- Home Appliances

- Commercial Laundry Equipment Market

Commercial Laundry Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Commercial Laundry Equipment market by Capacity Type (Up to 15 kg, 15-30 kg, 30-50 kg, Above 50 kg), Mode of Operation (Semi-automatic, Automatic), Application (Hospitality, Healthcare, Dry cleaners & laundromats, Others), and Regional Analysis for 2025 - 2032

Commercial Laundry Equipment Market Size and Trends Analysis

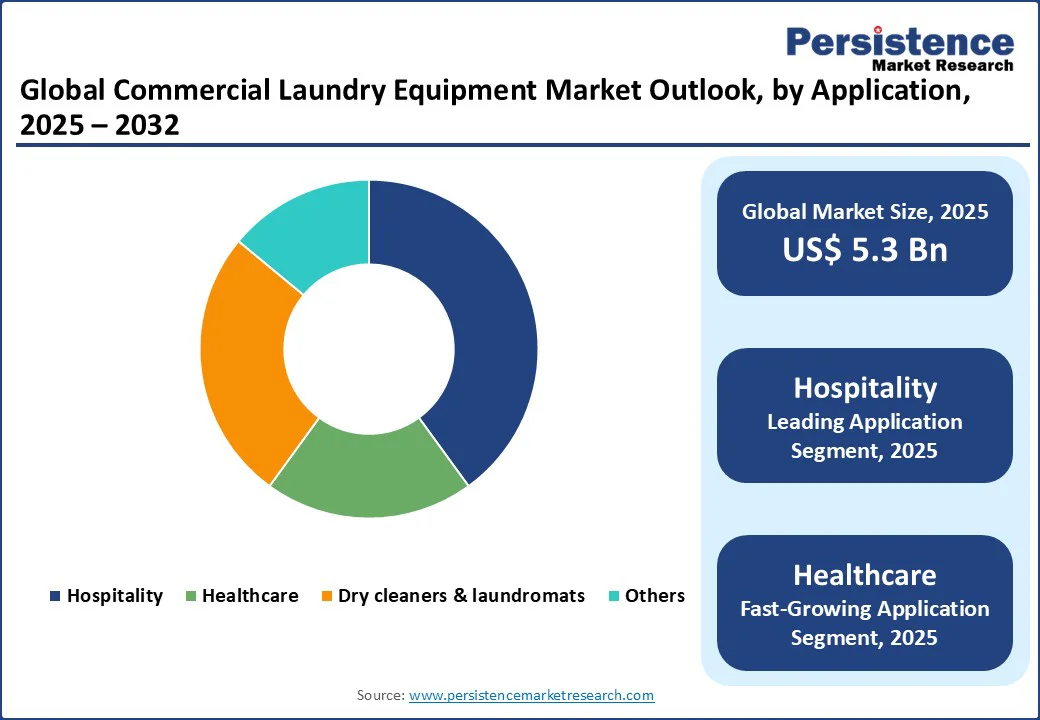

The global commercial laundry equipment market is projected to grow from US$5.3 Bn in 2025 to US$7.5 Bn by 2032, registering a CAGR of 5.1% during the forecast period from 2025 to 2032. The market has shown consistent growth, driven by heightened consumer awareness of hygiene and sanitation standards, particularly in healthcare and hospitality sectors. Rising demand for advanced, energy-efficient laundry solutions and the introduction of innovative equipment designs by leading manufacturers are further accelerating adoption, ensuring better performance, cost-effectiveness, and environmental sustainability across various industries.

Key Industry Highlights:

