- Automotive Components & Materials

- Commercial Vehicle Telematics Market

Commercial Vehicle Telematics Market Size, Share, and Growth Forecast, 2026 - 2033

Commercial Vehicle Telematics Market by Component (Hardware, Software, Services), Application (Fleet Management, Vehicle Tracking, Driver Behavior & Safety Monitoring, Predictive Maintenance & Diagnostics, Fuel & Energy Management, Compliance & Regulatory Monitoring, Insurance Telematics, Cargo & Asset Monitoring), Vehicle Type (LCVs, MCVs, HCVs, Specialized Commercial Vehicles), and Regional Analysis for 2026 - 2033

Commercial Vehicle Telematics Market Share and Trends Analysis

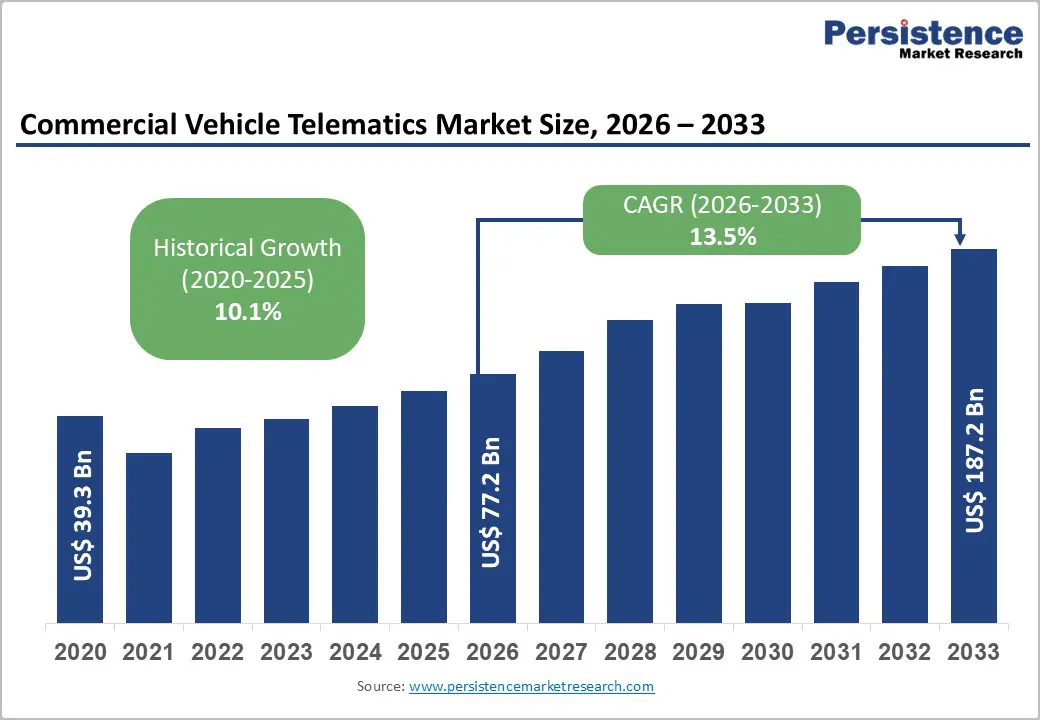

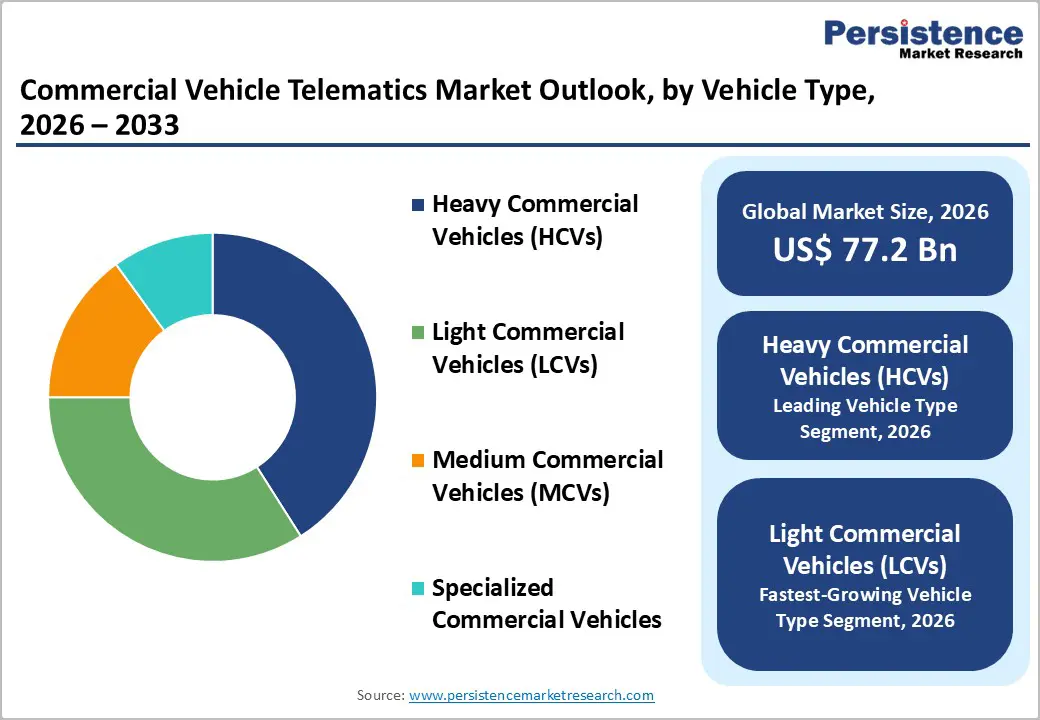

The global commercial vehicle telematics market size is likely to be valued at US$ 77.2 billion in 2026, and is projected to reach US$ 187.2 billion by 2033, growing at a CAGR of 13.5% during the forecast period 2026 - 2033.

With fleet operators increasingly digitizing operations and integrating advanced analytics into transportation workflows, the market is poised to experience steady expansion. Organizations are deploying telematics platforms to improve fuel efficiency, enhance vehicle utilization, and strengthen compliance with emissions and safety regulations. Specialists in telematics are incorporating AI capabilities to generate predictive insights that are improving operational decision-making and reducing downtime risks. Market growth is gaining momentum from the sustained adoption of telematics across both original equipment manufacturer (OEM) embedded systems and aftermarket deployments.

Macroeconomic and regulatory dynamics are reinforcing this growth trajectory. The International Transport Forum (ITF) projects that global freight demand will nearly triple by 2050. Governments are implementing compliance mandates, such as electronic logging devices (ELDs) in the U.S. and next-generation smart tachographs in the European Union (EU), which are accelerating technology adoption across commercial fleets. Electrification trends are further expanding telematics applications, as operators are using connected platforms to monitor battery health, optimize charging schedules, and manage total energy costs. Fleet managers are also integrating telematics with enterprise resource planning (ERP) and transportation management systems (TMS) to improve supply chain visibility and operational coordination.

Key Industry Highlights

