- Processed Food

- Butternut Squash Market

Butternut Squash Market Size, Share, and Growth Forecast, 2026 - 2033

Butternut Squash Market by Form (Fresh, Frozen, Puree, Others), Application (Food & Beverages, Cosmetics, Baby Food), Distribution Channel (Supermarkets, Online Retail), and Regional Analysis for 2026 - 2033

Butternut Squash Market Share and Trends Analysis

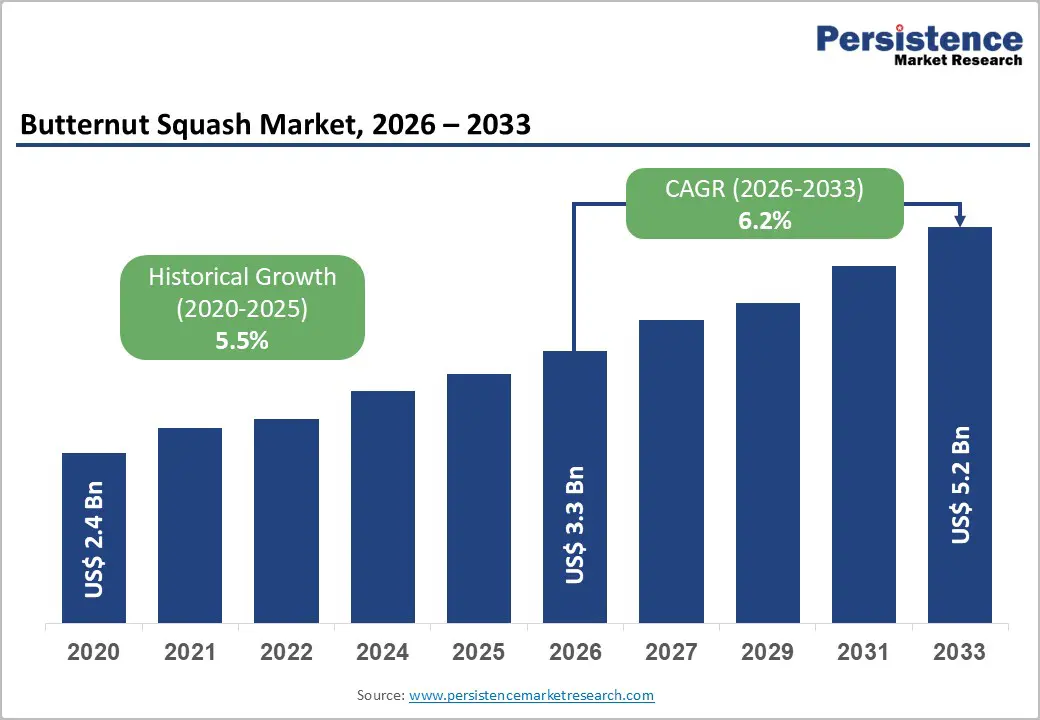

The global butternut squash market size is likely to be valued at US$ 3.3 billion in 2026, and is projected to reach US$ 5.2 billion by 2033, growing at a CAGR of 6.2% during the forecast period 2026 - 2033.

This robust expansion is primarily driven by increasing consumer awareness regarding the nutritional benefits of butternut squash, which contains high levels of vitamin A, potassium, and dietary fiber. The market has demonstrated consistent growth momentum, with accelerating demand from the food processing industry, particularly in organic and frozen food segments. Rising preference for plant-based diets and clean-label products continues to fuel market penetration across developed and emerging economies, while innovations in preservation technologies and distribution infrastructure enhance product accessibility.

