- Food Ingredients & Additives

- Butter Fat Fraction Market

Butter Fat Fraction Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Butter Fat Fraction Market by Product Type (Anhydrous Milk Fat (AMF), Ghee and Clarified Butter, Fractionated Butter Oil, Others), End-user (Bakery & Confectionery, Dairy & Ice Cream, Cosmetic & Personal Care, Pharmaceuticals, Others), and Regional Analysis, 2026 - 2033

Butter Fat Fraction Market Share and Trends Analysis

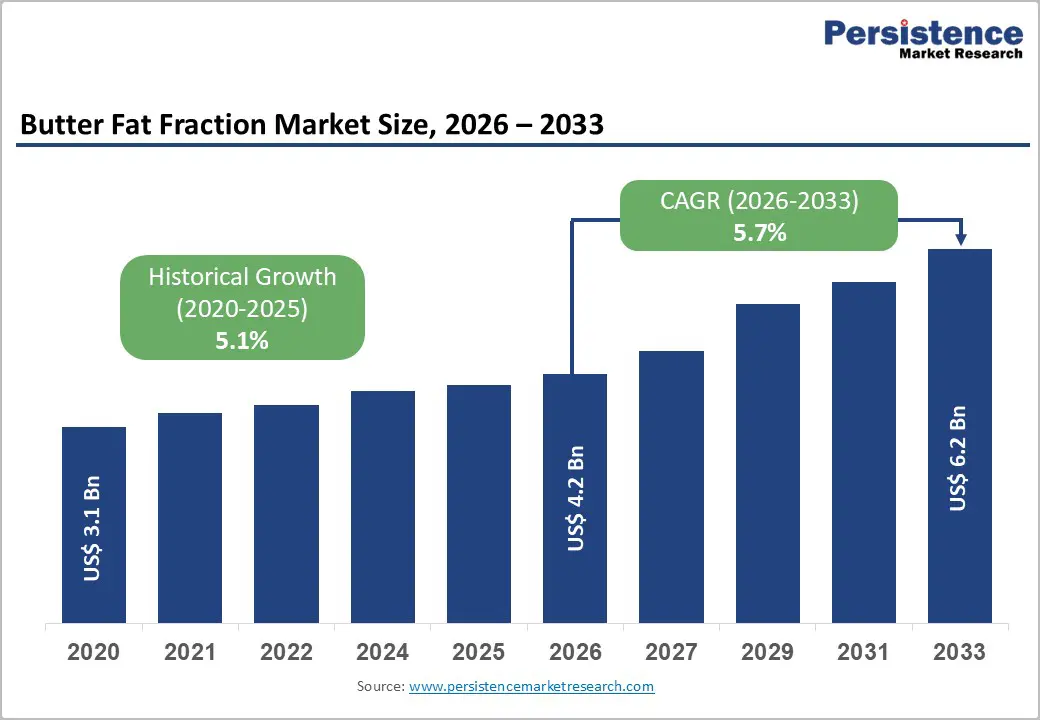

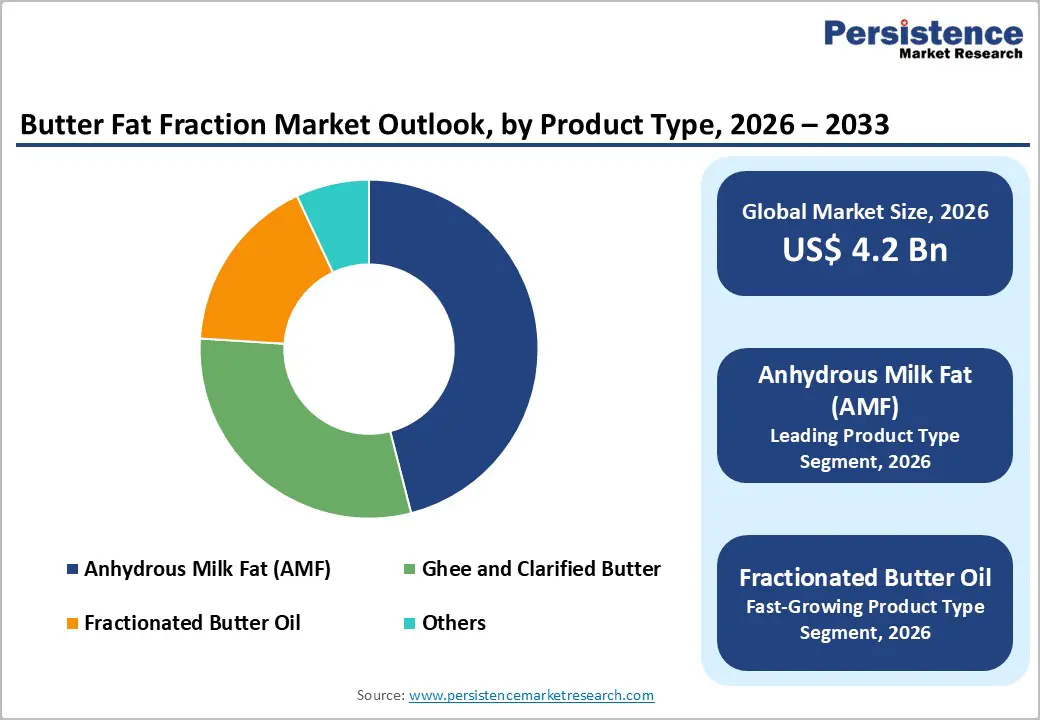

The global butter fat fraction market size is expected to be valued at US$ 4.2 billion in 2026 and projected to reach US$ 6.2 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

The robust market growth is primarily driven by the expanding industrial use of dairy-based fats that offer superior functional properties, such as precise melting points and enhanced flavor stability. As the global food processing industry seeks clean-label alternatives to hydrogenated vegetable oils, butter fat fractions