- Automotive Components & Materials

- CNG & LNG Commercial Vehicle Market

CNG & LNG Commercial Vehicle Market Size, Share, and Growth Forecast, 2025 - 2032

CNG & LNG Commercial Vehicle Market by Vehicle Type (Heavy-duty Trucks, Light-duty Trucks, Buses, Vans, Specialty Vehicles), Fuel Type (Compressed Natural Gas, Liquefied Natural Gas), Application (Passenger Transport, Freight Transport, Urban Transportation, Long Haul Freight, Construction and Mining), and Regional Analysis for 2025 - 2032

CNG & LNG Commercial Vehicle Market Size and Trends Analysis

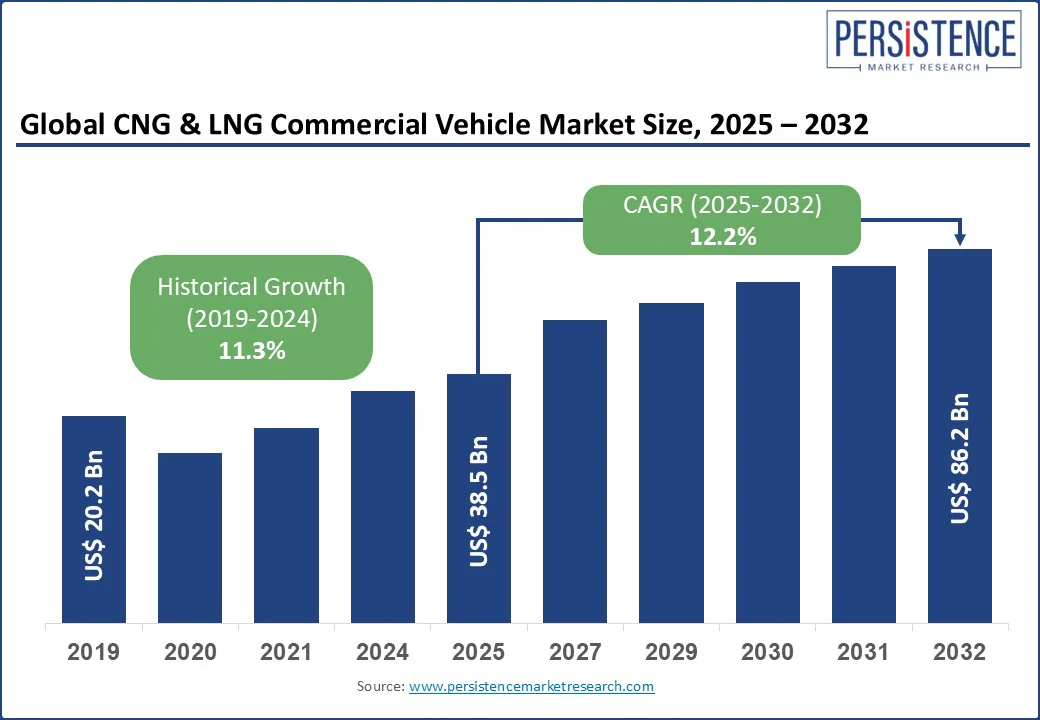

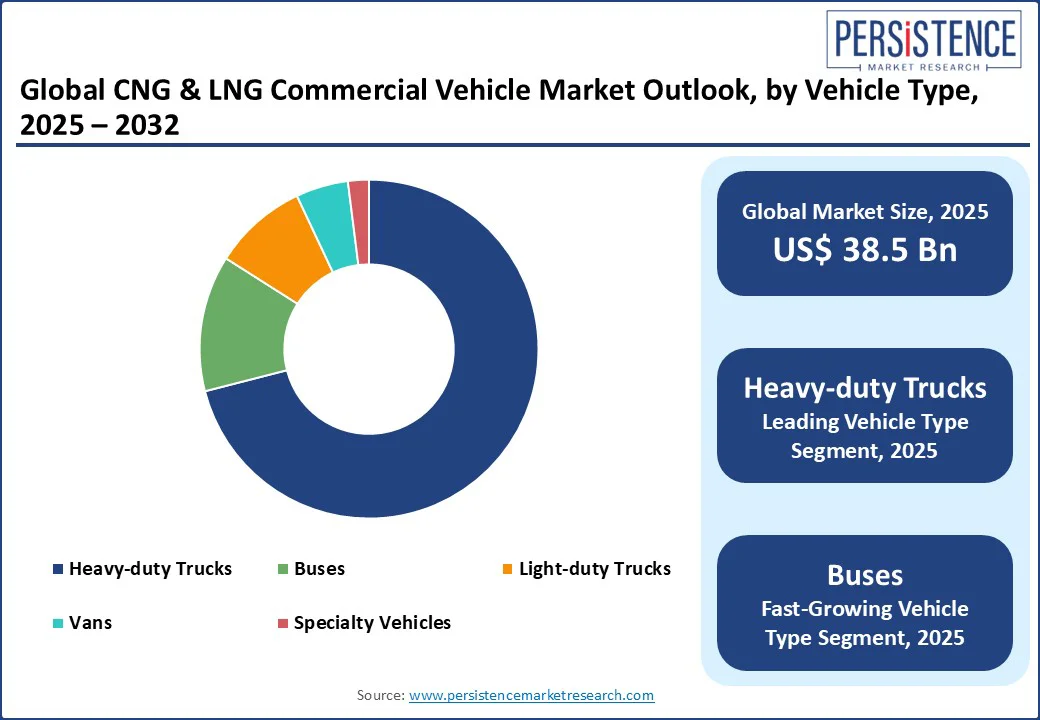

The global compressed natural gas (CNG) and liquefied natural gas (LNG) commercial vehicle market size is poised for significant growth, likely to be valued at US$38.5 Bn in 2025, and expected to reach US$86.2 Bn by 2032, achieving a CAGR of 12.2% during the forecast period from 2025 to 2032.

The sector is driven by increasing environmental regulations, advancements in natural gas vehicle technologies, and growing demand for cost-effective and sustainable transportation solutions. The industry benefits from the global push toward reducing carbon emissions, coupled with the economic advantages of natural gas as a cheaper alternative to diesel and gasoline.

Key Industry Highlights:

