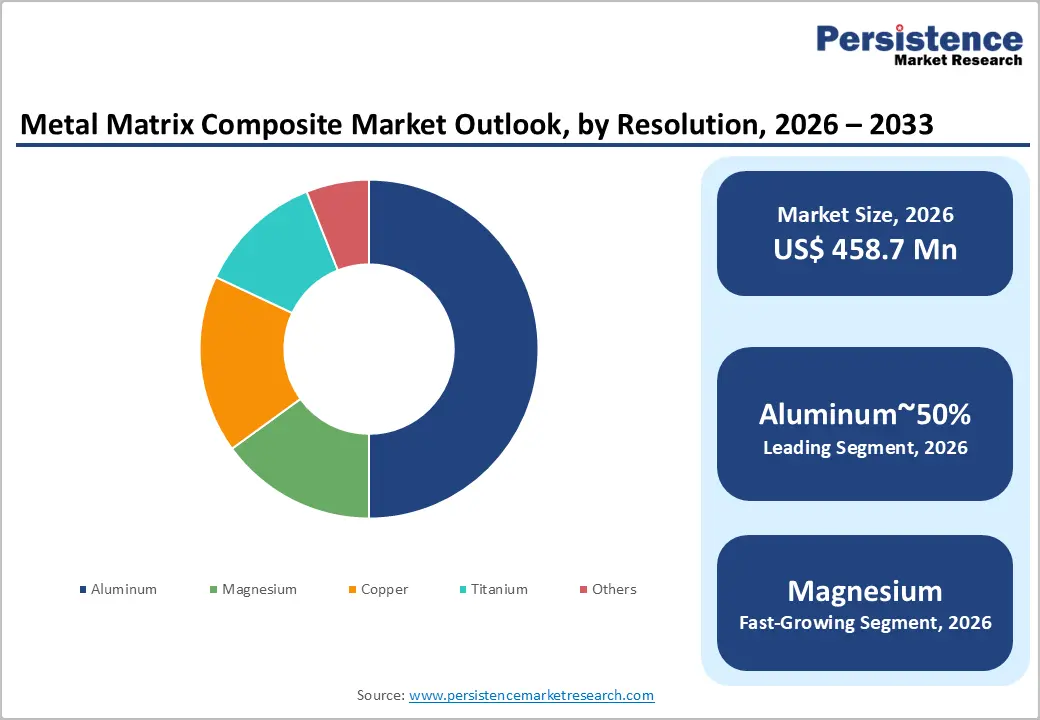

- Leading Segment: Within product categories, the aluminum matrix segment is the dominant matrix material, accounting for the 50% share of MMC usage due to its favorable density, recyclability, and alignment with automotive and aerospace lightweighting strategies worldwide.

- Fastest-Growing Segment: Among end-use industries, the automotive segment is poised to be the fastest-growing, as rising aluminum content per vehicle and electrification trends boost demand for lightweight, thermally stable, and wear-resistant MMC components for braking, powertrain, and chassis systems.

- Key Market Opportunity lies in EVs and power electronics thermal management, where high thermal conductivity and low-weight metal matrix composites can address heat dissipation challenges in inverters, battery enclosures, and high-power modules, enabling higher power densities and reliability.

| Key Insights | Details |

|---|---|

| Metal Matrix Composite Market Size (2026E) | US$ 458.7 Million |

| Market Value Forecast (2033F) | US$ 658.5 Million |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.1% |

Market Dynamics

Market Growth Drivers

Lightweight metal matrix composites support EV-driven weight reduction while delivering superior strength, wear resistance, and thermal performance

Lightweighting in transportation remains a major growth driver for metal matrix composites, as automotive OEMs increasingly seek materials that reduce vehicle weight while maintaining high mechanical strength. The global shift toward electric vehicles is accelerating this trend, since EVs require significantly higher aluminum content than traditional internal combustion engine vehicles. Industry outlooks suggest that aluminum usage per electric vehicle in Europe could reach around 310 kg by 2026, highlighting a structural transition toward lightweight metals in body, chassis, and battery systems.

Metal matrix composites, particularly aluminum- and magnesium-based MMCs reinforced with silicon carbide or carbon fibers, directly support this transition. These materials offer higher stiffness, superior wear resistance, and improved thermal performance compared with conventional alloys. As a result, MMCs are increasingly adopted in brake rotors, pistons, engine components, and load-bearing structural parts, where durability, efficiency, and weight reduction are critical for next-generation vehicle platforms.

Aerospace and defense programs increasingly adopt MMCs for high-temperature, lightweight, and durability-critical advanced structural applications

Aerospace and defense programs worldwide are increasingly prioritizing lightweight and high-strength materials to improve fuel efficiency, payload capacity, and overall operational performance. Advanced composites already account for more than 50% of the structural weight in aircraft such as the Airbus A350, demonstrating a long-term shift toward high-performance materials in primary structures. Metal matrix composites complement polymer-based composites by offering higher temperature resistance, better damage tolerance, and superior thermal conductivity.

