- Smart Packaging

- Automated Poly Bagging Machines Market

Automated Poly Bagging Machines Market Size, Share, and Growth Forecast, 2026 - 2033

Automated Poly Bagging Machines Market by Machine Type (Horizontal Bagging Machines, Vertical Bagging Machines), Automation Level (Fully Automated, Semi-Automated, Others), Capacity, End-Use Industry, and Regional Analysis for 2026 - 2033

Automated Poly Bagging Machines Market Size and Trends Analysis

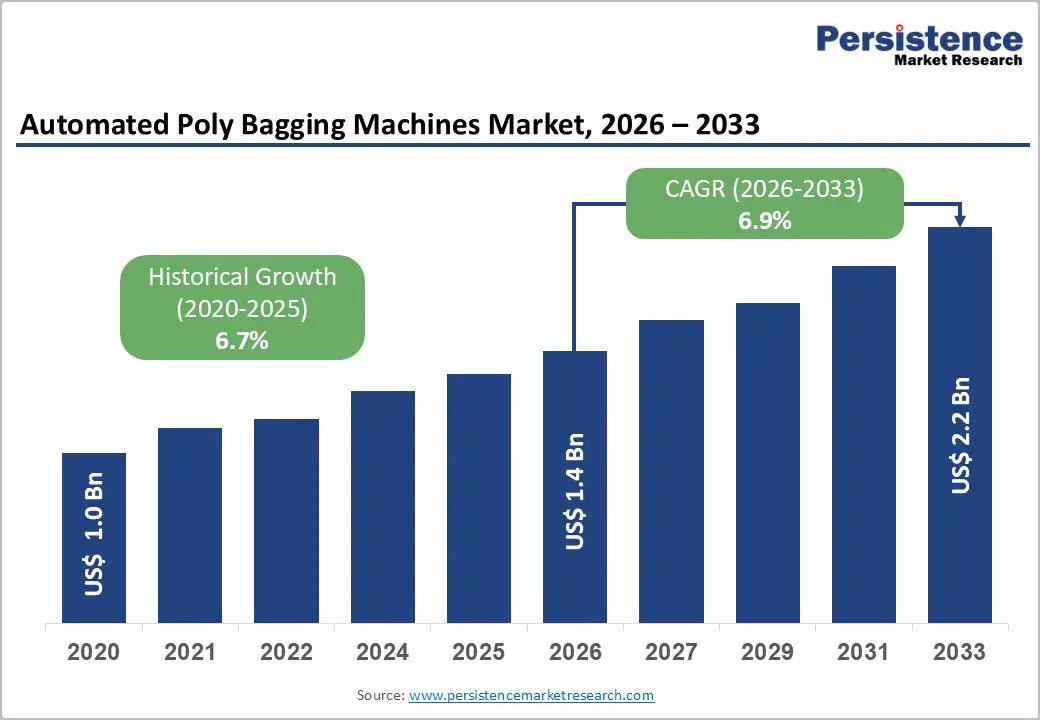

The global automated poly bagging machines market size is likely to be valued at US$1.4 billion in 2026 and is expected to reach US$2.2 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033, driven by the rapid expansion of e-commerce fulfillment operations, modernization of food and beverage packaging lines, and increasing automation adoption to mitigate labor shortages and rising wage pressures.

Market growth reflects a shift toward high-throughput, digitally integrated bagging systems that improve OEE, enhance traceability, and reduce manual handling. Companies are prioritizing scalable, flexible platforms that manage diverse SKUs with minimal changeover time. While high capital costs and supply chain volatility constrain adoption, particularly in price-sensitive segments, modular designs, leasing options, and lifecycle service models are reducing these barriers. As a result, adoption is accelerating among small- and mid-sized enterprises and expanding across emerging markets.

