- Medical Devices

- Bone Grafts Market

Bone Grafts Market Size, Share and Growth Forecast, 2026-2033

Bone Grafts Market by Graft Type (Autografts, Allografts, Xenografts, Synthetic Bone Grafts, Cell‑based), Composition (Ceramic‑based, Polymer‑based, Composite Materials, Growth Factor‑based, Cell‑based Scaffolds), Application (Spinal Fusion, Trauma Repair, Craniomaxillofacial, Joint Reconstruction, Dental Bone Grafting, Others), and Regional Analysis for 2026-2033

Bone Grafts Market Share and Trends Analysis

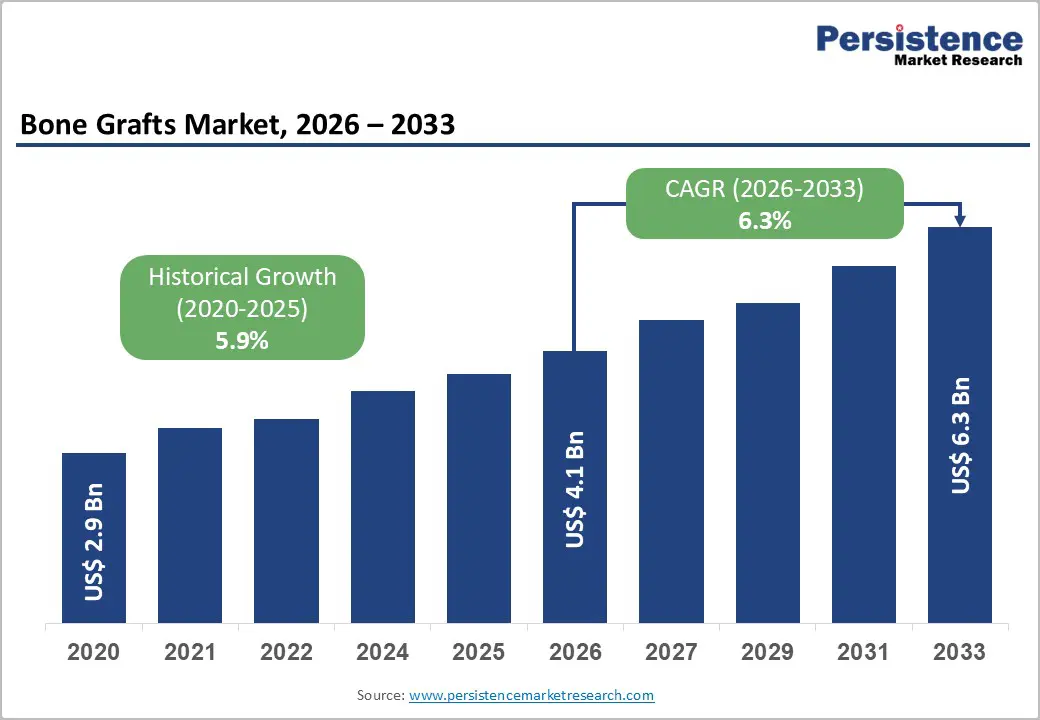

The global bone grafts market size is likely to be valued at US$ 4.1 billion in 2026, and is projected to reach US$ 6.3 billion by 2033, growing at a CAGR of 6.3% during the forecast period 2026–2033. This growth reflects sustained demand for orthopedic and dental bone graft solutions driven by rising procedural volumes in spinal fusion, trauma repair, and reconstructive surgeries.

Technological advancements in biologic and synthetic graft materials, combined with a growing geriatric population and higher incidence of bone disorders, underpin industry expansion. Additionally, regulatory approvals and investments in innovative cell-based graft matrices continue to improve clinical outcomes and broaden adoption across surgical disciplines.

