- Processed Food

- Clarified Butter Market

Clarified Butter Market Size, Share, and Growth Forecast, 2026 - 2033

Clarified Butter Market By Nature Type (Organic, Conventional), Packaging Type (Jars, Tubs, Tins), Distribution Channel (Online, Offline), and Regional Analysis for 2026 - 2033

Clarified Butter Market Size and Trends Analysis

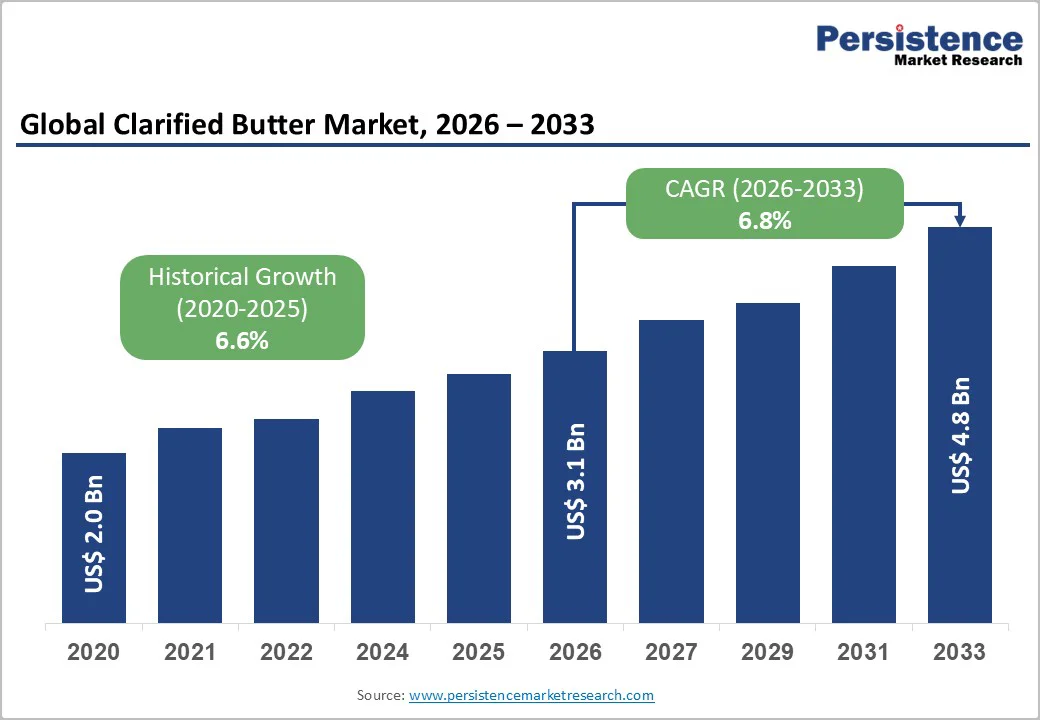

The global clarified butter market size is likely to be valued at US$3.1 billion in 2026. It is expected to reach US$4.8 billion by 2033, growing at a CAGR of 6.8% from 2026 to 2033, driven by health-conscious consumers seeking lactose-free alternatives, integration into ketogenic, paleo, and Ayurvedic diets, and expansion in foodservice applications.

Organic and grass-fed variants are gaining traction amid clean-label and premiumization trends, while conventional types maintain volume leadership due to affordability. Expansion in foodservice, bakery, confectionery, and ready-to-eat meals contributes to growing market adoption.

Key Industry Highlights:

