- Medical Devices

- Digital Dentistry Market

Digital Dentistry Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Digital Dentistry Market by Product (CAD/CAM Systems, Cone-Beam Computed Tomography (CBCT) Imaging Systems, Intraoral Sensors, Software, Dental 3D Printers, Intraoral X-ray Systems, Intraoral Cameras, and Intraoral Plate Scanners), End-user, and Regional Analysis from 2026 - 2033

Digital Dentistry Market Share and Trends Analysis

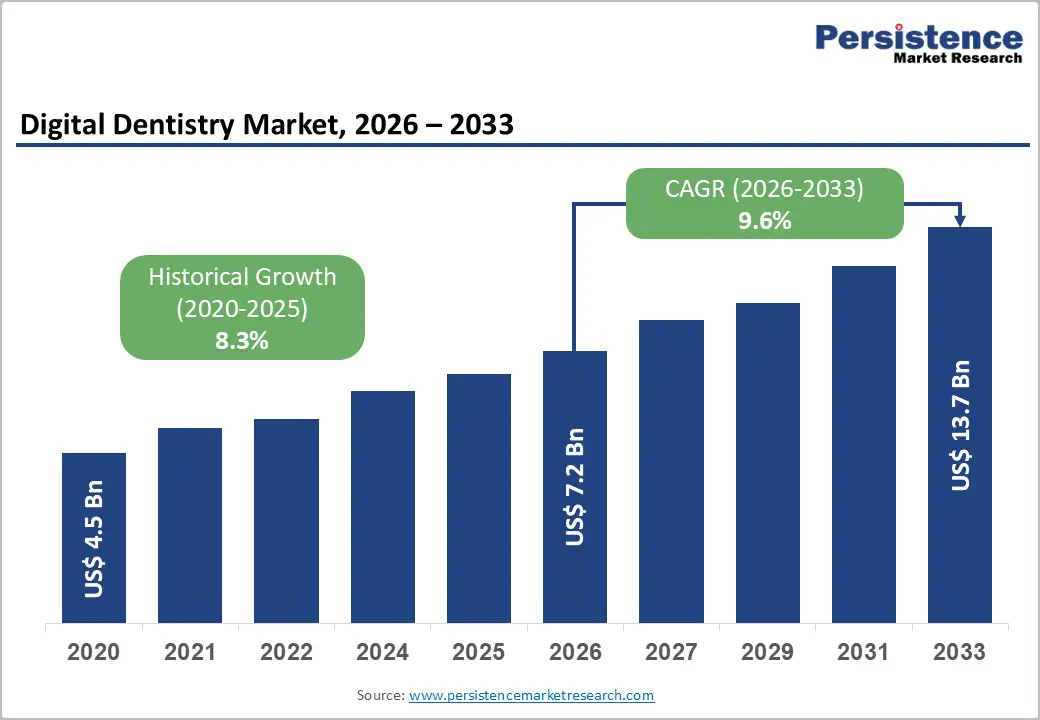

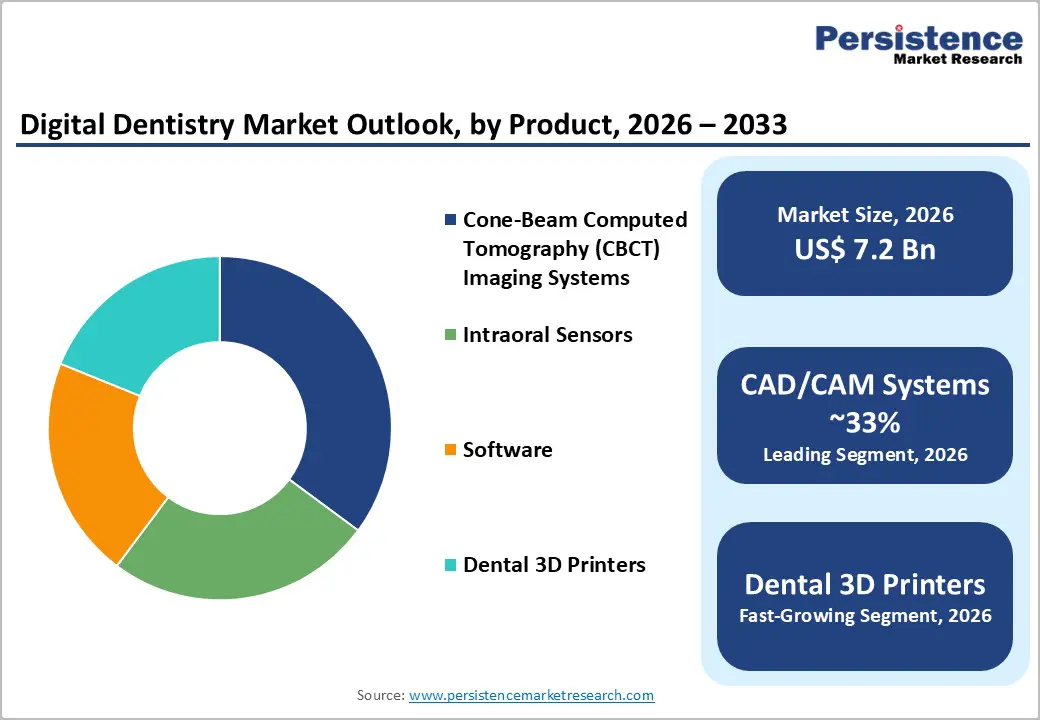

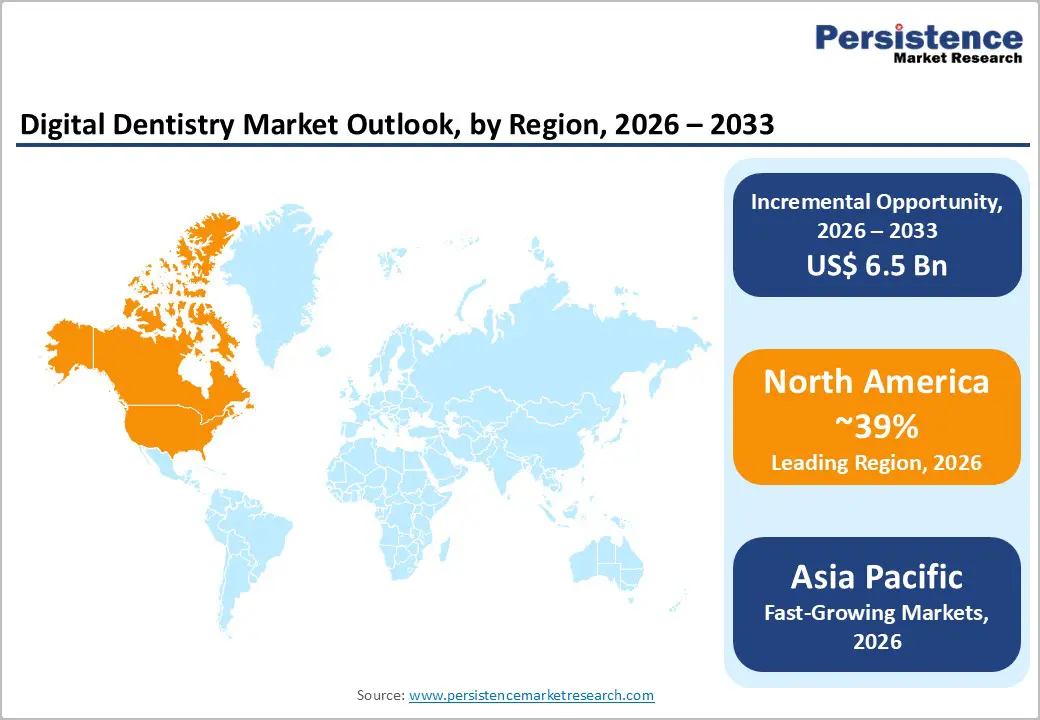

The global digital dentistry market size is estimated to grow from US$ 7.2 billion in 2026 to US$ 13.7 billion by 2033. The market is projected to grow at a CAGR of 9.6% from 2026 to 2033.