have emerged as a premium solution for maintaining product quality across varying temperatures. This trend is particularly evident in the Bakery & Confectionery sector, where specialized fractions facilitate the production of laminated pastries and high-stability chocolates. Furthermore, the surging consumer demand for authentic and minimally processed dairy ingredients in emerging economies, notably within the Asia Pacific, continues to provide a significant tailwind for global market valuation through the forecast period.

Key Industry Highlights:

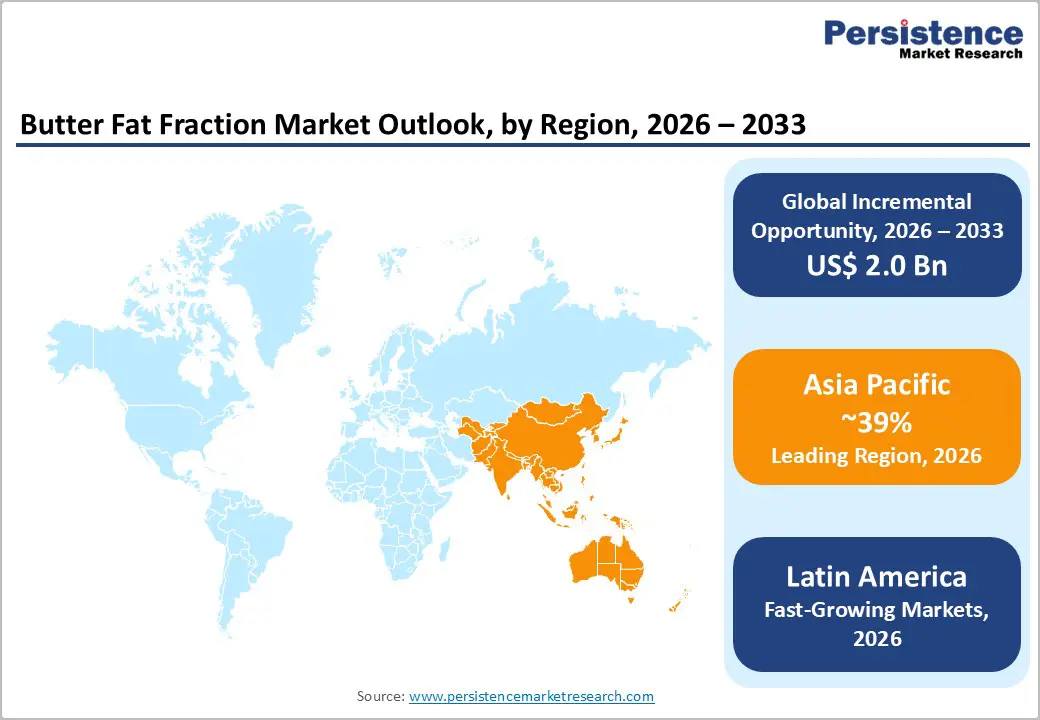

- Leading Region: Asia Pacific, accounting for around 39% market share, supported by expanding bakery and confectionery production, recombined dairy demand, and large-scale processing investments in China, India, and ASEAN countries.

- Dominant Product Type Segment: Anhydrous Milk Fat (AMF), holding approximately 46% share, favored for its long shelf life, export suitability, and versatility across chocolates, recombined dairy, and premium spreads.

