- Hardware & Software IT Services

- Storage in Big Data Market

Storage in Big Data Market Size, Share, and Growth Forecast, 2025 - 2032

Storage in Big Data Market By Deployment Mode (Cloud, On-Premises), Component (Hardware, Software, Services), Storage Type (Network Attached Storage (NAS), Others), Industry (BFSI, Healthcare, Retail, Others), and Regional Analysis for 2025 - 2032

Storage in Big Data Market Share and Trends Analysis

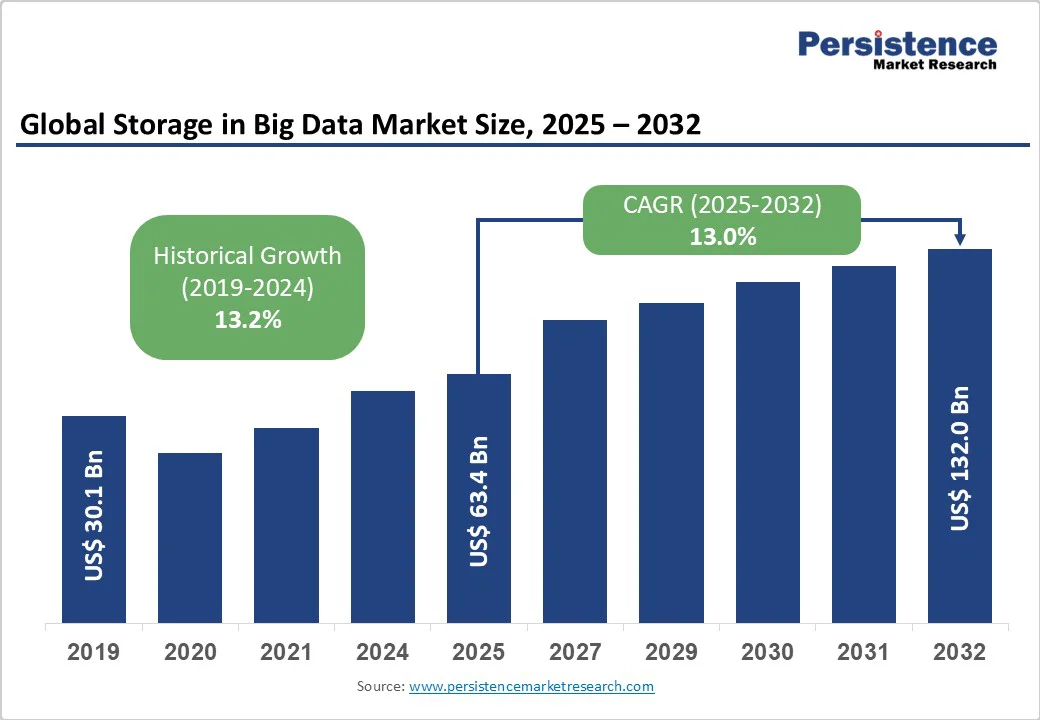

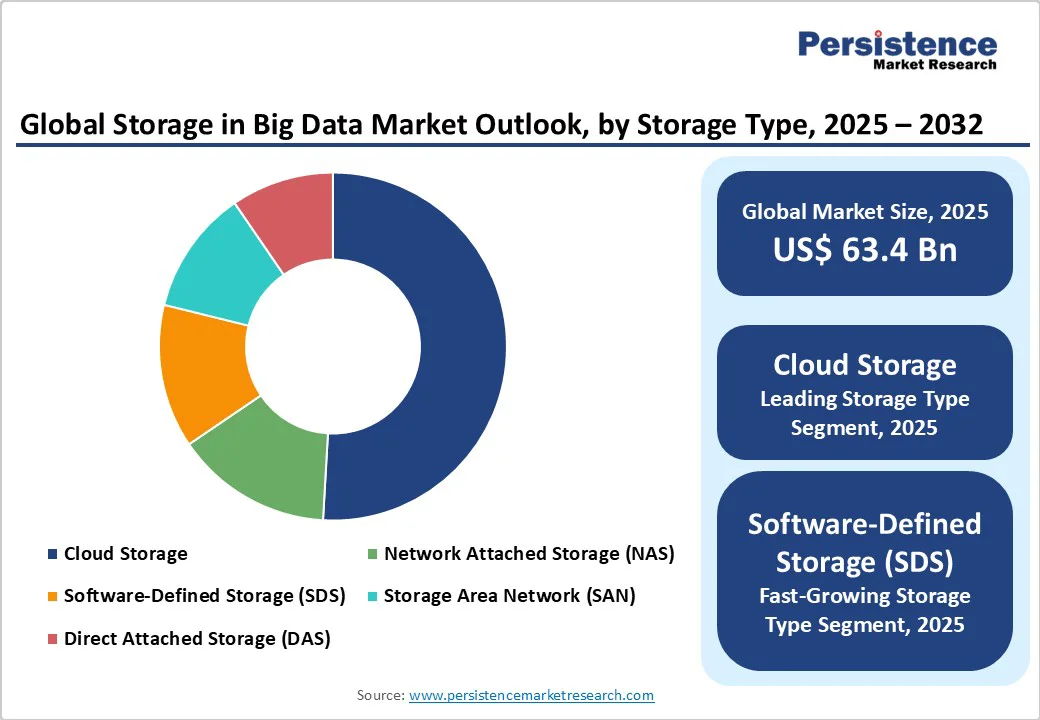

The global storage in big data market size is likely to be valued at US$63.4 Billion in 2025 and is estimated to reach US$132 Billion by 