- Electrical Equipment & Services

- Carbon Brush Market

Carbon Brush Market Size, Share, and Growth Forecast, 2025 - 2032

Carbon Brush Market By Product Type (General Graphite, Metal Graphite, Carbon Graphite, Electro Graphite, Silver Graphite, and Resin-Bonded Graphite), Application (Motor, Generator & Alternator, Current & Signal Transmission, and Grounding Devices), Regional Analysis for 2025 - 2032

Carbon Brush Market Size and Trends Analysis

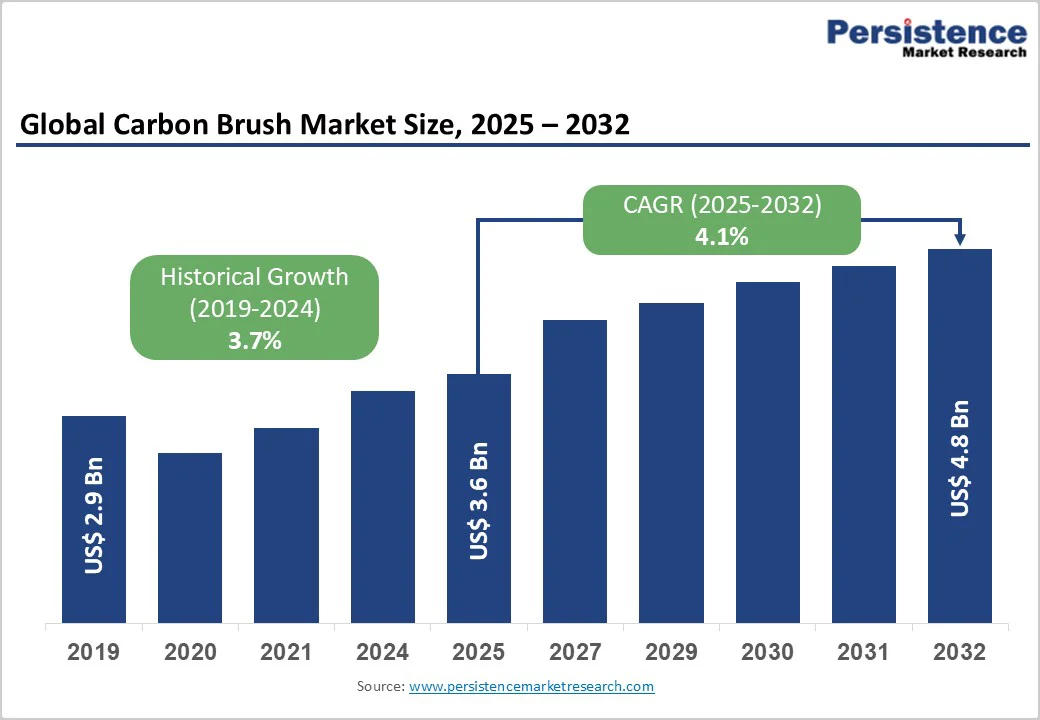

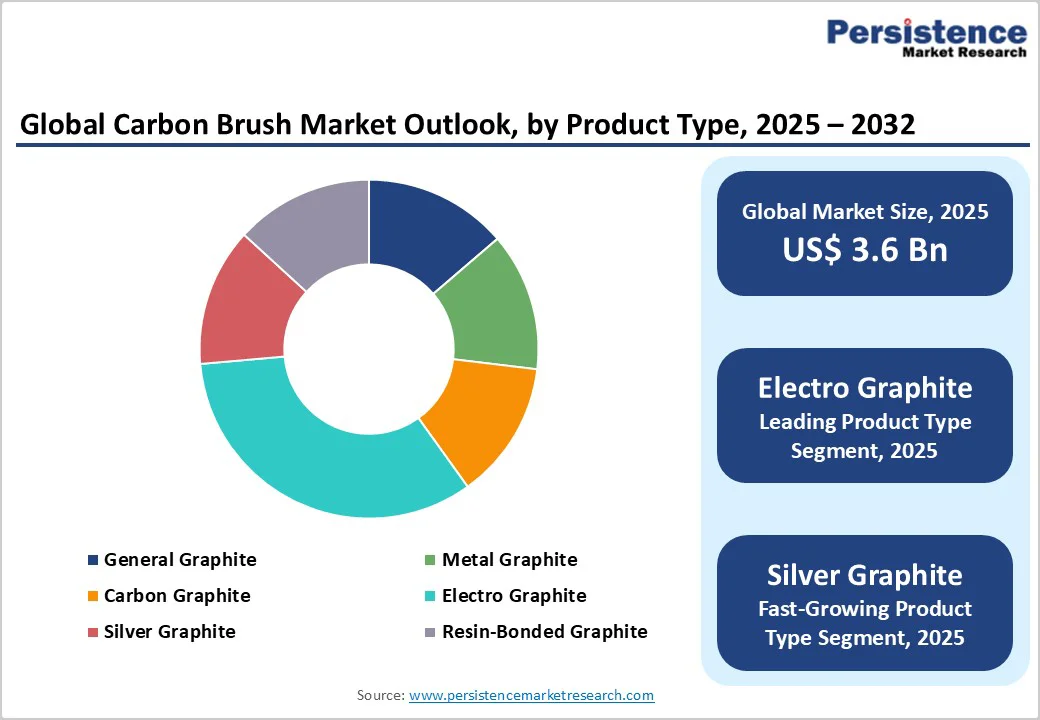

The global carbon brush market is expected to reach US$3.6 billion in 2025. It is expected to reach US$4.8 billion by 2032, growing at a CAGR of 4.1% from 2025 to 2032, driven by accelerating electrification across the automotive and industrial sectors, particularly through rising electric vehicle (EV) adoption and the development of renewable energy infrastructure that requires reliable electrical power transmission components.

