- Automotive Components & Materials

- Automotive Bearings Market

Automotive Bearings Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Bearings Market by Product Type (Plain Bearings, Roller Bearings, Deep Grooved Ball Bearings, Others), Application (Wheel Hub, Motor & E-axle (EV Specific), Engine, Transmission & Drivetrain, Steering Systems, Suspension, Others), Vehicle Type, Sales Channel, and Regional Analysis for 2026 - 2033

Automotive Bearings Market Size and Trend Analysis

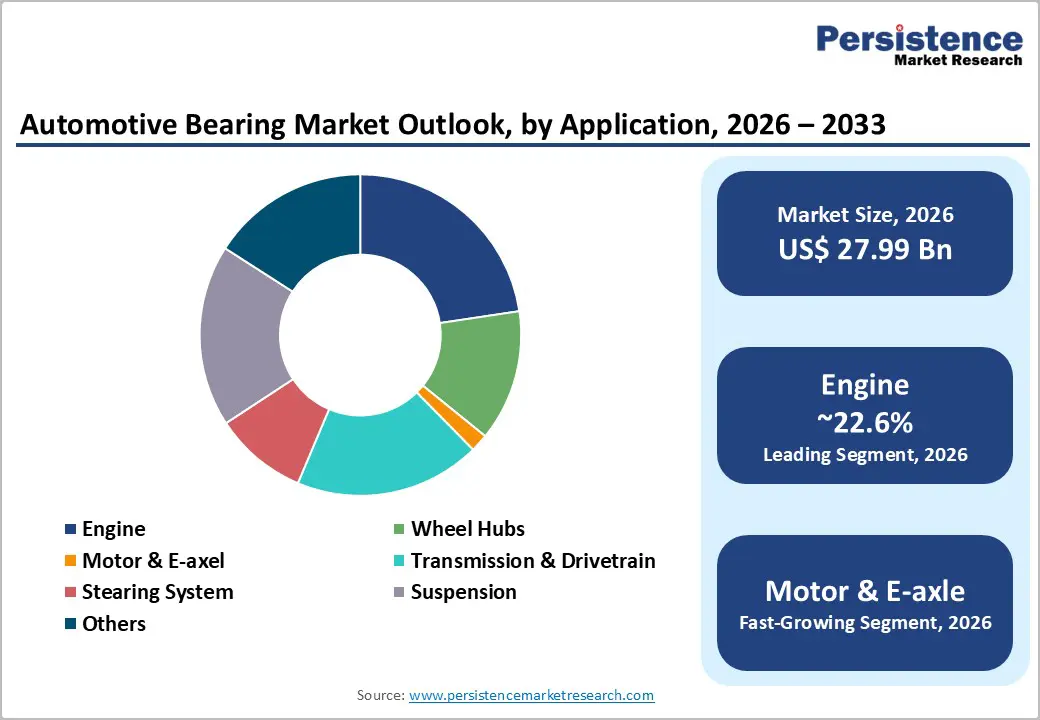

The global Automotive Bearings market size is valued at US$ 28.0 billion in 2026 and is projected to reach US$ 37.5 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033. The market is propelled by a convergence of accelerating electric vehicle adoption, stringent global emission norms, and sustained growth in automotive production across the Asia Pacific.

As EVs require bearings with significantly lower friction coefficients, superior electrical insulation, and enhanced high-speed durability, automotive OEMs are accelerating procurement of precision-engineered bearing assemblies. The structural expansion of the global vehicle aftermarket, driven by an aging parc exceeding 1.4 billion vehicles in operation, further reinforces the market's upward growth trajectory through the forecast period.