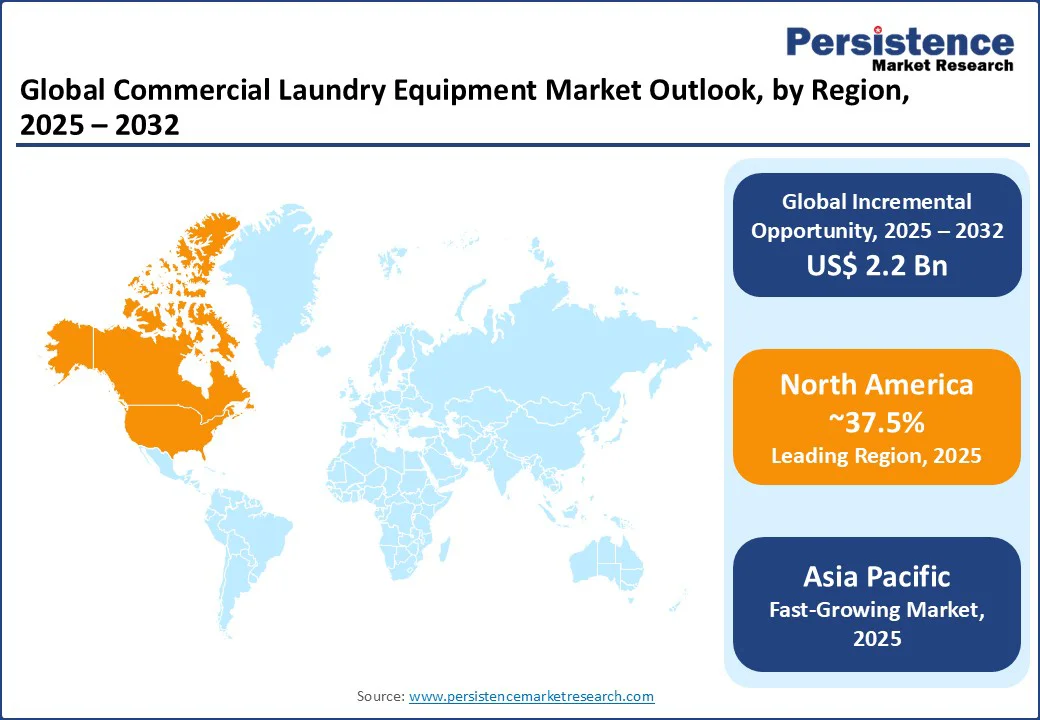

- Leading Region: North America holds a 37.5% market share in 2025, supported by advanced infrastructure, high consumer spending on commercial services, and strong manufacturer presence.

- Fastest-growing Region: Asia Pacific, driven by rapid urbanization, rising disposable incomes, and growing hygiene awareness in countries such as India, China, and Japan.

- Dominant Capacity Type in Commercial Laundry Equipment Market: 15-30 kg capacity accounts for nearly 45% of the market share, driven by demand for mid-sized equipment in hospitality and healthcare sectors.

- Leading Application: Hospitality leads with a 40% share, offering wide equipment availability for hotels and restaurants.

|

Global Market Attribute |

Key Insights |

|

Commercial Laundry Equipment Market Size (2025E) |

US$5.3 Bn |

|

Market Value Forecast (2032F) |

US$7.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.4% |

Market Dynamics

Driver- Rising Hygiene Awareness and Expansion of the Hospitality Sector Push Demand

The commercial laundry equipment market is propelled by increasing hygiene awareness and the expanding hospitality sector. The global rise in tourism and hotel infrastructure has driven demand for efficient, high-capacity laundry solutions. For instance, according to the UN Tourism, International tourism rebounded strongly in 2023 to reach 1.3 Bn arrivals, about 89% of the pre-pandemic figure, while receipts climbed to USD 1.5 trillion, virtually the same as in 2019. Boosting the need for clean linens and uniforms in hotels. Commercial washers and dryers, such as those with advanced sanitation features, align with hygiene standards and help reduce water and energy consumption.

Urbanization and busy lifestyles continue to drive demand for convenient laundry services. Dry cleaners and laundromats equipped with automatic machines are gaining popularity, especially in urban areas. In markets such as the U.S., consumers are increasingly opting for commercial laundry services as efficient alternatives to home washing. Government-backed hygiene programs further support market growth. In India, initiatives such as the Swachh Bharat Mission have promoted sanitation through public and institutional channels, encouraging the adoption of commercial equipment in healthcare and hospitality.

The rise of healthcare facilities has further driven demand for specialized laundry equipment. Hospitals require robust machines to handle high volumes of contaminated linens, with features such as ozone disinfection. For example, according to WHO data, global healthcare expenditure has grown significantly, leading to increased investments in laundry infrastructure to prevent infections.