Key Industry Highlights

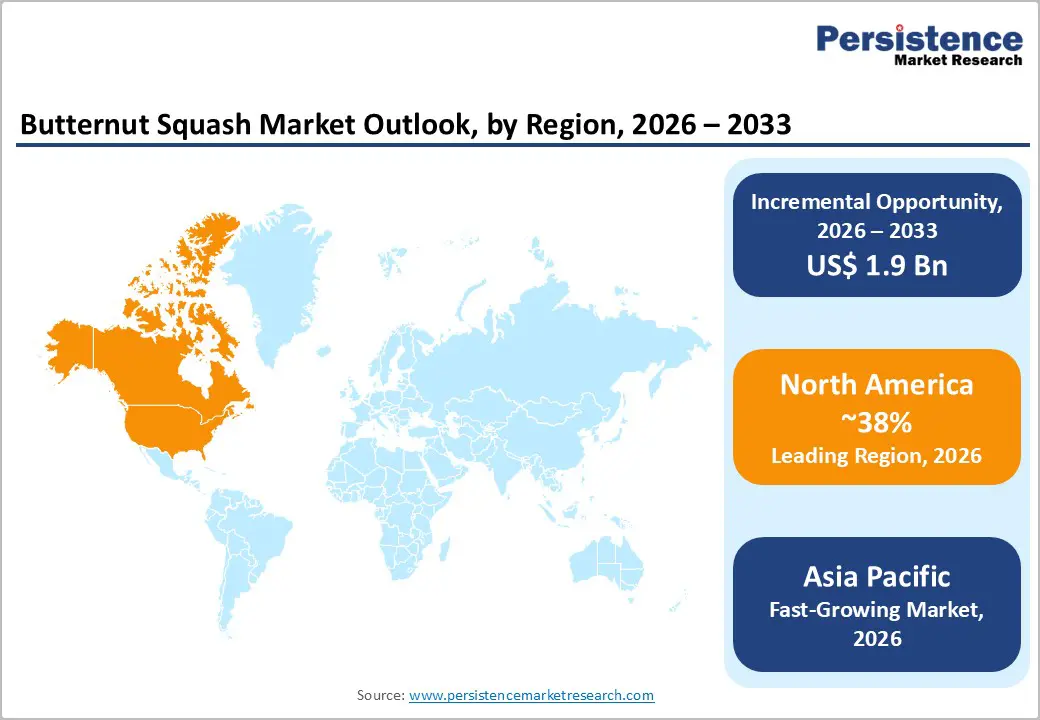

- Dominant Region: North America is expected to command about 38% market share in 2026, sustained by high per-capita vegetable intake and a mature cold chain infrastructure.

- Fastest-growing Regional Market: The Asia Pacific market is set to be the fastest-growing through 2033, due to distinct culinary traditions.

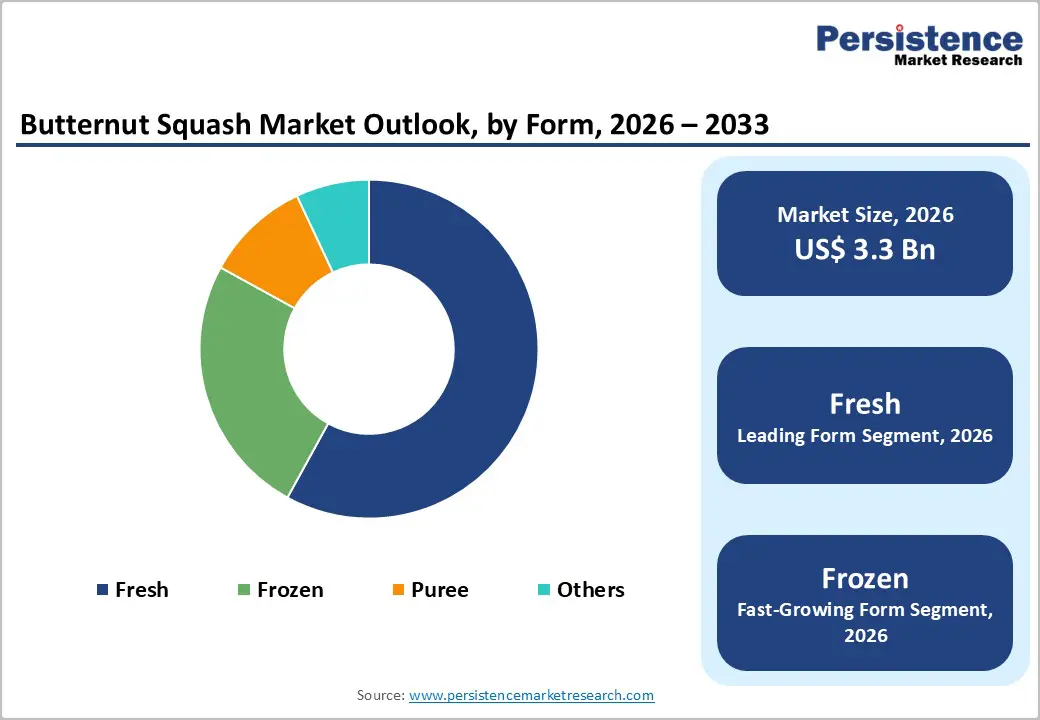

- Leading Form: Fresh form is likely to be the leading segment with an approximate 58% revenue share in 2026, owing to strong consumer preference for whole, unprocessed vegetables.