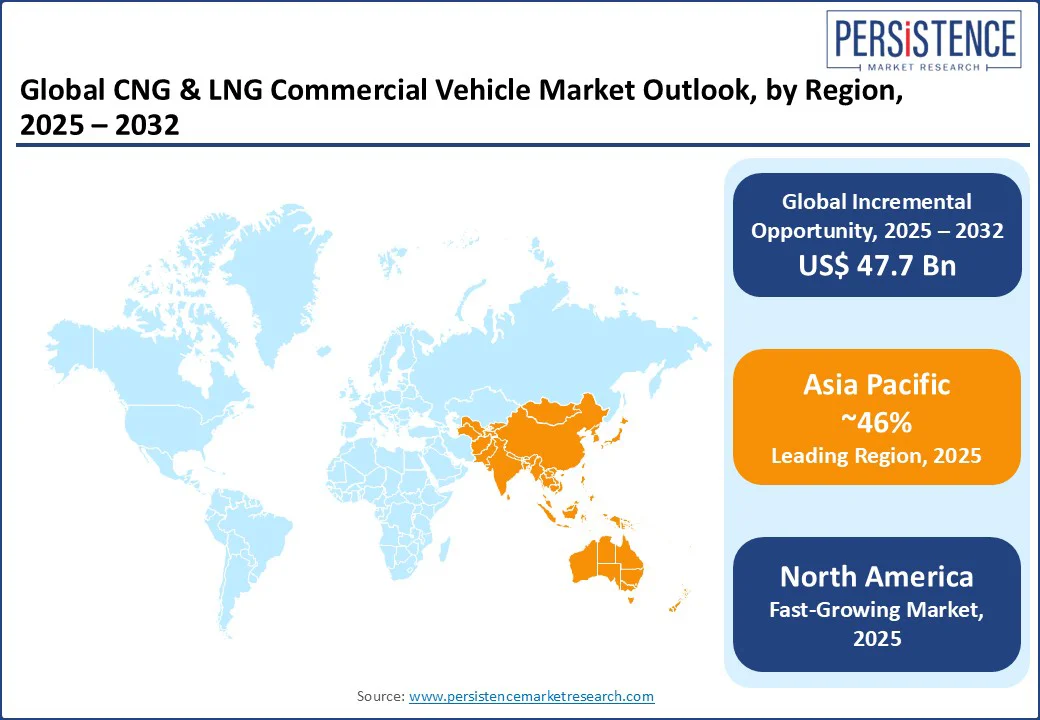

- Leading Region: Asia Pacific, holding a 46% market share in 2025, driven by rapid urbanization, supportive government policies, and large-scale adoption in countries such as China and India.

- Fastest-growing Region: North America, fueled by stringent emission standards, government incentives, and expanding refueling infrastructure in the U.S. and Canada. Europe is advancing through initiatives such as the European Green Deal, which promotes clean energy in transportation, boosting the adoption of CNG and LNG vehicles.

- Dominant Vehicle Type: Heavy-duty Trucks, commanding approximately 71% market share in 2025, due to their extensive use in freight and long-haul transport.

- Leading Application: Freight Transport, accounting for 42% of global market revenue, driven by the need for cost-effective and eco-friendly logistics solutions.

|

Global Market Attribute |

Key Insights |

|

CNG & LNG Commercial Vehicle Market Size (2025E) |

US$38.5 Bn |

|

Market Value Forecast (2032F) |

US$86.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

11.3% |

Market Dynamics

Driver - Stringent Environmental Regulations and Carbon Emission Reduction Goals

Stringent environmental regulations and global carbon emission reduction goals are key drivers propelling the growth of the CNG and LNG commercial vehicle market. Governments worldwide are implementing strict emission standards, such as Euro VI in Europe, BS-VI in India, and EPA regulations in the United States, to curb harmful pollutants such as nitrogen oxides (NOx), particulate matter (PM), and greenhouse gases (GHGs). These policies are pushing fleet operators and manufacturers to adopt cleaner fuel alternatives to diesel.

CNG and LNG vehicles offer significant environmental advantages, producing lower CO2 emissions and minimal particulate pollution compared to conventional engines. International agreements such as the Paris Climate Accord further intensify pressure on industries to transition toward sustainable transportation solutions.

For instance, China’s “Blue Sky” initiative actively promotes natural gas-powered trucks to improve air quality in urban areas, while in India, the government’s National Gas Grid expansion aims to make CNG more accessible nationwide, encouraging commercial fleet conversion to cleaner fuel options. This regulatory push, combined with growing public awareness of environmental issues, is accelerating the adoption of CNG and LNG commercial vehicles globally.

Restraint - Limited Refueling Infrastructure Challenges Growth

Limited refueling infrastructure is a significant restraint hindering the growth of the CNG and LNG commercial vehicle market. Unlike conventional diesel and petrol stations, CNG and LNG refueling facilities are relatively sparse, particularly in rural areas and along long-haul transport routes.

This lack of widespread availability creates “range anxiety” for fleet operators, discouraging them from adopting natural gas-powered vehicles despite their environmental and cost benefits.

Building CNG and LNG stations requires substantial investment in specialized equipment, storage tanks, and safety systems, which can be challenging for governments and private investors, especially in emerging economies. For instance, in many parts of Africa and Latin America, the inadequacy of LNG refueling corridors limits the viability of heavy-duty long-distance trucks.

Even in developed markets, LNG stations are concentrated mainly in specific freight corridors, leaving vast areas underserved. Without significant advancements in refueling network coverage, the full potential of CNG and LNG commercial vehicles may remain untapped.

Opportunity - Expansion of CNG and LNG in Emerging Markets

The expansion of CNG and LNG commercial vehicles in emerging markets presents a significant growth opportunity for the industry. Countries across the Asia Pacific, Latin America, and parts of Africa are increasingly shifting toward cleaner fuel alternatives to reduce air pollution and meet climate goals.