These properties make MMCs well-suited for turbine components, helicopter structures, satellite systems, and advanced defense platforms operating in extreme environments. Governments and defense agencies in North America and Europe continue to invest heavily in research and development through clean aviation initiatives and military modernization programs. This sustained funding supports the scaling of advanced materials technologies and encourages broader adoption of MMCs in safety-critical and high-performance aerospace and defense applications.

Market Restraints

High manufacturing costs and complex processing limit MMC adoption to premium, performance-driven aerospace, defense, and automotive applications

Metal matrix composites face adoption challenges due to their high production costs and technically complex manufacturing processes. Common production routes such as powder metallurgy, liquid metal infiltration, and advanced deposition methods require precise control over microstructure, reinforcement dispersion, and metal-matrix bonding. These processes rely on specialized equipment, high-temperature furnaces, and skilled technical expertise, which significantly increase capital and operating expenses.

In addition, MMC components often require secondary processing, including precision machining and specialized joining techniques, further raising total production costs. Compared with conventional steel or aluminum alloys, MMCs are therefore less cost-competitive for mass-market applications. As a result, their use is largely limited to high-value segments such as aerospace, defense, and premium automotive components. In price-sensitive industries and emerging markets, these cost barriers slow widespread adoption and restrict MMCs to niche, performance-driven applications.

Limited design standards and complex material behavior slow MMC certification and adoption in regulated, safety-critical industries

Design complexity and the lack of standardization present additional barriers to the broader adoption of metal matrix composites. MMCs often exhibit anisotropic mechanical properties and complex stress-strain behavior, requiring advanced modeling tools and specialized engineering expertise. Extensive testing and validation are necessary to ensure consistent performance, particularly in safety-critical applications. However, the absence of universally accepted design codes, testing standards, and long-term performance databases for many MMC systems creates uncertainty among OEMs and tier suppliers.

This challenge is especially significant in highly regulated industries such as aerospace and automotive manufacturing, where certification timelines are strict, and risk tolerance is low. As a result, product development cycles become longer and more expensive. Many end users continue to favor conventional alloys or polymer composites that have established standards, proven reliability, and mature global supply chains, limiting rapid MMC scale-up.

Market Opportunities

Rapid EV and electronics growth creates strong demand for MMCs offering lightweight structures with superior thermal management

Rapid growth in electric vehicles, renewable energy systems, and high-power electronics is creating significant opportunities for metal-matrix composites with advanced thermal management capabilities. Global electric vehicle sales have reached tens of millions of units annually, with EVs now representing nearly one-fifth of total global car sales. This rapid electrification trend is increasing demand for materials that offer high thermal conductivity, dimensional stability, and low weight.

MMCs based on aluminum or copper matrices reinforced with silicon carbide or carbon fibers are increasingly considered for heat sinks, inverter housings, battery trays, and braking and suspension systems. These applications require efficient heat dissipation to support higher power densities and improved reliability. As thermal management becomes a critical design constraint in EVs and electronics, MMCs are well-positioned to emerge as a key material solution within the broader advanced materials and composites ecosystem.

Rapid industrial growth and government investment position the Asia Pacific as the fastest-growing MMC production and consumption hub

The Asia Pacific region presents a significant growth opportunity for metal matrix composites, driven by rapid industrialization and expanding advanced manufacturing capabilities. Countries such as China, India, and Japan are witnessing strong growth in automotive, electronics, aerospace, and industrial machinery production, creating robust demand for lightweight and high-performance materials. Asia Pacific already accounts for a substantial share of global MMC revenues, estimated at over US$ 300 million in recent years, and is expected to grow strongly through 2032.

This growth is supported by large-scale manufacturing bases, cost-efficient production, and increasing government investments in advanced materials and R&D infrastructure. Regional initiatives focused on electric vehicles, aerospace localization, and industrial modernization are further accelerating MMC adoption. As a result, the Asia Pacific is emerging as both the fastest-growing producer and consumer of metal matrix composites globally.

Category-wise Insights

By Matrix Material Analysis

Aluminum matrix composites account for the largest share of the metal matrix composite market, with an estimated 50% of total consumption by matrix material. This dominance is driven by aluminum’s low density, excellent castability, corrosion resistance, and recyclability. Aluminum usage per vehicle continues to rise steadily, with projections in North America and Europe indicating an increase of nearly 100 pounds per vehicle between 2020 and 2030. Electrification and lightweighting initiatives are the primary drivers of this trend.