- Fastest-growing Form: Frozen form is slated to be the fastest-growing during the 2026 - 2033 forecast period, fueled by convenience advantages and extended shelf life.

- October 2025: Waitrose, the British supermarket chain, announced its expectations of doubling its butternut squash harvest due to perfect summer conditions and new hardy varieties trialed by Barfoots.

| Key Insights | Details |

|---|---|

| Butternut Squash Market Size (2026E) | US$ 3.3 Bn |

| Market Value Forecast (2033F) | US$ 5.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of Organic and Clean-Label Food Segments

The organic food movement has transformed butternut squash cultivation and consumption patterns worldwide. Growing demand for organically produced food has encouraged farmers to adopt more sustainable practices, reduce the use of synthetic inputs, and pursue organic certification to meet evolving consumer expectations. This shift has strengthened the position of butternut squash as a wholesome, naturally nutritious vegetable aligned with broader lifestyle trends focused on wellness, environmental responsibility, and food transparency. As awareness of farming methods and supply chain practices has increased, consumers have become more discerning about how their vegetables are grown, handled, and sourced.

At the retail and product level, organic butternut squash has benefited from a strong preference for cleaner ingredient profiles and naturally derived products. Shoppers increasingly seek produce and packaged foods with simple, transparent formulations and minimal processing, particularly in frozen and puree formats where butternut squash serves as a versatile base. In these segments, its role as a familiar, kitchen-style ingredient aligns closely with the clean-label movement, supporting brand differentiation and consumer trust. This trend has encouraged manufacturers and retailers to feature organic butternut squash more prominently in their assortments, reinforcing its status as a core component of modern health-oriented diets.

Seasonality and Supply Chain Vulnerabilities

Butternut squash production remains closely tied to seasonal growing cycles and climate conditions, which leads to periodic supply-demand imbalances that undermine overall market stability. Even with improvements in storage technologies, the availability of fresh butternut squash can vary noticeably throughout the year, creating fluctuations that complicate retail planning and influence consumer purchasing behavior. Producers must also navigate increasingly unpredictable weather patterns that can disrupt planting and harvesting schedules, ultimately affecting both yield levels and product quality.

Transportation and storage requirements for fresh butternut squash add further complexity to distribution networks, especially for smaller retailers that may lack access to specialized handling or temperature-controlled facilities. These challenges can limit the ability of supply chains to maintain consistent product quality during both transit and storage. In regions where cold chain logistics remain underdeveloped, market penetration is constrained and access to fresh butternut squash is often uneven, which contributes to higher levels of post-harvest waste and reduces the overall efficiency of the value chain.

Innovation in Value-Added Product Formats

The processed butternut squash products offers significant opportunities for differentiation and margin enhancement through innovative product development. Growing demand for convenience-oriented solutions has created space for pre-cut, pre-seasoned, and ready-to-cook offerings that reduce preparation time and simplify meal preparation. These formats appeal to time-constrained consumers who still want wholesome, vegetable-based options that integrate easily into everyday cooking routines. As a result, retailers and brands increasingly position value-added butternut squash products as premium yet practical choices across refrigerated, frozen, and ambient categories.

The puree and frozen forms are particularly well positioned to benefit from this shift toward value-added innovation. Purees offer versatile applications in infant nutrition, health-focused formulations, and as a reliable culinary ingredient in professional and institutional kitchens. Frozen butternut squash helps mitigate seasonality constraints while preserving taste and nutritional quality, supporting more consistent year-round consumption. In parallel, emerging applications in plant-based meat alternatives and protein-enriched foods are expanding the ingredient’s role in next-generation product development, reinforcing its relevance within evolving dietary and product innovation trends.

Category-wise Analysis

Form Insights

Fresh form is expected to be the leading segment with an approximate 58% of the butternut squash market revenue share in 2026. This dominance reflects strong consumer preference for whole, unprocessed vegetables that provide versatility in home cooking and clear, visible indicators of quality. Retail supermarkets and specialty produce stores prioritize fresh butternut squash because it offers attractive profit margins and steady consumer demand throughout most of the year, even though availability peaks during harvest periods. The segment also benefits from the growing presence of farmer markets and direct-to-consumer agricultural channels, which emphasize freshness and locally sourced attributes.

Frozen form is likely to be the fastest-growing segment during the 2026-2033 forecast period. This accelerated growth stems from convenience advantages, extended shelf life, and elimination of preparation labor for consumers with time constraints. Food service establishments increasingly source frozen butternut squash to ensure consistent supply and reduce food waste, while retail frozen food sections dedicate expanding space to premium frozen vegetable offerings. Technological advances in flash-freezing and packaging preserve nutritional content effectively, addressing previous consumer concerns about quality degradation in frozen produce.

