- Food Packaging

- Food Cold Chain Market

Food Cold Chain Market Size, Share, and Growth Forecast, 2025 - 2032

Food Cold Chain Market By Component (Refrigerated Storage, Refrigerated Transportation, Others), Temperature Type (Chilled, Frozen), Application, and Regional Analysis for 2025 - 2032

Food Cold Chain Market Size and Trends Analysis

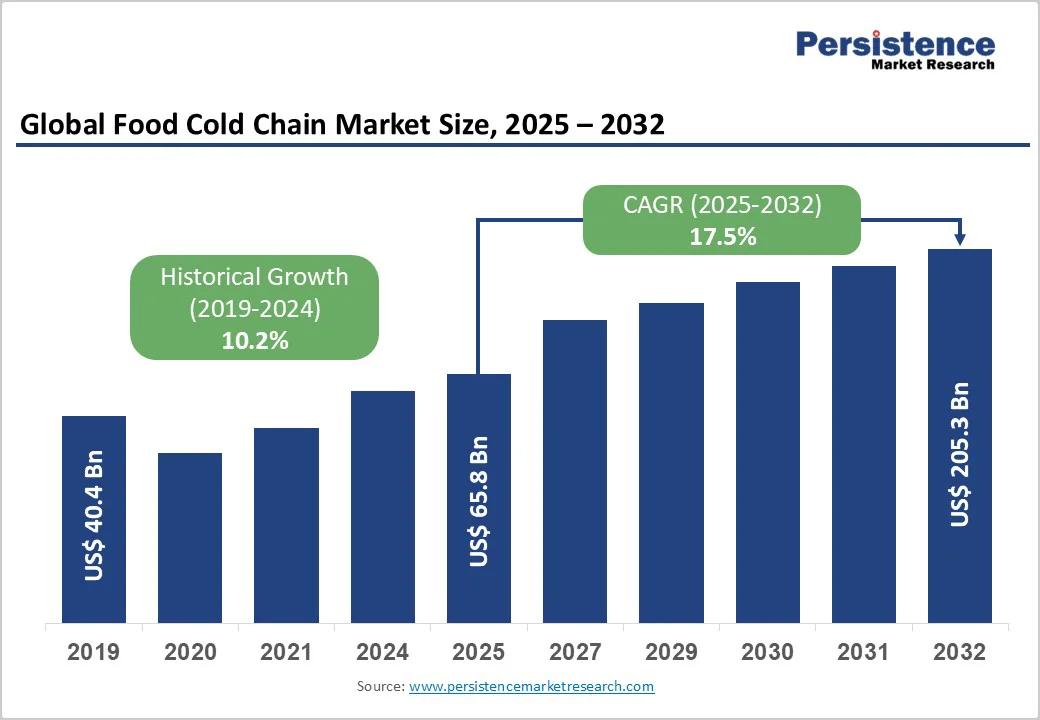

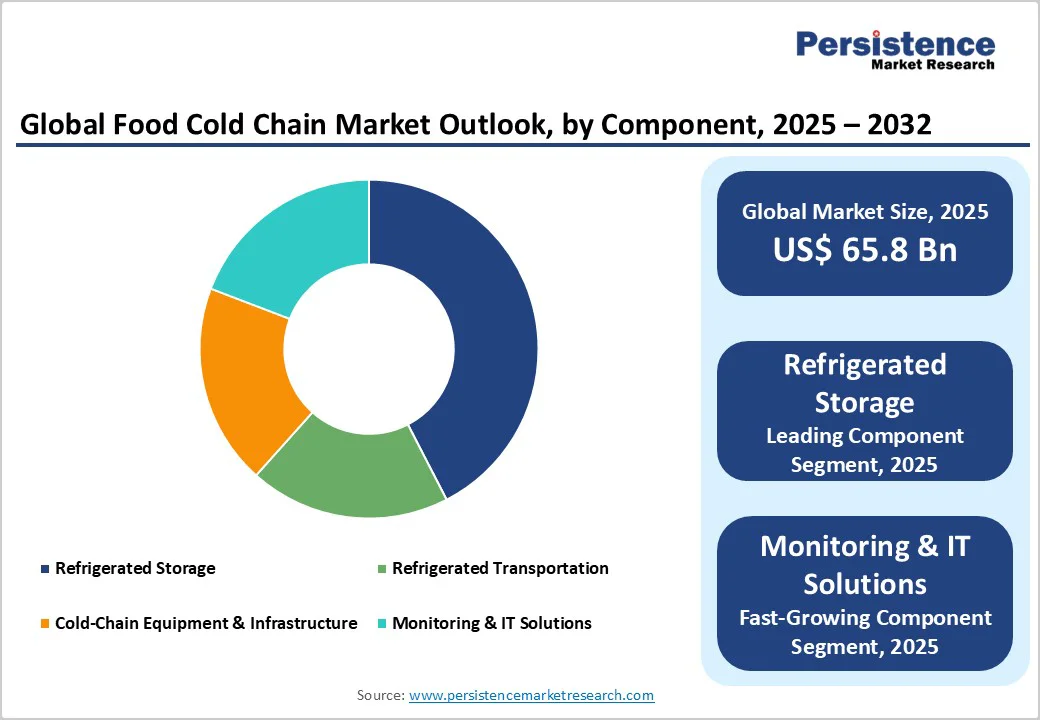

The global food cold chain market is expected to reach US$65.8 billion in 2025. It is expected to reach US$205.3 billion by 2032, growing at a CAGR of 17.5% during the forecast period from 2025 to 2032, driven by the surging global demand for temperature-controlled logistics to reduce food spoilage, meet quality standards, and comply with safety regulations.

Growth is driven by rising demand for frozen and packaged foods, expanding quick-service restaurants, and increasing cross-border trade of perishables. Digital cold chain systems and sensor-based monitoring are boosting efficiency and traceability across the supply chain.

Key Industry Highlights

- Leading Region: North America, commanding 32% of the global market share in 2025, driven by advanced infrastructure, automation, and stringent food safety regulations under the FSMA.

- Fastest-growing Region: Asia Pacific, propelled by large-scale investments in cold storage capacity in China and India, and the surge in e-commerce food logistics.

- Investment Plans: Global investments are increasingly focused on sustainable cold chain infrastructure, with companies such as Lineage Logistics, Americold, and Snowman Logistics announcing expansions worth over US$5 billion cumulatively between 2023 and 2025 in automation, green refrigeration, and renewable-powered cold storage facilities.

- Dominant Component: Refrigerated Storage, leading with a 58.6% share of total market revenue in 2025, supported by high utilization in meat, seafood, and frozen food warehousing across major economies.

- Leading Temperature Type: Frozen Segment, accounting for over 59.7% of total market volume in 2025, fueled by global consumer demand for frozen meals, seafood, and processed meat products.

| Key Insights | Details |

|---|---|

|

Food Cold Chain Market Size (2025E) |

US$65.8 Bn |

|

Market Value Forecast (2032F) |

US$205.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

17.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

10.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Processed and Frozen Foods

Global consumption of processed and frozen foods has increased significantly, fueled by rapid urbanization and lifestyle shifts. According to the Food and Agriculture Organization (FAO), demand for processed food has grown by more than 30% globally since 2018, especially in emerging economies such as India and Indonesia. The expansion of e-commerce grocery delivery services has further boosted cold storage and distribution needs. Major retailers and online food platforms are investing heavily in cold storage infrastructure, with online grocery penetration expected to reach over 20% of global grocery sales by 2030. These trends directly stimulate cold chain expansion, ensuring safe and quality food delivery.

