- Technology

- Automated Passenger Counting System Market

Automated Passenger Counting System Market Size, Share, and Growth Forecast 2026 - 2033

Automated Passenger Counting System Market by Component (Hardware; Software; Services), by Transportation Mode (Buses, Railways, Trams/Metro, Ferries, Airlines, Others), by Technology (Infrared, Ultrasonic, Video/Camera based, Time-of-Flight, Thermal Imaging, LiDar based), by End User (Public Transport Authorities, Private Transport Operators, Fleet Management Companies, Infrastructure/Smart City Projects, Airport Authorities), by Regional Analysis, 2026 - 2033

Automated Passenger Counting System Market Size and Trend Analysis

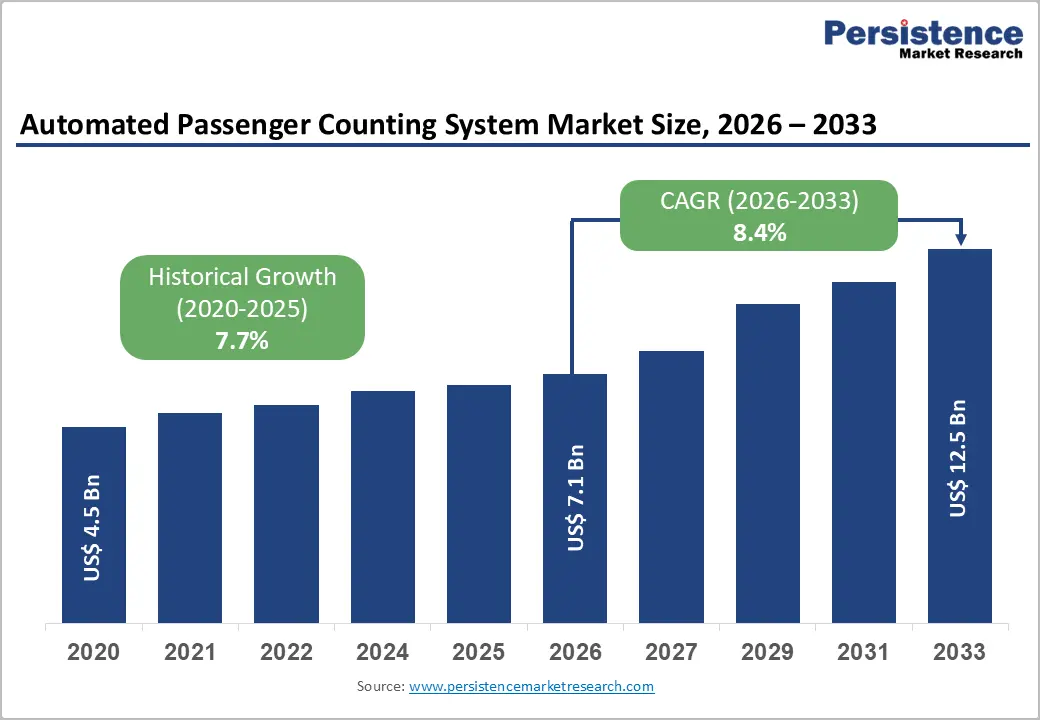

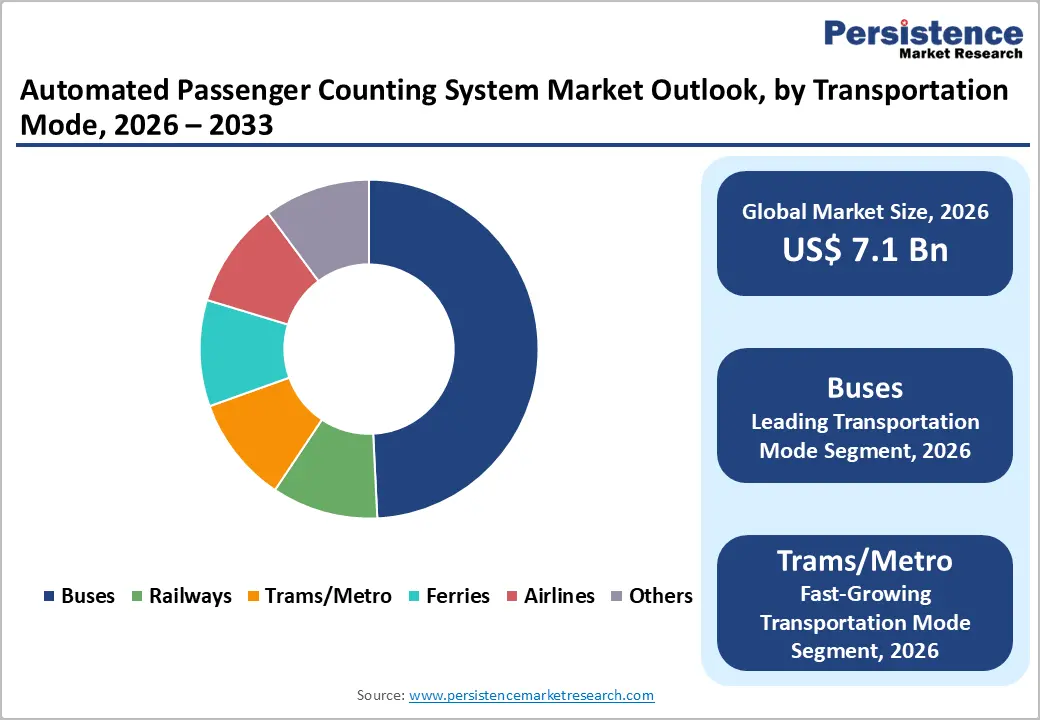

The global automated passenger counting system market size is expected to be valued at US$ 7.1 billion in 2026 and projected to reach US$ 12.5 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033.

The automated passenger counting system market is experiencing robust growth driven by escalating demand for real-time transit data, government investments in smart city infrastructure, and widespread digitalization of public transportation systems globally. Connected public transport represents the #1 IoT use case for smart cities with 74% implementation rate, reflecting unprecedented adoption of automated passenger counting systems supporting operational efficiency and enhanced passenger experiences. Technological advancements including video-based counting systems achieving 98%+ accuracy, AI-powered algorithms, and cloud-based analytics platforms are fundamentally transforming how transit agencies optimize routes, manage resources, and understand passenger mobility patterns.