- Fastest-Growing Product Type Segment: Fractionated Butter Oil, propelled by demand for tailored melting profiles in pharmaceuticals, cosmetics, and climate-resilient confectionery applications.

- Growth Indicator: Rising demand for functional dairy fats that deliver controlled crystallization, enhanced mouthfeel, and thermal stability in premium food and industrial formulations.

- Opportunity: Precision fractionation technologies and low-carbon processing models enabling customized, high-purity fractions aligned with ESG-driven procurement by food, cosmetic, and pharma brands.

- Key Developments: In December 2025, Open Country Dairy expanded its manufacturing footprint to prioritize high-value butter and milk fat products. In October 2025, Fonterra committed USD 75 million to expand butter and butter oil production at its Clandeboye site.

| Key Insights | Details |

|---|---|

| Global Butter Fat Fraction Market Size (2026E) | US$ 4.2 Bn |

| Market Value Forecast (2033F) | US$ 6.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Dynamics

Driver – Rising Demand for Functional Dairy Ingredients in Premium Food Processing

The accelerating shift toward specialized dairy ingredients that offer customized physical and chemical properties encourages the need for butter fat fractions. Food manufacturers are increasingly moving away from standard butter toward fractionated butter oil to achieve specific textural outcomes in high-end food products. According to data from the International Dairy Federation (IDF), the requirement for high-stability fats that can withstand varied processing temperatures is critical for large-scale production. Fractions such as high-melting stearins are vital for creating crispiness in biscuits and structural integrity in chocolates, while low-melting oleins are preferred for cold-spreadable butter blends. This demand for "tailored functionality" allows processors to optimize their formulations for better mouthfeel and shelf-stability, thereby driving the consumption of premium fractions globally.

Restraints – Increasing Competition from Plant-Based and Vegan Fat Alternatives

The rapid ascent of the plant-based and vegan food industry poses a significant challenge to the traditional dairy fat market. As a growing demographic of consumers adopts flexitarian or vegan diets for environmental and ethical reasons, the demand for non-dairy fat substitutes has surged. Innovations in vegetable fat fractionation utilizing shea, palm, and cocoa butter alternatives now offer functional performance that closely mimics that of dairy fats. According to the Good Food Institute (GFI), the market for plant-based alternatives is expanding positively, siphoning off potential growth from the dairy-based segment. This competitive pressure is particularly strong in the dairy & ice-cream and bakery sectors, where cost-effective vegetable fat blends are often used to replace expensive butter fat fractions in mass-market products, thereby limiting the volume expansion of the dairy fat sector.

Opportunity – Technological Advancements in Precision Fractionation and Sustainable Processing

The integration of advanced processing technologies presents a transformative opportunity for market participants to differentiate their offerings. Innovations such as supercritical fluid extraction and membrane-based fractionation are enabling the production of fractions with unprecedented purity and specific fatty acid profiles. These technologies allow for the creation of unique textures and melting behaviors that were previously impossible to achieve through traditional thermal cooling methods. Furthermore, as the industry moves toward "Carbon-Zero" goals, as demonstrated by Fonterra's recent investments in renewable energy for dairy processing, there is a clear opportunity to market sustainably produced fractions. Brands that can verify the ethical sourcing and low-carbon footprint of their butter fat fractions will find a receptive audience among premium Cosmetic & Personal Care and high-end food brands that prioritize ESG metrics in their procurement strategies.

Category-wise Analysis

By Product Type Insights

The anhydrous milk fat (AMF) segment is the leading product type, commanding a dominant 46% share in 2025. This leadership is primarily due to its versatility and exceptional shelf-stability, which makes it an ideal ingredient for international trade and industrial-scale food manufacturing. AMF is virtually free of water and protein, containing at least 99.8% milk fat, allowing it to be stored without refrigeration for extended periods. Its neutral yet rich profile makes it indispensable in the production of high-quality chocolates, recombined dairy products, and premium spreads. However, Fractionated Butter Oil is identified as the fastest-growing segment. The rising demand for specialized melting profiles for seasonal food products and the expansion of the pharmaceutical industry’s need for pure lipid carriers are driving this rapid growth. The ability to offer "hard" and "soft" fractions tailored to specific industrial requirements provides this segment with a significant competitive edge over standard AMF.

By End-user Insights

The bakery & confectionery segment accounts for the highest volume consumption in 2025. The inherent flavor-carrying properties and unique crystallization behavior of milk fat fractions are irreplaceable in the production of gourmet chocolates and puffed pastries. For instance, the use of high-melting fractions allows for the production of "blooming-resistant" chocolates, which are essential in tropical climates. While bakery leads, the pharmaceutical segment is witnessing a surge in interest. Furthermore, the Cosmetic & Personal Care sector is showing increasing adoption of fractions due to their emollient properties and biocompatibility with human skin. The trend toward using natural, food-grade ingredients in luxury skincare is expected to bolster demand for low-melting butter oleins as bases for high-end lotions and creams through 2033.