In the Asia Pacific, which holds around 40% of the global market share, nations such as China, India, and Pakistan are leading adoption due to supportive government policies, urbanization, and rising fuel costs.

For instance, India recorded a 46% year-on-year increase in CNG vehicle sales from January to August 2024 and has announced plans to add 4,500 new CNG stations to its network. Similarly, China’s “Blue Sky” initiative actively promotes LNG-powered heavy-duty trucks to improve air quality.

These developments, coupled with growing investments in refueling infrastructure and favorable tax incentives, are creating fertile ground for market players to expand their presence and capitalize on the increasing demand for sustainable transportation solutions.

Category-wise Analysis

Vehicle Type Insights

Heavy-duty Trucks dominate the CNG and LNG Commercial Vehicle Market, expected to account for approximately 71% of the industry share in 2025. Their dominance is driven by their widespread use in freight transport and long-haul logistics, where fuel efficiency and cost savings are critical.

Companies such as Volvo Group and Daimler Truck have introduced advanced CNG and LNG-powered heavy-duty trucks, such as the Volvo FH LNG and Mercedes-Benz Actros, which offer comparable performance to diesel trucks with lower emissions.

The Buses segment is the fastest-growing from 2025 to 2032, driven by increasing adoption in urban transportation and public transit systems. Cities worldwide are transitioning to CNG and LNG buses to meet emission reduction targets and improve air quality.

In Europe, cities such as Madrid and London are integrating LNG buses into their fleets as part of the European Green Deal. The scalability of CNG and LNG buses, coupled with their lower operating costs, makes them ideal for high-frequency urban routes, driving rapid growth in this segment.

Fuel Type Insights

CNG holds the largest market share, accounting for approximately 70% in 2025. Its dominance is attributed to its widespread availability, lower infrastructure costs compared to LNG, and suitability for light-duty trucks, vans, and buses. CNG vehicles are also easier to integrate into existing fleets due to their compatibility with smaller-scale refueling systems, making them a preferred choice for urban and regional applications.

LNG is the fastest-growing fuel type, driven by its higher energy density and suitability for long-haul freight and heavy-duty trucks. LNG offers a longer driving range compared to CNG, making it ideal for applications requiring extended travel distances. Companies such as Iveco and Scania are investing heavily in LNG-powered trucks, with models such as the Iveco Stralis NP and Scania G410 LNG gaining traction in Europe and North America.

Application Insights

Freight Transport commands the largest share, accounting for 42% of the global market revenue in 2025. The need for cost-effective and sustainable solutions in logistics and supply chain management drives the segment’s dominance. CNG and LNG trucks offer significant fuel cost savings and compliance with emission regulations, making them attractive for fleet operators.

Urban Transportation is the fastest-growing application, driven by the global push for cleaner public transit systems. Cities are increasingly adopting CNG and LNG buses and vans to reduce urban air pollution and meet sustainability goals. European cities are integrating LNG buses into their fleets, with initiatives such as the EU’s Clean Bus Deployment Initiative driving adoption. The scalability and environmental benefits of natural gas vehicles make this segment a key growth area.

Regional Insights

North America CNG & LNG Commercial Vehicle Market Trends

North America is emerging as a key market for CNG & LNG commercial vehicles, fueled by stringent emission standards, supportive government policies, and growing investments in clean transportation infrastructure.

In the United States, regulations set by the Environmental Protection Agency (EPA) and the California Air Resources Board (CARB) are pushing fleet operators toward low-emission alternatives, while federal and state-level incentives, such as tax credits and grants, are encouraging adoption. Canada is also taking significant steps, with programs such as the Green Freight Assessment Program promoting the transition to alternative fuels.

The expansion of CNG and LNG refueling infrastructure across major freight corridors, particularly in states such as California, Texas, and Pennsylvania, is reducing range anxiety and improving operational feasibility for long-haul and regional transport.