Key Industry Highlights

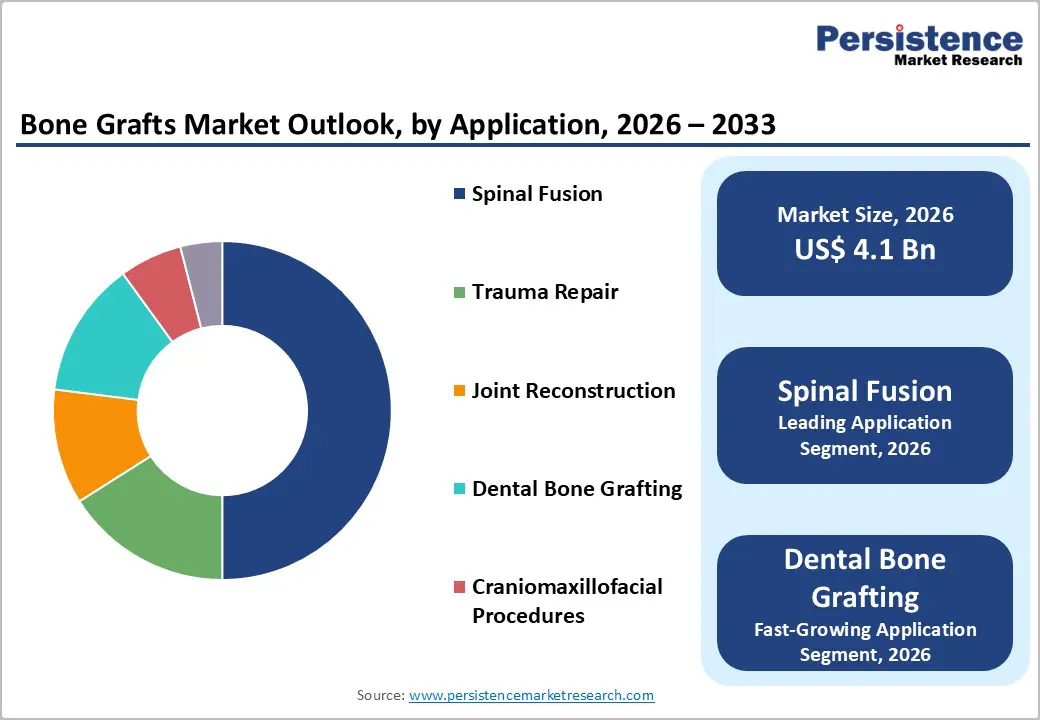

- Dominant Application: Spinal fusion is estimated to account for over 50% of graft demand in 2026, whereas dental bone grafting is projected to grow the fastest at a 9.1% CAGR through 2033, supported by rising demand for cosmetic dentistry.

- Leading Graft Types: Allografts are projected to lead with approximately 42% share in 2026, while synthetic grafts are expected to register the fastest growth, with a CAGR of approximately 8.2% during 2026–2033, reflecting advancements in biomaterials and biologics.

- Material Composition Leadership: Ceramic-based materials are projected to account for approximately 45% of the market in 2026, while cell-based scaffolds are expected to grow fastest, with a 2026-2033 CAGR of 13%, driven by regenerative medicine innovations.