The digital dentistry market is transforming oral healthcare by integrating advanced data-driven technologies across diagnosis, treatment planning, and restorative procedures. Beyond CAD/CAM, digital dentistry now includes intraoral scanning, digital imaging, software-based decision support, and connected treatment workflows that improve accuracy, efficiency, and patient outcomes.

The shift from conventional impressions and manual fabrication toward digital impressions, automated design, and precision manufacturing is accelerating adoption across dental clinics and laboratories. Growing use of big data, Internet and Communication Technologies (ICT), and Internet of Things (IoT) solutions is further enabling real-time data capture, analysis, and long-term patient care, positioning digital dentistry as a core component of modern dental practice.

Key Industry Highlights:

- Leading Region: North America leads the digital dentistry market, driven by high dental clinic density, technology adoption, and strong patient demand.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, supported by expanding clinics, rising dental awareness, and cost-effective digital dentistry solutions.

- Dominant Segment: CAD/CAM systems dominate the market, enabling precise restorative workflows, same-day prosthetics, and seamless integration with intraoral scanners and 3D printers.

- Fastest-Growing Segment: Dental 3D printers are the fastest-growing product segment, driven by chairside manufacturing, clear aligner adoption, and localized prosthetic production.

| Key Insights | Details |

|---|---|

|

Digital Dentistry Market Size (2026E) |

US$ 7.2 Bn |

|

Market Value Forecast (2033F) |

US$ 13.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.3% |

Market Dynamics

Driver - Acceleration of Chairside CAD/CAM and Intraoral Scanning

The rapid adoption of intraoral scanners and chairside CAD/CAM systems is a major driver of growth in the digital dentistry market. By 2024, a significant share of dental clinics worldwide had transitioned from conventional impression materials to digital scanning, driven by the need to improve clinical efficiency and patient comfort. Digital impressions reduce chair time, eliminate remakes caused by impression errors, and enable more predictable restorative outcomes. New dental practices are increasingly designed around digital-first workflows, integrating scanners at the point of care rather than adopting them gradually, highlighting a structural shift in clinical operations.

Chairside CAD/CAM systems further strengthen this trend by enabling same-day restorations such as crowns, inlays, onlays, and aligners. The seamless integration of scanners with milling units and dental 3D printers allows dentists to shorten treatment cycles, increase patient throughput, and enhance overall practice profitability. In mature markets such as North America, widespread daily use of intraoral scanners underscores their role as core clinical infrastructure rather than optional technology. Continuous upgrades in software accuracy, scanning speed, and material compatibility are sustaining repeat investments, driving long-term demand for both hardware and associated digital services.

Restraints - Ethical Issues Concerning Patient Data

Ethical and data privacy concerns represent a key restraint to the adoption of digital dentistry technologies. The increasing use of mHealth platforms and teledentistry relies heavily on the electronic collection, storage, and transmission of sensitive patient data, raising concerns around confidentiality, consent, and cybersecurity. Networked systems can be vulnerable to unauthorized access, particularly when data is transferred over inadequately secured digital channels, posing risks to both patients and providers.

Consent-related challenges further complicate adoption. Patients may not always be fully informed about how their clinical images, scans, or treatment data are stored, shared, or reused for research, training, or algorithm development. In educational and multi-site clinical environments, data linkage across systems can make it difficult to clearly define ownership and usage boundaries. Studies have highlighted that insufficient transparency around data utilization can limit trust in digital platforms. These ethical considerations impose regulatory and operational constraints, slowing adoption and requiring additional investments in data governance frameworks, compliance systems, and staff training.