Key Industry Highlights:

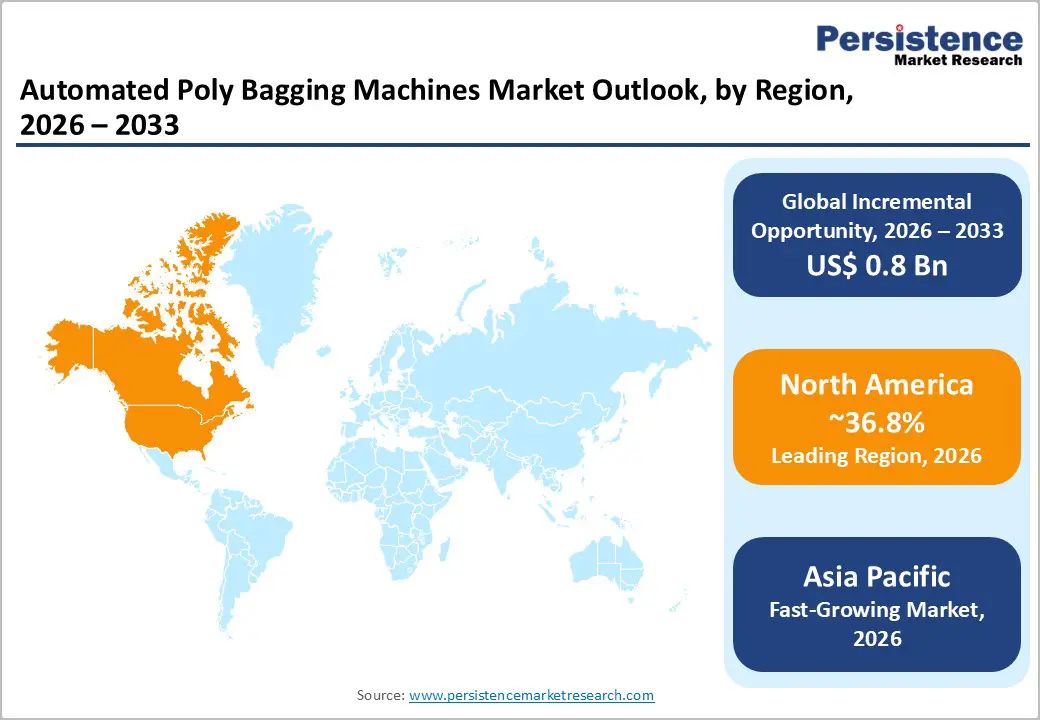

- Leading Region: North America is projected to account for over 36.8% of market share in 2026, driven by U.S.-led automation investments, high labor costs, strong e-commerce infrastructure, and regulatory compliance requirements under the FDA and FSMA frameworks.

- Fastest-growing Region: Asia Pacific, projected to record the highest CAGR through 2033, supported by industrial expansion in China and India, rising automation adoption in ASEAN, and rapid e-commerce growth across major regional platforms.

- Investment Plans: OEMs are prioritizing IIoT-enabled systems, predictive maintenance services, localized manufacturing hubs, and modular automation platforms, particularly in North America and Asia Pacific, to reduce lead times and strengthen lifecycle service revenue streams.

- Dominant Machine Type: Horizontal bagging machines are expected to hold 57.2% market share in 2026, driven by strong adoption in high-throughput food, confectionery, and e-commerce packaging lines that require modular integration and consistent feed orientation.