Key Market Highlights

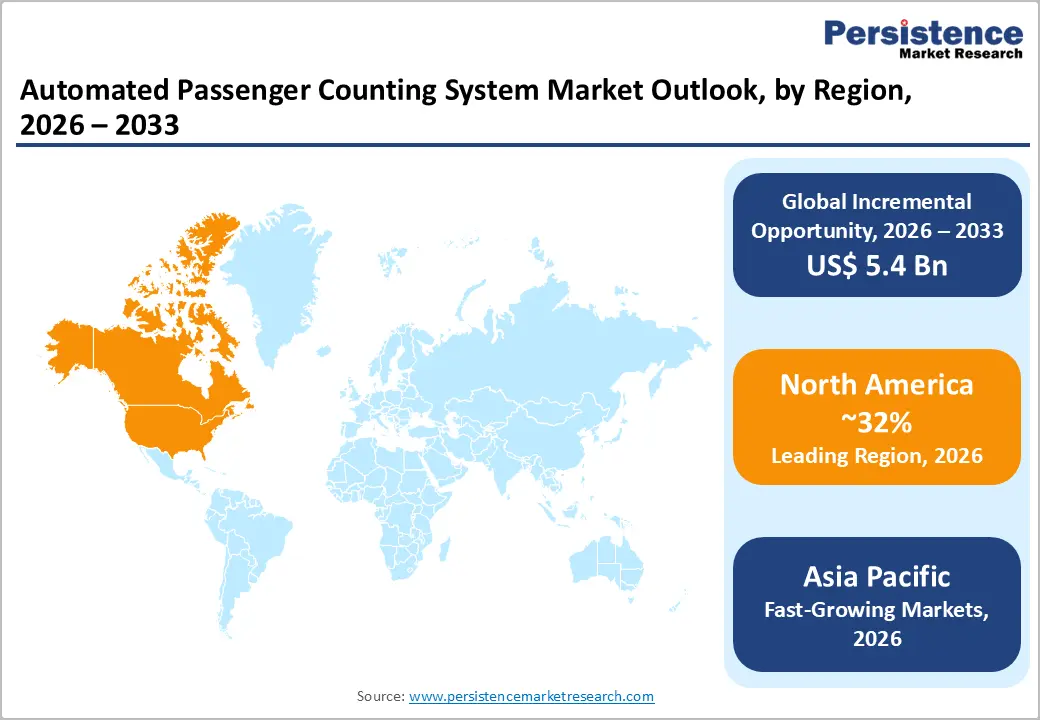

- Leading Region: North America leads the market with about 32% share, supported by advanced transit infrastructure, strong federal funding, smart city investments, and high technology adoption.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, registering a CAGR of 11.2% during 2026 - 2033 due to rapid urbanization, expanding public transport networks, and large-scale smart city programs.

- Dominant Segment: Bus transportation dominates the market with nearly 48% share, driven by its widespread use in urban transit systems and cost-effective APC deployment.

- Fastest Growing Segment: Software solutions are the fastest-growing segment, expanding at a CAGR of 12.1% as demand rises for cloud-based analytics, AI insights, and system integration.

- Key Market Opportunity: AI and advanced analytics integration presents the strongest opportunity by enabling high-accuracy counting, predictive demand forecasting, and real-time occupancy optimization.

| Global Market Attributes | Key Insights |

|---|---|

| Market Size (2026E) | US$ 7.1 Billion |

| Market Value Forecast (2033F) | US$ 12.5 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.4% |

| Historical Market Growth (2020 - 2025) | 7.7% |

Market Dynamics

Market Growth Drivers

Rising Demand for Real-Time Transit Data and Operational Efficiency

Transit agencies face mounting pressure to optimize operational efficiency, reduce costs, and improve service quality through data-driven decision-making, driving widespread adoption of automated passenger counting systems providing real-time occupancy and ridership information. Manual ridership data collection remains labor-intensive, costly, and limited to occasional checkpoints with low accuracy, prompting agencies to transition toward automated solutions providing continuous, accurate passenger flow monitoring.

Automated passenger counting systems enable route optimization, vehicle frequency planning, and resource allocation based on actual demand patterns, reducing operational costs through prevention of empty runs and optimization of vehicle deployment. Revenue protection represents critical value proposition, with systems verifying fare compliance, minimizing ticket fraud, and providing trend analysis supporting strategic planning and financial forecasting. Government agencies and transit authorities increasingly recognize that historical passenger data enables accurate route and schedule planning while minimizing operating costs and maximizing resource utilization, creating compelling business cases justifying substantial capital investments in advanced counting infrastructure.

Smart City Initiatives and Government Investment in Public Transportation Digitalization

Global governments are investing billions supporting smart city infrastructure development, public transportation modernization, and digital transformation of urban mobility systems, establishing regulatory tailwinds for automated passenger counting adoption. Federal Transit Administration (FTA) in the United States provides substantial funding through grants and incentive programs specifically supporting smart transit technology implementation including passenger counting systems. The European Union’s emphasis on sustainable mobility and emissions reduction is driving widespread adoption of public transportation technologies enabling operational efficiency and contributing to urban decarbonization objectives.

China’s smart factory initiatives and India’s Smart Cities Mission allocating US$ 100 billion are catalyzing rapid deployment of automated counting systems throughout Asia-Pacific public transportation networks. Regulatory requirements mandating ridership reporting for federal agencies, combined with increasing emphasis on data transparency and accountability, are establishing mandatory adoption frameworks supporting exponential market expansion across developed and emerging economies.

Market Restraints

High Installation Costs and Legacy System Integration Challenges

Implementation of automated passenger counting systems requires substantial upfront capital investment including hardware procurement, sensor installation, software customization, and system integration with existing vehicle management and data analysis platforms. Integration challenges with legacy systems pose significant technical obstacles, requiring extensive database redesign, software modifications, and establishment of defined interfaces between computerized scheduling packages and automated counting infrastructure.