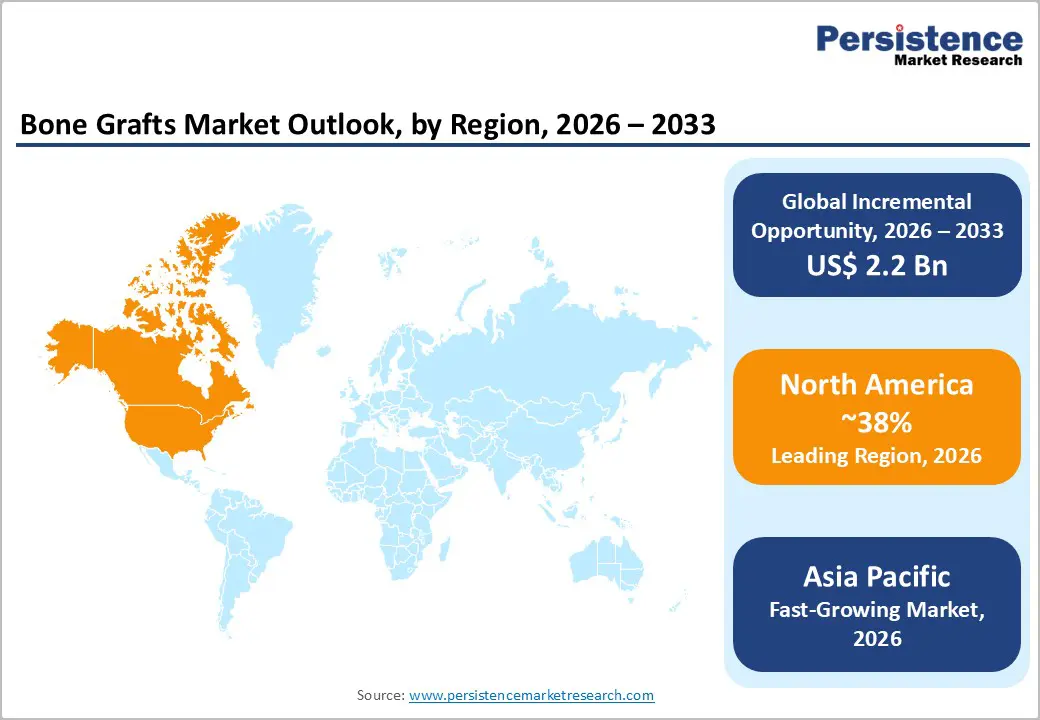

- Regional Leadership: North America is estimated to dominate with a roughly 38% share in 2026, while the Asia Pacific market is likely to record the fastest growth at 7% CAGR through 2033, fueled by rising surgical volumes.

- Competitive Dynamics: Market developments are expected to include M&A, portfolio expansion into synthetic and biologic grafts, and geographic expansion into high-potential markets such as China, India, and Southeast Asia.

| Global Market Attributes | Key Insights |

|---|---|

| Bone Grafts Market Size (2026E) | US$ 4.1 Bn |

| Market Value Forecast (2033F) | US$ 6.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Surge in Surgical Demand Coupled with Industry Innovation and Healthcare Expansion

The growth of the bone grafts market is likely to be boosted by the rising global volume of orthopedic and dental surgical procedures, particularly spinal fusion and trauma repair, alongside rapid technological innovation. Companies such as Xtant Medical launched nanOss Strata, a next-generation synthetic bone graft designed for enhanced bioactivity and improved integration with native bone. Concurrently, Stryker introduced BIO4® viable bone matrix, a cellular allograft engineered to mimic natural bone regeneration, while Cerapedics Inc. received approval from the U.S. Food and Drug Administration (FDA) for PearlMatrix P-15 Peptide Enhanced Bone Graft targeting lumbar fusion procedures. These product launches reflect a strategic shift toward materials that improve osteoconductivity and clinical outcomes, increasing surgeon confidence and expanding use across hospitals, specialty clinics, and ambulatory surgical centers.

In addition to product innovation, healthcare access and infrastructure growth in emerging regions are amplifying market uptake. Regulatory support, such as breakthrough designations, accelerates commercial pathways for advanced graft technologies, shortening the time from development to clinical use. Expanding healthcare expenditures in the Asia-Pacific, particularly in China, India, and Southeast Asia, are enabling broader procedural coverage and adoption, while government initiatives and private investments are improving affordability and surgical capacity. This dual impact of innovative graft solutions and expanding care-delivery systems is resulting in measurable increases in procedural volumes, thereby encouraging manufacturers to deepen their geographic presence and pursue strategic partnerships.

High Costs, Regulatory Complexity, and Supply Chain Constraints

The adoption of advanced bone graft technologies remains constrained by high treatment and material costs, particularly for growth factor-enhanced and cell-based grafts. Cerapedics’ P-15 peptide-enhanced bone grafts and cellular allograft products, such as Stryker’s BIO4®, entered wider clinical use for spinal and trauma applications at premium price points, limiting adoption in cost-sensitive hospitals. In several markets, reimbursement coverage for these newer biologics remains inconsistent, requiring providers to absorb higher costs or rely on traditional graft options. As a result, purchasing decisions continue to favor conventional allografts and ceramics, slowing near-term penetration of advanced graft technologies despite their clinical advantages.

Regulatory oversight and supply chain limitations continue to restrain market expansion. Products involving cell-based matrices and biologics are subject to extended review timelines under U.S. FDA and European Union Medical Device Regulation (EU MDR) frameworks, particularly when extensive clinical validation is required. Allograft availability also depends on donor tissue supply, which is constrained by strict screening, sterilization, and cold-chain logistics. Several hospital networks in Europe and Asia reported procedure-scheduling delays attributable to limited allograft availability, underscoring how donor dependence and transportation complexity can constrain procedure volumes. The pricing pressure, regulatory delays, and donor-supply constraints together continue to act as structural barriers to faster market adoption.