- Vehicle Type Dominance: Heavy commercial vehicles (HCVs) are projected to contribute around 41% of total market revenue in 2026, reflecting higher telematics return on investment in long-haul freight operations

- Fastest-growing Vehicle Type: Light commercial vehicles (LCVs) are anticipated to grow the fastest through 2033 at about 14.9% CAGR, due to rapid expansion in e-commerce delivery networks.

- Regional Dynamics: North America is expected to dominate with an estimated 34% market share in 2026, owing to advanced fleet digitization, while Asia Pacific is set to be the fastest-growing market at roughly 15.2% CAGR, fueled by expanding logistics infrastructure.

- Application Leadership: Fleet management is estimated to account for nearly 32% of global revenues in 2026, driven by enterprise demand for route optimization and utilization monitoring.

- Technology Transformation: Increasing integration of AI, electric vehicle (EV) energy management, and predictive analytics platforms has transformed telematics into comprehensive fleet intelligence ecosystems with recurring software revenue models.

- February 2026: Geotab unveiled its next-generation GO and GO Plus telematics devices built on a unified architecture that delivers faster processing, high-fidelity data capture, and support for AI analytics.

| Key Insights | Details |

|---|---|

| Commercial Vehicle Telematics Market Size (2026E) | US$ 77.2 Bn |

| Market Value Forecast (2033F) | US$ 187.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Digitization of Fleet Compliance Systems to Meet Regulatory Requirements

Governments are increasingly implementing digital monitoring mandates to improve road safety outcomes, strengthen emissions compliance, and enhance labor transparency across commercial transportation sectors. Regulatory agencies are requiring fleet operators to adopt connected monitoring technologies that capture driver activity, vehicle performance, and operational data in real time. In the U.S., for example, the ELD rule of the Federal Motor Carrier Safety Administration (FMCSA) requires most commercial drivers to use telematics-enabled systems to record hours of service. Similarly, the EU introduced Smart Tachograph Version 2 requirements in 2024 under the EU Mobility Package, which will become mandatory for cross-border freight operations from 2025 onward. Emerging economies are also introducing regulatory frameworks such as the Automotive Industry Standard 140 (AIS-140) mandate in India that requires vehicle tracking systems for public transport fleets.

