- Inks, Coatings, Adhesives & Sealants (ICAS)

- Adhesive Activator Market

Adhesive Activator Market Size, Share, and Growth Forecast 2026 - 2033

Adhesive Activator by Resin Type (Epoxy, Polyurethane, Acrylic, Silicone, Cyanoacrylate), by Application (Automotive, Construction, Electronics, Packaging, Others), by Regional Analysis, 2026-2033

Adhesive Activator Market Size and Trend Analysis

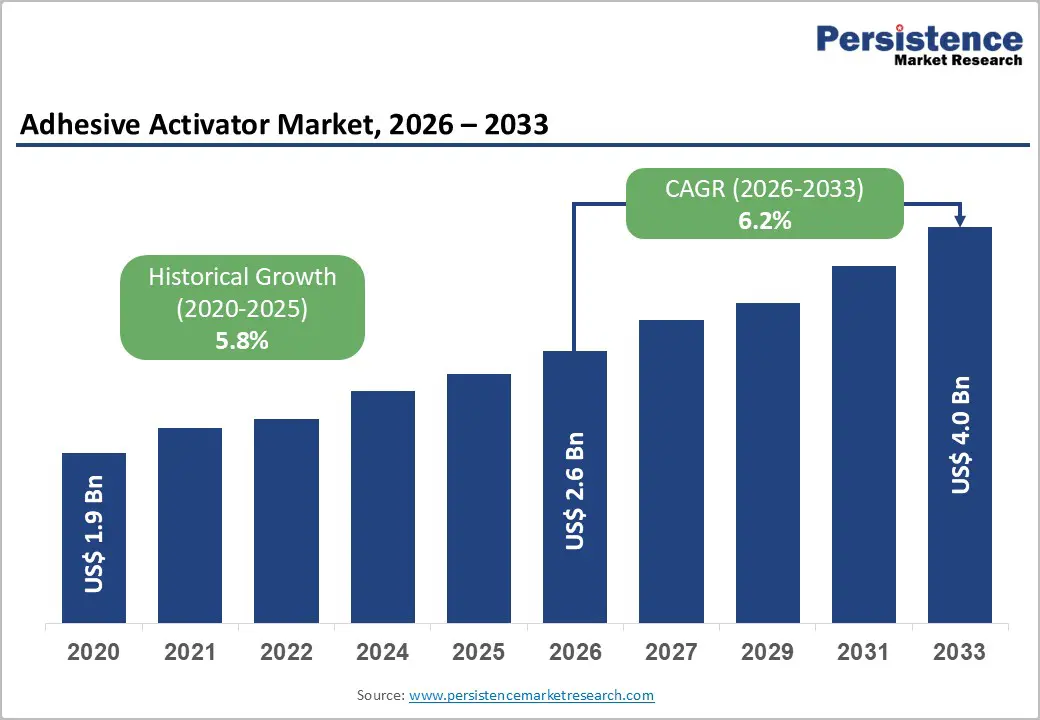

The global adhesive activator market is projected to reach around US$ 4.0 billion by 2033, up from US$ 2.6 billion in 2026, growing at a CAGR of about 6.2%.

Market growth is driven by the rapid rise in electric vehicle production, increasing use of lightweight composites in automotive and aerospace, and strong demand for fast-curing bonding solutions in electronics and construction. Stricter VOC regulations are also accelerating the shift toward eco-friendly adhesive activators. In addition, infrastructure expansion across Asia Pacific and advances in automated dispensing technologies are further boosting adoption across industrial manufacturing environments.