Key Industry Highlights:

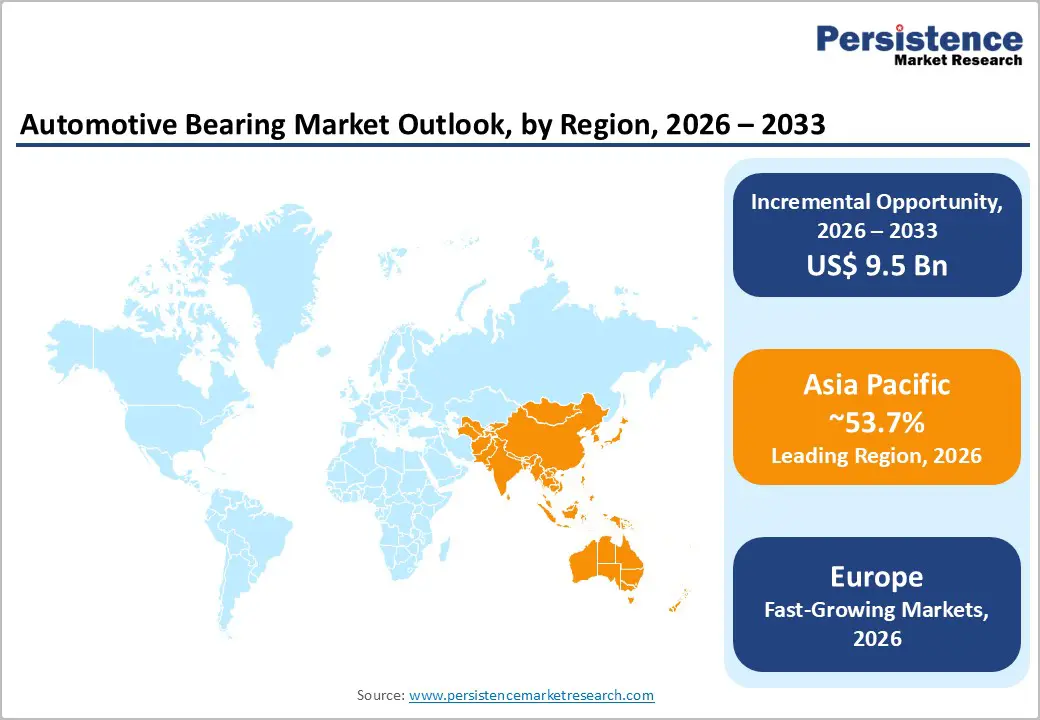

- Leading Region: Asia Pacific leads the global Automotive Bearings market with approximately 53.7% of global revenue share, anchored by China’s massive EV production, Japan’s precision manufacturing capabilities, India’s expanding vehicle parc, and government-backed EV programs across ASEAN nations through 2033.

- Fastest Growing Region: Europe is the fastest growing region, propelled by the European Union’s mandate to phase out new internal combustion engine vehicle sales by 2035, accelerating the adoption of EV-grade bearing technologies.

- Dominant Segment: Roller Bearings represent the leading segment, accounting for approximately 54% of total automotive bearing sales globally.

- Fastest Growing Segment: Motor & E-axle (EV Specific) is the fastest-growing application, expanding at a CAGR approaching 20%, driven by EV powertrain proliferation that requires precision, high-speed, current-insulated bearing assemblies across all passenger and commercial vehicle EV platforms.

- Key Market Opportunity: The Independent Aftermarket (IAM) presents a compelling growth opportunity supported by aging vehicle fleets globally, rapid e-commerce distribution expansion, and rising EV-compatible replacement bearing demand in India and Southeast Asia.

| Key Insights | Details |

|---|---|

|

Automotive Bearings Market Size (2026E) |

US$ 28.0 Bn |

|

Market Value Forecast (2033F) |

US$ 37.5 Bn |

|

Projected Growth CAGR (2026–2033) |

4.3% |

|

Historical Market Growth (2020–2025) |

2.3% |

DRO Analysis

Drivers - Rising Demand for Lightweight and Durable Bearings Driving Material Innovation

The growing emphasis on lightweight and durable automotive components has emerged as a critical driver of innovation in the global automotive bearings market. As vehicle manufacturers prioritize fuel efficiency, emission reduction, and improved performance, there is a clear shift toward lowering vehicle weight without compromising structural integrity. Bearings, as essential components across multiple automotive systems, are central to this transition. Consequently, manufacturers are moving beyond conventional steel toward advanced alloys and alternative materials that offer superior strength-to-weight ratios.