2032, growing at a CAGR of 13% during the forecast period 2025-2032, driven by exponential data generation and the shift toward cloud-based storage solutions. This growth is fueled by the increasing adoption of advanced storage technologies and rising demand across the BFSI, healthcare, and retail sectors.

Key Industry Highlights

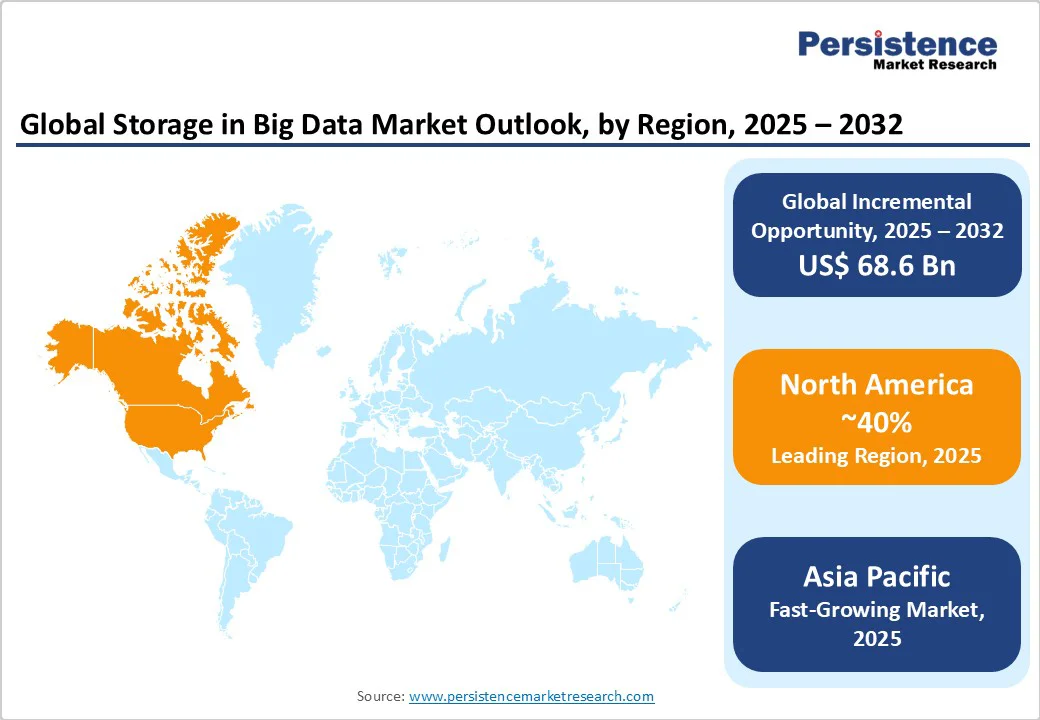

- Leading Region: North America will be the largest market with an estimated 39.8% share in 2025, driven primarily by the U.S., which benefits from advanced digital infrastructure, early and widespread cloud adoption, and a strong innovation ecosystem centered around Silicon Valley.

