- Automotive Components & Materials

- Automotive Flanges Market

Automotive Flanges Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Flanges Market By Product Type (Welding Neck, Slip-On, Others), Material (Carbon Steel, Stainless Steel, Aluminum, Others), End-user (Automotive, Aviation and Aerospace, Petrochemicals and Chemicals, Others), and Regional Analysis for 2026 - 2033

Automotive Flanges Market Size and Trends Analysis

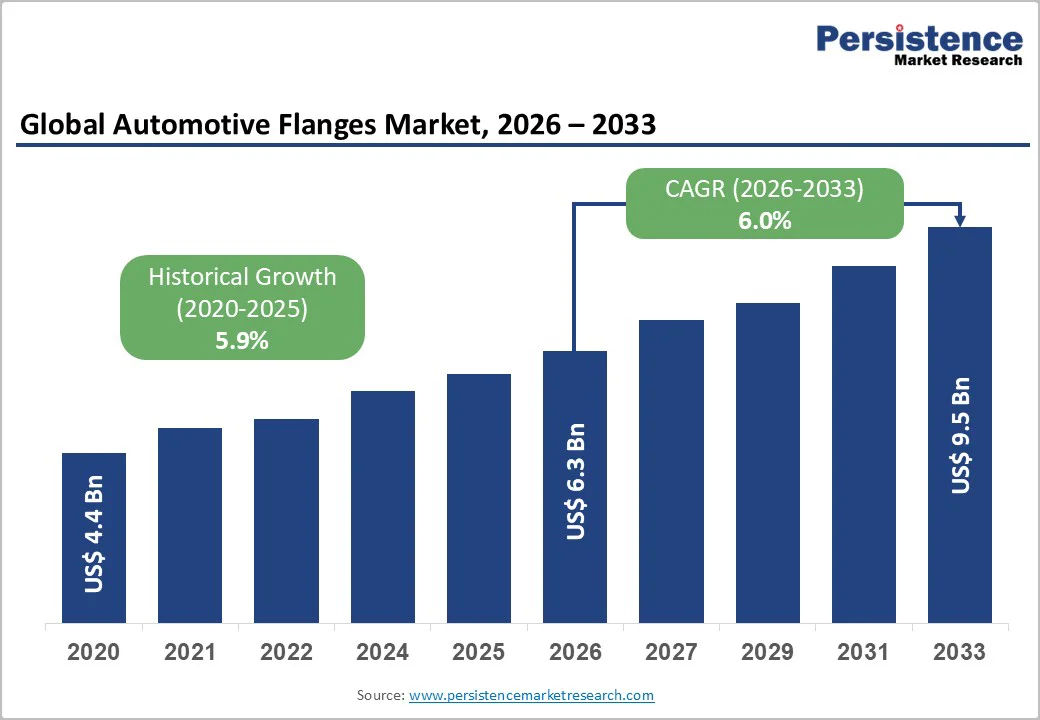

The global automotive flanges market size is likely to be valued at US$6.3 billion in 2026 and is expected to reach US$9.5 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by consistent demand from vehicle manufacturing, aftermarket replacements, and advancements in lightweight automotive material technologies.

Rapid growth in automotive production, especially in the Asia-Pacific region, continues to drive demand for exhaust, engine, powertrain, and chassis flanges. The rising penetration of electric and hybrid vehicles is reshaping component requirements.

Key Industry Highlights:

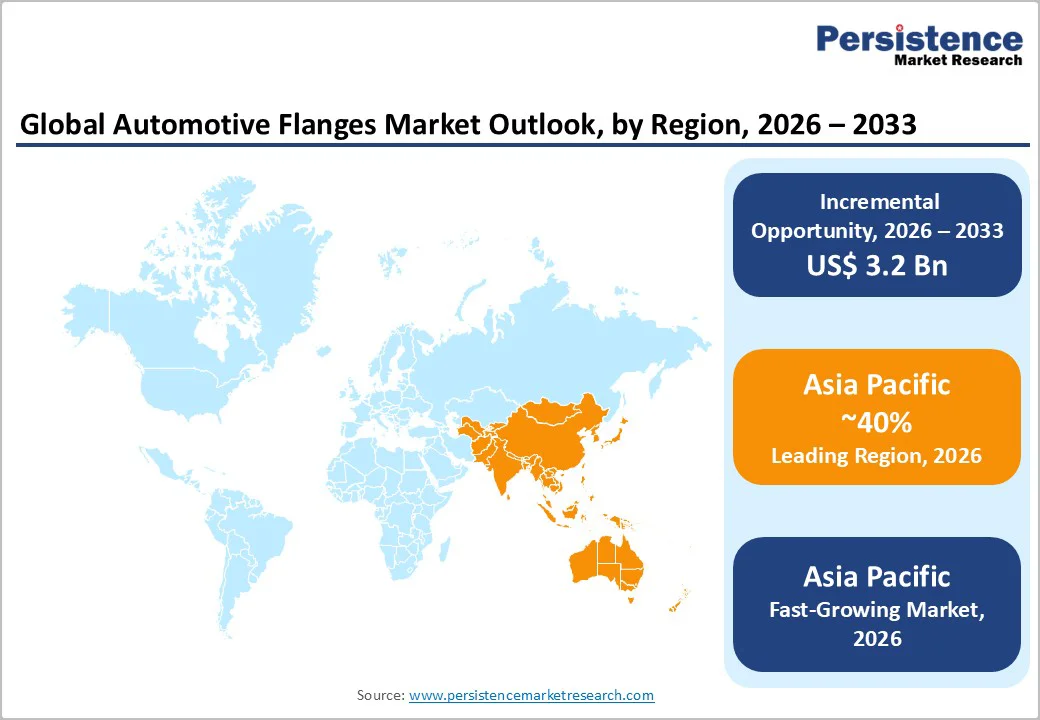

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by high vehicle production volumes, cost-competitive manufacturing, and robust demand for precision-engineered automotive components.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the automotive flanges market in 2026, driven by rapid automotive manufacturing expansion and rising demand for EV components.

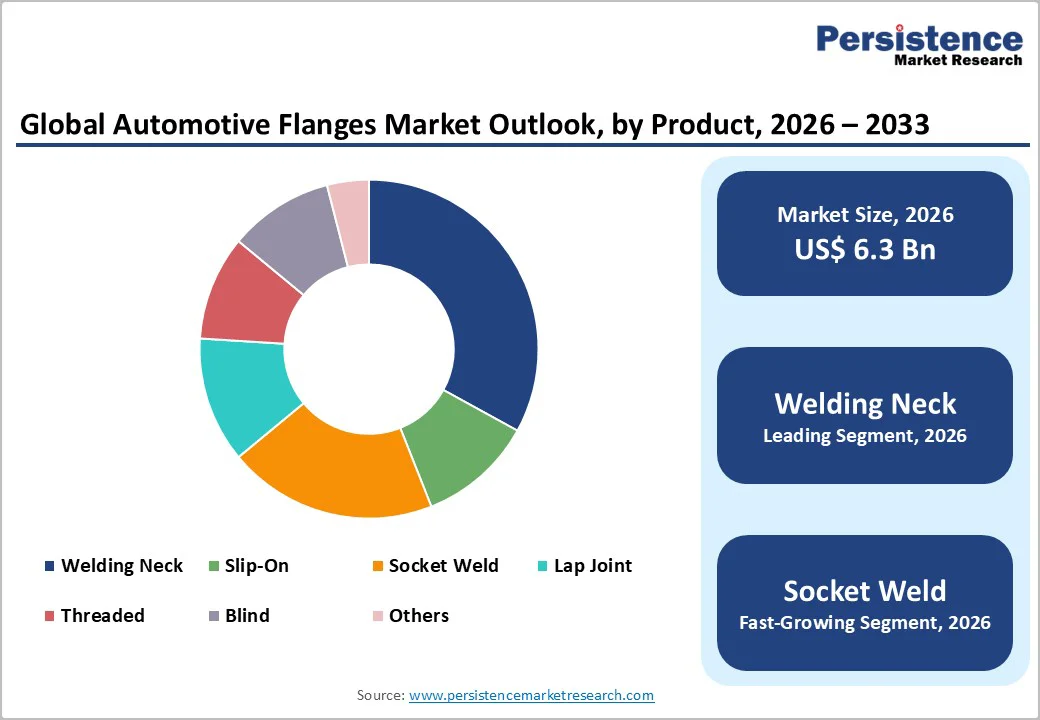

- Leading Product Type: The welding neck segment is projected to lead in 2026, accounting for 38% of the market, driven by its superior strength, leak-proof performance, and suitability for high-pressure automotive exhaust and engine applications.