Leading companies, including SKF India, Schaeffler India, and NRB Bearings, are investing significantly in material innovation. For example, SKF’s Hub Bearing Unit integrates ball and tapered roller technologies, delivering reductions in both weight and friction. In addition to weight savings, these advanced materials enhance corrosion resistance, fatigue strength, and operational reliability under demanding conditions, reinforcing their importance in modern automotive design.

Shift Toward High-Precision, Low-Friction Bearings for Electrified Powertrains

The rapid global shift toward vehicle electrification is fundamentally reshaping the performance requirements for automotive bearings. Compared with internal combustion engines, which typically operate at 6,000–8,000 RPM, electric motors routinely reach speeds of 15,000–20,000 RPM, placing substantially higher demands on bearings in terms of centrifugal forces, thermal stress, and compact system integration. These conditions necessitate a new generation of high-precision, low-friction bearings capable of delivering reliable performance over a vehicle’s 10-year service life.

Additional complexity arises from stray electrical currents generated by high-voltage inverter switching, which can damage conventional steel bearings and accelerate wear. The widespread adoption of integrated e-axle architectures further intensifies these requirements, driving demand for advanced sealing, optimized lubrication systems, and precision-engineered bearing solutions. Collectively, these developments indicate that electrification is not only expanding but structurally redefining the automotive bearings market.

Restraints - High Cost of Advanced Bearing Materials and Technologies Limiting Adoption

The high cost of advanced materials, surface coatings, and precision engineering technologies represents a key constraint on the global automotive bearings market. As the industry advances toward electric mobility, high-speed operations, and compact system architectures, demand is rising for bearings manufactured from premium materials such as ceramics, hybrid composites, and high-performance alloys. The incorporation of specialized surface treatments, including diamond-like carbon (DLC) coatings, along with advanced lubrication systems, further elevates production costs.

Although these technologies deliver substantial improvements in efficiency, durability, and operational performance, they also increase unit pricing relative to conventional bearing solutions. This poses challenges in cost-sensitive segments, particularly entry-level vehicles and emerging markets, where affordability remains a primary purchasing criterion. Additionally, the already elevated cost base of electric vehicles intensifies cost pressures, compelling manufacturers to balance innovation with economic viability and slowing large-scale adoption of advanced bearing technologies.

Stringent Performance Requirements in High-Speed EV Applications

The increasing complexity of performance requirements, particularly in high-speed electric vehicle (EV) applications, represents a significant restraint on the automotive bearings market. EV motors operate at very high rotational speeds and are exposed to rapid torque fluctuations, subjecting bearing components to elevated mechanical and thermal stresses. A critical technical challenge is electrical erosion, or electrical pitting, caused by stray currents passing through bearings in high-voltage EV systems, leading to surface damage and reduced service life.

Furthermore, inadequate lubrication, improper installation, or minor misalignments can result in overheating, excessive vibration, and accelerated wear. Bearing failures may lead to reduced vehicle efficiency, costly repairs, warranty claims, and reputational risks for automakers. Addressing these challenges requires significant investment in research, testing, and quality control, increasing development complexity and costs.

Opportunities - Emergence of High-Speed Electric Motors Creating Need for Specialized Bearing Solutions

The accelerating transition toward high-performance electric drivetrains is creating one of the most technically demanding opportunities within the automotive bearings industry. Electric vehicle (EV) motors routinely operate at rotational speeds between 15,000 and 20,000 RPM, subjecting bearings to extreme centrifugal forces that can lead to deformation, increased friction, and premature wear. These operating conditions differ fundamentally from those of conventional internal combustion platforms, prompting extensive industry investment in ultra-high-speed bearing technologies featuring advanced cage designs, specialized lubrication systems, and enhanced thermal management.

Leading manufacturers such as NSK and Schaeffler have introduced next-generation solutions capable of operating at exceptionally high dmN values while providing improved thermal stability and protection against electrical discharge. Higher-speed bearing capability supports increased motor efficiency, reduced system weight, and extended vehicle range, underscoring the premium value and strategic importance of these advanced bearing solutions in next-generation EV platforms.