Restraint- High Initial Costs and Maintenance Challenges Limit Adoption

The industry faces challenges due to high initial costs and maintenance requirements. Many operators question the long-term benefits of advanced machines because of concerns about energy consumption and repair needs. A survey by the Coin Laundry Association indicated that a significant share of U.S. laundromat owners avoided high-end equipment, citing high upfront costs and potential downtime. This skepticism restricts adoption among small businesses and those preferring basic models.

High production and installation costs for energy-efficient and smart equipment also hinder growth. Incorporating features such as IoT connectivity or water recycling increases manufacturing expenses. For example, equipping machines with smart sensors can significantly raise costs, as per industry estimates. These costs are often passed to consumers, limiting accessibility in price-sensitive markets such as rural Asia or Latin America.

Opportunity- Innovation in Energy-Efficient Equipment and Smart Technologies Boosts Consumption

The industry presents substantial opportunities through advancements in energy-efficient and smart technologies. The growing preference for eco-friendly machines aligns with increasing consumer demand for sustainability and regulatory pressure on energy use. Energy-efficient commercial washers have gained traction in regions promoting green building initiatives. Manufacturers can capitalize by introducing models that minimize water consumption, incorporate renewable energy integration, and feature IoT-based performance monitoring, helping businesses reduce operational costs while meeting environmental standards.

Sustainable practices are another growth avenue. With global concerns about water scarcity, brands are adopting water-saving technologies. In 2025, LG Electronics' sustainability report highlights that, in 2024, the company reduced product carbon emissions by 19.4 percent compared to 2020. Notably, LG was the first South Korean home appliance manufacturer to have its emissions reduction targets validated by the Science Based Targets initiative (SBTi). These targets include a 20 percent cut in Scope 3 emissions across seven key product categories by 2030 (based on a 2020 baseline).In the Asia Pacific, companies such as Haier are exploring IoT-enabled machines for remote monitoring, extending equipment life, and cutting operational costs.

The rise of e-commerce for equipment sales is creating opportunities. Online platforms offer subscription models and direct-to-business channels for purchasing commercial machines. Brands are using digital strategies to engage sectors such as hospitality, providing customized recommendations and financing options. This shift allows broader reach and loyalty among operators.

Category-wise Analysis

By Capacity Type

The commercial laundry equipment market is segmented into up to 15 kg, 15-30 kg, 30-50 kg, and above 50 kg. The 15-30 kg segment dominates, expected to account for approximately 45% of the commercial laundry equipment market share in 2025, due to its versatility for mid-sized operations in hotels and hospitals. Brands such as Alliance Laundry System and LG Electronics have strengthened their position through durable designs and energy-efficient features. Their suitability for frequent use in commercial settings drives adoption.

The above 50 kg segment is the fastest-growing, fueled by demand from large-scale facilities such as industrial laundries. These high-capacity machines appeal to operators handling bulk loads, particularly in healthcare. Products from Haier Group and GE Appliances, with advanced loading systems, have gained traction for efficiency in high-volume environments.

By Mode of Operation Type

Automatic machines lead the mode of operation, expected to account for 65% of the commercial laundry equipment market share in 2025. Their dominance stems from ease of use, efficiency, and integration with smart controls. Manufacturers such as Toshiba Corporation and IFB Industries offer extensive automatic ranges, catering to diverse needs in hospitality.

Semi-automatic machines are the fastest-growing, driven by affordability in emerging markets. These models provide flexibility for smaller operations, with companies such as Haier expanding offerings for cost-conscious buyers. The shift toward semi-automatic in developing regions boosts this channel’s growth.

By Application Type

The hospitality application dominates, expected to hold a 40% share in 2025. The surge in hotels and restaurants has driven demand for reliable equipment to maintain hygiene. Companies such as LG Electronics provide specialized solutions for linen processing, ensuring quick turnaround times.

The healthcare application is the fastest-growing, fueled by the need for sanitized equipment in hospitals. Post-COVID-19, adoption has increased for machines with disinfection features. For instance, providers are using equipment to comply with health standards, driving demand.