Aluminum matrix composites reinforced with silicon carbide or carbon fibers are widely used in brake discs, engine components, structural automotive parts, and aerospace applications. These materials deliver enhanced wear resistance, higher stiffness, and improved thermal performance without significantly increasing vehicle weight. Their favorable balance of performance, cost, and scalability ensures continued leadership over magnesium, copper, and titanium matrix systems.

By Reinforcement Type Analysis

Particulate-reinforced metal matrix composites hold the largest share of the market by reinforcement type, accounting for approximately 45% of total demand. This leadership is primarily due to their relatively lower cost and compatibility with conventional manufacturing methods such as casting and powder metallurgy. Common reinforcements, including silicon carbide and alumina particles, enable the production of wear-resistant components such as brake rotors, cylinder liners, pistons, and industrial machinery parts.

These systems support scalable manufacturing while maintaining acceptable mechanical and thermal performance. In contrast, continuous and discontinuous fiber-reinforced MMCs offer superior strength and stiffness but involve more complex and expensive production processes. As a result, fiber-reinforced MMCs are mainly used in aerospace, defense, and high-end industrial applications. Particulate-reinforced systems continue to dominate higher-volume, cost-sensitive automotive and engineering markets.

By Reinforcement Material Analysis

Silicon carbide is the most widely used reinforcement material in metal matrix composites, representing approximately 53% of total reinforcement usage. Its popularity stems from its high hardness, excellent wear resistance, good thermal conductivity, and strong compatibility with aluminum and magnesium matrices. SiC-reinforced aluminum composites are extensively adopted in automotive brake discs, pistons, and aerospace structural components, where reduced weight and improved fatigue performance are essential.

Compared with traditional cast iron or steel components, these systems offer superior durability and efficiency. The ability to precisely control particle size, volume fraction, and distribution allows manufacturers to tailor performance for specific applications. While alumina and carbon fibers remain important alternatives, silicon carbide offers the best balance of performance, cost, and scalability for high-volume applications. Emerging hybrid and nano-reinforced MMCs are currently under active research for next-generation performance improvements.

By Production Technology Analysis

Powder metallurgy remains the leading production technology for metal matrix composites, accounting for close to 46% of global MMC production volume. This process enables uniform reinforcement distribution, precise control over porosity, and the manufacture of near-net-shape components with consistent mechanical properties. Powder metallurgy is particularly well-suited for high-performance automotive, aerospace, and industrial applications where reliability and dimensional accuracy are critical.

The technology also supports complex geometries with minimal machining, reducing material waste and post-processing costs. While casting and liquid metal infiltration techniques are gaining traction for larger components and cost-sensitive applications, powder metallurgy continues to dominate high-specification MMC production. Ongoing improvements in powder quality, advanced sintering methods, and integration with additive manufacturing technologies are further enhancing process efficiency and performance consistency, reinforcing powder metallurgy’s central role in the MMC value chain.

By End-Use Industry Analysis

The automotive industry represents the largest end-use segment for metal matrix composites, accounting for approximately 35% of global MMC consumption. This leadership is driven by tightening emissions regulations, fuel-efficiency targets, and the rapid transition to battery-electric vehicles. Aluminum and magnesium MMCs offer lighter and more wear-resistant alternatives to conventional steel and cast iron components. They are increasingly used in brake systems, pistons, connecting rods, driveline components, and structural parts.

These materials directly contribute to reduced vehicle weight, improved energy efficiency, and enhanced durability. The rising aluminum content in modern vehicles, combined with growing thermal management needs in EV platforms, strongly supports MMC adoption. While aerospace and defense applications generate higher value per unit, automotive applications dominate overall volume, positioning the automotive sector as the primary growth engine for the global MMC market.

Regional Insights

North America Metal Matrix Composite Market Trends

North America remains a critical market for metal matrix composites, led by the United States’ strong aerospace, defense, and automotive industries. The U.S. accounts for nearly 40% of global defense spending, creating sustained demand for high-performance materials used in military aircraft, armored vehicles, and space platforms. MMCs are increasingly evaluated for applications requiring weight reduction, durability, and thermal stability.

In civil aerospace, the push for fuel-efficient aircraft and sustainable aviation solutions further supports advanced material adoption. The North American automotive sector is also a major driver, with studies indicating aluminum content per vehicle could increase by almost 100 pounds between 2020 and 2030. This shift creates opportunities for aluminum matrix composites in brake systems, driveline components, and thermal management applications. Strong R&D ecosystems, national laboratories, and university-industry partnerships further reinforce regional leadership.

Europe Metal Matrix Composite Market Trends

Europe’s metal matrix composite market is shaped by strict environmental regulations, decarbonization goals, and a strong aerospace and automotive manufacturing base. Countries such as Germany, France, the U.K., and Spain are at the forefront of lightweighting and sustainable mobility initiatives. Programs under the European Green Deal and long-term clean aviation strategies emphasize fuel efficiency and reduced emissions, supporting demand for advanced materials, including MMCs.