Growing Aftermarket and Replacement Bearing Demand Fueled by an Aging Global Vehicle Parc

The progressive aging of the global vehicle fleet is generating a resilient and recurring revenue opportunity within the automotive bearings aftermarket. Persistently high new-vehicle prices across major markets have led consumers to extend vehicle service lives, directly increasing the incidence of bearing wear, fatigue, and scheduled replacement. In the United States, total vehicles in operation reached approximately 289 million in 2024, with passenger car and light truck ages averaging 14.5 and 11.9 years, respectively, underscoring prolonged usage cycles.

A similar trend is evident in Europe, where the average passenger car age exceeded 12 years, reflecting sustained affordability pressures. As a result, aftermarket demand is expanding faster than OEM channels, supported by shortened maintenance intervals, predictive maintenance adoption, and the growth of online distribution platforms. Additionally, higher torque loads and vehicle weights in electric vehicles are accelerating bearing wear, further reinforcing long-term replacement demand.

Category-wise Analysis

Product Type Insights

Roller bearings represent the leading segment, accounting for approximately 54% of total automotive bearing volume globally. Roller Bearings, particularly tapered and cylindrical variants, retain a strong application fit in heavy-duty drivetrains and commercial vehicles.

The deep groove ball bearings represent the fastest growing segment, due to their exceptional versatility in handling both radial and axial loads, making them the bearing of choice for automotive motors, wheel hubs, and transmissions. Over 60% of electric vehicles globally rely on DGBBs due to their high-speed efficiency, low friction, and proven durability. The segment has been further elevated by materials innovation, including hybrid ceramic DGBBs that integrate silicon nitride rolling elements with steel rings, offering superior electrical insulation, lower heat generation, and longer service life.

Application Insights

Engine application remains the leading segment within the automotive bearings market, accounting for approximately 22.6% of total demand. Engine-related bearing wear remains a critical maintenance consideration across both passenger and commercial vehicles. This dominance is largely supported by Europe’s extensive vehicle fleet, with more than 240 million vehicles older than five years, which continues to generate strong and sustained aftermarket replacement demand.

Third-generation double-row hub bearing modules with integrated ABS encoder rings are increasingly mandated by OEMs, improving safety system integration. Motor & E-axle (EV Specific) is the fastest-growing application sub-segment, expanding at a CAGR of approximately 20%, driven by global EV platform proliferation and the shift to high-speed precision bearing assemblies.

Vehicle Type Insights

The passenger vehicle segment is leading, representing approximately 49% of total automotive bearing demand by value. OICA data records global passenger car production in excess of 67 million units in 2023, making passenger vehicles the largest volume category by far. The increasing penetration of battery electric passenger vehicles within this segment amplifies bearing content per vehicle, as EV platforms require specialized bearings in e-axles, motors, and transmission systems. Rising ADAS penetration in compact crossovers and battery SUVs further increases average bearing value per unit.

The Electric Vehicles sub-segment is the fastest-growing vehicle category within automotive bearings, growing at a CAGR of approximately 19.1% through the forecast period, significantly outpacing the broader ICE passenger vehicle category. Two- and Three-Wheelers represent a structurally important volume segment in India and Southeast Asia, supporting regional aftermarket demand.

Sales Channel Insights

The OEM (Original Equipment Manufacturers) channel dominates the Automotive Bearings market, accounting for approximately 63.9% of global unit shipments, as every new vehicle rolls off the assembly line pre-equipped with bearings. Long-term platform development partnerships give leading suppliers such as Schaeffler AG, SKF AB, and NSK Ltd. volume certainty and co-engineering influence, creating significant switching barriers.

However, the Independent Aftermarket (IAM) channel is growing at a significant rate, driven by aging vehicle fleets, e-commerce expansion, and broadening vehicle service infrastructure in developing markets. The OES (Original Equipment Suppliers) channel supplies OEM-specification replacement bearings through authorized dealer networks, offering a quality-assured alternative to the independent aftermarket for premium vehicle owners.