Application Insights

Food & beverages is slated to be dominant with an estimated 72% of market revenue share in 2026. This leadership reflects the vegetable's culinary versatility across multiple food categories, including soups, side dishes, baked goods, and beverage applications such as smoothies and health-focused drinks. Restaurant menus increasingly feature butternut squash in both traditional and modern preparations, aligning with consumer demand for seasonal, nutritious ingredients that offer distinctive yet approachable flavor profiles. The segment spans retail purchases for home cooking as well as commercial procurement by foodservice operators and food manufacturers, reinforcing butternut squash as a staple ingredient in both household kitchens and professional culinary environments.

Baby food is expected to be the fastest-growing segment during the 2026-2033 forecast period. This expansion reflects parental preferences for natural, nutrient-dense first foods that support infant development without artificial additives or heightened allergen concerns. Butternut squash’s naturally sweet flavor profile enhances palatability for infants while providing essential vitamins and minerals that are important for early childhood growth. Major baby food manufacturers have expanded their butternut squash-based product lines, often combining it with other vegetables and proteins to create nutritionally balanced meals that appeal to health-conscious parents seeking more premium options.

Distribution Channel Insights

Supermarkets are set to lead with an approximate market revenue share of 64% in 2026. This channel leadership stems from extensive geographic coverage, established consumer shopping habits, and comprehensive produce departments that provide both variety and quality assurance. Large-format retailers leverage economies of scale in procurement and distribution to offer competitive pricing while maintaining freshness through efficient inventory turnover. Dedicated produce sections with controlled conditions help preserve product quality, and prominent displays during peak seasons stimulate impulse purchases and provide shoppers with recipe inspiration.

Online retail is anticipated to be the fastest-growing segment during the 2026-2033 forecast period. This acceleration reflects broader e-commerce adoption, improved last-mile delivery capabilities, and better packaging technologies that help maintain produce integrity during transportation. Digital platforms allow consumers to access specialty and organic butternut squash varieties that may be less available in physical stores, while subscription models support regular deliveries aligned with household consumption patterns. The channel particularly resonates with urban professionals and health-conscious millennials who prioritize convenience and are willing to pay delivery premiums in exchange for time savings.

Regional Insights

North America Butternut Squash Market Trends

North America is set to command a significant portion of the butternut squash market share at an estimated 38% in 2026, with the United States setting the pace in both consumption patterns and product innovation. Strong market performance is supported by high per-capita vegetable intake, a mature cold chain infrastructure, and broad availability across supermarket, club, specialty, and online retail formats. Demand in the United States is further reinforced by health and wellness trends, where butternut squash features prominently in popular dietary approaches such as paleo, low-carbohydrate, and plant-forward eating styles. Its use spans home cooking, foodservice menus, and packaged products, highlighting its versatility and alignment with consumer preferences for nutrient-dense, flavorful ingredients.

Regulatory frameworks in North America support market development through stringent food safety oversight and well-established organic certification schemes that reinforce consumer confidence and encourage grower participation. Canada adds meaningful depth to regional dynamics through rising nutrition awareness, expanding distribution networks, and sustained interest in locally grown produce. The region’s innovation ecosystem promotes new product formats in frozen and processed categories, including pre-cut, seasoned, and ready-to-cook options designed for convenience-oriented shoppers. Ongoing investment in agricultural technology, post-harvest handling, and alternative production systems such as controlled-environment agriculture is improving efficiency and resilience, while direct-to-consumer channels such as farmers’ markets and community-supported agriculture programs help producers secure premium positioning and build long-term customer loyalty.

Europe Butternut Squash Market Trends

Europe will play a pivotal role in the global supply and consumption of butternut squash, with Germany, the United Kingdom, France, and Spain serving as the primary demand centers. Germany leads in overall market size, supported by strong domestic consumption and active re-export activities within the region, while the United Kingdom is experiencing particularly dynamic growth as butternut squash transitions from a niche ingredient to a mainstream staple in everyday cooking. Public health campaigns promoting higher vegetable intake, combined with the ingredient’s growing presence in home cooking, foodservice, and prepared food offerings, further strengthen its position within European diets.