Key Market Highlights

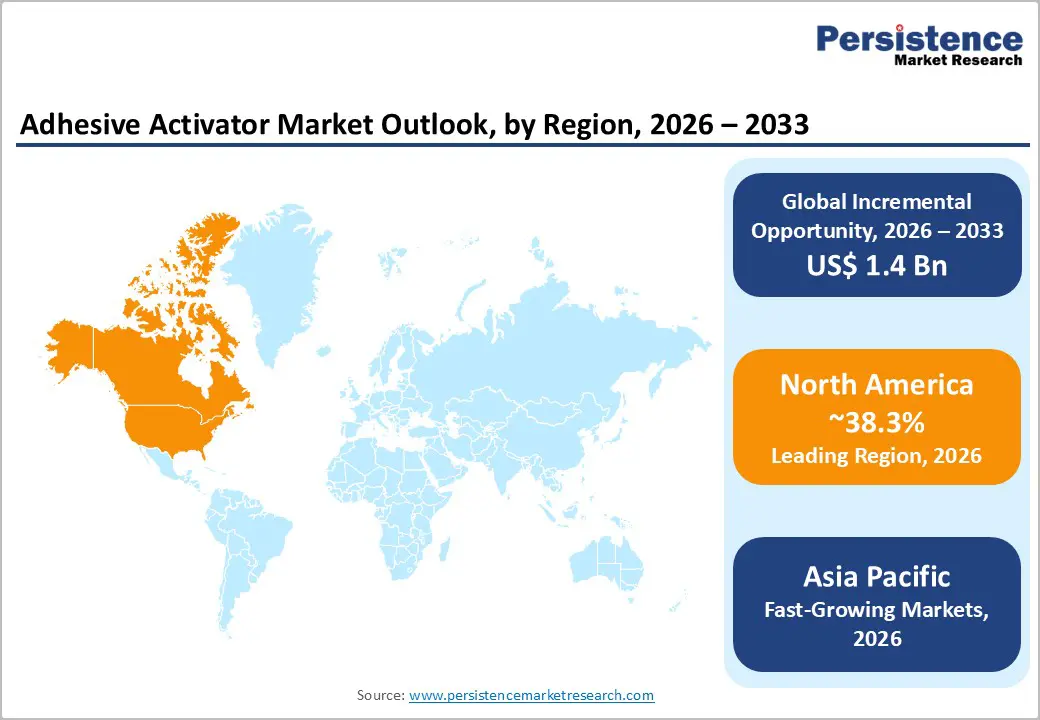

- Leading Region: North America leads the adhesive activator market with around 38.3% share, supported by aerospace, EV platforms, automation, and premium-performance bonding needs.

- Fastest-Growing Region: Asia Pacific remains the fastest-expanding market, holding around 34.1% share, driven by large-scale automotive, electronics, and industrial manufacturing growth.