Regulatory digitization is extending its influence beyond compliance into broader fleet management strategies. Fleet operators are integrating telematics platforms to monitor driver working hours, optimize routing efficiency, and improve safety performance within centralized digital ecosystems. This integration is reducing operational risks and supporting insurance cost optimization, as insurers are increasingly offering telematics-linked pricing models based on driver behavior data. Organizations are also leveraging compliance-driven telematics investments to unlock secondary value through analytics, predictive maintenance insights, and operational automation. Governments are strengthening transport safety regulations and emissions reporting requirements, bolstering long-term demand prospects for telematics platforms.

Electrification of Commercial Fleets and Energy Optimization Needs

Commercial vehicle electrification is spurring the demand for specialized telematics capabilities that support battery performance monitoring, charging analytics, and energy cost optimization. Fleet operators are adopting connected platforms to track battery health, state of charge, and charging cycles in real time, which is expanding the functional scope of telematics beyond traditional internal combustion engine (ICE) vehicle monitoring. The International Energy Agency (IEA) reports sustained growth in electric truck adoption, supported by policy incentives and decarbonization programs across China, Europe, and North America. This transition is increasing the value proposition of telematics solutions by enabling operators to manage vehicle performance, range planning, and charging infrastructure utilization more effectively.

Fleet managers are increasingly using telematics platforms to optimize total cost of ownership for electric vehicles through intelligent charging scheduling and predictive maintenance insights. Logistics companies are deploying advanced analytics to reduce charging downtime, improve asset utilization, and minimize operational disruption across delivery networks. Integration with charging infrastructure management systems and enterprise platforms such as TMS and fleet management software is strengthening operational coordination. As electric commercial vehicle adoption continues expanding globally, telematics solutions are evolving into comprehensive energy and fleet intelligence platforms rather than simple tracking tools.

Cybersecurity and Data Sovereignty Risks in Connected Fleets

Connected commercial vehicles are generating huge volumes of operational and location data, exposing operators to cybersecurity threats. Regulatory authorities are strengthening requirements for vehicle cybersecurity governance to mitigate risks associated with unauthorized access, data manipulation, and operational disruption. The United Nations Economic Commission for Europe (UNECE) World Forum for Harmonization of Vehicle Regulations (WP.29) cybersecurity framework mandates vehicle manufacturers to implement certified cybersecurity management systems, which is raising compliance complexity for telematics providers and automotive OEMs. Security incidents involving fleet management platforms can disrupt logistics operations, expose sensitive route information, and create reputational and financial liabilities for fleet operators. These risks are forcing fleet companies to invest in secure data architectures, encryption protocols, and continuous monitoring systems, spiking deployment costs.

Cybersecurity requirements are also influencing cross-border fleet operations and technology procurement decisions. Data localization regulations in regions such as China and parts of Europe are requiring companies to store and process telematics data within national boundaries, which is complicating multinational fleet management strategies. Large enterprise fleets integrating multiple telematics platforms, ERP systems, and TMS are facing higher cybersecurity implementation costs due to system interoperability challenges. Smaller fleet operators are encountering adoption barriers because they often lack the technical expertise and financial resources required to maintain secure digital infrastructure. Constraints of such nature are slowing technology penetration among cost-sensitive segments, particularly in developing markets.

High Integration Costs and Fragmented Legacy Fleet Infrastructure

Telematics adoption has to confront integration challenges associated with legacy vehicle fleets and existing enterprise information technology (IT) environments. Several commercial fleet operators are managing heterogeneous vehicle portfolios that include multiple manufacturers, varying model years, and inconsistent onboard electronics architectures, which is requiring customized installation and configuration processes. Hardware retrofitting, system integration services, and workforce training programs are increasing upfront deployment costs, particularly for small and medium-sized enterprises that operate with limited capital budgets. Organizations are also needing to upgrade internal digital infrastructure to support data processing and analytics requirements, further extending implementation timelines.