Opportunity - AI-Enhanced Workflows and Cloud-Based Collaboration Platforms

The expansion of dental infrastructure in the Asia Pacific, Latin America, and parts of the Middle East and Africa presents strong opportunities for digital dentistry solutions tailored to cost-sensitive and high-growth markets. Rising investments in dental clinics, laboratories, and education centers are accelerating demand for digital tools that improve productivity and standardize outcomes. Dental 3D printing, in particular, is gaining traction as local laboratories seek faster turnaround times and reduced dependence on imported restorations.

Artificial intelligence and cloud-based collaboration platforms further enhance this opportunity by enabling remote treatment planning, automated design, and seamless data exchange between clinics and laboratories. Cloud-enabled systems allow smaller practices to access advanced capabilities without heavy upfront investments, while AI-assisted workflows improve accuracy and consistency in diagnostics and prosthetic design. Vendors offering flexible business models, such as equipment leasing, subscription-based software, training support, and regionally sourced materials, are well-positioned to capture emerging market demand. These innovations support scalable adoption and are expected to play a central role in expanding global digital dentistry penetration.

Category-wise Analysis

By Product Type

CAD/CAM systems dominate the global digital dentistry market, accounting for approximately 37% of revenue in 2025. These systems are central to restorative workflows, connecting intraoral scanners with design software and milling or 3D printing units to produce precise crowns, bridges, inlays, and implant restorations. High patient demand for same-day restorations and widespread adoption by dental service organizations have driven the North American CAD/CAM dental devices market to exceed US$ 2 billion in 2024. Innovations such as AI-assisted design, multi-material milling, and direct 3D printer integration continue to enhance the functionality and efficiency of these systems. The shift from conventional lab-based fabrication to chairside digital workflows is accelerating, enabling faster turnaround, improved accuracy, and better patient outcomes. As dental practices increasingly embrace digital workflows, CAD/CAM systems are expected to maintain their leading position in product adoption, remaining the backbone of restorative and implant dentistry across clinics, laboratories, and large healthcare facilities globally.

By End-user

Hospitals represent the largest end-user segment in the digital dentistry market, capturing an estimated 36% share in 2025. Large hospitals and university dental centers manage complex restorative, oncologic, and maxillofacial cases that benefit significantly from CBCT imaging, digital treatment planning, and 3D-printed surgical guides and prosthetics. Tertiary care centers are more likely to invest in high-end CBCT scanners, integrated CAD/CAM systems, and in-house 3D printing laboratories, supported by multidisciplinary teams and academic research mandates. Many hospitals in North America and Europe incorporate digital dentistry into broader digital health strategies, linking imaging, electronic health records, and surgical planning platforms to optimize patient care. While specialty clinics and dental laboratories are rapidly expanding their digital equipment capabilities, the complexity of cases and the research-oriented environment in hospitals ensure they remain the dominant end-user segment. The integration of advanced technologies within hospital workflows continues to drive sustained adoption and reinforces hospitals’ leading position in the global digital dentistry market.

Regional Insights

North America Digital Dentistry Market Trends

North America remains the largest market for digital dentistry, supported by a high concentration of dental clinics, strong patient spending capacity, and early acceptance of advanced digital tools. In the U.S., thousands of dental practices now rely on intraoral scanners as part of their daily clinical workflows, while chairside CAD/CAM systems are common in multi-chair clinics and large dental service organizations. Regular approvals from regulatory authorities such as the U.S. FDA encourage frequent upgrades of scanners, 3D printers, and restorative materials, allowing dentists to expand the range of procedures performed digitally.

Universities, research hospitals, and innovation centers across the U.S. and Canada play a major role in advancing areas such as AI-supported treatment planning, digital orthodontics, and implant dentistry. These institutions often collaborate with established industry players, accelerating real-world adoption. Digital dentistry is also increasingly integrated into dental education, ensuring new practitioners are trained with modern workflows from the outset. In parallel, teledentistry and cloud-based planning platforms are gaining acceptance, particularly for remote consultations, strengthening North America’s position as a global leader in digital dental technologies.