Many developing countries lack financial resources and technical expertise to implement sophisticated counting systems, constraining market expansion in price-sensitive regions where agencies continue relying on manual collection methods. Retrofitting existing vehicle fleets represents extraordinary complexity and cost barriers, particularly for transit agencies operating thousands of buses requiring systematic sensor installation and integration procedures.

Data Privacy Concerns and Technological Skepticism in Developing Nations

Implementation of camera-based and advanced sensor technologies raises significant data privacy concerns regarding passenger identification, tracking, and potential surveillance applications, creating regulatory and public acceptance obstacles. Unfamiliarity with technology in developing countries perpetuates reliance on traditional manual counting methods despite superior accuracy and cost-effectiveness of automated alternatives.

Cybersecurity vulnerabilities associated with cloud-based data storage and connected IoT devices create organizational hesitancy regarding system adoption and data vulnerability exposure. Lack of standardization across diverse vendor solutions creates technological fragmentation preventing seamless data integration and system interoperability across multi-modal transportation networks.

Market Opportunities

Integration of Artificial Intelligence and Advanced Analytics Capabilities

Artificial intelligence and machine learning algorithms are revolutionizing passenger counting through advanced computer vision models, deep learning architectures including YOLOv3 and MobileNet-SSD, and anomaly detection capabilities enabling sophisticated analysis beyond simple occupancy monitoring. AI-powered predictive analytics enable transit agencies to forecast demand patterns, optimize scheduling, and implement proactive resource allocation supporting superior service quality and operational efficiency improvements.

Real-time occupancy monitoring with color-coded passenger guidance on platform displays enables passengers to spread evenly throughout vehicles, improving comfort while optimizing capacity utilization and reducing congestion. Behavioral analytics powered by machine learning identify peak travel times, passenger flow patterns, and emerging mobility trends supporting strategic planning and infrastructure investment decisions. Integration of edge computing and 5G connectivity enables processing of massive passenger counting datasets locally while maintaining data privacy through anonymized analysis, addressing key adoption barriers in privacy-conscious markets.

Expansion into Railways, Airports, and Multi-Modal Transportation Networks

Railway systems represent the largest application segment anticipated to hold dominant market share through 2030s, with accurate passenger data driving optimization of operational efficiency and enhanced passenger experience across complex rail networks requiring sophisticated demand management. Airport passenger counting systems for terminal operations, security checkpoint monitoring, and gate management create specialized market opportunities supporting pedestrian traffic management, crowd flow optimization, and safety compliance verification.

Multi-modal transportation integration combining buses, trains, ferries, and emerging mobility services creates opportunities for comprehensive passenger counting platforms supporting seamless mobility experiences and integrated fare collection systems. Airlines increasingly implement automated cabin crew and passenger counting systems optimizing seat utilization, baggage handling, and in-flight resource allocation. Smart parking integration with public transportation data enables trip-end decisions and parking availability information supporting end-to-end mobility optimization and enhanced user experience driving adoption of integrated transportation platforms.

Category-wise Insights

Component Analysis: Software Solutions

Software solutions represent the fastest-growing component of the Automated Passenger Counting System market, registering a projected CAGR of 12.1% during 2026-2033. Growth is driven by rising demand for cloud-based analytics, real-time dashboards, and AI-enabled insights that allow transit agencies to maximize value from installed sensor hardware. Software platforms enable centralized data access, reduce on-premise infrastructure costs, and support enterprise-wide fleet monitoring across distributed networks. Advanced analytics capabilities such as predictive demand modeling, behavioral trend analysis, and dynamic route optimization strengthen operational efficiency. Seamless integration with fare collection, scheduling, and passenger information systems further positions software as a critical digital backbone for data-driven public transportation management.

Transportation Mode Analysis: Buses

Bus transportation remains the dominant application segment, accounting for approximately 48% market share in 2025, supported by the widespread presence of urban bus networks and relatively lower system deployment costs. Buses operate across diverse geographies and ownership models, enabling large-scale adoption of passenger counting solutions at the municipal level. Growing urban congestion and rising ridership volumes have intensified the need for accurate passenger data to optimize routes, adjust service frequencies, and manage overcrowding. Integration of APC systems with vehicle location and fleet management platforms enhances real-time occupancy visibility and service planning. As bus fleets are typically modernized ahead of rail systems, they continue to serve as the primary growth driver for APC adoption.