Interoperability challenges are further increasing deployment complexity as telematics platforms must integrate with ERP systems, TMS, and fleet maintenance software to deliver full operational value. Fragmentation among telematics vendors is creating compatibility concerns because proprietary data formats and platform architectures are limiting seamless system integration. These structural barriers are particularly evident in emerging markets where fleet modernization remains uneven and digital maturity levels vary significantly across operators. Vendors that provide modular architectures, open application programming interfaces (APIs), and simplified deployment models are expected to reduce integration risks and accelerate adoption across diverse fleet environments over the coming years.

AI-Driven Predictive Fleet Intelligence Platforms

AI is transforming commercial vehicle telematics from passive monitoring solutions into predictive decision-support platforms that are improving operational efficiency across logistics networks. Fleet operators are deploying machine learning algorithms to forecast component failures, optimize route planning, and reduce fuel consumption through data-driven insights. Predictive maintenance applications are enabling organizations to identify potential mechanical issues before failures occur, lowering downtime and reducing repair costs. Industrial internet of things (IIoT) studies referenced by international manufacturing associations are indicating that predictive maintenance can reduce maintenance expenses by approximately 25% while improving asset utilization rates. Telematics providers are integrating advanced analytics modules into software platforms, opening avenues to introduce premium subscription tiers with higher recurring revenue potential.

The commercialization of AI-enabled telematics solutions is expected to generate substantial revenue opportunities by 2033, particularly among large enterprise fleets and global logistics operators that require advanced optimization capabilities. Vendors are increasingly combining telematics-generated data with external datasets such as traffic intelligence, weather forecasts, and supply chain performance metrics to deliver comprehensive fleet intelligence solutions. For instance, Iteris delivers real-time North American traffic data to vehicles through its ClearData engine, processing billions of GPS points and 150+ sources daily with AI integration. This convergence is positioning telematics providers as strategic technology partners rather than hardware vendors, which is strengthening customer retention and long-term contract value.

Fleet Digitization and Government Smart Mobility Programs in Developing Economies

Large, emerging economies of Asia, Latin America, and the Middle East are actively implementing smart transportation initiatives that are accelerating the deployment of commercial vehicle telematics solutions. Governments are promoting digital fleet monitoring systems to improve road safety performance, optimize fuel consumption, and enhance urban logistics efficiency within rapidly growing metropolitan areas. National programs are supporting connected vehicle adoption through regulatory mandates and infrastructure investments, which are creating favorable conditions for telematics expansion. For instance, India is advancing intelligent transport system initiatives to improve public transportation oversight, while China is investing heavily in smart logistics networks that integrate connected fleet technologies with digital freight platforms. These policy-driven developments are encouraging fleet operators to adopt telematics platforms as part of broader digital transformation strategies aimed at improving operational visibility and regulatory compliance.

Telematics penetration in new and emerging markets remains substantially lower than in North America and Europe, unlocking highly attractive long-term growth potential for technology providers. Market players that can offer localized software platforms, cost-efficient hardware configurations, and region-specific service models are positioning themselves to capture substantial market share across these high-growth regions. Strategic partnerships with government agencies, transportation authorities, and local fleet operators are further strengthening market entry opportunities. Companies that prioritize scalable deployment models and localized compliance capabilities are likely to benefit from sustained demand growth across logistics, public transportation, and commercial fleet modernization programs in these economies.

Category-wise Analysis

Application Insights

Fleet management is projected to account for approximately 32% of the commercial vehicle telematics market revenue share in 2026. Organizations are integrating routing optimization, dispatch coordination, asset utilization tracking, and workforce management into unified digital platforms to improve operational efficiency and cost control. Logistics operators are prioritizing these solutions as fuel prices remain volatile and driver shortages are continuing to affect productivity across freight networks. Fleet management platforms are also functioning as central integration hubs that support additional modules such as predictive maintenance, compliance monitoring, and energy management, which is strengthening vendor retention and expanding recurring software revenue streams.