Industrial automation expansion, modernization of aging electrical equipment, and stringent efficiency standards mandating high-performance carbon brushes across motor, generator, and alternator applications sustain consistent market demand globally.

Key Market Highlights

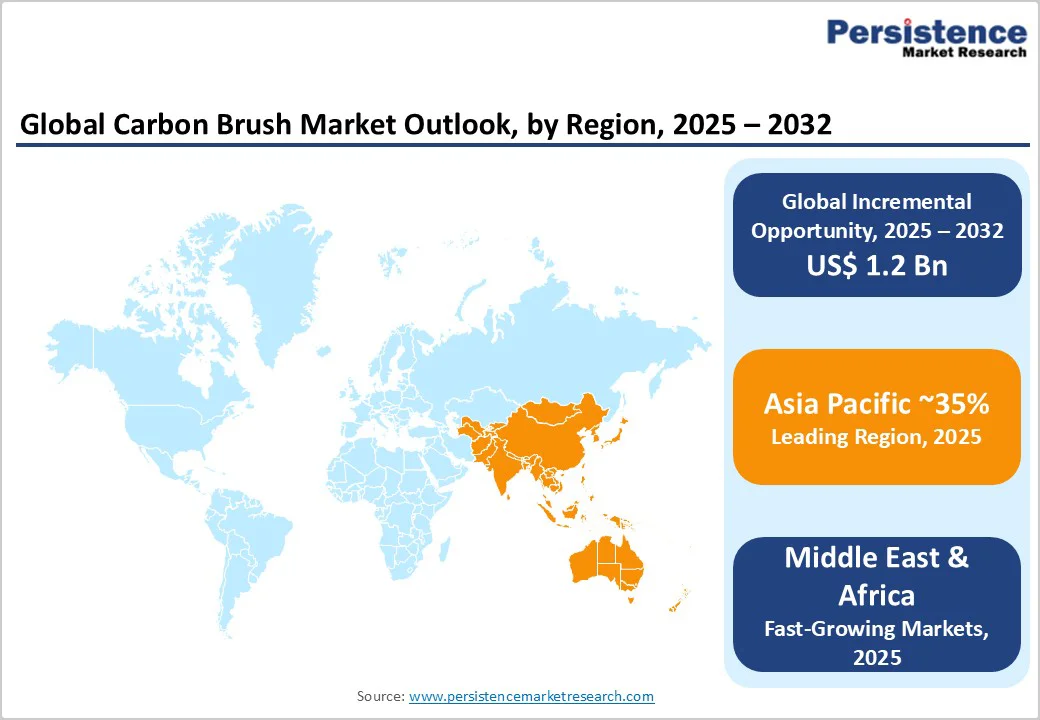

- Leading Region: Asia Pacific commands a dominant market position with 49% market share, driven by extensive manufacturing capacity, accelerating automotive electrification, expanding industrial automation, and rapid urbanization, which support sustained carbon brush demand.

- Fastest-growing Region: Asia Pacific demonstrates the highest growth trajectory, propelled by emerging market industrialization, infrastructure development investments, and automotive manufacturing expansion across China, India, and Southeast Asia.