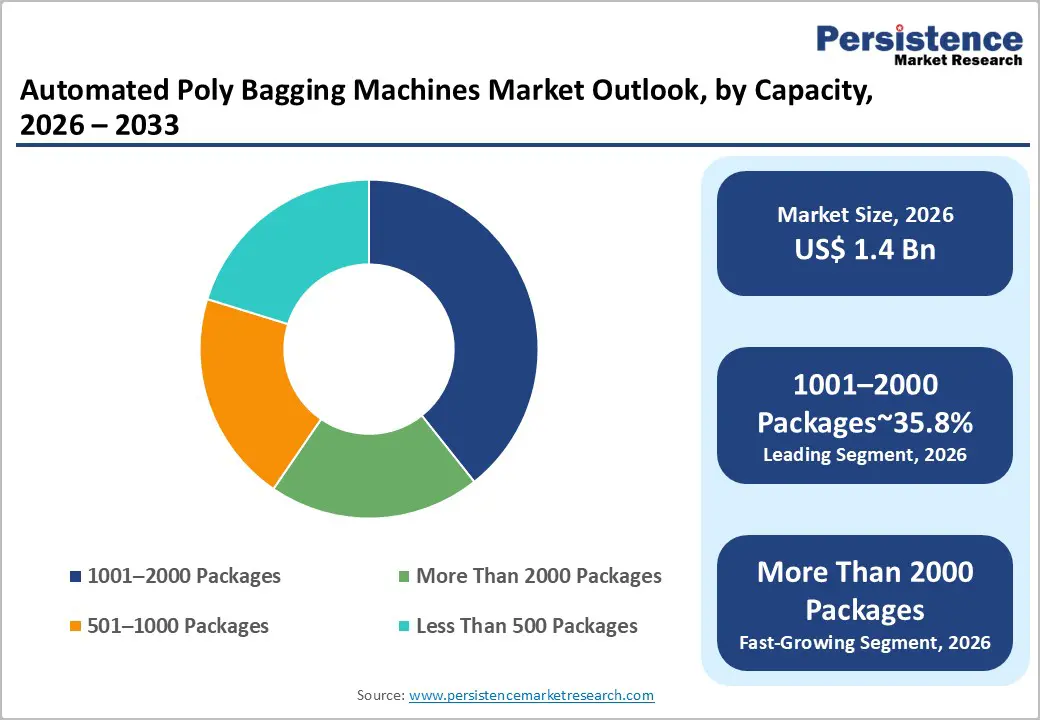

- Leading Capacity: 1001 to 2000 Packages per Hour, representing an anticipated 35.8% market share, as medium-to-large processors favor this range for balancing throughput efficiency, changeover flexibility, and multi-shift operational reliability.

| Key Insights | Details |

|---|---|

| Automated Poly Bagging Machines Market Size (2026E) | US$1.4 Bn |

| Market Value Forecast (2033F) | US$2.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of E-Commerce and Modern Retail Infrastructure

Global e-commerce continues to expand as digital penetration, urbanization, and consumer demand for rapid delivery drive investments in fulfillment centers. According to multilateral trade and logistics agencies, global parcel volumes have grown at a consistent annual rate in the high single digits, with emerging Asia and North America leading in growth. Fulfillment centers increasingly require high-speed automated bagging systems capable of handling diverse SKUs with minimal downtime. Automated poly bagging machines support throughput targets exceeding 2,000 packages per hour, reduce manual labor hours by up to 20-40% on pack lines, and improve order accuracy. As same-day and next-day delivery models become standard, retailers and third-party logistics providers invest in integrated bagging, labeling, and inspection solutions. This structural shift is transforming bagging from a peripheral operation into a strategic investment in automation.

Technology Convergence and Industry 4.0 Integration

Advancements in servo drives, programmable logic controllers, vision systems, and Industrial Internet of Things (IIoT) connectivity are increasing machine precision, flexibility, and predictive maintenance capability. Servo-driven changeover systems can reduce downtime during SKU transitions by as much as 50-60%, based on benchmark manufacturing case studies. Integrated inspection systems reduce rejection rates and improve quality compliance. Real-time telemetry enables predictive maintenance, lowering unplanned downtime and enhancing OEE. Automated poly bagging machines are increasingly embedded within plant-level Manufacturing Execution Systems (MES), enabling digital traceability and performance analytics. This integration aligns with Industry 4.0 initiatives supported by manufacturing modernization programs in North America, Europe, and parts of Asia Pacific.

Strengthening Food Safety and Traceability Regulations

Food and pharmaceutical regulatory frameworks emphasize traceability, hygiene, and tamper evidence. In the U.S., food safety modernization policies require preventive controls and improved documentation across processing operations. The European Union enforces packaging and hygiene directives requiring validated process controls and material compliance. Automated poly bagging machines that integrate coding, serialization, and inspection systems facilitate compliance with these regulatory mandates. Hygienic design features such as stainless steel frames, washdown capabilities, and sanitary sealing systems are increasingly mandatory in food and healthcare packaging environments. As regulatory audits intensify, processors are replacing legacy equipment with validated automated solutions that provide electronic records and audit-ready documentation, reinforcing demand across regulated industries.