Driver behavior and safety monitoring applications are expected to register the fastest growth between 2026 and 2033, aided by increasing investments in video telematics systems and AI risk analytics by fleet operators to reduce accident frequency, improve driver performance, and lower insurance costs. Insurance providers are increasingly incorporating telematics-derived behavioral data into underwriting models, incentivizing the deployment of safety monitoring technologies. Regulatory authorities are strengthening road safety requirements, further encouraging adoption across commercial transportation sectors. Integration with advanced driver-assistance systems (ADAS) and intelligent camera platforms is expanding functionality by enabling real-time alerts, driver coaching, and incident reconstruction capabilities.

Vehicle Type Insights

HCVs are expected to dominate with approximately 41% of the commercial vehicle telematics market share in 2026. Fleet operators managing long-haul transportation networks are increasingly deploying telematics solutions because the technology delivers measurable return on investment through fuel efficiency improvements, predictive maintenance planning, and route optimization. Heavy trucks typically operate at higher utilization rates and accumulate greater mileage compared to other vehicle classes, which is increasing the economic value of real-time monitoring and analytics. Large fleet sizes within this segment are also enabling economies of scale in telematics deployment, reinforcing market dominance and encouraging deeper integration with enterprise fleet management systems.

LCVs are anticipated to register the highest 2026-2033 CAGR of nearly 15%, powered by the proliferation of e-commerce and last-mile delivery services that need telematics to improve route efficiency, driver productivity, and asset utilization within urban logistics environments. Fleet operators are increasingly adopting connected platforms to manage delivery schedules, monitor vehicle performance, and optimize operational workflows in densely populated cities. Electrification trends within delivery vans are also creating new requirements for telematics capabilities related to battery monitoring, charging management, and energy optimization. Small and medium-sized fleet operators are progressively adopting digital fleet platforms as costs decline and software-as-a-service (SaaS) models become more accessible.

Regional Insights

North America Commercial Vehicle Telematics Market Trends

North America is slated to capture an estimated 37% of the commercial vehicle telematics market value in 2026 on the back of strong regulatory enforcement, mature logistics infrastructure, and high digital adoption across enterprise fleets. The U.S. drives regional demand owing to the ELD mandates issued by the FMCSA that have already accelerated widespread deployment of connected fleet systems. Fleet operators are continuing to invest in software as a service (SaaS) telematics platforms to improve productivity, reduce operating costs, and manage compliance requirements. The American Trucking Associations (ATA) has been reporting persistent driver shortages, pushing companies to adopt telematics-enabled workforce management and route optimization tools to enhance operational efficiency.

Technology innovation is concentrated in North America due to the presence of leading telematics providers, cloud computing firms, and AI analytics companies that are shaping next-generation fleet intelligence solutions. Investment is flowing into connected vehicle ecosystems, autonomous trucking pilot programs, and commercial fleet electrification initiatives. In Canada, the uptake of commercial vehicle telematics is gaining momentum as a result of government infrastructure investments and cross-border logistics integration with the U.S. Companies operating in North America are deeply focusing on value-added capabilities such as predictive analytics, energy optimization, and safety intelligence to sustain revenue growth and competitive differentiation during the 2026-2033 forecast period.

Europe Commercial Vehicle Telematics Market Trends

The Europe market is likely to progress at a notable pace through 2033, driven by stringent regulatory frameworks and sustainability objectives that are encouraging digital fleet transformation across transportation networks. The EU Mobility Package has introduced enhanced compliance requirements for driver working hours, cabotage operations, and cross-border freight monitoring, which is increasing demand for connected fleet solutions. The rollout of next-generation smart tachographs is further strengthening telematics penetration among commercial vehicle operators. Decarbonization policies promoted by the European Commission (EC) are accelerating commercial fleet electrification, expanding telematics applications related to battery performance monitoring, energy consumption optimization, and emissions reporting.

Germany, France, and the U.K. are leading regional adoption due to advanced logistics infrastructure, high digital maturity among transport operators, and strong enforcement of compliance regulations. European telematics providers are increasingly developing integrated mobility platforms that combine fleet management, regulatory reporting, sustainability analytics, and driver safety monitoring within unified software environments. Investment is also increasing in cross-border fleet visibility technologies to support seamless freight movement across the European single market. Partnerships between telematics vendors, vehicle manufacturers, and transportation authorities are strengthening ecosystem integration and providing impetus to innovation.