Technology Analysis: Video/Camera Based Systems

Video and camera-based systems are the fastest-growing technology segment, expanding at a projected CAGR of 11.8% during 2026-2033 due to superior accuracy levels exceeding 98%. Advancements in computer vision and deep learning enable these systems to deliver real-time passenger counting alongside congestion detection and behavioral analysis. Single-camera infrastructures support multiple use cases, improving return on investment for transit operators. Declining hardware costs and enhanced processing capabilities have accelerated adoption across high-density transit environments. Privacy-preserving algorithms that anonymize data without personal identification address regulatory concerns, particularly in Europe. These systems also support real-time occupancy displays, improving passenger experience and operational responsiveness.

End User Analysis: Public Transport Authorities

Public transport authorities constitute the largest end-user segment, holding nearly 56% market share in 2025, driven by their responsibility for managing large-scale urban and regional transit networks. Increasing pressure to improve efficiency, justify public funding, and enhance service quality has elevated the importance of accurate ridership data. Regulatory requirements for transparent reporting and performance benchmarking further reinforce APC adoption. Budget limitations within the public sector encourage investment in solutions that deliver high operational intelligence with measurable cost benefits. Automated passenger counting systems provide objective, defensible data that supports policy decisions, capacity planning, and accountability reporting to governments, city councils, and the traveling public.

Regional Insights

North America Automated Passenger Counting System Market Trends and Insights

North America maintains significant market position with approximately 32% regional share, driven by advanced transit infrastructure, substantial government funding through Federal Transit Administration programs, and digital technology adoption leadership. The United States transit systems including New York Metropolitan Transportation Authority, Chicago CTA, and Los Angeles Metro have systematically implemented automated passenger counting systems supporting operational optimization and data-driven planning. Federal transit agencies mandate ridership reporting as prerequisite for continued funding, establishing regulatory requirements driving widespread adoption across regional and municipal transportation systems. Canadian transit systems in Toronto, Vancouver, and Montreal have pioneered advanced passenger counting implementations supporting smart city initiatives and emissions reduction objectives aligned with climate change commitments.

The region experiences high technology adoption rates, sophisticated integration ecosystem supporting seamless platform connectivity, and substantial capital allocation supporting premium-priced solutions. Siemens Mobility, Cisco Systems, and INIT Innovations maintain strong North American market positions through established relationships with major transit operators and demonstrated experience delivering enterprise-scale solutions. The region’s emphasis on operational efficiency and cost containment drives adoption of sophisticated analytics capabilities enabling superior resource optimization compared to alternative solutions.

Europe Automated Passenger Counting System Market Trends and Insights

Europe represents a mature and technologically advanced market characterized by stringent data privacy regulations including GDPR, emphasis on sustainable public transportation, and advanced digital infrastructure. Germany, United Kingdom, and France lead European adoption with comprehensive modernization programs transforming transit networks through integrated technology platforms combining passenger counting with dynamic route displays and real-time passenger information systems. European Union sustainability mandates and carbon neutrality objectives drive government investment in public transportation digitalization supporting emissions reduction and modal shift away from personal vehicles. Regulatory harmonization throughout European markets facilitates cross-border technology deployment and vendor competition establishing efficient procurement frameworks.

The region prioritizes privacy-preserving technologies and demonstrates preference for anonymized analysis without passenger identification, supporting adoption of advanced sensor technologies and video analytics respecting data protection values. HELLA AGLAIA Mobile Vision and regional technology providers maintain competitive positions through specialized expertise in European compliance requirements and multilingual system support. Government agencies throughout the region increasingly view public transportation digitalization as strategic infrastructure investment supporting smart city development and attracting global talent to urban centers.

