- Automotive Components & Materials

- Automotive Ignition Parts Market

Automotive Ignition Parts Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Ignition Parts Market by Engine Type (Gasoline, Diesel, Others), Ignition (Coil on Plug Ignition, Simultaneous Ignition, Compression Ignition, Others), Component (Ignition Switch, Spark Plug, Glow Plug, Ignition Coil, Others), Vehicle (Passenger Cars, Commercial Vehicles, Others), and Regional Analysis for 2025 - 2032

Automotive Ignition Parts Market Size and Trend Analysis

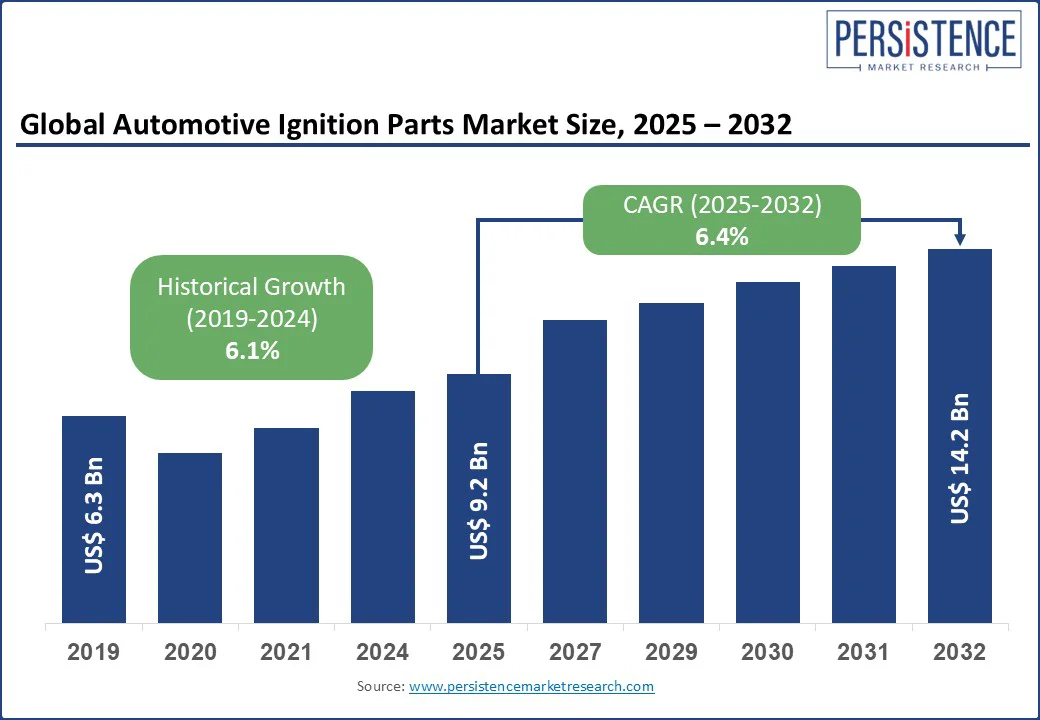

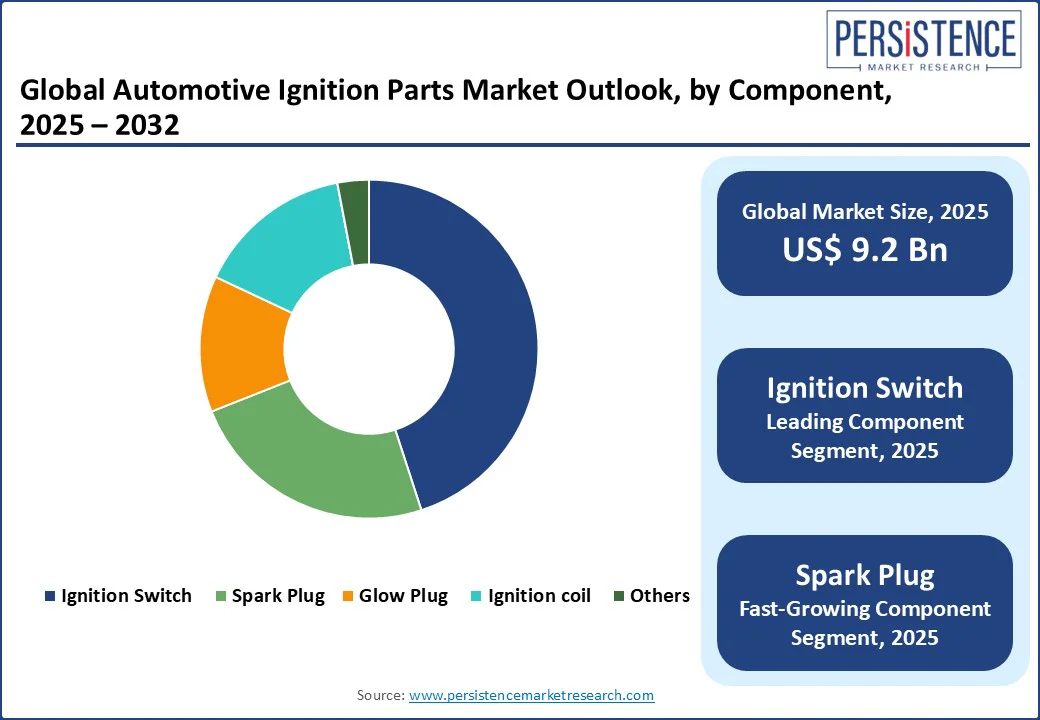

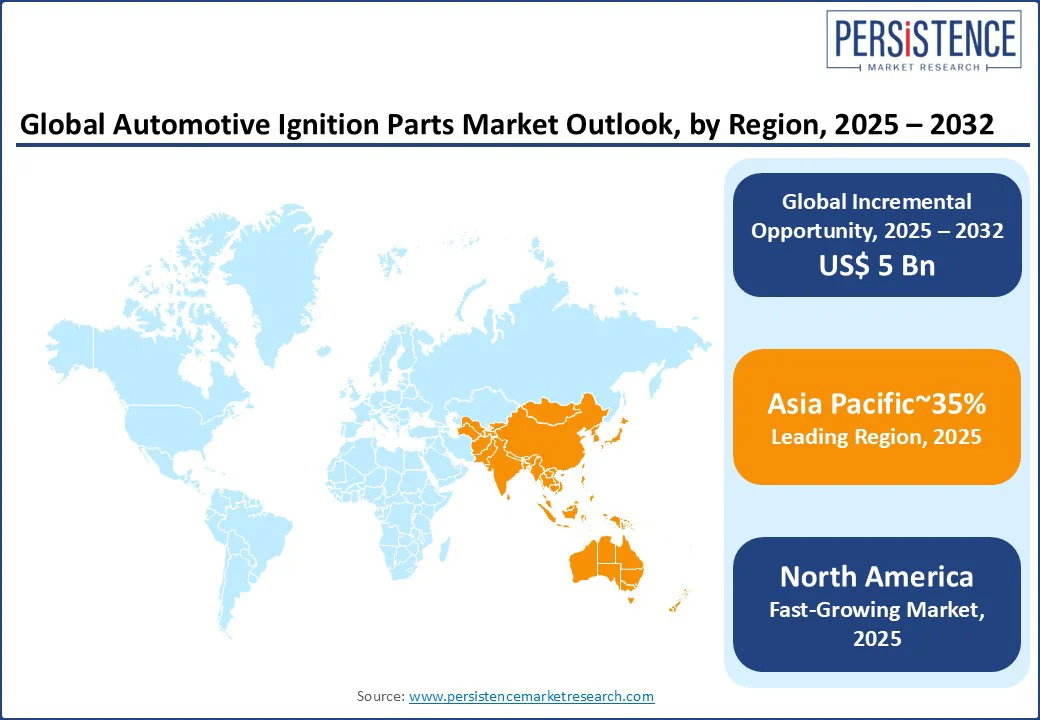

The global automotive ignition parts market size is likely to be valued at US$9.2 Bn in 2025 and is expected to reach US$14.2 Bn by 2032, growing at a CAGR of 6.4% during the forecast period from 2025 to 2032.

