- Energy Storage Solutions

- Intelligent Energy Storage System Market

Intelligent Energy Storage System Market Size, Share, and Growth Forecast, 2026 - 2033

Intelligent Energy Storage System Market by Product Type (Lithium-Ion Battery-based ESS, Lead-Acid Battery-based ESS, Flow Battery-based ESS, Solar-based ESS), Energy Source (Renewable Energy Storage, Grid Energy Storage, Hybrid Systems), Application (Residential, Commercial, Industrial, Grid Scale) and Regional Analysis for 2026 - 2033

Intelligent Energy Storage System Market Size and Trends Analysis

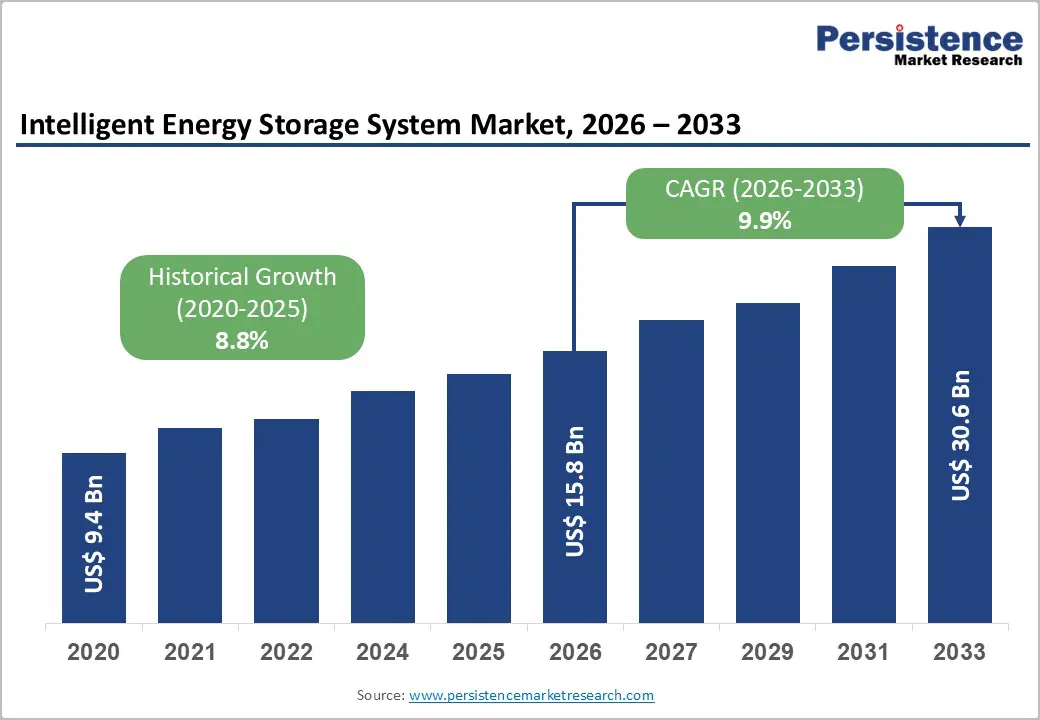

The Global Intelligent Energy Storage System market size was valued at US$ 15.8 Billion in 2026 and is projected to reach US$ 30.6 Billion by 2033, expanding at a CAGR of 9.9% during the 2026-2033 period. This market trajectory reflects substantial growth momentum driven by accelerating renewable energy adoption, critical grid stability requirements, and significant technological advancement in battery chemistries and intelligent management systems.

The market's expansion is underpinned by government policies mandating renewable energy integration, declining battery system costs, and the essential role of energy storage in supporting the global decarbonization agenda.

Key Industry Highlights:

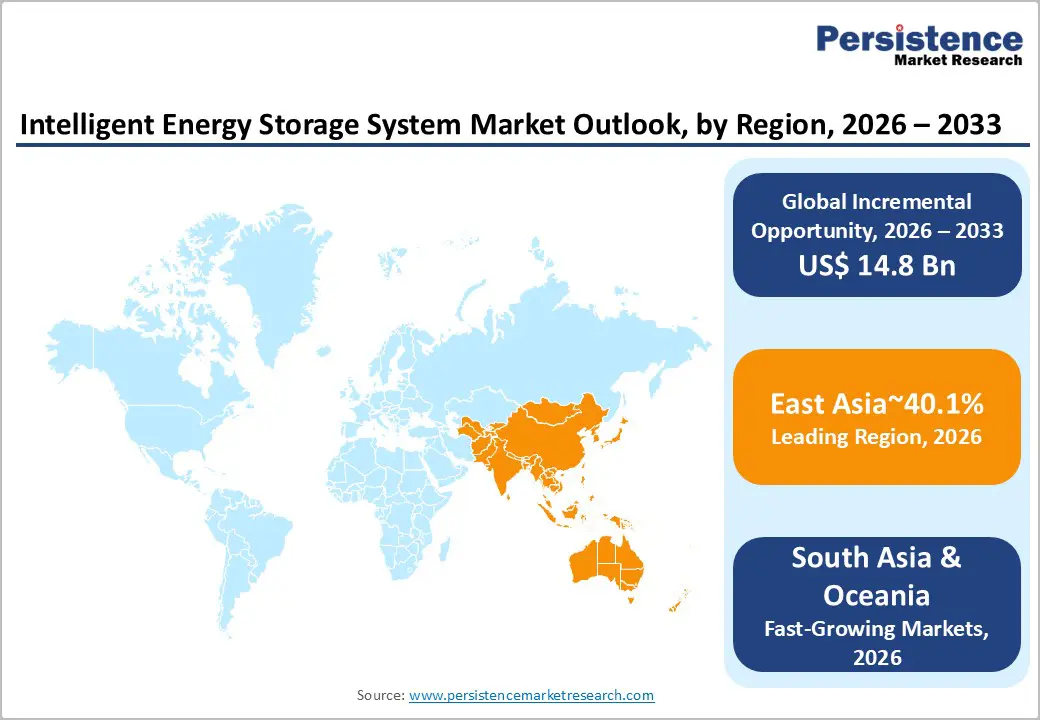

- Regional Leadership: East Asia leads the global Intelligent Energy Storage System market with 40.1% share, driven by China’s massive grid modernisation, renewable energy targets, and extensive lithium battery manufacturing capacity.

- •Strong North American Market: North America holds 25.3% share, supported by U.S. deployment incentives under the Inflation Reduction Act, utility-scale storage expansion, and rapid residential behind-the-meter adoption.

- Established European Presence: Europe captures 15% share, fueled by ambitious decarbonization goals, regulatory mandates for renewable integration, and growth in both grid-scale and behind-the-meter energy storage systems.

- Leading Application Segment: Grid-scale energy storage dominates with 42.2% share, driven by utility-scale renewable integration, energy shifting, frequency regulation, and ancillary grid services.

- Fastest-Growing Product Segment: Solar-based integrated energy storage systems are the fastest-growing, enabled by combined PV generation, intelligent controls, peak shaving, and self-consumption optimization.

| Key Insights | Details |

|---|---|

|

Intelligent Energy Storage System Market Size (2026E) |

US$ 15.8 Bn |

|

Market Value Forecast (2033F) |

US$ 30.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.8% |

Market Dynamics

Growth Drivers

Renewable Energy Integration and Grid Intermittency Management

The integration of variable renewable energy sources, primarily solar and wind, into existing electrical grids presents both operational challenges and strategic opportunities for the Intelligent Energy Storage System Market. Global renewable energy capacity reached 3,372 GW in 2023, representing 260 percent cumulative growth since 2010, yet grid infrastructure adaptation remains inadequate to manage the inherent intermittency of these sources. In 2024, renewable energy additions surpassed 473 GW globally, with solar photovoltaic systems dominating deployment across China, the European Union, and the United States.

The variability introduced by renewable sources creates critical demand for intelligent storage solutions that can absorb excess generation during high-production periods and discharge energy during peak demand hours. Advanced energy storage systems have demonstrated an 85 percent cost reduction since 2010, making them economically viable for large-scale grid applications. Energy shifting, storing renewable energy during low market prices or excess production and releasing it during peak demand has become the primary use case, accounting for 67 percent of total capacity additions in 2024. This fundamental shift in grid operations requires sophisticated, AI-driven Intelligent Energy Storage Systems that can predict renewable generation patterns and optimise charge-discharge cycles in real time.

Government Policy Support and Regulatory Mandates

Regulatory frameworks and government incentives have emerged as critical catalysts for the Intelligent Energy Storage System Market expansion globally. In the United States, the Inflation Reduction Act (IRA) of 2022 established the investment tax credit (ITC) of 30 percent for standalone energy storage facilities, transforming project economics and accelerating deployment pipelines. The United States Energy Information Administration projects battery energy storage additions of 18.2 GW in 2025, representing the second-largest source of new utility-scale capacity after solar.

India's government has implemented Energy Storage Obligations (ESO), mandating that energy storage deployment increase from 1 percent in FY24 to 4 percent by FY30, with at least 85 percent of stored energy sourced from renewable resources. India's stated objective to achieve 500 GW of non-fossil capacity by 2030 and 50 percent of energy requirements from renewables by 2030 necessitates complementary energy storage infrastructure projected to expand from 82 GWh in 2026-27 to 2,380 GWh by 2047. Europe's evolving regulatory landscape, including enhanced state aid frameworks and flexibility assessments, is expected to accelerate deployment momentum from 2027 onwards.