Stringent Food Safety and Quality Regulations

Food safety regulations worldwide have become more comprehensive, compelling companies to adopt reliable cold chain logistics. The U.S. Food Safety Modernization Act (FSMA) and the European Union’s General Food Law (EC 178/2002) emphasize temperature control, traceability, and the prevention of contamination. Regulatory compliance has increased investments in IoT-based temperature tracking and real-time logistics analytics. According to the Global Cold Chain Alliance (GCCA), over 70% of food exporters in North America and Europe now use digital monitoring solutions to meet compliance standards, reinforcing the importance of cold chain efficiency and transparency.

Expansion of Global Perishable Trade

The growing international trade of meat, seafood, dairy, and fresh produce requires robust cold chain systems. FAO data shows that perishable food exports grew by 5.6% annually between 2018 and 2023, driven by Asia-Pacific and Latin America. Emerging economies are scaling up cold chain infrastructure to support the export of fruits, vegetables, and seafood. For instance, India’s refrigerated warehouse capacity expanded by 35% between 2020 and 2024, while China’s has surpassed 200 million cubic meters, underscoring how infrastructure modernization fuels trade expansion and revenue growth across the cold chain ecosystem.

Barrier Analysis - High Infrastructure and Energy Costs

Cold storage construction and maintenance are capital-intensive, with costs averaging US$150-250 per square foot depending on temperature requirements. Refrigeration systems account for nearly 60% of total operating costs, driven by high energy consumption. Small and mid-sized logistics firms in emerging economies often struggle to invest in advanced cold storage technologies, leading to uneven distribution of cold chain capacity globally. Rising energy prices also put pressure on profitability, particularly in regions with limited renewable energy integration.

Fragmented Logistics and Temperature Gaps

Developing regions continue to face fragmented logistics networks and last-mile inefficiencies. In countries such as India and Indonesia, up to 30% of perishable produce is lost annually due to inadequate temperature control during transport. Lack of standardization in reefer vehicles, insufficient rural infrastructure, and weak intermodal connectivity limit the efficiency of cold chain operations. These systemic gaps hinder optimal utilization of storage and transportation capacities.