This growth is fueled by global demand for fuel-efficient vehicles, adoption of advanced driver-assistance systems (ADAS), and sustained ICE vehicle production despite the rise of electric vehicles (EVs).

Key Industry Highlights:

- Leading Region: Asia Pacific, holding over 35% market share in 2025, driven by high vehicle production in China, Japan, and India.

- Fastest-growing Region: North America, fueled by advanced ignition system adoption and aftermarket growth.

- Dominant Engine Type: Gasoline, capturing 55% market share in 2025, due to its prevalence in passenger cars and hybrid vehicles.

- Dominant Ignition Type: Coil on plug (COP) ignition, leading with 52% market share, valued for precision and efficiency.

- Dominant Component: Ignition switch, holding 45% market share, critical for vehicle operation and reliability.

- Dominant Vehicle Type: Passenger cars, with 48% market share, driven by global production volumes.

|

Global Market Attribute |

Key Insights |

|

Automotive Ignition Parts Market Size (2019) |

US$6.3 Bn |

|

Automotive Ignition Parts Market Size (2025E) |

US$9.2 Bn |

|

Market Value Forecast (2032F) |

US$14.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.2% |

Market Dynamics

Driver: Surge in Vehicle Production and Emission Regulations

The demand for fuel-efficient and high-performance vehicles is accelerating due to rising fuel costs, stricter emission regulations, and shifting consumer preferences toward sustainable mobility.

Automakers are increasingly investing in lightweight materials, turbocharged engines, hybrid technology, and electric drivetrains to deliver vehicles that combine fuel economy with superior performance. This trend not only reduces operating costs for consumers but also aligns with global efforts to curb greenhouse gas emissions, making it a critical growth driver in the automotive market.

For instance, the U.S. Department of Transportation (NHTSA) has implemented updated Corporate Average Fuel Economy (CAFE) standards that mandate automakers to achieve a fleetwide average of nearly 49 miles per gallon by 2026.

Similarly, the EPA’s Automotive Trends Report highlights that real-world fuel economy improved to 27.1 mpg in 2023, while CO? Emissions dropped to 319 grams per mile. These government-backed benchmarks illustrate how the growing demand for fuel-efficient cars and high-performance vehicles is reshaping the automotive industry.

Restraint: High Adoption of Electric Vehicles

The adoption of electric vehicles (EVs) faces notable restraints despite the global push for sustainable mobility. One of the biggest barriers is the high upfront cost of EVs, which remains significantly above that of conventional vehicles, limiting affordability for mass consumers.

In addition, the limited charging infrastructure creates range anxiety and makes EV ownership less convenient, particularly in emerging economies and rural areas. Factors such as long charging times, battery degradation, and higher maintenance costs for advanced components further reduce the penetration of the automotive ignition parts market.

Another major restraint is the uneven pace of government incentives and policies, which directly influence consumer adoption rates. While urban markets show faster growth, rural and developing regions lag due to inadequate infrastructure and limited availability of EV models.

These challenges highlight how EV adoption barriers, including cost, infrastructure gaps, and market readiness, continue to restrain the expansion of electric mobility despite strong demand for cleaner transportation.

Opportunity: Hybrid Vehicles and Aftermarket Expansion

The rising popularity of hybrid vehicles presents a strong growth opportunity for the automotive industry. As consumers seek a balance between fuel efficiency and performance, hybrids are increasingly positioned as a practical alternative to both conventional internal combustion engine (ICE) vehicles and fully electric cars.

Their growing adoption creates sustained demand for specialized components such as batteries, electric motors, regenerative braking systems, and power electronics. Automakers and suppliers who focus on innovation in hybrid technology can capture significant market share by offering cost-effective and environmentally friendly solutions.