Barrier Analysis - High Capital Expenditure and Extended Payback Periods

Fully automated poly bagging lines require substantial upfront investment, often ranging from tens to several hundred thousand U.S. dollars per installation when integration, inspection, and robotics are included. For small and medium-sized enterprises operating on thin margins, extended payback periods limit adoption. In emerging markets, currency volatility and higher financing costs increase the effective capital burden. As a result, many operators defer full automation and instead adopt semi-automated or retrofitted solutions. Capital intensity remains the most significant structural barrier to widespread penetration.

Supply Chain and Component Dependencies

Automated bagging systems depend on motors, drives, sensors, and electronic components sourced through global supply chains. Disruptions in semiconductor availability, precision components, and industrial metals can extend equipment lead times by 20-40% during constrained periods. OEMs relying on specialized suppliers face single-source risks, increasing project delays. Customers with strict commissioning timelines may postpone automation investments when lead times are uncertain. These supply-side vulnerabilities affect pricing stability and reduce short-term market agility.

Opportunity Analysis - Expansion of Aftermarket Services and Predictive Maintenance

The installed base of automated poly bagging machines represents a growing opportunity for recurring revenue through service contracts, spare parts, and digital monitoring subscriptions. Lifecycle service agreements can generate 15-25% of the original machine value over a five-year period. Predictive maintenance platforms reduce downtime and enhance asset utilization, increasing customer lifetime value. As more facilities digitize operations, service-based revenue models are expected to become a core growth pillar for OEMs.

Emerging Market Penetration via Modular Automation

Rising wages in India, Southeast Asia, and Latin America are accelerating the adoption of mechanization. Modular bagging solutions designed for phased automation reduce entry costs and allow incremental upgrades. Greenfield industrial expansion in these regions creates significant addressable demand. Vendors that offer local assembly, financing structures, and regional service hubs can enhance competitiveness and shorten response times, thereby increasing adoption rates.

Specialized Solutions for Healthcare and Pharmaceuticals

Healthcare and pharmaceutical packaging require cleanroom-compatible systems that support serialization and documentation. Automated poly bagging machines tailored to these environments command premium pricing and longer service contracts. As global pharmaceutical production expands and regulatory scrutiny intensifies, validated bagging systems with traceability integration represent a high-margin niche opportunity within the broader market.

Category-wise Analysis

Machine Type Insights

Horizontal bagging machines lead with an anticipated 57.2% market share in 2026. These systems dominate high-throughput environments such as snacks, confectionery, bakery items, personal care kits, and e-commerce fulfillment applications, where product orientation and sealing consistency are critical. Their modular configuration supports seamless integration with conveyors, case packers, checkweighers, metal detectors, and vision inspection systems. Horizontal designs are particularly preferred for rigid and semi-rigid products that require consistent feed alignment, such as energy bars or multipack consumer goods. Leading OEMs frequently supply turnkey horizontal lines for large food processors and third-party logistics providers, reinforcing their strong installed base. Established supplier ecosystems, standardized spare parts availability, and broad operator familiarity further strengthen their leading market position.

Vertical bagging machines are expected to be the fastest-growing segment. Growth is driven by rising demand for packaging bulk goods, powders, granules, frozen foods, and small hardware components in flexible formats. Vertical form-fill-seal systems offer compact footprints and efficient gravity-fed filling, making them suitable for facilities with space constraints. Applications in rice, pulses, pet food, snack pellets, and industrial fasteners illustrate their versatility. Multi-lane vertical fillers, servo-driven film transport, and advanced multi-head weighing systems are narrowing the throughput gap with horizontal alternatives. These technological upgrades expand vertical machines into higher-speed FMCG and contract packaging operations, accelerating adoption across both developed and emerging markets.