Opportunity Analysis - Integration of IoT and Data-Driven Cold Chain Systems

The adoption of IoT, artificial intelligence (AI), and blockchain for temperature tracking, predictive maintenance, and inventory optimization presents substantial opportunities. The digital cold chain solutions market is expected to exceed US$12 billion by 2030, enabling real-time traceability and automated compliance reporting. IoT-based cold chain platforms reduce spoilage by up to 15% and improve energy efficiency by 10-12%, representing a strong investment area for logistics technology providers.

Emerging Cold Chain Infrastructure in Developing Economies

Rapid infrastructure development in the Asia Pacific, Latin America, and Africa is unlocking major opportunities. India’s cold chain market is growing at a CAGR of over 20%, driven by government incentives under the Pradhan Mantri Kisan SAMPADA Yojana. Similarly, Indonesia and Vietnam are witnessing significant foreign direct investment (FDI) in cold storage and reefer container projects. By 2032, emerging economies are projected to account for over 45% of new cold chain capacity additions, creating lucrative opportunities for investors and equipment manufacturers.

Rising Demand for Sustainable Cold Chain Solutions

Sustainability and energy efficiency are emerging as critical differentiators. The market for eco-friendly refrigerants (such as CO2 and ammonia systems) is expanding rapidly as global regulations phase down hydrofluorocarbons (HFCs). Cold chain operators adopting renewable-powered and low-emission refrigeration systems are likely to achieve up to 25% energy savings and qualify for green financing mechanisms. These trends are transforming sustainability from a compliance obligation into a strategic opportunity.

Category-wise Analysis

Component Insights

Refrigerated storage dominates the market with a share of over 58.6% in 2025, supported by expanding frozen food inventories and supermarket distribution centers. The proliferation of large-scale cold storage facilities in China, India, and the U.S. underpins this dominance. Public refrigerated warehouses, offering flexible rental models, are seeing increased utilization rates of 85-90%, especially among food exporters and importers managing seasonal surpluses. Companies are adopting automation and robotic palletization systems to optimize throughput and reduce manual handling.

The monitoring and IT solutions segment is the fastest-growing, driven by demand for real-time temperature monitoring, predictive maintenance, and traceability. Implementation of smart sensors and blockchain technology is enabling digital record-keeping and automated compliance. Food manufacturers and logistics providers are integrating IoT systems with enterprise resource planning (ERP) tools to streamline quality assurance and supply chain transparency.

Temperature Type Insights

The frozen category represents the largest market share, accounting for over 59.7% of the total food cold chain market in 2025. Rising global consumption of frozen meals, meat, and seafood, coupled with extended product shelf life, drives this dominance. Retailers across North America and Europe continue to expand freezer sections to cater to changing consumer preferences for convenience. Advanced freezing technologies such as individual quick freezing (IQF) and blast freezing maintain product quality and reduce microbial growth.

The chilled segment is the fastest-growing segment, led by growing demand for fresh produce, dairy products, and ready-to-eat meals. The segment benefits from urban consumers seeking minimally processed foods with fresh appeal. Investments in short-haul chilled transport and city-based micro cold storage facilities are driving this growth, particularly in Asia’s megacities.

Application Insights

Meat and seafood represent the largest application, contributing to about 41% of market revenue in 2025. Global seafood exports surpassed US$170 billion in 2023, emphasizing the reliance on efficient cold logistics. Major exporters in Norway, China, and India are adopting high-capacity reefer fleets and advanced storage systems to maintain export competitiveness. The segment continues to benefit from the rising consumption of animal protein and seafood in both developed and emerging markets.

The fruits and vegetables segment is the fastest-growing segment. With increasing awareness of post-harvest losses and growing demand for fresh produce exports, governments and cooperatives are investing in farm-level pre-cooling and pack-house facilities. Countries, including India and Brazil, have launched targeted programs to build rural cold storage hubs to minimize wastage and boost farmer incomes.

Regional Insights

North America Food Cold Chain Market Trends - Technologically Advanced & Sustainability-Focused Cold Chain Infrastructure

North America accounted for over 31.3% of the global market share in 2025, driven by well-established infrastructure and advanced regulatory frameworks. The U.S. leads the region with large-scale refrigerated warehousing capacities exceeding 180 million cubic meters. Strict enforcement of the FSMA and demand from major food retail chains such as Walmart and Kroger drive technology adoption. The region’s emphasis on sustainability has led to widespread use of low-GWP refrigerants and renewable-powered warehouses.