Composite materials already account for more than 50% of structural weight in aircraft like the Airbus A350, highlighting the region’s commitment to lightweight design. In the automotive sector, aluminum content in electric vehicles is projected to reach approximately 310 kg per vehicle by 2026. MMCs offer superior wear resistance and thermal performance for brake systems, powertrain components, and electronics housings. Strong public funding and research programs accelerate innovation and gradual industrial adoption.

Asia Pacific Metal Matrix Composite Market Trends

Asia Pacific is the fastest-growing regional market for metal matrix composites, supported by rapid industrialization and expanding manufacturing capacity. Regional revenues have exceeded US$ 300 million in recent years and are expected to grow significantly through 2032. China plays a central role as the world’s largest manufacturing hub, benefiting from cost-effective raw material supply chains and strong investments in advanced materials. Japan focuses on high-quality, technology-driven production, with MMC demand growing steadily in premium applications.

India’s expanding automotive and aerospace sectors, along with government initiatives promoting domestic manufacturing, further support regional growth. Across Southeast Asia, investments in EV supply chains, electronics manufacturing, and powder metallurgy infrastructure are creating favorable conditions for the adoption of MMCs. The region is emerging as both a major production center and a rapidly growing consumption market for metal matrix composites.

Competitive Landscape

The global metal matrix composite market is moderately concentrated, featuring a mix of specialized MMC manufacturers, advanced materials companies, and integrated metal producers. These players serve high-specification customers across aerospace, defense, automotive, and industrial sectors. Competitive differentiation is driven by strong R&D capabilities, proprietary matrix-reinforcement combinations, and process expertise in powder metallurgy, casting, and liquid metal infiltration. Leading companies focus on delivering consistent quality at scale and producing complex, near-net-shape components with tight tolerances.

Strategic partnerships with OEMs enable co-development of application-specific solutions, strengthening long-term customer relationships. Emerging business models emphasize regional manufacturing hubs in Asia Pacific, integration with additive manufacturing, and advanced surface engineering techniques. These strategies aim to improve performance, reduce costs, and expand MMC adoption across a broader range of high-growth industrial applications.

Key Market Developments

- In March 2023: Materion Corporation expanded its advanced materials portfolio for aerospace and defence applications, including high-performance composites for thermal management and structural uses.

- In June 2023: Sumitomo Electric Industries Ltd announced development initiatives in lightweight and high-thermal-conductivity materials aimed at next-generation automotive and electronics applications.

- In October 2024: Hitachi Metals Ltd (now under a rebranded corporate structure) continued to invest in advanced alloy and composite technologies for mobility and industrial sectors, reinforcing its footprint in high-performance materials.

Companies Covered in Metal Matrix Composite Market

- 3A Composites

- 3M

- ADMA Products Inc

- CPS Technologies Corp

- DAT Alloytech

- Denka Company Limited

- GKN Sinter Metals Engineering GmbH

- Hitachi Metals Ltd

- Materion Corporation

- MTC Powder Solutions AB

- Plansee Group

- Sumitomo Electric Industries Ltd

- Thermal Transfer Composites LLC

- TISICS Ltd

- TWI Ltd

- Sandvik AB

- SGL Carbon SE

- Alvant Ltd

- DWA Aluminum Composites

Frequently Asked Questions

The global metal matrix composite market is expected to be around US$ 458.7 Million in 2026 and reach approximately US$ 658.5 Million by 2033, reflecting a CAGR of about 5.3% during 2026-2033.

Key demand drivers include lightweighting in automotive and aerospace, rising adoption of electric vehicles, and growing use of high-performance thermal management materials in power electronics and industrial systems requiring high strength and fatigue resistance.

By matrix material, aluminum matrix composites hold the leading share, supported by expanding aluminum usage per vehicle and strong compatibility with reinforcements such as silicon carbide and carbon fibers across mobility and aerospace applications.

The Asia Pacific region leads the market, driven by large automotive, electronics, and industrial manufacturing bases in China, Japan, and India, combined with competitive production costs and increasing R&D investments in advanced materials.

A major opportunity lies in EV and power electronics thermal management, where MMCs with high thermal conductivity and low weight can improve heat dissipation and reliability in inverters, battery systems, and high-power electronic modules.

Prominent companies include 3A Composites, 3M, ADMA Products Inc, CPS Technologies Corp, Materion Corporation, Plansee Group, Sumitomo Electric Industries Ltd, Hitachi Metals Ltd, TISICS Ltd, and GKN Sinter Metals Engineering GmbH, along with several specialized regional producers.