Capacity Insight

The 1001-2000 packages-per-hour segment is expected to lead, with an anticipated 35.8% market share in 2026. This capacity range aligns with medium-to-large processors and contract packers seeking an optimal balance between throughput, flexibility, and capital efficiency. Machines in this segment are widely deployed in snack-processing plants, bakery operations, medical-disposable packaging, and mid-scale e-commerce distribution centers. They are engineered to optimize changeover speed, multi-shift reliability, and integration with MES platforms for performance tracking. OEMs often position this band as the operational “sweet spot,” offering scalable automation options such as robotic infeed or automated case packing without the higher capital burden of ultra-high-speed lines.

The more than 2,000 packages-per-hour segment is likely to be the fastest-growing capacity segment. Rapid e-commerce scaling, subscription-based retail models, and high-volume FMCG production lines are driving demand for ultra-high-speed solutions. These systems are commonly integrated with robotic pick-and-place units, automated palletizers, inline inspection, and real-time quality monitoring. Large snack manufacturers and national fulfillment centers increasingly deploy multi-lane bagging configurations exceeding 2000 packages per hour to manage peak seasonal demand. Investments in servo-driven motion control and synchronized robotics continue to improve uptime and overall equipment effectiveness, reinforcing growth momentum in this high-capacity segment.

Regional Insights

North America Automated Poly Bagging Machines Market Trends - Automation Acceleration Driven by Labor Costs, Regulatory Compliance, and IIoT Integration

North America is projected to account for over 36.8% of market share in 2026, led by the U.S., where high labor costs and persistent workforce shortages continue to accelerate automation investment. Large food processors, contract packers, and major e-commerce operators such as Amazon and Walmart have expanded automated fulfillment and packaging infrastructure, increasing demand for high-speed horizontal and vertical bagging systems integrated with robotics. Regulatory compliance frameworks under the FDA and FSMA guidelines drive procurement of validated, hygienic equipment with serialization and traceability capabilities.

Equipment manufacturers and packaging automation providers have reinforced regional capacity in response to this demand. Companies such as ProMach have expanded their North American packaging solutions portfolio through acquisitions and the integration of end-of-line automation brands, strengthening turnkey offerings for the food and consumer goods sectors. Syntegon and MULTIVAC continue to invest in service infrastructure and digital lifecycle support across the U.S., emphasizing predictive maintenance and remote diagnostics.

Rockwell Automation's partnerships with packaging OEMs further accelerate IIoT integration across bagging lines. These developments enhance uptime, shorten mean time to repair, and position North America as a launch market for advanced automation platforms. OEMs increasingly prioritize localized manufacturing and spare-parts hubs to mitigate supply-chain risks and improve response times, reinforcing the region’s leadership position.

Europe Automated Poly Bagging Machines Market Trends - Sustainability-Led Innovation and Energy-Efficient, CE-Compliant Engineering

Europe maintains strong demand, driven by Germany, the U.K., France, Italy, and Spain. Germany remains a central engineering hub with globally recognized packaging machinery manufacturers such as Syntegon, MULTIVAC, and KHS Group, which continue to develop servo-driven and energy-efficient bagging solutions aligned with EU regulatory standards. Regulatory harmonization under EU packaging, CE marking, and food hygiene directives shapes procurement decisions, often extending evaluation cycles but raising equipment quality benchmarks.

Sustainability mandates under the EU Packaging and Packaging Waste Directive are pushing the adoption of machines compatible with recyclable mono-material films and reduced material usage. For example, several European OEMs have introduced systems optimized for thinner films and recyclable polyethylene structures showcased at trade fairs such as FACHPACK and Interpack. These innovations directly respond to retailer and brand-owner sustainability targets across Western Europe.

In the U.K. and France, strong e-commerce penetration has increased demand for automated fulfillment bagging lines, while Southern European food producers are replacing legacy lines with hygienic, washdown-compatible designs to meet export requirements. Energy-efficient motors, servo systems, and digital performance monitoring are becoming procurement priorities, supporting steady modernization-driven growth across the region.