Regional Insights

North America Automotive Bearings Market Trends

North America represents a strategically significant market for automotive bearings, supported by the United States’ robust original equipment manufacturing (OEM) ecosystem, which includes General Motors, Ford Motor Company, Stellantis, and electric vehicle-focused manufacturers such as Tesla and Rivian Automotive. Federal policy initiatives, notably the Inflation Reduction Act (IRA), provide substantial incentives for domestic electric vehicle production and component localization, thereby reinforcing demand for high-specification, locally manufactured bearing assemblies.

The region’s aftermarket is further strengthened by an extensive vehicle parc of approximately 290 million registered vehicles. Ongoing compliance with CAFE standards and EPA emission regulations continues to drive OEM adoption of fuel-efficient and electrified platforms. Additionally, the increasing integration of advanced driver-assistance systems (ADAS) is raising bearing content per vehicle, supporting sustained market growth.

Europe Automotive Bearings Market Trends

Europe remains at the forefront of global automotive electrification policy, with the European Union’s mandate to phase out new internal combustion engine vehicle sales by 2035 accelerating the adoption of EV-grade bearing technologies. Germany leads the regional market, accounting for nearly 30% of Europe’s ball bearing demand, supported by strong automotive production and rapid EV penetration. According to the German Association of the Automotive Industry (VDA), vehicle production in Germany exceeded 3.3 million units in 2023, including more than 700,000 electric vehicles, reflecting robust growth momentum.

In May 2024, Schaeffler AG further strengthened the region’s innovation ecosystem by establishing a dedicated center for electrified powertrain bearing and sealing technologies. Across France, the United Kingdom, Spain, and Italy, harmonized Euro 6 and Euro 7 emission standards ensure stable OEM demand, while the U.K.’s planned 2035 ban on new petrol and diesel vehicles is driving EV-compatible aftermarket bearing uptake.

Asia Pacific Automotive Bearings Market Trends

Asia Pacific dominates the global automotive bearings market, accounting for approximately 53.7% of global market share, supported by its extensive manufacturing base and strong automotive production ecosystem. The region is anchored by China, Japan, India, and South Korea, which collectively produce nearly 60% of global bearing volume. China remains the world’s largest electric vehicle market, underpinned by sustained government incentives and a rapidly expanding charging infrastructure.

Japan continues to play a critical role through globally leading bearing manufacturers, including NSK Ltd., NTN Corporation, JTEKT Corp., and Nachi-Fujikoshi Corp., whose precision manufacturing capabilities support advanced EV bearing innovation. India is emerging as a high-growth market, driven by rising vehicle production and the government’s FAME II scheme accelerating electric mobility adoption.

Competitive Landscape

The global automotive bearings market exhibits a moderately consolidated structure, with leading players, Schaeffler AG, SKF AB, NSK Ltd., NTN Corporation, JTEKT Corp., and The Timken Company, commanding significant revenue through deep OEM relationships and proprietary technologies. Market leaders are differentiating through ceramic hybrid bearings, current-insulated EV designs, and smart sensor-embedded bearing units enabling predictive maintenance. Strategic acquisitions, such as Timken’s acquisition of GGB Bearings in November 2022, and OEM co-engineering partnerships are reshaping competitive positioning. Emerging Asian producers continue to intensify competition in cost-sensitive aftermarket and mid-market vehicle segments.

Key Developments:

- March 2026: The Timken Company, a global technology leader in engineered bearings and industrial motion, has acquired the assets and related businesses of North Carolina-based Bijur Delimon International (BDI), a leading global designer and manufacturer of automated lubrication systems.

- October 2025: Tenneco proudly introduces GLYCODUR® NEO, its latest bearing solution featuring GLYCO 692, a groundbreaking, PFAS-free material engineered to meet the growing demand for sustainable, high-performance sliding solutions. Designed for both dry and lubricated use, GLYCODUR® NEO with GLYCO 692 sets a new benchmark in tribological performance, safety and versatility.