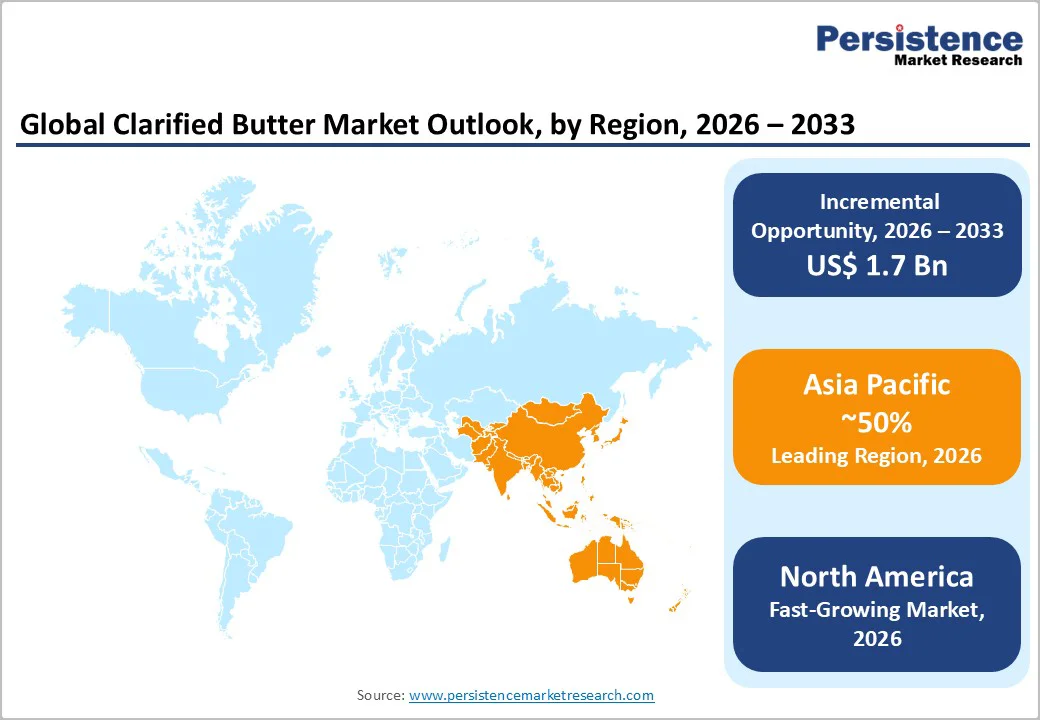

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 50% in 2026, driven by cultural consumption, large-scale production, regulatory standards, key player consolidation, urbanization, and investments in processing infrastructure.

- Fastest-growing Region: North America is likely to be the fastest-growing region in the market in 2026, driven by keto diet trends, adoption of multicultural cuisine, demand for organic and grass-fed products, supportive labeling regulations, and investments in sustainable dairy production.

- Leading Nature Type: Conventional is projected to represent the leading nature type in 2026, accounting for 78% of the market share, driven by affordability and wide availability.

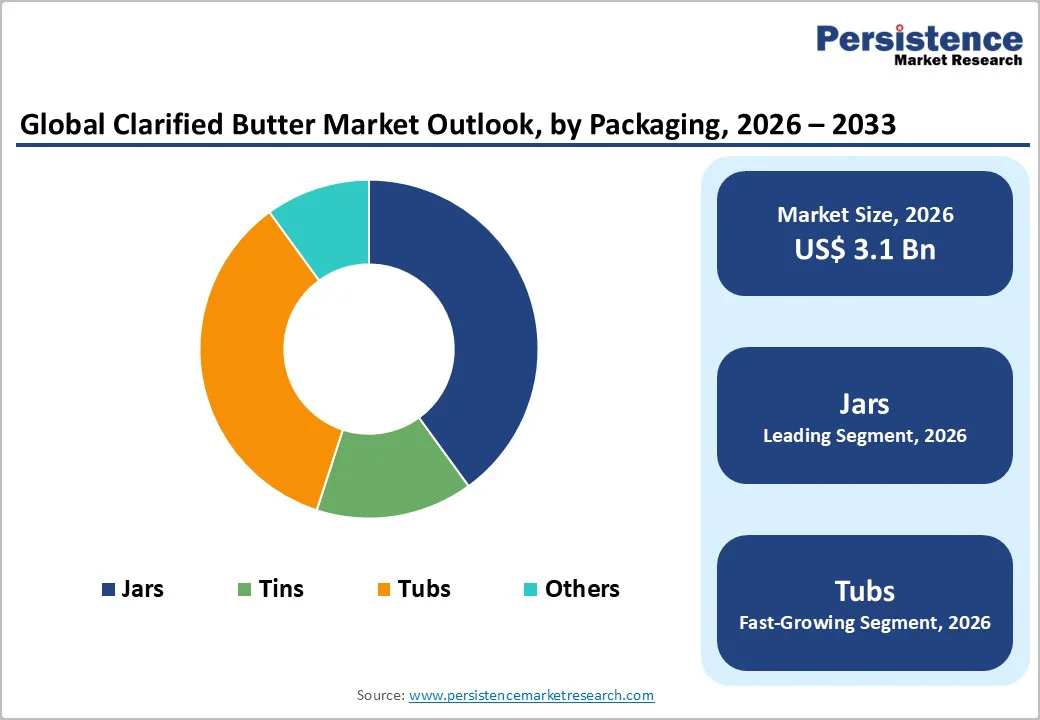

- Leading Packaging Type: Jars are expected to be the leading packaging type, accounting for over 42% of revenue share in 2026, driven by durability, product purity, and strong consumer preference for premium glass packaging.