At the same time, the aftermarket expansion linked to hybrid vehicles represents a lucrative revenue stream. With a growing fleet of hybrids on the road, demand for replacement parts, maintenance services, and performance upgrades is set to increase rapidly. Opportunities exist for companies in aftermarket batteries, advanced spark plugs, sensors, and diagnostic tools, making this segment a crucial driver of long-term profitability and customer retention.

Category-wise Insights

Engine Type Insights

Gasoline-powered vehicles dominate the global automotive ignition parts market, holding a market share of more than 55% worldwide. Their strong presence is driven by lower purchase costs, widespread availability of fueling infrastructure, and high demand in the passenger car segment. Gasoline-powered engines remain the preferred choice in both developed and emerging economies, reinforcing their position as the leading fuel type.

In contrast, diesel vehicles are emerging as the fastest-growing segment, particularly in commercial transportation. Known for their superior fuel efficiency, durability, and torque performance, diesel engines are widely adopted in heavy-duty trucks, buses, and industrial vehicles, thereby supporting market growth in the logistics and freight industries.

Ignition Type Insights

Coil-on-Plug (COP) ignition systems currently dominate the global automotive ignition parts market, accounting for around 52% of total market share. This leadership is attributed to their ability to deliver a direct spark to each cylinder, eliminating the need for ignition cables.

COP systems improve fuel efficiency, reduce emissions, and enhance engine reliability, making them the preferred choice for modern gasoline engines. Their widespread adoption is further supported by stricter emission norms and the industry’s push toward high-performance, compact engine designs.

In contrast, Simultaneous Ignition systems are emerging as a fast-growing technology segment. These systems ignite multiple cylinders simultaneously, enhancing combustion stability and overall performance in specific engine applications. Although their current share is comparatively smaller, advancements in high-performance vehicles and emission-compliant engine technologies are expected to accelerate the adoption of simultaneous ignition systems in the years to come.

Component Insights

Within ignition system components, the ignition switch dominates the automotive ignition parts market, accounting for nearly 45% of the overall share. Its critical role in powering the ignition coil, starter, and other electronic systems makes it an indispensable part of both passenger and commercial vehicles. The rising production of vehicles and the demand for advanced safety and ignition features continue to reinforce the ignition switch’s leadership in the component segment.

In comparison, the Spark Plug segment also holds a significant position, driven by its function in igniting the air-fuel mixture and ensuring efficient combustion. With innovations such as iridium and platinum spark plugs that enhance durability and fuel efficiency, this component remains a rapidly evolving part of the automotive ignition system market.

Vehicle Type Insights

Passenger Cars dominate the ignition system market, holding approximately 48% of the total market share. High global production volumes, strong consumer demand, and the rising preference for fuel-efficient, low-emission gasoline vehicles drive this growth.

Passenger cars widely integrate advanced ignition technologies such as coil-on-plug systems and iridium spark plugs, which enhance performance, reduce emissions, and comply with increasingly strict government regulations. This makes them the leading vehicle type in the ignition system market.

On the other hand, Commercial Vehicles represent the fastest-growing segment, supported by rising demand in logistics, construction, and long-haul transportation. The need for durable and efficient ignition systems in trucks, buses, and heavy-duty vehicles fuels this growth. With the expansion of e-commerce, infrastructure development, and global trade, the adoption of advanced ignition technologies in commercial fleets is expected to accelerate significantly over the forecast period.

Regional Insights

North America Automotive Ignition Parts Market Trends

North America is emerging as the fastest-growing market. The growth is supported by strong demand for high-performance vehicles, SUVs, and light trucks, coupled with a rising shift toward fuel-efficient and low-emission technologies. Automakers in the U.S. and Canada are increasingly integrating advanced ignition systems, such as coil-on-plug and multi-spark technologies, to comply with stringent emission regulations set by organizations like the EPA and NHTSA.