- Fastest-growing Region: Asia Pacific is the fastest-growing regional market during 2025-2032, driven by accelerated urbanization, government-led digital transformation initiatives, and robust manufacturing expansion, which are key factors set to drive market growth.

- Significant Development: In August 2025, Meta Platforms entered a six-year cloud-computing contract with Google Cloud, valued at over US$10 Billion, under which Meta will use Google’s servers, storage, networking, and other cloud services.

- Dominant Component Type: Services are slated to dominate the component category with 44.2% market share in 2025, while software is likely to exhibit the fastest growth between 2025 and 2032.

- Leading End-user: Among industry verticals, BFSI is anticipated to lead with approximately 25% market share, and healthcare is expected to grow the fastest.

- Leading Storage: Cloud storage is anticipated to lead the market in 2025, capturing around 50.9% share, primarily because of its ability to scale dynamically while reducing upfront capital expenses.

| Key Insights | Details |

|---|---|

|

Storage in Big Data Market Size (2025E) |

US$63.4 Bn |

|

Market Value Forecast (2032F) |

US$132 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

13.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

13% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Explosive Data Generation and Digitization

Global data generation is accelerating rapidly, with projections that data creation will exceed 180 zettabytes by 2025. This surge is fueled by digital transformation across sectors such as manufacturing, healthcare, finance, and consumer services. The expansion of IoT devices, AI applications, and 5G networks has significantly increased the volume, speed, and complexity of data, driving demand for scalable, advanced storage solutions. Enterprises are increasingly adopting cloud-based infrastructures for their flexibility, cost-effectiveness, and ability to support business agility. Another study states that, by 2025, around 80% of organizations will deploy hybrid or multi-cloud strategies to enhance resource efficiency and operational responsiveness.

Moreover, growing regulatory pressures are shaping enterprise storage decisions. Frameworks such as the EU’s GDPR and California’s CCPA require secure, compliant data handling practices. Companies must now invest in storage systems with robust encryption, detailed auditing, and stringent access controls to meet these standards. Reports from TechRepublic and NIST indicate that compliance-related investments can constitute up to 20% of overall storage budgets. As a result, regulatory compliance has become a major market driver, pushing organizations to modernize storage infrastructure. These trends collectively broaden the market reach, attracting businesses of all sizes seeking resilient, agile, and compliant data storage ecosystems.

High Infrastructure and Operational Costs

High capital costs remain a significant barrier to adopting advanced storage solutions, particularly for small and medium-sized enterprises (SMEs). Expenses related to hardware procurement, proprietary software licensing, and ongoing system maintenance can be prohibitive. Premium technologies such as solid-state drives (SSDs) and NVMe systems often cost 30–40% more than traditional disk-based storage. Additionally, the high energy consumption and cooling needs of large-scale data centers further increase the total cost of ownership, limiting adoption in price-sensitive sectors.

Global supply chains face ongoing disruptions due to semiconductor shortages, logistical delays, and geopolitical tensions. Trade conflicts, such as the U.S.-China tariff escalations, have increased raw material costs and constrained hardware availability. These challenges are expected to raise market prices and delay product rollouts, potentially slowing growth by 2-3% in impacted regions. Extended supply chain disruptions also risk hindering innovation cycles, delaying critical advancements needed to meet the rapidly expanding global demand for data storage.