Asia Pacific Commercial Vehicle Telematics Market Trends

Asia Pacific is slated to secure about 30% of the global market for commercial vehicle telematics, and is expected to expand at an estimated CAGR of 15.2% through 2033. Growth is being driven by large commercial vehicle populations, rapid expansion of logistics networks, and strong government support for smart mobility initiatives. China is leading regional adoption due to well-established domestic telematics ecosystems, extensive deployment of connected vehicle technologies, and policy support for intelligent transportation infrastructure. India is also contributing to market expansion through regulatory mandates such as the AIS-140, which requires vehicle tracking systems in public transport fleets. Increasing urbanization and industrialization across major economies are encouraging fleet operators to adopt digital platforms that improve operational visibility, compliance management, and cost efficiency.

The ASEAN bloc is emerging as a high-growth sub-region as governments and private sector stakeholders are investing in transportation infrastructure modernization and digital freight platforms. Indonesia, Thailand, and Vietnam are experiencing increasing demand for telematics solutions due to expanding urban logistics activity and cross-border trade integration. Regional vendors are providing cost-efficient hardware and localized software platforms that address the needs of small and medium-sized fleet operators, which is improving accessibility and adoption rates. Asia Pacific is well-position to attract technology investments and strategic partnerships as telematics providers seek to capitalize on large-scale fleet digitization opportunities and strong long-term growth potential.

Competitive Landscape

Dominated by Verizon, Trimble, Geotab, MiX, and Omnitracs in terms of revenue share, the global commercial vehicle telematics market structure remains moderately fragmented. Competition is centered on hardware devices, software platforms, and integrated fleet management ecosystems that combine connectivity, analytics, and operational intelligence. Vendors are increasingly differentiating their offerings through advanced capabilities such as AI analytics, video-based safety monitoring, and cloud-delivered subscription services rather than relying solely on hardware performance. SaaS models are enabling recurring revenue generation and strengthening customer retention, which is shifting competitive focus toward platform scalability and data-driven value creation.

Leading market participants are actively forming partnerships with OEMs, telecommunications providers, and cloud computing companies to expand ecosystem integration and accelerate innovation. Mergers and acquisitions are increasingly targeting software analytics firms and regional telematics providers to strengthen technological capabilities and geographic presence in high-growth markets. Investment is also focusing on emerging areas such as electric fleet management, autonomous vehicle monitoring, and predictive maintenance platforms to capture future demand opportunities. Competitive intensity is expected to increase as traditional telematics providers are facing competition from mobility technology companies and digital platform firms that are entering the connected fleet sector.

Key Industry Developments

- In February 2026, SIXT van & truck launched a new telematics solution, Drive+, for its long-term hire customers, providing real-time insights into vehicle location, performance, and utilization through a single platform powered by Geotab technology. The solution also aims to support insurance discussions through driver behavior and risk data analytics.

- In February 2026, Daimler Truck North America (DTNA) teamed up with Class8 to deliver digital trucking tools for Freightliner owner-operators and small fleets, including ELD services, load optimization, and AI-based dispatch planning. The collaboration aims to simplify operations, improve profitability, and expand DTNA’s connected services ecosystem built on its Detroit Connect platform.

- In February 2026, Trimble partnered with Fleetsafe.ai to integrate its PC*Miler commercial mapping technology into the AI-powered video telematics platform, improving routing accuracy, map visualization, and real-time fleet awareness for global customers. The collaboration enhances driver safety, operational efficiency, and compliance by delivering fleet-optimized navigation tools and richer location intelligence.

Companies Covered in Commercial Vehicle Telematics Market

- Verizon Communications Inc.

- Trimble Inc.

- Geotab Inc.

- MiX Telematics Limited

- Omnitracs, LLC

- Teletrac Navman US Ltd

- TomTom N.V.

- Samsara Inc.

- Continental AG

- Robert Bosch GmbH

- AT&T Inc.

- Octo Group S.p.A.

- Zonar Systems, Inc.

- Inseego Corp.

- Bridgestone Mobility Solutions B.V.

Frequently Asked Questions

The global commercial vehicle telematics market is projected to reach US$ 77.2 billion in 2026.

Active digitization of operations and integrating advanced analytics into transportation workflows by fleet companies and soaring demand for freight globally are driving the market.

The market is poised to witness a CAGR of 13.5% from 2026 to 2033.

Incorporation of AI capabilities to generate predictive insights by specialists, implementation of compliance mandates, such as ELD, and fleet electrification drives that are expanding telematics applications are key market opportunities.

Verizon Communications Inc., Trimble Inc., Geotab Inc., and MiX Telematics Limited are some of the key players in the market.