Asia Pacific Automated Poly Bagging Machines Market Trends - Rapid Industrial Automation Expansion Fueled by E-Commerce and Local Manufacturing Growth

Asia Pacific exhibits the highest growth rate, driven by China, Japan, India, South Korea, and ASEAN economies. Rapid industrial expansion, rising labor costs in urban manufacturing centers, and strong e-commerce growth across platforms such as Alibaba, JD.com, Flipkart, and Shopee are accelerating automation uptake. China hosts a large domestic packaging machinery base, with companies such as Guangdong-based manufacturers and Shanghai-headquartered automation firms scaling production of cost-competitive vertical form-fill-seal and horizontal bagging systems for both domestic and export markets.

Japan continues to emphasize high-precision and regulated-sector automation, with companies such as Ishida introducing advanced weighing and packaging technologies integrated into high-speed bagging systems for snack and pharmaceutical applications. In India, increasing investments in food processing under government-backed manufacturing initiatives have supported the adoption of modular and semi-automated bagging systems, while global OEMs expand local subsidiaries and service operations to improve affordability and after-sales support.

MULTIVAC’s expansion of its Indian technology and digital solutions footprint strengthens regional lifecycle services, reducing downtime and improving technical accessibility. Across ASEAN markets such as Vietnam and Thailand, export-oriented food manufacturing growth is stimulating demand for validated, high-speed systems. Government incentives for industrial modernization and localized assembly partnerships are improving return on investment, reinforcing Asia Pacific’s position as the fastest-growing regional market.

Competitive Landscape

The global automated poly bagging machines market is moderately concentrated. Global OEMs lead high-value turnkey installations, while regional manufacturers compete in price-sensitive segments. North America and Europe favor integrated solutions from established players, whereas Asia Pacific features stronger regional competition.

Leading vendors emphasize product innovation, lifecycle service expansion, and geographic diversification. Differentiation centers on total cost of ownership, integration expertise, regulatory validation support, and digital connectivity. Subscription-based maintenance and modular upgrade pathways are emerging business model trends.

Key Industry Developments:

- In September 2025, Sealed Air Corporation announced the launch of the AUTOBAG® 850HB Hybrid Bagging Machine, a new automated solution designed to run both poly and recyclable paper mailers to improve flexibility and efficiency in fulfillment operations.

- In January 2025, PAC Machinery unveiled its latest “Flexible Sustainability” series of automatic bagging systems at the ProMat Show, featuring new dual-material models such as the Rollbag® R985 and R3200 designed to handle both eco-friendly paper and traditional poly materials.

Companies Covered in Automated Poly Bagging Machines Market

- MULTIVAC Group

- Syntegon Technology

- Ishida Co., Ltd.

- ProMach

- PAC Machinery

- Automated Packaging Systems

- KHS Group

- ULMA Packaging

- Rockwell Automation (packaging integrations)

- Hayssen Flexible Systems

- Viking Masek

- Triangle Package Machinery

- Clamco (LINC Systems)

- Rennco

- American-Newlong

- Tension Packaging & Automation

- Mollers

- Fuji Machinery Co., Ltd.

Frequently Asked Questions

The global automated poly bagging machines market size is projected to be valued at US$1.4 billion in 2026.

The automated poly bagging machines market is expected to reach US$2.2 billion by 2033.

Key trends include rising adoption of fully automated high-throughput systems, increasing integration of IIoT and predictive maintenance technologies, growing demand for sustainable and recyclable packaging compatibility, expansion of robotic end-of-line automation, and modular machine designs enabling phased automation upgrades in emerging markets.

By machine type, horizontal bagging machines lead the market with an anticipated 57.2% share, driven by strong demand in food, confectionery, and e-commerce fulfillment applications requiring consistent product orientation and modular integration.

The automated poly bagging machines market is projected to grow at a CAGR of 6.9% between 2026 and 2033.

Major companies include MULTIVAC Group, Syntegon Technology, ProMach, Ishida Co., Ltd., and ULMA Packaging.