- Leading Material Type: Carbon steel is expected to lead, accounting for over 42% of revenue share in 2026, supported by its cost-effectiveness, durability, and widespread use in chassis, engine, and structural automotive applications.

- Leading End-user: The automotive segment is expected to lead, contributing 28% of total revenue, driven by high global vehicle production volumes and consistent demand for exhaust, powertrain, and structural flange components.

| Key Insights | Details |

|---|---|

| Automotive Flanges Market Size (2026E) | US$6.3 Bn |

| Market Value Forecast (2033F) | US$9.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Automotive Production and EV Transition

Vehicle manufacturing continues to expand, especially in the Asia-Pacific region, where China, India, Japan, and ASEAN collectively account for a major share of global output. Higher production volumes directly increase the consumption of exhaust flanges, engine flanges, powertrain connectors, and chassis-mounted flange assemblies.

OEMs increasingly rely on precision-engineered flange components to ensure durability, vibration resistance, and thermal stability in both passenger and commercial vehicles.

The transition toward electric vehicles (EVs) is reshaping the flange application landscape rather than reducing demand. EVs require a different set of precision flanges for battery cooling loops, thermal management modules, HVAC connections, inverter housings, e-motor assemblies, and lightweight structural interfaces.

The shift to electrification increases the use of stainless steel, aluminum, and polymer-based flanges due to the need for corrosion resistance, weight reduction, and high thermal efficiency.

Raw Material Price Volatility

Raw material price volatility is a significant restraint in the market, as carbon steel, stainless steel, aluminum, and alloy materials account for the majority of production costs. Frequent fluctuations in metal prices driven by supply chain disruptions, geopolitical tensions, and energy cost spikes directly affect manufacturing budgets and squeeze profit margins for OEMs and component suppliers.

As flanges require precision forging, machining, and high-grade metals, even small price shifts can substantially increase overall production costs.

The volatility especially impacts small and mid-sized flange manufacturers, who often lack long-term fixed-price contracts and depend on spot market purchases. As a result, they face inconsistent production planning, reduced cost predictability, and weaker competitive positioning against large integrated suppliers.

Sudden price hikes also limit automakers' ability to maintain stable procurement costs, leading to delays in order cycles and reluctance to adopt advanced or premium-material flange solutions.

EVs and Hybrid Powertrain Expansion

The shift toward EVs and hybrid powertrains presents a significant growth opportunity for the automotive flanges market. While traditional internal combustion engine (ICE) vehicles rely heavily on exhaust, engine, and fuel-line flanges, EVs and hybrids require specialized flanges for battery cooling systems, inverter and e-motor housings, HVAC assemblies, and lightweight structural connections.

This evolution expands the scope of flange applications beyond conventional exhaust and powertrain systems.

Manufacturers can capitalize on this trend by developing high-performance, corrosion-resistant, and lightweight flanges using materials such as stainless steel, aluminum, and engineered polymers. The demand for compact, modular designs that reduce assembly time in EV production further enhances market potential.

As governments worldwide enforce stricter emission targets and incentivize EV adoption, flange suppliers that innovate and adapt to EV- and hybrid-specific requirements are positioned to gain a competitive advantage and capture long-term market growth.

Category-wise Analysis

Product Type Insights

Welding neck flanges are expected to dominate the automotive flanges market, accounting for approximately 38% of total revenue in 2026, primarily due to their superior mechanical strength and reliability in high-pressure applications such as exhaust systems and engine manifolds.

Their high structural integrity allows them to withstand extreme pressure, thermal expansion, and vibration, making them a preferred choice for OEMs adhering to stringent quality and durability standards. For example, Mercedes-Benz uses welding neck flanges in its AMG exhaust manifolds to withstand temperatures above 900°C without deformation.

Welding neck flanges also support high-volume production processes, aligning with the rapid automotive manufacturing output in regions such as the Asia Pacific.