Minimally Invasive Surgery Expansion, Emerging Market Investment, and Dental Regeneration Demand

The market for bone grafts is well positioned to benefit from the rapid shift toward minimally invasive orthopedic and dental procedures, driven by faster recovery and reduced surgical trauma. Stryker expanded clinical adoption of injectable graft solutions compatible with minimally invasive spinal fusion, while Zimmer Biomet introduced procedure-optimized bone graft materials designed for outpatient orthopedic settings. These developments support broader adoption across spinal fusion, trauma repair, and joint reconstruction, thereby enabling higher procedural throughput in ambulatory surgical centers. As healthcare systems increasingly prioritize same-day surgery models, graft products tailored for minimally invasive techniques represent a clear avenue for sustained volume growth.

At the regional and clinical level, emerging market healthcare investments and dental bone regeneration demand are reinforcing the market opportunity. India and China increased public and private investment in hospital infrastructure and surgical training, improving access to orthopedic procedures and advanced graft materials. At the same time, Geistlich Pharma expanded adoption of its dental bone graft portfolio for ridge augmentation and sinus lift procedures, reflecting rising implant volumes and demand for cosmetic dentistry. Clinicians’ preference for biocompatible graft materials with predictable outcomes continues to strengthen long-term growth potential across both orthopedic and dental applications.

Category-wise Analysis

Graft Type Insights

Allografts are projected to account for approximately 42% of the bone grafts market revenue in 2026, owing to strong clinical familiarity and reliable osteoinductive performance. Their availability in formats such as demineralized bone matrix and freeze-dried grafts supports broad use across spinal fusion, trauma repair, and joint reconstruction. LifeNet Health expanded its processed allograft portfolio with enhanced sterility and handling characteristics, thereby reinforcing surgeons' confidence and the reliability of allograft supply. These developments are expected to sustain allografts’ leadership position as hospitals continue to prioritize proven graft materials with predictable outcomes.

Synthetic grafts and cell-based matrices are projected to be the fastest-growing graft types, with an estimated CAGR of 8.2% through 2033. Growth is driven by improved safety profiles, tunable resorption rates, and rising use in minimally invasive procedures. Zimmer Biomet introduced a next-generation synthetic graft substitute optimized for controlled resorption and enhanced bone integration, targeting spine and trauma applications. These innovations, combined with increasing regulatory clarity for biologic matrices, are expected to accelerate adoption across outpatient and specialty surgical settings.

Composition Insights

Ceramic-based materials are projected to account for approximately 45% of the bone grafts market share in 2026. Calcium phosphate and bioactive glass formulations exhibit consistent demand owing to their structural similarity to native bone tissue and strong osteoconductive properties. Surgeons are relying on these materials in spinal fusion and orthopedic reconstruction procedures because of their long clinical history and predictable performance. Their compatibility with the host bone and mechanical stability support widespread procedural use. Kuros Biosciences has expanded clinical indications for its ceramic graft platform after reporting favorable real-world fusion outcomes, and this development is reinforcing practitioner confidence. Hospitals continue to adopt ceramic substitutes because they offer standardized composition and reduced variability relative to donor-derived materials. These advantages are expected to sustain ceramics as the dominant composition category over the near term.

Cell-based scaffolds are emerging as the fastest-growing material segment and are projected to expand at an estimated CAGR of 13% through 2033. Demand is increasing for biologically active grafts that stimulate osteogenesis and accelerate tissue regeneration in complex surgical cases. Surgeons are favoring these advanced constructs in multi-level spinal fusion and challenging trauma reconstructions where an enhanced healing response is critical. Medtronic plc is advancing next-generation biologic graft formulations that integrate controlled growth factor delivery, and this investment is signaling a strong commitment to regenerative technologies. Research and development efforts are focusing on improving cellular viability, scaffold architecture, and integration efficiency. As clinical data supporting improved fusion rates continues to accumulate, biologically enhanced scaffolds are expected to reshape the material composition landscape and influence procurement strategies across orthopedic and dental specialties.