- Leading Distribution Channel: Offline is anticipated to be the leading distribution Channel, accounting for over 70% of the revenue share in 2026, driven by strong retail presence, consumer trust, and preference for in-store product selection.

| Key Insights | Details |

|---|---|

|

Clarified Butter Market Size (2026E) |

US$3.1 Bn |

|

Market Value Forecast (2033F) |

US$4.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Health Awareness and Dietary Shifts

As consumers become increasingly conscious of the ingredients they use daily, ghee, clarified butter, has gained popularity as a natural, lactose-free, and nutrient-rich alternative to traditional cooking fats. Its high smoke point, rich antioxidant profile, and presence of fat-soluble vitamins (A, D, E, and K) make it appealing to individuals seeking cleaner, minimally processed sources of nutrition. The global rise of ketogenic, paleo, and Ayurvedic diets has further positioned clarified butter as a functional fat that supports metabolism, digestive health, and cognitive performance.

Consumers are moving away from artificial trans-fat products and embracing traditional fats believed to offer wellness benefits. Organic, grass-fed clarified butter has seen particularly strong momentum among premium health-focused buyers. This trend is reinforced by growing trust in products that are perceived as natural, heritage-based, and compatible with modern wellness lifestyles. As awareness spreads through influencers, nutritionists, and digital education platforms, clarified butter continues to transition from a regional staple to an internationally recognized health-forward ingredient.

High Production Costs

Clarified butter requires a large volume of raw milk and high-quality butter, both of which are subject to price volatility driven by feed costs, seasonal supply fluctuations, and dairy industry dynamics. The multi-stage heating, simmering, and filtration process used to remove milk solids also increases fuel, labor, and quality-control expenses. Organic and grass-fed clarified butter further elevate production costs due to premium raw material sourcing and stricter certification requirements. These factors make clarified butter considerably more expensive than common cooking oils and regular butter.

Maintaining consistent quality standards and complying with regional food safety regulations, such as FSSAI in India, FDA guidelines in the U.S., and EU dairy standards, adds operational complexity and cost. Packaging preferences, including glass jars used in premium segments, raise logistics and handling expenses due to higher weight and fragility.

For manufacturers, this cost structure limits scalability and pressures them to balance premium positioning with competitive pricing. High-quality packaging, especially glass jars preferred for premium clarified butter, adds notable cost due to heavier transportation loads, higher breakage risk, and specialized storage conditions.

Innovation in Functional and Premium Products

Evolving consumer preferences and the rising appeal of natural, nutrient-rich foods. Manufacturers are increasingly exploring value-added variations such as grass-fed, A2 milk–based, flavored, spiced, and fortified ghee, targeting consumers seeking healthier and more versatile cooking fats. Functional enhancements such as blends with turmeric, ashwagandha, MCT oil, omega-rich ingredients, or herbal infusions align well with the growing demand for products that support digestion, immunity, cognitive function, and metabolic health. Such enriched formulations allow clarified butter to move beyond traditional culinary use and enter wellness, sports nutrition, and functional food categories.

Premium product lines offer additional revenue potential through organic certifications, sustainable sourcing, small-batch artisanal production, and eco-friendly packaging, which appeal to high-income and health-oriented consumers in North America, Europe, and the Asia Pacific. As clarified butter becomes more integrated into international cuisines, functional beverages, sports nutrition, and gourmet foodservice, brands have opportunities to differentiate through creativity and premiumization.

Category-wise Analysis

Nature Type Insights

The conventional segment is expected to lead the market, accounting for approximately 78% of the total revenue in 2026, driven by the best combination of affordability, accessibility, and large-scale production efficiency. Conventional ghee benefits from strong dairy supply chains in key producing countries such as India, e.g., brands such as Amul have extensive rural procurement networks and high-volume processing facilities capable of meeting mass-market demand. This scale advantage reduces per-unit manufacturing costs by nearly 40% compared to organic variants, enabling competitive pricing across supermarkets, hypermarkets, and general trade outlets. Multinational players such as Nestlé leverage wide retail penetration and established dairy distribution to maintain consistent availability.