- Dominant Product Type: Electro Graphite carbon brushes command the largest product type segment with 38% market share, delivering superior electrical conductivity and extended service life for demanding industrial applications.

- Fastest Product Type: Silver Graphite carbon brushes represent the fastest-growing material segment, driven by premium applications in aerospace, precision instruments, and high-performance wind energy systems.

- Key Market Opportunity: Renewable energy sector expansion and wind turbine manufacturing growth create substantial demand for specialized high-performance carbon brushes.

| Key Insights | Details |

|---|---|

|

Carbon Brush Market Size (2025E) |

US$3.6 Bn |

|

Market Value Forecast (2032F) |

US$4.8 Bn |

|

Projected Growth CAGR(2025-2032) |

4.1% |

|

Historical Market Growth (2019-2024) |

3.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Surging Electric Vehicle Production and Automotive Electrification

The automotive industry's accelerating transition toward EVs represents the primary growth catalyst for the carbon brush market globally. EV production expanded at approximately 18% CAGR from 2019-2024, with global EV sales exceeding 14 million units in 2024 according to industry data. Carbon brushes are essential components in EV motors, facilitating efficient electrical energy transmission between stationary and rotating components.

Automotive electrification extends beyond passenger vehicles to commercial trucks and buses, creating diverse carbon brush applications across vehicle electrical systems, including power windows, seat adjusters, and autonomous driving components. Government mandates targeting vehicle emission reductions of 50-80% by 2035 across the European Union and North American markets accelerate EV adoption rates, directly correlating with sustained carbon brush demand as the automotive sector transforms.

Renewable Energy Infrastructure Expansion and Wind Power Generation Growth

Renewable energy adoption is demonstrating exceptional growth momentum, with global wind energy capacity reaching approximately 1,200 GW by 2024 and projected to expand to 2,000 GW by 2032, according to international renewable energy assessments. Wind turbine generators depend critically upon high-performance carbon brushes for current transmission through slip rings, directly converting mechanical rotation into electrical output. Onshore and offshore wind installations require specialized carbon brush grades designed for extreme environmental conditions, including corrosion-resistant formulations for coastal installations and thermally stable materials for high-speed generators.

The convergence of declining renewable energy costs, supportive government policies, including renewable energy subsidies and tax incentives, and corporate sustainability commitments is driving accelerating wind capacity deployment globally. This infrastructure expansion creates consistent replacement demand for carbon brushes, as turbine generators operate continuously and require periodic brush maintenance and component replacement, ensuring sustained market demand through 2032.

Barrier Analysis - Competition from Brushless Motor Technology and Technological Substitution

Emerging brushless direct current (BLDC) motor technology offers competitive advantages, including extended operational lifespan, reduced maintenance requirements, improved efficiency, and minimal electromagnetic interference compared to traditional brushed motor designs. Brushless technology adoption accelerates across consumer electronics, power tools, and industrial applications, where these advantages justify premium pricing.

Industrial automation trends favor the integration of brushless motors, reducing carbon brush demand in certain high-speed, precision applications. Technological improvements in brushless motor controllers and performance characteristics are narrowing the competitive advantages previously favoring traditional carbon brush applications, potentially constraining carbon brush market growth in emerging technology segments.

Raw Material Price Volatility and Supply Chain Disruptions

Carbon brush manufacturing depends critically upon specialty graphite materials and metal additives, including copper and silver, which experience significant commodity price volatility. Graphite prices fluctuated by 35-45% during 2022-2024, directly impacting production costs and manufacturer margins.

Geopolitical tensions affecting rare-earth material supplies, international trade disputes, and tariff implementations create supply chain uncertainty, affecting component sourcing timelines and manufacturing economics. Transportation disruptions and logistics cost inflation experienced during recent global supply chain challenges continue to affect raw material availability and procurement costs, limiting manufacturers' profit margins and potentially constraining market expansion in price-sensitive regions.

Opportunity Analysis - Advanced Material Innovation and High-Performance Carbon Brush Development

Continuous advances in materials science create substantial opportunities for manufacturers developing superior carbon brush formulations that address demanding industrial requirements. Silver-graphite and electro-graphite brushes demonstrate superior electrical conductivity, extended service life, and minimal wear compared to conventional materials, commanding a premium price of 30-50% above standard offerings. Manufacturers, including Mersen, Schunk Group, and Morgan Advanced Materials, invest substantially in research and development programs focused on self-lubricating formulations, thermally stable compounds for extreme-temperature environments, and oxidation-resistant materials that extend operational life under harsh conditions.