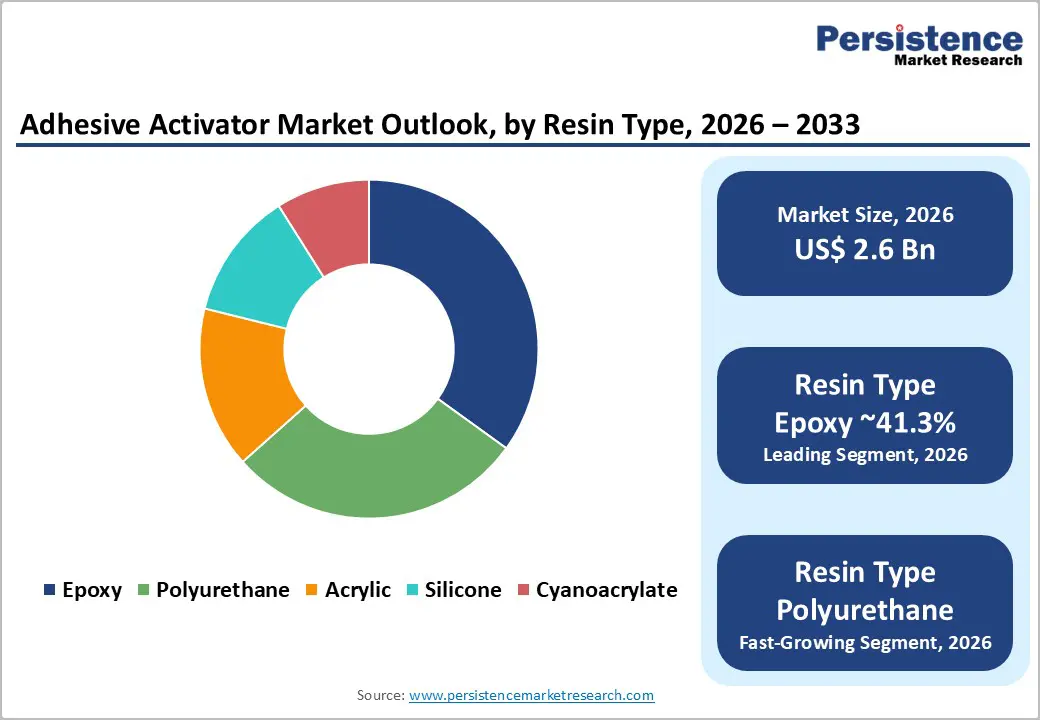

- Dominant Resin Type: Epoxy-based adhesive activators retain leadership with about 41.3% share, thanks to superior strength, heat resistance, and multi-substrate bonding.

- Fastest-Growing Application: Electronics and semiconductor assembly is the fastest-growing segment, supported by miniaturization, high-speed automation, and reliability demands.

- Key Opportunity: Bio-based and sustainable adhesive activators gain traction as sustainability policies and ESG commitments boost adoption and pricing premiums.

| Key Insights | Details |

|---|---|

| Adhesive Activator Market Size (2026E) | US$ 2.6 Billion |

| Market Value Forecast (2033F) | US$ 4.0 Billion |

| Projected Growth CAGR (2026-2033) | 6.2% |

| Historical Market Growth (2020-2025) | 5.8% |

Market Dynamics

Market Growth Drivers

Surging Electric Vehicle Battery Assembly Needs and Intensifying Thermal Management Challenges

The fast-expanding EV ecosystem is dramatically boosting demand for adhesive activators that deliver fast, reliable bonding across battery modules, thermal interface layers, and protective encapsulations. Epoxy-based activators are especially critical because they offer strong mechanical integrity, thermal conductivity, and chemical resistance under harsh operating environments characterized by vibration, heat cycling, and moisture exposure.

As EV battery technologies scale, automakers are prioritizing thermally conductive adhesive systems and injectable thermal compounds to improve heat dissipation and extend battery lifespan. Leading players, including Henkel with solutions like Loctite TLB 9300 APSi, are shaping performance benchmarks. With global EV production projected to grow sharply through 2030, specialized activators that shorten cure times while preserving bond integrity are gaining significant traction.

Rapid Advancement in Electronics Manufacturing and Component Miniaturization Requirements

Growing adoption of flexible electronics, foldable smartphones, wearables, and IoT devices is driving the need for precision adhesive activators that enable ultra-fast curing in compact assembly spaces. The expansion of the electronics adhesives market supported by semiconductor packaging, die-attach, and encapsulation applications is closely tied to performance-driven activators capable of delivering reliable bonds within seconds.

Cyanoacrylate and silicone-based activators are increasingly favored for semiconductor manufacturing, where consistency, thermal stability, and moisture resistance are essential. Expanding 5G infrastructure, smaller device footprints, and automated high-volume production environments demand activators that ensure zero-defect assembly and repeatable performance. As manufacturers pursue tighter tolerances and faster throughput, advanced activation technologies are becoming central to next-generation electronics manufacturing strategies.

Market Restraints

Volatile Raw Material Costs and Heightened Global Supply Chain Vulnerabilities

The adhesive activator market is constrained by sharp fluctuations in prices of petroleum-derived intermediates, specialty polymers, and catalyst systems that collectively account for most production costs. Crude oil swings, geopolitical instability, and export controls on chemical feedstocks disrupt material availability and create unpredictable pricing structures, particularly for manufacturers operating in developing economies with limited sourcing diversity.

Extended lead times for high-performance accelerators and catalysts have increased procurement costs, compressed margins, and delayed innovation cycles. At the same time, tightening regulations such as REACH and global restrictions on hazardous substances are forcing expensive reformulation programs. Many companies require lengthy validation windows to develop compliant chemistries that match legacy performance, slowing product launches and dampening overall market expansion.

Short Shelf Life, Storage Constraints, and Environmental Sensitivity of Liquid Activators

Many adhesive activators especially cyanoacrylate-based systems exhibit inherent chemical instability, resulting in limited shelf lives and frequent spoilage. Exposure to humidity, heat, and transportation stress can degrade reactivity, generating inventory waste and complicating logistics for distributors and end users who must carefully control handling conditions throughout the supply chain.