Key investments include Lineage Logistics’ expansion of its automated cold storage facilities and Americold’s acquisition of new distribution centers. Canada is focusing on modernizing its cold chain for seafood exports, while Mexico’s fresh produce exports to the U.S. are fueling cross-border cold logistics demand. With continuous integration of automation, robotics, and digital temperature monitoring, North America will remain a pivotal market through 2032.

Europe Food Cold Chain Market Trends - Green Transition & Regulatory Alignment Driving Cold Chain Standardization

Europe holds a market share of approximately 27% in 2025, led by Germany, the U.K., France, and Spain. The region’s strong policy alignment under the EU Green Deal and harmonized food safety regulations has stimulated cold chain standardization. Demand for organic, fresh, and plant-based foods drives the expansion of chilled logistics services. European logistics providers are investing in hydrogen-powered refrigerated trucks and CO2-based refrigeration systems to meet sustainability mandates.

Germany’s cold storage market benefits from proximity to major food producers and retailers, while the U.K. market is adapting to post-Brexit trade complexities through enhanced border storage facilities. The European Cold Chain Confederation (ECCC) is promoting digital traceability across member states, boosting transparency and operational resilience. Europe’s transition toward net-zero logistics will further accelerate the adoption of green cold chain technologies by 2032.

Asia Pacific Food Cold Chain Market Trends - Rapidly Expanding Cold Chain Fueled by Infrastructure Growth & E-Commerce Demand

Asia Pacific is the fastest-growing regional market, projected to grow at a CAGR above 22% from 2025 to 2032, supported by rapid infrastructure investments and rising middle-class consumption. China dominates the region with an extensive cold storage network exceeding 200 million cubic meters and a rapidly expanding e-commerce food delivery ecosystem. India’s cold chain capacity is growing at more than 20% annually, backed by public-private partnerships and agri-infrastructure schemes.

Japan and South Korea are focusing on automation and energy-efficient cold storage systems, while ASEAN countries are expanding cold chain corridors to support export-driven agribusinesses. The region’s expanding seafood, dairy, and fruit exports are key drivers of growth. By 2032, the Asia Pacific is expected to represent over 40% of global food cold chain capacity, driven by strong domestic demand and export-oriented logistics modernization.

Competitive Landscape

The global food cold chain market remains moderately consolidated, with the top ten players holding about 55% of the global market share. Market leaders such as Lineage Logistics, Americold Logistics, and Nichirei Logistics dominate through extensive storage capacities and strategic acquisitions. Mid-sized regional firms focus on niche transport and chilled logistics services.

The competition is increasingly based on technology integration, energy efficiency, and service reliability. Market leaders emphasize technological innovation, sustainability, and global expansion as core strategies. Partnerships with retail and e-commerce players, investment in renewable energy cold storage, and the use of AI-based logistics optimization tools are shaping the competitive edge across the industry.

Key Industry Developments

- In April 2024, Lineage Logistics expanded its automated cold storage facility in Texas, integrating AI-based warehouse management systems to increase throughput by 30%.

- In June 2024, Americold Logistics acquired two major cold storage facilities in Spain to strengthen its European distribution network and reduce cross-border transit time.

- In March 2025, Snowman Logistics (India) launched a sustainable cold storage park powered by solar energy, setting a precedent for green logistics infrastructure in Asia.

Companies Covered in Food Cold Chain Market

- Lineage Logistics Holdings, LLC

- Americold Logistics, LLC

- United States Cold Storage, Inc.

- Nichirei Logistics Group, Inc.

- Kloosterboer Group B.V.

- NewCold Advanced Cold Logistics

- Burris Logistics

- VersaCold Logistics Services

- Snowman Logistics Ltd.

- Frialsa Frigoríficos S.A. de C.V.

- Swire Cold Storage Ltd.

- AGRO Merchants Group

- Preferred Freezer Services

- Congebec Logistics

- Henningsen Cold Storage Co.

- XPO Logistics, Inc.

- DHL Supply Chain (Deutsche Post AG)

- Maersk Cold Chain Logistics

- Trenton Cold Storage Inc.

- Interstate Warehousing, Inc.

Frequently Asked Questions

The market size in 2025 is estimated at US$65.8 Billion, supported by the rising demand for temperature-controlled storage and transport of perishable food products.

By 2032, the market is projected to reach US$205.3 Billion.

Key trends include the integration of IoT-based temperature monitoring, the use of sustainable refrigerants, automation in cold warehousing, and the rapid expansion of e-commerce-driven grocery logistics, especially in Asia Pacific.

The refrigerated storage segment leads the market with a 58% share in 2025, owing to strong demand for long-term preservation of frozen food, seafood, and dairy products.

The food cold chain market is projected to grow at a CAGR of 17.5% from 2025 to 2032.

Major companies include Lineage Logistics Holdings, LLC, Americold Logistics, LLC, Nichirei Logistics Group, Inc., NewCold Advanced Cold Logistics, and DHL Supply Chain (Deutsche Post AG).