Regional Insights

North America Commercial Laundry Equipment Market Trends

In North America, the U.S. dominates the commercial laundry equipment market, having a market share of approximately 37.5%. Driven by high consumer spending on hygiene products. The U.S. market is experiencing strong growth, driven by evolving consumer preferences and rising hygiene consciousness. Automatic machines and high-capacity models continue to lead, supported by the increasing popularity of laundromats and the demand for energy-efficient equipment. Leading brands such as Alliance Laundry System and GE Appliances are expanding their offerings in the hospitality segment, while newer entrants are gaining traction with smart, IoT-enabled machines.

Clean-label and sustainable options are becoming increasingly important to consumers. Brands emphasizing eco-friendly features are seeing growing popularity due to natural designs and transparent operations. Sustainability is also a major focus in the U.S. market, with companies introducing water-saving technologies and committing to environmentally responsible practices. In the premium segment, ethical sourcing and transparency, such as the use of recycled materials, are emerging as key brand differentiators.

Europe Commercial Laundry Equipment Market Trends

Europe’s market is led by Germany, the U.K., and France, driven by stringent regulations and increasing consumer demand for efficient products. Germany maintains the largest market share, with a strong focus on automatic and high-capacity machines. The popularity of international brands such as Haier Group, along with local innovations, underscores this trend. Environmental policies under the EU’s Green Deal, along with restrictions on energy use, are encouraging companies to adopt sustainable solutions, with formats such as energy-efficient dryers gaining traction.

In the U.K., the sector is fueled by hygiene-conscious millennials and Gen Z consumers who favor smart, automatic equipment. Brands are expanding their offerings, emphasizing transparency and efficient profiles. Meanwhile, France is witnessing steady growth in healthcare applications, with products leading in preference. Regulatory encouragement for energy efficiency and environmentally friendly designs continues to support overall market growth across the region.

Asia Pacific Commercial Laundry Equipment Market Trends

Asia Pacific is expected to grow at the fastest rate from 2025 to 2032, led by India, China, and Japan. In India, hospitality and healthcare applications dominate the commercial laundry equipment market, driven by affordability and strong support from government-backed hygiene programs. Leading players such as IFB Industries Limited and LG Electronics have broadened their portfolios with automatic and mid-capacity options, effectively targeting both urban and rural demographics. The commercial laundry equipment market is bolstered by increasing hygiene awareness and the ongoing trend of urbanization.

China’s commercial laundry sector is largely propelled by demand for high-capacity and automatic machines. Prominent brands such as Haier Group and Toshiba Corporation continue to lead the segment. The expansion of the middle-income groups and growing interest in efficient services have significantly contributed to increased consumption, particularly in the dry cleaners category.

Competitive Landscape

The commercial laundry equipment market is highly competitive, with a mix of global giants and regional players vying for market share. Companies compete on product innovation, pricing, and distribution efficiency. The rise of energy-efficient and smart equipment has intensified competition, as consumers demand sustainability and technology. Digital marketing and partnerships with hospitality chains are key strategies for brand differentiation.

Key Developments

- In February 2024, the newest washing machines from LG Electronics have SmartThinQ technology, which allows users to remotely control and monitor laundry cycles using smartphones. This invention, which offers improved convenience and efficiency in laundry management, is in line with the expanding trend of smart home appliances. Users can maximize time and energy use by starting, pausing, or checking the status of their laundry from any location. LG's dedication to using technology to enhance user experiences in home appliance operations is demonstrated by the integration of SmartThinQ.

- In March 2024, Haier Group expanded its commercial portfolio in Europe by launching a new line of high-capacity machines. Formulated with water-saving features, these aim to support environmental goals, targeting eco-conscious operators.

Companies Covered in Commercial Laundry Equipment Market

- Alliance Laundry System LLC

- GE Appliances

- Haier Group

- IFB Industries Limited

- LG Electronics

- Toshiba Corporation

- Others

Frequently Asked Questions

The commercial laundry equipment market is projected to reach US$5.3 Bn in 2025.

Rising hygiene awareness, hospitality expansion, and government programs are the key market drivers.

The commercial laundry equipment market is poised to witness a CAGR of 5.1% from 2025 to 2032.

Innovation in energy-efficient equipment and smart technologies is the key market opportunity.

Alliance Laundry System LLC, LG Electronics, and Haier Group are among the key market players.