Asia Pacific Digital Dentistry Market Trends

Asia Pacific is projected to be the fastest-growing digital dentistry market, driven by rising incomes, greater healthcare awareness, and rapid expansion of dental clinics across China, Japan, India, and Southeast Asia. Demand for cosmetic orthodontics, implants, and restorative procedures is expanding quickly, especially in urban areas where patients seek advanced and aesthetic treatment options. New dental hospitals and training institutes are being established with digital equipment such as intraoral scanners, CBCT systems, and dental 3D printers included as standard infrastructure from the beginning.

The region is also emerging as an important production base for digital dental technologies. Manufacturers in China, South Korea, and Japan are developing affordable CAD/CAM systems, 3D printers, materials, and software designed for local market needs. Several initiatives launched in recent years focus on enabling same-day restorations and faster prosthetic delivery through localized digital laboratories. Global companies are also expanding their digital lab presence in countries like India to reduce turnaround times and support regional demand. Together with growing use of AI-based design tools and cloud-enabled collaboration, these trends position the Asia Pacific as a key growth driver for digital dentistry worldwide.

Competitive Landscape

The digital dentistry market is moderately fragmented, featuring a blend of global imaging and CAD/CAM leaders, specialized 3D printing companies, and regional software and materials providers. Major players such as Dentsply Sirona, Institut Straumann AG, 3D Systems, Inc., Planmeca Oy, Stratasys Ltd., Roland DG Corporation, and Zimmer Biomet Holdings, Inc. offer integrated portfolios spanning scanners, CAD/CAM units, 3D printers, and software, often bundled with training and service contracts. Niche manufacturers like Asiga, SprintRay, Inc., and Formlabs, Inc. focus on dental-specific 3D printers and resins, differentiating through print speed, material diversity, and cloud management tools. Emerging business models include subscription-based design platforms, equipment leasing, and centralized printing hubs serving multiple clinics, while vendors increasingly incorporate AI into design and diagnostic software to strengthen value propositions and customer stickiness.

Key Industry Developments:

- In December 2025, Korea-based Leaders Dental Laboratory unveiled a new vision to become a central hub for the digital dentistry ecosystem, supported by major investments in AI-enabled CAD, 3D printing, and IoT-driven production automation.

- In December 2025, PreVu Software announced that its patient-simulation platform, PreVu, was named among Dentistry Today’s Top 50 Technology Products of 2025, highlighting its impact on digital dentistry, patient communication, aesthetic planning, and practice revenue.

- In September 2025, Align Technology shared highlights from the 2025 Invisalign GP Summit, showcasing clinical education, peer networking, and digital solutions, including Invisalign aligners, iTero scanners, and exocad software.

Companies Covered in Digital Dentistry Market

- 3D Systems, Inc.

- Asiga

- BEGO GmbH & Co. KG

- BIOLASE, Inc.

- Carestream Dental LLC.

- Dentsply Sirona

- Formlabs, Inc.

- imes-icore GmbH

- Institut Straumann AG

- Planmeca Oy

- Roland DG Corporation

- SprintRay, Inc.

- Stratasys Ltd.

- Zimmer Biomet Holdings, Inc.

- Others

Frequently Asked Questions

The global digital dentistry market is projected to be valued at US$ 7.2 Bn in 2026.

Rise in chairside CAD/CAM adoption, intraoral scanning penetration, demand for same-day restorations, workflow efficiency, and improved patient experience.

The global market is poised to witness a CAGR of 9.6% between 2026 and 2033.

AI-driven diagnostics, cloud-based collaboration, dental 3D printing expansion, emerging market infrastructure growth, and service-based digital solutions.

North America is the leading region in the global healthcare clinical analytics market.