Application Insights

Spinal fusion is projected to account for nearly 50% of application-based demand in 2026, becoming the largest clinical use case for bone graft materials. High procedural volumes associated with degenerative disc disease, spinal stenosis, and trauma-related instability are sustaining steady utilization of graft substitutes. Surgeons are requiring materials that deliver structural reinforcement while promoting consistent bone integration. Device manufacturers are introducing integrated spinal fusion systems that combine graft materials with fixation instrumentation, and this bundling approach is streamlining operating room workflows. Hospitals are favoring comprehensive solutions that reduce procedural variability and improve surgical efficiency. These coordinated product strategies are strengthening adoption rates and are reinforcing spinal fusion as the core application segment within the broader bone grafts market.

Dental bone grafting is emerging as the fastest-growing application, projected to expand at a 2026-2033 CAGR of approximately 9.1%. Growth is being driven by rising dental implant placements, ridge preservation procedures, and increasing demand for cosmetic oral rehabilitation. Patients are seeking improved aesthetic outcomes, and clinicians are incorporating advanced graft materials to support implant stability and bone regeneration. Geistlich Pharma AG has expanded practitioner engagement through targeted clinical education programs on sinus lift and socket-preservation techniques. Dental practices are increasingly investing in regenerative materials that enhance predictability and reduce healing time. As implant-centered dentistry continues to expand across both developed and emerging markets, dental bone grafting is expected to capture a growing share of total procedural demand within the forecast period.

Regional Insights

North America Bone Grafts Market Trends

North America is estimated to account for around 38% of the bone grafts market value in 2026, maintaining its position as the leading regional contributor. Demand is anchored by high procedural volumes in spinal fusion and joint reconstruction, supported by advanced hospital infrastructure and widespread access to specialty surgical centers. Favorable reimbursement mechanisms enable consistent adoption of advanced bone graft materials, including biologics and synthetic substitutes. Orthofix Medical expanded its U.S. orthobiologics portfolio with newly approved graft substitutes for spine and trauma care, reinforcing clinical confidence. The region continues to serve as an early commercialization market for new graft technologies. Strong surgeon familiarity and established treatment protocols further support sustained leadership.

North America continues to expand at a measured pace, reflecting a mature market supported by steady, innovation-driven demand. Regulatory oversight provides predictable approval pathways, which helps accelerate clinician adoption once products receive clearance. Globus Medical increased investments in biologics-integrated spine systems across U.S. surgical networks, underscoring the growing convergence of implants and graft materials. Competitive intensity remains high, with established players relying on robust clinical evidence and surgeon education programs. Hospitals increasingly prioritize graft solutions supported by strong outcome data. This environment supports stable, long-term regional expansion. Overall growth remains consistent rather than rapid, aligned with the region’s mature market profile.

Europe Bone Grafts Market Trends

Europe remains a major contributor to market demand, supported by strong public healthcare systems in Germany, the U.K., France, and Spain. Consistent orthopedic procedure volumes, particularly in spinal fusion and joint reconstruction, underpin regional performance. Standardized regulatory oversight under the EU MDR has strengthened confidence in the compliance of bone graft materials and improved transparency in procurement. B. Braun expanded its MDR-aligned bone graft and substitute portfolio across major European healthcare systems, reiterating the growing institutional adoption of these products. Clinical decision-making increasingly emphasizes the documentation of safety and performance. These factors collectively support Europe’s stable and structured market presence.

The regional market is foreseen to continue to progress at a balanced pace across Western and Southern Europe. While reimbursement policies vary between countries, hospitals favor graft materials with established clinical track records and regulatory compliance. European academic hospitals expanded participation in post-market clinical follow-up programs for bone graft substitutes, strengthening real-world evidence and clinician confidence. Investment in regenerative and biologically active materials continues to rise. Procurement decisions increasingly focus on long-term outcomes and lifecycle value. Europe remains a quality-driven and regulation-anchored market. Growth follows a steady, methodical trajectory rather than accelerated expansion.

Asia Pacific Bone Grafts Market Trends

Asia Pacific is projected to be the fastest-growing regional market for bone grafts, registering an estimated CAGR of 7.7% from 2026 to 2033, driven by expanding surgical access and rising healthcare expenditure. China, Japan, and India are primary growth engines, driven by increasing volumes of orthopedic and dental procedures. Olympus strengthened its distribution network for orthopedic biomaterials across Southeast Asia, thereby improving access in emerging healthcare facilities. Growing awareness of advanced graft solutions supports wider clinical adoption. Infrastructure development remains a key catalyst for growth. These factors collectively position the Asia-Pacific region as the fastest-growing market.