Widening Opportunities in Emerging Markets

Asia Pacific is emerging as a pivotal growth frontier for big data storage, with rapid digitalization, expanding manufacturing bases, and robust government initiatives underpinning demand. China and India, in particular, are investing heavily in smart city infrastructure, cloud computing capabilities, and national digital economies. Government policies fostering ICT adoption and infrastructure development are catalyzing the diversification and expansion of storage ecosystems. Market projections estimate that the Asia Pacific will reach an incremental US$20 to 25 Billion in market value by 2030, reflecting vast opportunities for providers focusing on local partnerships and tailored solutions addressing regional requirements.

Another lucrative area for market players is the fusion of big data storage with AI-driven analytics and edge computing technologies, which is revolutionizing data management paradigms by enabling rapid real-time processing and reducing latency. Industries such as autonomous vehicles, smart manufacturing, and healthcare are leveraging decentralized, localized storage architectures to support mission-critical applications, where immediate data insights are essential. This convergence motivates demand for specialized storage products that deliver enhanced performance, low latency, and scalability at the network edge. Vendors innovating in this space are unlocking new market segments and differentiating their offerings to capitalize on emerging technology adoption trends. Moreover, government policies promoting cloud adoption, particularly among public sector organizations, are fostering accelerated migration to cloud storage services. Incentives, including subsidies, grants, and regulatory directives, for digital modernization are expanding the customer base for cloud providers, especially in North America and Europe.

Category-wise Analysis

Component Insights

In 2025, the services segment is likely to dominate the storage in big data market with an estimated 44.2% share. This dominance is driven by the increasing complexity of storage infrastructures that demand expert lifecycle management, including consulting, system integration, and maintenance services. Enterprises are increasingly relying on specialized providers to navigate cloud migration, optimize storage architectures, and ensure compliance with evolving security standards.

At the same time, the software segment is experiencing rapid expansion with a high CAGR through 2032, fueled by the growing need for automation in storage management, data orchestration, and analytics-ready solutions. Software offerings such as data management platforms, virtualization tools, and advanced storage orchestration provide enterprises with enhanced control, efficiency, and scalability to manage vast data repositories effectively.

Storage Type Insights

Cloud storage is anticipated to lead the market in 2025, capturing around 50.9% share, primarily because of its ability to scale dynamically while reducing upfront capital expenses. Public cloud storage options dominate due to their extensive scalability and pay-as-you-go pricing models, favored by organizations with fluctuating storage needs. Hybrid cloud storage is also gaining momentum as organizations seek to balance security and flexibility, enabling sensitive data to be retained in private environments while leveraging public cloud capacity for less critical workloads.

Software-defined storage (SDS) is poised for impressive growth from 2025 to 2032, offering hardware-agnostic control, automation, and enhanced efficiency. SDS adoption is driven by enterprises’ increasing demands for agile storage management, cost reduction, and seamless integration across hybrid and multicloud environments.

Industry Insights

The banking, financial services, and insurance (BFSI) industry is expected to occupy the top position by capturing approximately 25% of the storage in big data market revenue share in 2025. This leadership stems from the highly data-intensive operations in the BFSI sector requiring secure, scalable, and compliant storage infrastructure to manage transactional data, risk analytics, and regulatory mandates.

On the other hand, the healthcare sector is anticipated to witness robust growth at the highest CAGR through 2032, driven by expanding electronic health records, medical imaging, genomics, and personalized medicine data. Healthcare storage solutions prioritize compliance with stringent data protection regulations, high capacity, and rapid access to large datasets crucial for patient care and research advances.

Regional Insights

North America Storage in Big Data Market Trends

North America is projected to hold the largest share of about 39.8% in 2025, with the U.S. leading due to advanced digital infrastructure, widespread early cloud adoption, and a vibrant innovation ecosystem, notably in Silicon Valley. The market growth is propelled by investments in AI, edge computing, and regulatory compliance, such as HIPAA enforcement.

Major industry players, including IBM, Dell, and AWS, dominate the competitive landscape. Investment activities focus on mergers, acquisitions, and strategic expansions targeting hybrid cloud storage capabilities combined with AI-powered data management solutions to sustain market leadership.