Integration of advanced binders, specialized impregnations with copper or antimony compounds, and composite materials incorporating nanostructured elements creates differentiated product offerings justifying premium positioning in industrial and aerospace applications. These technological advancements enable market penetration into specialized segments, including precision instruments, large crane systems, ship propulsion drives, and aircraft auxiliary power systems.

Industrial Automation Expansion and Emerging Market Industrialization

Accelerating industrial automation initiatives across developed and emerging markets creates sustained carbon brush demand through factory modernization projects and equipment replacement cycles. Asia Pacific regions, including China, India, and Southeast Asian countries, pursue aggressive industrialization programs, with manufacturing capacity expanding by 8-12% annually in certain sectors. Industrial machinery modernization targeting productivity improvement and energy efficiency optimization necessitates higher-performance motor and generator systems requiring advanced carbon brush specifications.

Government infrastructure investment programs totaling trillions of dollars across emerging markets support railway electrification, metro system expansion, and power distribution infrastructure development, incorporating substantial motor and generator requirements. These industrial expansion initiatives create multi-year procurement opportunities for carbon brush manufacturers, establishing regional distribution partnerships and customized product offerings addressing localized industrial requirements.

Category-wise Analysis

Product Type Insights

Electro Graphite carbon brushes represent the dominant product type, commanding approximately 38% market share, driven by superior electrical conductivity, exceptional thermal stability, and a longer operational lifespan compared to alternative materials. Electrographite formulations result from carbonization processes at temperatures exceeding 2,500-3,000 degrees Celsius, creating dense, crystalline structures that deliver optimal electrical performance across demanding industrial applications. These brushes demonstrate excellent commutation characteristics, minimal sparking during operation, and superior wear resistance under high-load conditions characteristic of industrial motor and generator applications.

The material's self-lubricating properties minimize maintenance requirements and reduce friction-related heat generation, extending the brush lifespan to typically 2-5 years, depending on operational intensity. Industries prioritizing reliability and total cost of ownership optimization, including power generation, heavy equipment manufacturing, and railway systems, typically specify electro graphite formulations, which justify their dominant market position.

Application Insights

Motor applications dominate the carbon brush market, capturing approximately 42% of the market, reflecting widespread motor deployment across automotive, industrial, commercial, and consumer product categories. Electric motors ranging from fractional-horsepower units in household appliances to multi-megawatt industrial drive systems utilize carbon brushes for reliable electrical energy transmission. Automotive applications, including power window motors, seat adjustment systems, starter motors, and heater blower fans, account for significant carbon brush demand.

Industrial motor applications encompassing crane drives, conveyor systems, pump motors, and machine tool drive systems create sustained demand across manufacturing, construction, mining, and infrastructure sectors. The proliferation of motor applications, combined with consistent replacement cycles, ensures continued market growth as aging equipment undergoes modernization. Emerging motor applications in automated manufacturing systems, robotic equipment, and electric hand tools create incremental demand growth opportunities supporting market expansion through 2032.

Regional Insights

North America Carbon Brush Market Trends

North America maintains a significant market position through a robust automotive industry presence, advanced manufacturing capabilities, and established industrial infrastructure supporting sustained carbon brush demand. The U.S. carbon brush consumption reached approximately 6,100 tons in 2024, with domestic production accounting for 94% of national demand, reflecting substantial domestic manufacturing capacity and supply chain integration. The region's EV transition accelerates, driven by federal tax incentives and state-level regulations mandating zero-emission vehicle adoption targets, creating sustained demand for motor and generator components, including carbon brushes.

Canada's renewable energy initiatives targeting 80% clean electricity by 2030 are driving the expansion of wind turbine installations, requiring specialized, high-performance carbon brushes for generator systems. Mexico's automotive manufacturing growth, which supports North American vehicle production, creates demand for carbon brushes throughout regional supply chains. Aerospace and defense applications, including aircraft auxiliary power systems and military equipment, drive demand for specialized, aerospace-grade carbon brushes that meet stringent performance specifications. Leading manufacturers maintain extensive research facilities across North America, supporting product innovation and customized solutions addressing regional market requirements.

Europe Carbon Brush Market Trends

Europe is a mature, sophisticated market with established regulatory frameworks that promote automotive electrification and renewable energy adoption. Germany leads European market activity as a global automotive manufacturing center, with major manufacturers including Volkswagen, BMW, and Daimler accelerating EV production. European Union regulations targeting 100% emission-free new vehicles by 2035 drive aggressive automotive sector transformation, requiring substantial carbon brush supplies for EV motor systems. The region's renewable energy commitment, targeting 42.5% renewable electricity by 2030, supports continued wind turbine deployment and demand for carbon brushes for generator systems.