Organic clarified butter is likely to be the fastest-growing in 2026, driven by rising demand for natural, clean-label, and minimally processed dairy fats. Consumers increasingly associate organic dairy products with superior nutritional value, hormone-free sourcing, and ethical farming practices. This has made organic clarified butter particularly attractive to health-driven consumers in North America and Europe who follow ketogenic, paleo, Ayurvedic, and whole-food diets. Specialty stores, organic markets, and e-commerce platforms have accelerated their reach. Example Ancient Organics, a California-based brand, produces small-batch, grass-fed, USDA-certified organic ghee, which has become highly popular among health-conscious buyers seeking artisanal purity.

Packaging Type Insights

Jars are projected to lead the market, capturing around 42% of the total revenue share in 2026, driven by superior product protection, longer shelf stability, and strong premium appeal. Glass jars, in particular, prevent flavor migration, maintain clarity, and shield the product from air exposure, helping retain aroma and nutritional integrity over time. Their transparency allows consumers to visually verify purity and granulation, which is especially important for premium and organic clarified butter purchases. Example Organic Valley, a leading organic dairy brand, packages its clarified butter exclusively in glass jars to emphasize purity and premium quality.

Tubs are likely to be the fastest-growing packaging type in 2026, due to strong adoption in bulk, commercial, and foodservice applications. Their lightweight and cost-efficient nature makes them ideal for high-volume consumers such as restaurants, bakeries, cloud kitchens, and catering services. Tubs offer convenience through easy scooping and minimal risk of breakage, which is crucial in fast-paced commercial kitchens. Tubs are gaining traction among value-driven households, who are purchasing larger quantities for extended use. Example Annapurna Group supplies clarified butter in large-capacity tubs to major foodservice clients across South Asia and the Middle East, enabling cost-effective procurement for large-scale culinary operations.

Distribution Channel Insights

The offline channel is projected to lead, capturing around 70% of total revenue in 2026, driven by widespread availability across supermarkets, hypermarkets, dairy outlets, and traditional stores. In regions where clarified butter is a cultural staple, such as India, Sri Lanka, Bangladesh, and the Middle East, consumers prefer to buy in-store to assess freshness, packaging, aroma, and brand authenticity. Offline retail ensures strong visibility and trust, especially for daily-use pantry items. Traditional neighborhood stores continue to play a vital role in South Asia due to habitual buying patterns and local credit systems. Foodservice procurement also heavily depends on offline wholesale hubs. For instance, Patanjali Ayurved has built one of India’s largest offline FMCG distribution networks, enabling its clarified butter products to reach millions of retail counters nationwide.

Online retail is likely to be the fastest-growing distribution channel in 2026, driven by increased digital adoption, wide product accessibility, and rising comfort with ordering packaged dairy online. E-commerce platforms allow consumers to compare organic, grass-fed, flavored easily, and specialty clarified butter varieties, options often unavailable in neighborhood stores. Improved cold-chain logistics, faster delivery, and sealed packaging have further strengthened trust in online dairy purchases. Global platforms such as Amazon, BigBasket, and Instacart enable direct access to imported and premium clarified butter brands. The D2C boom has also accelerated sales, especially among younger consumers. Example Pure Indian Foods successfully uses its direct-to-consumer online store to sell organic, grass-fed ghee in the U.S., offering detailed farm-sourcing information and subscription-based auto-delivery.

Regional Insights

North America Clarified Butter Market Trends

The North America region is likely to be the fastest-growing region in 2026, driven by consumers increasingly adopting high-fat, low-carb diets such as keto and paleo, both of which position ghee as a preferred cooking fat due to its lactose-free profile and high smoke point. U.S. health-focused consumers are experimenting with keto diets, and clarified butter is a mainstream pantry item rather than an ethnic specialty product. Retail penetration has improved significantly, with clarified butter now a staple in stores such as Whole Foods, Costco, and Walmart, making it easier for mainstream consumers to adopt it.

Innovation-led growth is reshaping the competitive landscape as brands invest in flavored, fortified, and sustainable clarified butter products. For example, Fourth & Heart’s Vanilla Bean and Turmeric ghee lines have gained strong traction in North America, appealing to both functional food users and home chefs seeking premium alternatives to conventional butter. Brands are launching functional and flavored clarified butter products designed for health-conscious consumers. Variants infused with herbs, spices, or other wellness-focused ingredients are becoming increasingly popular, as consumers look for value-added dairy fats. For example, Fourth & Heart has seen rapid growth by offering flavors such as Vanilla Bean, Turmeric, and Himalayan Pink Salt, appealing to both health-focused and gourmet audiences.