Europe Storage in Big Data Market Trends

Europe is expected to secure roughly 25% of the storage in big data market revenue, with Germany, the U.K., France, and Spain as leading contributors. Regional market growth is aided by harmonized data protection laws such as GDPR, boosting trust and adoption of advanced storage infrastructures across BFSI, manufacturing, and healthcare sectors.

Regulatory harmonization enables simplified cross-border cloud storage operations, while sustainability trends push for environmentally friendly, energy-efficient storage technologies. Siemens, SAP, and Atos are key players, focusing investments on green IT initiatives and integrated cloud-storage services that prioritize compliance and digital sovereignty.

Asia Pacific Storage in Big Data Market Trends

Asia Pacific is the fastest-growing storage in big data market. Rapid urbanization, governmental digital transformation programs, and expansive manufacturing growth are factors that will catalyze market expansion.

The regional market is also likely to gain from cost advantages owing to its strong manufacturing base for storage hardware, and favorable policies promote extensive cloud adoption across retail, BFSI, and other sectors. Leading companies such as Huawei, Samsung, and Tata Consultancy Services are investing substantially to grow data center capacities and integrate AI-powered storage technologies, addressing the region’s burgeoning demand for scalable, efficient big data storage solutions.

Competitive Landscape

The global storage in big data market structure is moderately concentrated, with the top 10 players accounting for over 60% of the revenue share. Leading firms include IBM, Dell Technologies, Hewlett Packard Enterprise, and Amazon Web Services, reflecting a competitive environment characterized by innovation and strategic partnerships.

The market features a mix of legacy storage providers and newer cloud-native entrants, fostering a dynamic arena of intense competition. Prime players are prioritizing innovation in AI-integrated storage systems, cost leadership through scalable cloud offerings, and geographic expansion into emerging markets. The major emphasis on hybrid cloud solutions and customizable storage services differentiates key players, while subscription-based and consumption models gain traction.

Key Industry Developments

- In August 2025, MIT and Cloudian developed a unified storage-compute platform to accelerate AI workloads by delivering high-speed, parallel data access to GPUs. The system reduces latency and energy use by integrating storage, retrieval, and processing, and supports real-time vector database integration with NVIDIA GPU optimization for faster AI training and inference.

- In June 2025, researchers from the University of Manchester and Australian National University developed a single-molecule magnet using a dysprosium amide-alkene complex that retains magnetic memory up to 100 K, a record high. This advancement could enable ultra-dense data storage of up to 3 terabytes per square centimeter, though low operating temperatures remain a key challenge.

- In June 2025, Flinks partnered with European open banking firm Trask Solutions to accelerate open banking adoption in North America, especially Canada. Trask’s “Data-In Connector,” widely used in Europe, was localized and pre-integrated with Flinks to simplify infrastructure for consent management, data enrichment, and connectivity. The collaboration aims to speed up digital banking rollouts, cut development costs, and enhance user experience.

Companies Covered in Storage in Big Data Market

- IBM Corporation

- Dell Technologies Inc.

- Hewlett-Packard Enterprise Company

- Amazon Web Services, Inc.

- Huawei Technologies Co., Ltd.

- Samsung Electronics Co., Ltd.

- NetApp, Inc.

- Microsoft Corporation (Azure)

- Hitachi, Ltd. (Hitachi Vantara)

- Google LLC (Google Cloud)

- Oracle Corporation

- Cisco Systems, Inc.

- Western Digital Corporation

- Seagate Technology PLC

- Tata Consultancy Services Limited (TCS)

Frequently Asked Questions

The storage in big data market is projected to reach US$63.4 Billion in 2025.

Exponential data generation and the shift toward cloud-based storage solutions are driving the market.

The storage in big data market is poised to witness a CAGR of 13% from 2025 to 2032.

The increasing adoption of advanced storage technologies and enormous data volumes across the BFSI, healthcare, and retail sectors are key market opportunities.

IBM Corporation, Dell Technologies Inc., and Hewlett-Packard Enterprise Company are some of the key players in storage in the big data market.