France and Spain demonstrate particular strength in wind energy development, while the U.K.’s industrial modernization initiatives support demand for motor and generator replacements. German manufacturing excellence and precision engineering capabilities support premium product market positioning for advanced carbon brush solutions. European manufacturers, including Schunk Group and Mersen, maintain leading market positions through innovative product development and established customer relationships across automotive, industrial, and renewable energy sectors.

Asia Pacific Carbon Brush Market Trends

Asia Pacific dominates the market, commanding approximately 49% market share, driven by rapid industrialization, automotive manufacturing expansion, and emerging market infrastructure development. China is the region's largest producer and consumer, accounting for approximately 35-40% of global carbon brush production, and benefits from extensive automotive manufacturing capacity and the deployment of industrial automation. The nation's leadership in the EV market, with approximately 60% of global EV sales, creates massive demand for carbon brushes across motor manufacturing and component supply chains. India's accelerating industrial growth, 7-8% annual GDP expansion, and infrastructure modernization initiatives, including railway electrification and expansion of power distribution, drive sustained demand for carbon brushes across industrial sectors.

Japan's advanced automotive and industrial equipment manufacturing base, coupled with leadership in robotics and precision manufacturing, sustains premium carbon brush demand for specialized applications. Southeast Asian countries, including Thailand, Indonesia, and Vietnam, demonstrate emerging market potential through manufacturing expansion and infrastructure development. Regional manufacturers are increasingly establishing localized production capacity, reducing import dependency while capturing growing regional market share through competitive pricing and rapid delivery capabilities that support continued market expansion.

Competitive Landscape

The global carbon brush market exhibits moderate consolidation with leading manufacturers Mersen, Schunk Group, and Morgan Advanced Materials collectively controlling approximately 46% market share, while secondary players, including Helwig Carbon Products and Toyo Tanso Co. Ltd., capture 38% combined share. Tier-one players dominate through comprehensive product portfolios, advanced research capabilities, and established global distribution networks.

Strategic expansion strategies emphasize emerging market penetration, technological innovation in high-performance materials, and customer service excellence. Company differentiation focuses on material science expertise, custom engineering solutions, and sustainability commitment, aligning with evolving environmental regulations and customer preferences for eco-friendly manufacturing processes.

Key Industry Developments

- In July 2024, Mersen launched a high-density carbon brush series featuring extended lifespan and reduced wear for industrial motor applications, targeting the heavy manufacturing and material handling equipment sectors.

- In September 2024, Schunk Group expands its renewable energy carbon brush portfolio with specialized formulations for wind turbine generator systems optimized for extreme offshore environmental conditions.

- In April 2025, Morgan Advanced Materials invested in expanding its production facilities across Europe, increasing manufacturing capacity and supporting regional automotive and industrial market growth initiatives.

Companies Covered in Carbon Brush Market

- Mersen SA

- Schunk Group

- Helwig Carbon Products Inc.

- Morgan Advanced Materials

- Fuji Carbon Mfg Co. Ltd.

- TRIS

- E-Carbon

- Aupac Co. Ltd.

- Assam Carbon Products Limited

- Naeem Carbon and Industrial Products LLP

- Toyo Tanso Co. Ltd.

- Carbone Lorraine

Frequently Asked Questions

The global carbon brush market was valued at US$3.6 Billion in 2025 and is projected to reach US$4.8 Billion by 2032, representing a CAGR of 4.1% during the forecast period.

Key demand drivers include stricter vehicle electrification regulations, 18% annual growth in EV production, rising renewable energy adoption with wind capacity nearing 1,200 GW, expanding industrial automation, and tightening global emissions standards.

Electro graphite carbon brushes command the dominant segment at approximately 38% market share, delivering superior electrical conductivity, exceptional thermal stability, and extended operational lifespan.

Asia Pacific dominates with 49% market share, driven by extensive manufacturing capacity, rapid industrialization, accelerating automotive electrification across China and India, and infrastructure development investments supporting sustained carbon brush demand.

Renewable energy sector expansion, particularly wind turbine generator applications, represents the highest-growth opportunity, with specialized high-performance carbon brushes for wind systems projected to represent 18-22% of market demand by 2032, driven by global wind capacity expansion toward 2,000 GW.

Market leaders include Mersen SA, Schunk Group, and Morgan Advanced Materials, together holding about 46% market share, driven by strong revenues, advanced materials expertise, and long-standing industry experience.