The growth momentum is reinforced by improving affordability and localized production capabilities. Chinese manufacturers increased domestic production of synthetic bone graft materials to support national hospital procurement initiatives, enhancing supply reliability. Expanding insurance coverage and rising medical tourism further boost procedural volumes. International companies continue to invest in clinician training and regional partnerships. Adoption is extending beyond major urban hospitals into secondary care centers. Regulatory pathways are becoming more defined, improving market entry conditions. Asia Pacific is expected to steadily narrow the gap with mature regions. The region remains the primary engine of future market expansion.

Competitive Landscape

The global bone grafts market structure exhibits moderate consolidation. Major companies such as Medtronic, Zimmer Biomet Holdings, Stryker Corporation, Johnson and Johnson through DePuy Synthes, and Smith and Nephew control lion’s share of the total market revenue. These organizations are leveraging comprehensive portfolios that include allografts, synthetic substitutes, and biologic graft materials. Strong relationships with orthopedic and spine surgeons are reinforcing recurring product adoption. Integrated graft and implant systems are supporting streamlined procedural workflows in spinal fusion and trauma reconstruction. Extensive regulatory expertise and global manufacturing capacity are enabling consistent product availability across key markets. Continuous investment in clinical trials and post-market evidence generation is strengthening physician confidence and differentiating leading brands in competitive tender environments.

Alongside multinational leaders, specialized biologics firms and regional tissue banks are targeting niche indications and localized distribution models. Companies such as Orthofix Medical Inc., Geistlich Pharma AG, Kuros Biosciences AG, and LifeNet Health are emphasizing material innovation, surgeon training, and focused clinical applications. Regulatory approval processes, stringent tissue-sourcing controls, and extensive validation requirements maintain high entry barriers. Despite these constraints, advancements in synthetic scaffolds and regenerative technologies are enabling smaller innovators to compete selectively in high-growth sub-segments. Larger corporations are actively evaluating acquisition opportunities and strategic partnerships to expand technology access and pipeline depth. Gradual consolidation is likely to continue as established players seek to strengthen their regenerative medicine capabilities and broaden their procedural reach.

Key Industry Developments

- In January 2026, Alphatec Holdings (ATEC) entered a strategic agreement to obtain exclusive U.S. commercial rights for Theradaptive’s OsteoAdapt® osteoinductive bone graft platform, targeting spinal fusion and dental applications. The deal includes upfront and milestone payments plus perpetual royalties, representing a substantial financial commitment.

- In December 2025, Xtant Medical announced the commercial launch of its next-generation NanoSS Strata synthetic bone graft, which features enhanced material structure intended to support improved bone regeneration in orthopedic and spinal procedures. The product rollout aims to provide surgeons with refined handling characteristics and consistent performance.

- In July 2025, Medtronic announced that its INFUSE™ Bone Graft program reached a key regulatory milestone as the U.S. FDA designated the transforaminal lumbar interbody fusion (TLIF) indication as a Breakthrough Device. Initial study results met early success criteria and prompting preparation of a premarket approval (PMA) submission.

Companies Covered in Bone Grafts Market

- Medtronic Plc

- Stryker Corporation

- Zimmer Biomet

- Johnson & Johnson

- Smith & Nephew

- Baxter International

- LifeNet Health

- Arthrex, Inc.

- Integra LifeSciences

- NuVasive, Inc.

- Exactech, Inc.

- Geistlich Pharma AG

Frequently Asked Questions

The global bone grafts market is projected to reach US$ 4.1 billion in 2026.

Rising orthopedic and dental surgery volumes, advancements in synthetic and biologic graft materials, and expanding access to surgical care are key growth drivers.

The market is poised to witness a CAGR of 6.3% from 2026 to 2033.

Prime growth opportunities include minimally invasive surgical adoption, expanding healthcare infrastructure in emerging economies, and rising demand for dental bone regeneration.

Medtronic, Zimmer Biomet, Stryker, DePuy Synthes, and Smith+Nephew are among the key players in the market.