In addition, the region’s well-established automotive aftermarket and consumer preference for premium vehicles are accelerating the adoption of advanced ignition components such as iridium spark plugs, ignition coils, and automotive sensors. With continuous technological advancements and the increasing adoption of hybrid and gasoline vehicles, North America is expected to experience the highest growth rate in the ignition system market over the forecast period.

Europe Automotive Ignition Parts Market Trends

Europe plays a vital role in the global automotive ignition system market, driven by its strong base of leading automakers and strict environmental regulations. Countries such as Germany, France, and the UK are at the forefront of adopting advanced ignition technologies to meet Euro 6 and upcoming Euro 7 emission standards. The region’s focus on reducing carbon emissions and improving fuel efficiency has accelerated the integration of coil-on-plug ignition systems, advanced spark plugs, and electronic ignition controls.

Additionally, Europe is a hub for luxury and premium vehicles, where demand for high-performance engines drives the growth of innovative ignition solutions. Continuous R&D investments by OEMs and component manufacturers, along with the rising adoption of hybrid powertrains, reinforce Europe’s role as a key contributor to technological advancements and market expansion in the global ignition system industry.

Asia Pacific Automotive Ignition Parts Market Trends

Asia Pacific holds the largest share of the automotive ignition system market, accounting for over 35% of the global market share. This dominance is fueled by the region’s massive vehicle production base, strong consumer demand for passenger cars, and rapid industrialization in countries such as China, India, Japan, and South Korea. Additionally, government initiatives promoting fuel-efficient technologies and stricter emission standards further boost the adoption of advanced ignition systems in the region.

The region also benefits from the presence of leading automotive OEMs and component manufacturers, making it a hub for innovation and cost-effective production. Growing disposable incomes, rising urbanization, and expanding middle-class populations continue to drive vehicle ownership, reinforcing Asia Pacific’s leadership in the global ignition system market.

Competitive Landscape

The global automotive ignition parts market is moderately consolidated, with competition centered on technological innovation and compliance with emission regulations. Manufacturers are increasingly focusing on coil-on-plug systems, advanced spark plugs, and electronic ignition modules to enhance fuel efficiency and engine performance.

Growth is further supported by the expansion of the aftermarket segment and the rising adoption of hybrid and fuel-efficient vehicles across major automotive regions.

Key Developments

- November 2024: Diamond & Zebra Electric launched a revolutionary hydrogen engine ignition coil prototype featuring advanced pre-ignition control and superior high-voltage output technology. Sample evaluation orders began in October 2024, marking a breakthrough solution that addresses hydrogen's unique combustion properties to enable the development of zero-carbon engines amid rising climate concerns.

- December 2024: onsemi and DENSO Corporation strengthened their strategic alliance to accelerate the development of autonomous driving and ADAS technologies. Onsemi's intelligent sensor technologies enhance ignition system performance and vehicle connectivity solutions, driving improved safety outcomes and reduced traffic fatalities while securing reliable supply chains for next-generation automotive applications.

Companies Covered in Automotive Ignition Parts Market

- BorgWarner Inc.

- Continental AG (Schaeffler Group)

- Denso Corporation

- Diamond Electric Mfg. Co. Ltd.

- Federal-Mogul Corporation (Tenneco Inc.)

- Hitachi Ltd.

- Mitsubishi Electric Corporation

- NGK Spark Plug Co. Ltd.

- Robert Bosch GmbH

- Valeo

- Others

Frequently Asked Questions

The automotive ignition parts market is projected to reach US$ 9.2 Bn in 2025.

Rising vehicle production, emission regulations, and hybrid vehicle growth are key drivers.

The automotive ignition parts market is expected to grow at a CAGR of 6.4% from 2025 to 2032.

Hybrid vehicle advancements and aftermarket expansion offer significant potential.

Leading players include BorgWarner Inc., Denso Corporation, NGK Spark Plug Co. Ltd., and Robert Bosch GmbH.