- September 2025: NSK Ltd. established new business models that co-create value with its customers throughout the entire product lifecycle, from maintenance and repair of facilities that utilize its products through to disposal, in its efforts to realize a carbon-neutral society. As part of this initiative, NSK has launched a verification program to promote the reconditioning and reuse of bearings using its proprietary diagnostic technologies.

Top Companies in Automotive Bearings

Schaeffler AG (Herzogenaurach, Germany) is one of the world’s largest bearing and automotive component manufacturers. In 2024, the group reported total revenue of approximately €18.2 billion, with its Bearings & Industrial Solutions division contributing €6.57 billion. Its Automotive Technologies division recorded over €4.4 billion in e-Mobility order intake, demonstrating a deep strategic pivot toward electrification. Schaeffler holds an extensive patent portfolio covering EV-specific bearing technologies, including current-insulated and ceramic hybrid designs.

SKF AB (Gothenburg, Sweden) is a global leader in bearings, seals, and lubrication with annual revenues of approximately US$ 9.3 billion in 2024. The automotive segment represents approximately 29.6% of net sales. Across 77 production sites in over 40 countries, SKF maintains broad OEM coverage. The company launched the Infinium bearing series in 2024 and actively co-develops EV sealing and bearing solutions with leading European automakers, reinforcing its technology leadership and sustainability positioning.

NSK Ltd. (Tokyo, Japan) is a global bearing industry leader with a clear strategic focus on EV applications. The company has set a target of JPY 20 billion in EV bearing sales by 2026 through global OEM adoption. Recent innovations include a hub unit bearing with 40% friction reduction, a compact e-axle bearing delivering 25% lower friction, and a 2.2 kg vehicle weight reduction. NSK operates an expanded R&D center in China covering approximately 21,000 m², underscoring its commitment to the world’s largest EV market.

Companies Covered in Automotive Bearings Market

- Schaeffler AG

- NTN Corporation

- SKF AB

- Regal Rexnord Corporation

- The Timken Company

- NSK Ltd.

- JTEKT Corp.

- THK Co., Ltd.

- Minebea Mitsumi Inc.

- Nachi-Fujikoshi Corp.

- RBC Bearings Incorporated

- Wafangdian Bearing Group Corporation Limited

- Tenneco Inc.

- Nippon Thompson

Frequently Asked Questions

The global Automotive Bearings market is valued at approximately US$ 28.0 Bn in 2026 and is projected to reach US$ 37.5 Bn by 2033, growing at a CAGR of 4.3% during the forecast period. Historically, the market grew at a CAGR of 2.3% between 2020 and 2025 from a base of US$ 24.4 Bn. The acceleration in the forecast CAGR is primarily attributable to EV platform proliferation, rising global vehicle production, and robust aftermarket expansion.

The leading demand drivers are accelerating global EV adoption, with IEA data showing 17.1 million EV units sold in 2024, up 25% year-on-year, combined with stringent emission regulations across Europe, North America, and Asia. EVs require up to 15 specialized bearings per powertrain, far more than conventional ICE vehicles, driving premium-value bearing procurement from major OEMs and suppliers across all key markets.

The Roller Bearings segment leads the Product Type category with approximately 54% of total bearing value. Roller Bearings, particularly tapered and cylindrical variants, retain a strong application fit in heavy-duty drivetrains and commercial vehicles.

Asia Pacific leads globally, accounting for approximately 54% of global automotive bearing revenue. The region benefits from a concentration of vehicle manufacturing, with China, Japan, India, and South Korea producing nearly 60% of global bearing volume, backed by strong government EV incentives and the presence of globally dominant bearing manufacturers, including NSK Ltd., NTN Corporation, JTEKT Corp., and Nachi-Fujikoshi Corp.

The most compelling opportunity lies in the Motor & E-axle (EV-specific) bearing segment, growing at a CAGR approaching 20%. Concurrently, the Independent Aftermarket (IAM) offers strong upside potential as aging global vehicle fleets, e-commerce distribution expansion, and rising EV-compatible replacement bearing demand in India, Latin America, and Southeast Asia drive structural aftermarket growth.