Europe Clarified Butter Market Trends

Europe is likely to be a significant market for clarified butter in 2026, driven by the growing shift toward natural, lactose-free, and high-quality fat sources. The region’s growing interest in gourmet cooking, clean-label dairy, and Ayurveda-inspired wellness trends is driving ghee adoption across Germany, the U.K., France, and the Netherlands. European consumers are also embracing clarified butter for its high smoke point and suitability for baking and sautéing, replacing conventional butter in healthier cooking practices. Mainstream supermarkets such as Tesco, Carrefour, Edeka, and Waitrose are widening shelf space for clarified butter. A notable development is GHEE EASY, a leading European brand from the Netherlands, which expanded its organic product line across Germany and Scandinavia, making clarified butter more accessible to everyday households.

Premiumization and multicultural food influences continue to drive innovation, with European consumers seeking organic, grass-fed, and artisanal clarified butter variants. The growth of vegan and flexitarian lifestyles has indirectly boosted interest in pure, minimally processed animal fats as part of balanced nutrition. Brands are also focusing on sustainable sourcing, eco-friendly packaging, and transparent labeling to meet the EU standards. Flexitarian and health-conscious consumers seeking balanced diets rather than strict plant-based regimes are embracing clarified butter for its digestibility, lactose-free status, and suitability for high-heat cooking.

Asia Pacific Clarified Butter Market Trends

The Asia Pacific region is anticipated to be the leading region, driven by strong cultural consumption, high household usage, and traditional culinary applications. Countries such as India and China account for most regional demand, with ghee an essential ingredient in daily cooking, festive foods, and religious rituals. Large-scale dairy production and cooperative models in India, such as Amul, ensure widespread availability and affordable pricing, enabling conventional clarified butter to maintain a dominant market share.

Health-driven trends are shaping innovation across the region, with consumers increasingly seeking organic, grass-fed, and flavored clarified butter variants. Functional and clean-label products are gaining traction among health-conscious buyers, keto diet followers, and young urban professionals. Brands are introducing small-batch artisanal and fortified ghees to differentiate products and capture higher margins. Investments in processing facilities, modern packaging, and cold-chain logistics are helping manufacturers scale operations while maintaining quality standards.

Competitive Landscape

The global clarified butter market exhibits a moderately fragmented structure, driven by a mix of large dairy cooperatives, multinational food companies, regional players, and niche artisanal producers all vying for share across different regions, product types, and consumer segments.

The market’s fragmentation means many players, from heritage brands in South Asia to specialty organic producers in North America and Europe, coexist. With key leaders including Amul (GCMMF), Nestlé, Britannia Industries, Patanjali Ayurved Limited, Pure Indian Foods, Ancient Organics, Organic Valley, GHEE EASY, and others, the competitive environment is shaped by regional dominance as well as niche premium positioning.

These players compete through diversified product portfolios, including conventional, organic, grass-fed, flavored, and specialty ghee, by investing in quality certifications, scalable dairy sourcing, and consumer-facing branding. Firms leverage strategic distribution via modern retail, wholesale, exports, and direct-to-consumer channels, while pushing innovation in packaging, functional variants, and compliance with international food-safety standards to differentiate their offerings.

Key Industry Developments:

- In September 2025, 4th & Heart launched its Truffle Ghee at Whole Foods (US$12.99), a lactose-free, truffle-infused clarified butter offering a premium, health-focused alternative to traditional fats.

- In July 2024, Challenge Dairy Products launched its spreadable lactose-free clarified butter with canola oil nationwide, reinforcing its commitment to providing convenient, flavorful dairy options and meeting the rising demand for lactose-free products.

Companies Covered in Clarified Butter Market

- Amul (GCMMF)

- Nestlé

- Britannia Industries

- Patanjali Ayurved Limited

- Haryana Dairy Development Cooperative Federation Limited.

- Pure Indian Foods

- Ancient Organics

- GHEE EASY

- Almarai

- Annapurnagroup and M/s Sundarbans Food Products (I) Pvt. Ltd.

Frequently Asked Questions

The global clarified butter market is projected to reach US$3.1 billion in 2026.

Rising health awareness, demand for lactose-free and organic fats, and growing adoption in ketogenic, Ayurvedic, and multicultural cuisines drive the clarified butter market.

The clarified butter market is expected to grow at a CAGR of 6.8% from 2026 to 2033.

Innovation in functional and premium products (e.g., grass-fed, organic, flavored, and fortified ghee), expansion in e-commerce and online retail channels, and growth in multicultural and gourmet food applications.

Amul (GCMMF), Nestlé, Britannia Industries, Patanjali Ayurved Limited, and Haryana Dairy Development Cooperative Federation Limited are the leading players.