Regulatory harmonization efforts of the European Union (EU) has facilitated seamless cross-border trade while enforcing strict quality, safety, and sustainability standards that strengthen consumer confidence in both fresh and organic butternut squash. Southern European countries, particularly Spain and Italy, serve as key production hubs with favorable growing conditions, supplying northern markets through established distribution networks. Investment increasingly targets sustainable farming practices, including integrated pest management and water-efficient techniques, while growing interest in local and regional food systems especially in markets such as France supports the expansion of butternut squash cultivation to meet rising domestic demand. Central and Eastern European markets offer additional growth potential as awareness and acceptance of butternut squash gradually increase, creating opportunities that can be unlocked through consumer education, targeted marketing, and improved distribution capabilities.

Asia Pacific Butternut Squash Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing butternut squash market between 2026 and 2033. China, India, and ASEAN countries collectively drive this momentum, with consumption patterns shaped by distinct culinary traditions, varying levels of urbanization, and different stages of economic development. In China, rising health consciousness among the middle class and policy emphasis on balanced diets are supporting higher vegetable intake, while in Japan, butternut squash is appearing more frequently in premium dishes and fusion-style applications that combine Western and local cuisines. India and key ASEAN markets are gradually increasing their use of butternut squash as modern retail formats introduce consumers to a broader range of vegetables and recipe ideas beyond traditional staples.

The regional market also benefits from structural manufacturing advantages such as comparatively low production costs, abundant agricultural labor, and expanding processing capacity, which together support its emergence as a potential hub for value-added butternut squash products. Market development is constrained by gaps in cold chain coverage, fragmented retail structures dominated by informal markets, and the need for sustained investment in consumer education to build familiarity with the ingredient. Capital is increasingly directed toward modern distribution systems, climate-suited cultivation practices, and product formats tailored to local tastes and cooking styles. Regulatory conditions remain heterogeneous, with more developed economies enforcing stricter safety and quality standards, while emerging markets progressively upgrade their frameworks to support organized retail growth and strengthen consumer protection.

Competitive Landscape

The global butternut squash market structure is moderately fragmented, dominated by leading players such as Dole Food Company, Fresh Del Monte Produce, Sysco Corporation, and Nature's Pride. The butternut squash market features a blend of large commercial producers and smaller farming operations, creating an intensely competitive environment. Leading companies are prioritizing investments in modern agricultural techniques and production technologies to secure reliable, high-quality output and reduce seasonal variability. At the same time, producers, distributors, and retailers are forming strategic alliances to strengthen their presence across key channels and reach a broader customer base. Growing consumer emphasis on organic and sustainably sourced vegetables is adding further competitive pressure, prompting market participants to adopt more sustainable farming practices and enhance their environmental credentials.

Key Industry Developments

- In November 2025, P.F. Chang’s launched a limited-time holiday menu featuring the return of Longlife Noodles & Prawns and new dishes such as Miso Lobster Dumplings, Butternut Squash Dumplings, Black Pepper Filet, Butter Cake, and seasonal beverages including an Apple Spice Refresher and two festive cocktails.

- In June 2025, Morrisons rolled out a new Market Street Pizza Counter range and £ 10 meal deal, offering two freshly prepared pizzas, including new 11" woodfired, stuffed-crust and 14" stonebaked options) plus a side or dessert. The range features meat and vegetarian choices such as a Woodfired Butternut Squash, Portobello Mushroom & Roast Veg Pizza, with extras and a Monday 10% More Card discount.

- In January 2025, Pacific Foods introduced four new gluten-free, organic items - three soups (spicy garden tomato, condensed tomato, and butternut squash with cinnamon and nutmeg) and a chicken bone broth with ginger, turmeric, and black pepper. The soups are priced around US$ 2.92-US$ 3.99 and the bone broth at US$ 5.58, and all products will be available at Whole Foods Market and on Amazon.

Companies Covered in Butternut Squash Market

- Dole Food Company

- Fresh Del Monte Produce

- Sysco Corporation

- Earthbound Farm

- Green Giant

- Birds Eye Foods

- Cascadian Farm

- Bonduelle Group

- Riverford Organic Farmers

- Driscoll's

- Nature's Pride

- Taylor Farms

- Wholesum Harvest

- Grimmway Farms

- Organic Valley

Frequently Asked Questions

The global butternut squash market is projected to reach US$ 3.3 billion in 2026.

Rising health and wellness awareness, growth of plant-forward diets, and expanding use in convenience-oriented food products across retail and foodservice channels are driving the market.

The market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Key market opportunities include expansion in value-added processed formats, organic and sustainable offerings, and increasing adoption in plant-based and functional food applications.

Dole Food Company, Fresh Del Monte Produce, Sysco Corporation, and Nature's Pride are some of the key players in the market.