Socket-weld flanges are projected to be the fastest-growing product type in 2026, supported by their compact design, ease of installation, and compatibility with modern EV and hybrid fuel-line architectures. They offer minimal leakage and dependable connections in low- to medium-pressure environments, making them well-suited for thermal management circuits, battery cooling systems, and compact e-motor housings.

For example, a Raised Face (RF) carbon steel socket weld flange is commonly used in small-bore piping, such as 2-inch fluid lines, in industrial and automotive systems. In this setup, the pipe fits into the flange’s socket. It is secured with a fillet weld, creating a strong, leak-resistant joint capable of withstanding moderate pressure and temperature conditions.

Material Type Insights

Carbon steel is projected to lead the market, capturing around 42% of the total revenue share in 2026, driven by its cost-effectiveness, high durability, and versatility across various automotive applications. It is approximately 30% cheaper than stainless steel, yet provides sufficient strength and resistance for high-stress areas such as chassis, engine mounts, and exhaust system supports.

For example, Honda uses carbon steel flanges extensively in its chassis assembly and exhaust mounting systems, where both mechanical reliability and production cost efficiency are critical. The material allows large-scale welding, machining, and surface treatments, ensuring strength, corrosion resistance, and long-term durability.

Stainless steel is expected to be the fastest-growing material type in 2026, driven by rising demand for corrosion-resistant components in humid environments and electric powertrain systems. Its exceptional resistance to rust, chemical exposure, and thermal stress makes it well-suited for exhaust manifolds, battery cooling lines, and inverter housings in hybrid and electric vehicles.

In fuel delivery systems, for instance, stainless steel flanges provide secure, long-lasting connections for fuel lines and tanks. This growth trend is further reinforced by stricter regulations on component durability and environmental resilience, particularly in regions with high humidity or coastal climates.

End-user Insights

The automotive sector is projected to lead the market in 2026, capturing around 28% of revenue, driven by the sheer scale of global vehicle production. Automotive applications encompass exhaust systems, engine manifolds, powertrain connectors, cooling lines, and structural assemblies, all of which require reliable and precision-engineered flanges.

For example, Ford utilizes automotive flanges extensively in exhaust manifolds and engine powertrain assemblies, ensuring tight tolerances, minimal vibration, and extended service life. The continuous expansion of global automotive production, especially in the Asia Pacific, supports the sustained dominance of this end-user segment.

The aviation and aerospace segment is likely to be the fastest-growing end-user category in 2026, driven by the industry’s demand for lightweight, high-strength, and corrosion-resistant flanges to improve fuel efficiency and performance. Aerospace applications include hydraulic systems, fuel lines, engine mounts, and structural assemblies where precision and material integrity are critical.

For example, Boeing and Airbus incorporate stainless steel and aluminum flanges in aircraft hydraulic and fuel systems to meet strict regulatory requirements for safety and longevity. Growth in this segment is accelerated by the rising adoption of composite materials and electrification initiatives in aerospace propulsion and auxiliary systems.

Regional Insights

North America Automotive Flanges Market Trends

North America is likely to be a significant market in 2026, driven primarily by the region’s robust automotive production and modernization of assembly facilities. The U.S., Canada, and Mexico collectively form a strong automotive manufacturing hub, producing millions of passenger and commercial vehicles annually.

Rising demand for lightweight and high-performance components in internal combustion engine (ICE) vehicles has led to increased adoption of carbon steel, stainless steel, and aluminum flanges for exhaust systems, engine manifolds, and powertrain connections. Stringent regulatory standards for emission control, safety, and durability are encouraging manufacturers to adopt high-quality, precision-engineered flanges.

The shift toward electric and hybrid vehicles is creating new opportunities for flange manufacturers. EV and hybrid platforms require flanges for battery cooling systems, inverter housings, thermal management lines, and lightweight structural connections.

Stainless steel and aluminum flanges are gaining traction due to their corrosion resistance and high strength-to-weight ratio. Investments in advanced manufacturing technologies, such as precision forging, automated welding, and high-volume machining, are improving production efficiency while maintaining tight tolerances.

Europe Automotive Flanges Market Trends

Europe is likely to be a significant market owing to the region’s strong automotive manufacturing base, advanced engineering standards, and regulatory compliance requirements. Countries such as Germany, France, Italy, and the U.K. dominate vehicle production, focusing on both passenger and commercial vehicles.