Region-wise Insights

North America Butter Fat Fraction Market Trends and Insights

North America is characterized by high maturity and a strong focus on premiumization. The United States leads the region, supported by a robust innovation ecosystem and a regulatory framework that emphasizes food safety and labeling transparency. Consumers in this region are increasingly opting for "grass-fed" and "organic" butter products, leading to a niche but high-value demand for certified butter fat fractions.

Leading companies in the region, such as Saputo Inc. and Schreiber Foods, are investing in R&D to develop low-calorie and fortified fat options. The growth of the artisanal bakery sector and the resurgence of home baking post-pandemic have also contributed to the steady demand for specialized fractions. Furthermore, the region's pharmaceutical industry uses high-purity milk fat fractions as excipients in various formulations, further diversifying the market's reach. The integration of advanced supply chain technologies ensures that high-quality fractions are efficiently distributed from central processing hubs to diverse end-users across the continent.

Asia Pacific Butter Fat Fraction Market Trends and Insights

Asia Pacific is the leading market for butter fat fractions, holding a significant 39% market share in 2025. This dominance is fueled by the rapid expansion of the middle class in China, India, and ASEAN countries, alongside a massive shift toward Westernized diets. Yili Group and Mengniu Dairy are expanding their processing capacities to meet the local demand for premium dairy ingredients.

The region's growth is primarily driven by the booming bakery & confectionery sector and the increasing production of recombined milk products in regions with limited raw milk supply. The manufacturing advantage in Asia Pacific is bolstered by lower labor costs and significant government investments in food processing infrastructure. In China, the demand for specialized fractions for use in premium infant formula is a major market driver, as domestic brands seek to compete with international leaders. Furthermore, the rise of "fusion food" and the integration of dairy fats into traditional Asian desserts are creating new consumption occasions, ensuring that the Asia Pacific remains the engine of global market growth.

Competitive Landscape

The global butter fat fraction market is characterized by a moderate degree of consolidation, with a handful of global dairy cooperatives and multinational corporations holding significant market power. Leaders such as Fonterra, Lactalis, and FrieslandCampina leverage their vertically integrated supply chains to maintain competitive pricing and consistent quality. Key strategies employed by these leaders include aggressive expansion into emerging markets and the acquisition of niche technology providers to enhance their fractionation capabilities. Differentiation in the market is increasingly based on the ability to provide "tailored solutions" that are customized for specific industrial applications. Smaller regional players compete by offering localized service and flexible production batches, particularly in the Ghee and Clarified Butter segments in South Asia. Emerging business models are also focusing on digital platforms for B2B sales to streamline the procurement process for small-to-medium-sized food processors.

Key Developments:

- In December 2025, Open Country Dairy announced the expansion of its dairy manufacturing footprint, strategically prioritizing high-value butter and milk fat products to capture rising global demand for premium dairy ingredients and improve margin resilience.

- In October 2025, Fonterra announced a significant $75 million investment to expand its butter and butter oil production at its Clandeboye site.

- In August 2025, Arla Foods marked the 25th anniversary of the Arla–MD Foods merger, highlighting how the cross-border, farmer-owned cooperative model has enabled long-term scale, innovation, and global competitiveness in the dairy sector.

Companies Covered in Butter Fat Fraction Market

- Royal FrieslandCampina N.V.

- Arla Foods amba

- Fonterra Co-operative Group Limited

- Saputo Inc.

- Lactalis Group

- Flechard S.A.

- Schreiber Foods

- Uelzena Ingredients

- Yili Group

- Mengniu Dairy

- Others

Frequently Asked Questions

The global butter fat fraction market is expected to be valued at US$ 4.2 billion in 2026, following a steady growth trajectory driven by demand in the food processing industry.

Key growth drivers include the rising demand for functional dairy ingredients with specific melting points, the global clean-label movement, and the replacement of trans-fats in baked goods and confectionery.

Asia Pacific is the leading region, accounting for an estimated 39% market share in 2025, supported by rapid urbanization and the expansion of the bakery and confectionery sectors in China and India.

The integration of advanced processing technologies presents a transformative opportunity for market participants to differentiate their offerings.

Key companies include Fonterra Co-operative Group Limited, Royal FrieslandCampina N.V., Arla Foods amba, Lactalis Group, and Saputo Inc.