Additionally, rising fuel price volatility and the need to reduce dependency on diesel imports are prompting logistics companies and municipalities to shift toward natural gas-powered fleets, reinforcing North America’s leadership in this segment.

Europe CNG & LNG Commercial Vehicle Market Trends

Europe is emerging as a key market for CNG & LNG commercial vehicles, driven by strong environmental policies and the region’s commitment to reducing greenhouse gas emissions. Initiatives such as the European Green Deal and the EU’s “Fit for 55” package set ambitious targets for carbon neutrality, encouraging the adoption of cleaner fuels in transportation.

Many countries, including Germany, Italy, and France, offer tax incentives, subsidies, and toll exemptions for natural gas-powered trucks and buses. Italy remains a leader in CNG adoption, with an extensive refueling network supporting both passenger and commercial fleets, while Spain and the Netherlands are expanding LNG corridors for long-haul freight.

Additionally, major logistics companies in the region are transitioning their fleets to CNG and LNG to meet corporate sustainability goals. These combined efforts, along with continued investment in refueling infrastructure, position Europe as a fast-growing market for alternative fuel commercial vehicles, aligning with the EU’s long-term climate objectives.

Asia Pacific CNG & LNG Commercial Vehicle Market Trends

Asia Pacific dominates the global CNG & LNG commercial vehicle market, holding a 46% share in 2025, driven by rapid urbanization, favorable government policies, and the large-scale adoption of alternative fuel vehicles in major economies such as China and India.

In China, initiatives such as the “Blue Sky” policy actively promote LNG-powered heavy-duty trucks to curb air pollution and meet carbon neutrality goals. India is experiencing a surge in CNG adoption, with a 46% year-on-year increase in CNG vehicle sales from January to August 2024, alongside government plans to add 4,500 new CNG stations nationwide.

Additionally, Southeast Asian countries, including Thailand and Indonesia, are investing in infrastructure and subsidies to encourage fleet operators to switch to cleaner fuels. The region’s growing freight and logistics demand, combined with rising fuel prices and environmental concerns, is further accelerating the transition toward CNG and LNG, making Asia Pacific the largest and most influential market globally.

Competitive Landscape

The Global CNG & LNG commercial vehicle market is characterized by intense competition, with key players focusing on technological innovation, cost efficiency, and regional expansion. Companies compete on fuel efficiency, vehicle range, and compliance with emission standards. Strategic partnerships with refueling infrastructure providers and government agencies are common to enhance market penetration.

Volvo and Scania are focusing on LNG for long-haul applications, while Iveco and MAN Truck & Bus prioritize CNG for urban transport. Partnerships with energy companies, such as PACCAR’s collaboration with Shell, aim to expand refueling networks. In Asia, Dongfeng and Sinotruk leverage government subsidies to offer competitive pricing, while Daimler Truck focuses on integrating advanced telematics for fleet optimization.

Key Developments:

- December 2024: Clean Energy Fuels signed renewable natural gas (RNG) supply agreements with DHL (100,000 gallons per year), Food Express (3 million gallons over 10 years), and LA Metro (14 million gallons), showing growing adoption among fleets.

- October 2024: Nissan India announced that its USD 700 million program will include both CNG and hybrid vehicle options, to reach a 3% market share in India by 2026.CNG & LNG Commercial Vehicle Market Report Scope.

Companies Covered in CNG & LNG Commercial Vehicle Market

- Volvo Group

- Iveco

- PACCAR

- Scania

- MAN Truck & Bus

- Daimler Truck

- Dongfeng Motor Group

- Shaanxi Heavy Duty Automobile

- Sinotruk

- Others

Frequently Asked Questions

The Global CNG & LNG Commercial Vehicle Market is projected to reach US$ 38.5 Bn in 2025.

Stringent environmental regulations and the cost advantage of natural gas over diesel are key drivers.

The CNG & LNG Commercial Vehicle market is poised to witness a CAGR of 12.2% from 2025 to 2032.

Expansion in emerging markets such as India and Brazil offers significant growth potential.

Volvo Group, Iveco, PACCAR, Scania, and MAN Truck & Bus are among the key players.