Loss rates rise significantly in tropical and high-humidity regions where storage infrastructures struggle to maintain recommended temperature and moisture thresholds. Smaller regional players are disproportionately affected, as maintaining climate-controlled warehousing increases operating costs. These challenges limit product accessibility in cost-sensitive markets, restrict penetration into developing economies, and ultimately temper growth prospects despite strong underlying demand.

Market Opportunities

Acceleration Toward Bio-Based, Low-VOC, and Environmentally Sustainable Activator Chemistries

Growing regulatory pressure and corporate sustainability mandates are creating a significant opportunity for bio-based, solvent-free, and low-VOC adhesive activators. Water-based accelerators and plant-derived chemistries are gaining traction as customers prioritize safer handling, reduced emissions, and improved environmental credentials without compromising bonding performance, durability, or cure speed across industrial applications.

Leading producers are investing heavily in renewable feedstocks, including plant oils, cellulose derivatives, and fermentation-derived intermediates. Premium pricing, compliance advantages, and alignment with LEED, BREEAM, and ESG targets are generating attractive margins in the construction, packaging, and consumer goods sectors. As sustainable adhesives scale rapidly, eco-friendly activators positioned as performance-equivalent alternatives to legacy petrochemical systems are expected to capture meaningful share in regulated and brand-sensitive markets.

Rising Demand for Lightweight Composite Bonding in Aerospace, Wind Energy, and Advanced Manufacturing

The shift toward lightweight engineering especially in aerospace, transportation, and renewable energy is creating strong growth potential for high-performance adhesive activators tailored for composite bonding. As aircraft structures increasingly incorporate CFRP and advanced laminates, activators that enable dissimilar material bonding while ensuring structural reliability are becoming strategically important.

Adoption is expanding as OEMs replace mechanical fasteners with adhesive bonding to reduce weight, fuel consumption, and assembly complexity. Parallel momentum in wind turbine manufacturing further strengthens demand, with large blade structures requiring durable activators capable of rapid curing under harsh environmental and fatigue conditions. These specialized, premium-grade systems offer higher value capture and long-term, recurring demand across mission-critical composite applications.

Category-wise Insights

Resin Type Analysis

Epoxy-based adhesive activators hold the leading position in the resin segment, accounting for roughly 41.3% of market share. Their dominance is supported by outstanding mechanical strength, thermal stability, and chemical resistance, making them indispensable for automotive structures, aerospace assemblies, and heavy industrial equipment bonding. Superior adhesion to metals, plastics, and composites allows manufacturers to replace mechanical fasteners while improving durability and structural performance.

The fastest-growing opportunity lies with bio-aligned and specialty polyurethane activators engineered for flexible bonding environments. Demand is expanding across automotive interiors, construction sealants, and applications involving constant movement, dynamic loads, and environmental exposure. These systems offer greater design freedom, enhanced comfort, and long-term resilience positioning them as a preferred choice where traditional rigid adhesive systems cannot effectively perform.

Application Analysis

Automotive and transportation remain the dominant application segment, representing approximately 46.4% of overall demand. Automakers increasingly rely on adhesive activators to replace welding, rivets, and bolts, enabling lightweight designs, improved crash behavior, noise reduction, and faster assembly. Expanding vehicle electrification further reinforces usage in battery modules, structural bonding, and thermal management systems across global manufacturing lines.

The fastest-growing application opportunity emerges within advanced electronics and semiconductor assembly. Miniaturized components, tighter tolerances, and high-speed automated manufacturing require precision activators that deliver instant bonding, moisture protection, and thermal stability. As device complexity rises from wearables to power electronics, manufacturers are shifting toward high-performance activation systems that ensure reliability, defect reduction, and consistent throughput across next-generation production environments.

Regional Insights

North America Adhesive Activator Trends

North America represents a large, technologically sophisticated market, accounting for roughly 38.3% of global adhesive activator demand. Strong penetration across aerospace, defense, EV platforms, and automated manufacturing environments supports sustained consumption of high-performance epoxy and polyurethane activators designed for structural reliability, lightweighting, and stringent certification requirements across mission-critical applications.