Asia Pacific Automated Passenger Counting System Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market with CAGR of 11.2% during 2026-2033, projected to capture 40% global market share by 2033 driven by explosive urbanization, rapid public transportation expansion, and government smart city initiatives. China dominates regional adoption with systematic modernization of massive urban transit networks supporting billion-dollar infrastructure investments aligned with national urbanization strategies. The Indian government’s Smart Cities Mission allocating US$ 100 billion is catalyzing rapid passenger counting adoption throughout emerging urban centers. Japan maintains technological leadership through advanced system implementations supporting Tokyo Metro, Osaka Rail, and emerging technologies including AI-based occupancy prediction supporting crowding prevention.

Rapid urbanization creates unprecedented demand for public transportation capacity planning tools supporting infrastructure optimization. Cost-sensitive procurement environments favor Chinese manufacturers offering competitive pricing relative to European alternatives while providing similar functionality. Government-led digital transformation initiatives establish regulatory mandates supporting systematic technology adoption across entire regional transit systems. The region experiences exceptional growth in emerging technologies including autonomous vehicle integration and advanced analytics supporting next-generation transportation systems.

Competitive Landscape

Market Structure Analysis

The automated passenger counting system market demonstrates moderate fragmentation with 8-12 significant global competitors offering differentiated solutions across technologies, transportation modes, and service capabilities. Siemens Mobility, Cisco Systems, INIT Innovations in Transportation, and Eurotech maintain dominant competitive positions through comprehensive product portfolios, established OEM relationships, and proven delivery capabilities at enterprise scale. Market consolidation continues through strategic acquisitions, with larger technology companies acquiring specialized vendors to expand passenger counting capabilities within broader smart transportation platforms. Competitive differentiation strategies emphasize AI integration, cloud analytics, multi-modal support, and specialized expertise addressing unique regional requirements. European competitors including DILAX Intelcom and HELLA AGLAIA maintain competitive positions through GDPR compliance expertise and preference for privacy-preserving technologies. Emerging Chinese competitors gain market share through cost-competitive offerings and integration with domestic transportation ecosystems. Smaller specialized vendors differentiate through focused technology approaches, superior customer service, and ability to serve niche market segments where larger competitors lack specialized expertise.

Key Market Developments

- September 2024: Siemens Mobility commissioned advanced Communications-Based Train Control (CBTC) system for Oslo Metro increasing network capacity by 30% while demonstrating integration of real-time passenger data collection capabilities supporting automated occupancy monitoring and crowd management for modern rail systems.

- December 2024: Cisco Systems announced expanded partnership with transit authorities throughout Europe delivering integrated smart city solutions combining passenger counting systems with real-time passenger information displays and dynamic route optimization supporting superior service quality and operational efficiency improvements.

- March 2025: INIT Innovations in Transportation launched next-generation AI-powered passenger analytics platform enabling predictive demand forecasting and dynamic resource allocation supporting transit agencies’ transition toward intelligent, data-driven operational management approaches.

Companies Covered in Automated Passenger Counting System Market

- Eurotech S.p.A.

- Iris GmbH

- DILAX Intelcom GmbH

- Infodev Electronic Designers Inc.

- Siemens AG

- Hitachi, Ltd.

- Cubic Corporation

- Cisco Systems, Inc.

- INIT Innovations in Transportation, Inc.

- Vix Technology Pty Ltd

- Clever Devices Ltd

- Trapeze Group

- HELLA AGLAIA MOBILE VISION GMBH

- V-Count

- Xovis AG

- Pecco (Passenger Electronic Counting Company)

- IComtec Sistemas Inteligentes

- Nuada Software GmbH

- Calypso Networks Association

- Mobokey Technologies

Frequently Asked Questions

The market is expected to reach approximately US$ 7.1 billion in 2026.

Key drivers include demand for real-time transit data, smart city investments, regulatory ridership reporting requirements, and advances in AI-enabled high-accuracy counting technologies.

North America is expected to lead the market with around 32% share during the forecast period.

The biggest opportunity lies in integrating AI and advanced analytics for predictive demand forecasting and real-time occupancy optimization.

Major players include Siemens Mobility, Cisco Systems, INIT Innovations in Transportation, Eurotech, Hitachi, Cubic Corporation, Iris GmbH, DILAX Intelcom, V-Count, and Xovis AG.