High-quality flanges are essential in exhaust systems, engine manifolds, and powertrain assemblies to meet stringent EU emission and safety standards. Carbon steel and stainless steel flanges remain dominant due to their durability, corrosion resistance, and cost-effectiveness.

Europe is undergoing a transition toward electric and hybrid vehicles, which is reshaping flange applications. EV platforms require flanges for battery thermal management, cooling lines, inverter housings, and lightweight structural connections.

Aluminum and stainless steel flanges are gaining prominence due to their corrosion resistance and high strength-to-weight ratio. Moreover, the adoption of advanced manufacturing technologies such as precision forging, automated welding, and CNC machining supports higher efficiency and consistent quality.

Asia Pacific Automotive Flanges Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a 40% market share in 2026, driven by major automotive manufacturing hubs such as China, India, Japan, and ASEAN countries. The region accounts for a significant share of global vehicle production, including both passenger cars and commercial vehicles.

Rising automotive output, coupled with strong government initiatives such as production-linked incentives (PLI) in India and China’s automotive manufacturing policies, is fueling demand for high-quality flanges used in engine manifolds, exhaust systems, and powertrain assemblies.

The shift toward electric and hybrid vehicles is another major trend driving flange adoption in the region. EVs and hybrid platforms require flanges for battery cooling systems, inverter housings, and compact thermal management lines, often utilizing stainless steel and aluminum for corrosion resistance and high strength-to-weight ratios.

Asia-Pacific manufacturers are increasingly focusing on modular, lightweight, and high-performance flange designs to meet growing electrification and emission-reduction standards.

Competitive Landscape

The global automotive flanges market exhibits a moderately fragmented structure, driven by a mix of large multinational metal-flange manufacturers and many regional or local suppliers, each serving different sectors of the automotive, petrochemical, energy, and infrastructure industries.

As demand spans multiple flange types, such as weld-neck, socket-weld, slip-on, threaded, and blind, and a wide range of materials, including carbon steel, stainless steel, and various alloys, no single company holds a dominant market share.

Instead, the landscape is fragmented, with many firms maintaining small to mid-sized shares, resulting in a diverse and highly competitive industry ecosystem. With key leaders including Outokumpu Oyj, Sandvik AB, AFG Holdings, Inc., Texas Flange, and Viraj Profiles Limited, the market sees competition on multiple fronts.

These players compete through product portfolio breadth, supplying a wide array of flange types and materials to meet varied demands (automotive, oil & gas, industrial pipelines, power generation), technological innovation and quality control, such as advanced forging, precision machining, and corrosion-resistant materials suited for harsh conditions, and geographic reach and supply-chain reliability, enabling them to serve global OEMs and infrastructure projects.

Key Industry Developments:

- In October 2025, Tata Advanced Systems Ltd (TASL) and France-based Safran Aircraft Engines inaugurated a high-precision manufacturing facility at Adibatla, Hyderabad, dedicated to producing complex rotating parts for the next-generation CFM LEAP aircraft engines.

- In March 2025, INTLEF Group launched the world’s first Quick-Connect Flange, introducing a breakthrough hydraulic-locking system that transforms BOP and wellhead connection methods. The innovation enables rapid, tool-free connection between API 6A standard flanges, including wellhead, BOP, and pressure-test flanges, significantly reducing installation time and enhancing operational safety.

Companies Covered in Automotive Flanges Market

- SSI Technologies, Inc.

- AFG Holdings, Inc.

- Coastal Flange, Inc.

- Sandvik AB

- Bonney Forge Corporation

- Hitachi

- Parker Hannifin Corporation

Frequently Asked Questions

The global automotive flanges market is projected to reach US$6.3 billion in 2026.

The automotive flanges market is driven by rising vehicle production, the rapid growth of electric powertrains, and growing demand for durable, leak-proof connection components used in exhaust, cooling, and fuel systems.

The automotive flanges market is expected to grow at a CAGR of 6.0% from 2026 to 2033.

The growing adoption of flanges in EV thermal management systems, increasing demand for lightweight and corrosion-resistant materials, and expanding applications in hybrid powertrains and advanced manufacturing technologies.

SSI Technologies, Inc., Tomken Plastic Technologies, Signal Metal Industries, and Clampco Products, Inc. are the leading players.