Market expansion is reinforced by stricter VOC rules, preference for sustainable chemistries, and heavy investment in automation. Premium, low-emission activators command pricing advantages, while the ongoing shift toward EV assemblies, battery systems, and smart manufacturing helps maintain steady growth momentum despite market maturity and competitive pressure from alternative joining technologies.

Europe Adhesive Activator Trends

Europe remains an innovation-driven and highly regulated market, shaped by environmental mandates, circular-economy policies, and advanced manufacturing standards. The region’s demand is increasingly oriented toward low-VOC, solvent-free, and bio-based activator formulations aligned with Green Deal and REACH compliance expectations across automotive, aerospace, construction, and industrial sectors.

Europe is projected to expand at a steady ~6.5% CAGR, supported by EV transition programs, renewable infrastructure investments, and premium-grade adhesive technologies tailored for performance, durability, and sustainability leadership. Strong participation from leading chemical producers and a deeply integrated OEM ecosystem reinforces long-term innovation and value-added product adoption across key end-use industries.

Asia Pacific Adhesive Activator Trends

Asia Pacific is the fastest-growing regional market, commanding approximately 34.1% of global consumption driven by large-scale automotive production, electronics manufacturing hubs, and rapid industrialization across China, India, Japan, South Korea, and Southeast Asia. Concentrated activity in EV assembly, consumer devices, and infrastructure development fuels the accelerating adoption of high-performance activators across diverse bonding environments.

Growth is supported by expanding contract manufacturing, government-backed industrial programs, and rising localization of adhesive production facilities. Increasing investments in advanced composites, semiconductors, and high-speed automated manufacturing continue to elevate demand for precision, rapid-cure activator systems, positioning the Asia Pacific as the primary engine of future market expansion.

Competitive Landscape

The adhesive activator market is characterized by a moderately consolidated structure, where a limited group of global manufacturers sets performance standards, technology direction, and product innovation, while numerous regional suppliers compete on pricing, customization, and proximity to local customers. Larger participants benefit from strong distribution networks, technical support capabilities, and long-term partnerships with industrial OEMs.

Competition is increasingly shaped by sustainability commitments, portfolio expansion, and regional manufacturing strategies. Companies are investing in low-emission and bio-based formulations, acquiring specialized producers to expand applications expertise, and deploying digitally enabled dispensing systems to improve accuracy, efficiency, and customer retention across automotive, electronics, construction, and industrial sectors.

Key Market Developments

- In September 2025, Huntsman Advanced Materials unveiled a new variety of Araldite epoxy adhesives formulated without intentionally added BPA, addressing growing regulatory concerns and customer preferences for safer chemical profiles in automotive and electronics applications.

- In September 2025, Henkel expanded its manufacturing facility in Brandon, South Dakota, to deliver high-performance materials for the electronics and electric vehicle industries, signaling accelerated investment in North American capacity to support growing EV battery and semiconductor bonding demand.

- In May 2024, Henkel introduced Loctite TLB 9300 APSi, an innovative injectable thermally conductive adhesive specifically designed for EV battery systems, demonstrating commitment to specialized EV bonding solutions and thermal management innovations required for next-generation battery architectures.

Frequently Asked Questions

The global adhesive activator market is projected to reach US$ 4.0 Billion by 2033 from US$ 2.6 Billion in 2026, growing at 6.2% CAGR driven by automotive, electronics, and construction demand.

Market growth is propelled by EV battery assembly, lightweight composites in autos/aerospace, electronics miniaturization, Asia Pacific infrastructure push, and sustainability-driven low-VOC regulations.

Epoxy-based adhesive activators dominate the resin type category with about 41.3% share due to strong mechanical performance and reliability across critical bonding applications.

Asia Pacific remains the leading regional market with about 34.1% share, supported by strong manufacturing, automotive, and electronics output.

The major growth opportunity lies in bio-based and sustainable adhesive activators aligned with tightening regulations and corporate ESG commitments.

Major market players include Henkel AG & Co. KGaA, 3M Company, Sika AG, Arkema S.A., BASF SE, and H.B. Fuller Company.