These comprehensive policy frameworks establish market certainty and investment confidence, directly stimulating capital allocation toward Intelligent Energy Storage System projects across residential, commercial, and utility-scale applications.

Technological Advancement and Cost Reduction in Battery Systems

Successive generations of battery technology, coupled with manufacturing scale-up and supply chain optimisation, have substantially reduced the total cost of energy storage systems. Fully installed battery storage project costs declined by 93 percent between 2010 and 2024, from USD 2,571/kWh to USD 192/kWh. This dramatic cost trajectory reflects simultaneous improvements in multiple components: battery pack efficiency, power conversion systems, and balance-of-system components.

Lithium iron phosphate (LFP) chemistry now dominates new stationary storage installations, accounting for over 99 percent of deployed capacity in certain markets, due to superior cycle life, enhanced safety profiles, and cost competitiveness relative to nickel-based chemistries. Within the Intelligent Energy Storage System Market, cost reductions between 2023 and 2024 reached 38 percent for 2-hour systems and 32 percent for 4-hour systems, making grid-scale deployment economically viable even in markets without substantial subsidy support. Battery raw material costs, particularly lithium, nickel, and cobalt, have stabilised or declined as new mining and refining capacity came online, buffering against supply chain disruptions.

These technological and cost dynamics have expanded the addressable market for Intelligent Energy Storage Systems, enabling adoption across price-sensitive customer segments and extending application use cases from peak shaving and frequency regulation to energy arbitrage and renewable firming.

Market Restraining Factors

Grid Integration Technical Standards and Interconnection Bottlenecks

Despite rapid deployment, technical standards and grid interconnection remain significant barriers to accelerated Intelligent Energy Storage System Market penetration. Short Circuit Ratio (SCR) analysis indicates that certain grid nodes are characterised as "weak grids, where energy storage systems require advanced control schemes to maintain stability. Grid congestion in critical regions constrains renewable energy integration and limits energy storage deployment opportunities.

Permitting delays and interconnection queue backlogs, which exceed 10 years in certain U.S. jurisdictions, create project execution uncertainty and capital cost inflation. Legacy regulatory frameworks designed for centralised thermal generation remain inadequate for managing distributed energy storage resources and demand response coordination, requiring comprehensive regulatory reform.

Key Market Opportunities

Long-Duration Energy Storage and Grid-Forming Applications

Extended-duration storage solutions represent a high-growth opportunity within the Intelligent Energy Storage System Market, addressing a critical gap in current deployment patterns. While lithium-ion batteries dominate stationary applications, their economic viability is optimised for 2–4-hour durations. Grid scenarios with high renewable penetration require 8–12-hour or longer duration storage to address seasonal and multi-day renewable variability. Flow batteries, sodium-ion batteries, and hydrogen storage solutions are experiencing accelerated deployment and commercialisation.

India's National Electricity Plan projects long-duration storage requirements expanding from negligible levels in 2023 to hundreds of gigawatt-hours by 2035. In China, long-duration lithium-based C&I projects and all-vanadium redox flow batteries are witnessing accelerated deployment, signalling a strategic market shift. The global flow battery market is projected to expand by 2030, driven by recognition of scalability advantages and performance benefits over extended cycling horizons.

Grid-forming inverters and synthetic inertia capabilities represent an emerging technical requirement that creates product differentiation opportunities within the Intelligent Energy Storage System Market. As renewable penetration approaches 40-50 percent in leading markets, energy storage systems must transition from grid-following to grid-forming control paradigms, providing frequency regulation and voltage support services. This technical evolution drives premium valuations for systems incorporating advanced power electronics and control algorithms, favouring vendors with established capabilities in power systems and digital controls.

Behind-the-Meter and Distributed Energy Resource Integration

Commercial, industrial, and residential behind-the-meter (BTM) energy storage deployment represents a substantial market opportunity within the Intelligent Energy Storage System Market, driven by rising electricity costs, increasing reliability concerns, and favorable tax credit structures. In the United States, residential battery storage expanded by 608 MW in Q2 2025, representing a 132 percent year-over-year increase, driven by high attachment rates in distributed solar installations. Commercial and industrial (C&I) storage, while growing modestly at present, is accelerating due to programs such as Massachusetts' SMART 3.0 initiative.

In India, the shift from traditional lead-acid backup systems to sophisticated lithium-ion solutions is accelerating as costs decline and system intelligence improves, enabling demand charge management, peak shaving, and energy time-shifting for cost optimisation. The integration of distributed energy resources, combining behind-the-meter solar, storage, and smart controls with aggregation platforms, enables virtual power plant operations and participation in wholesale market services. Service-based delivery models, exemplified by ABB's Battery Energy Storage Systems-as-a-Service (BESS-as-a-Service) launched in May 2025, eliminate customer capital expenditure barriers and accelerate adoption by enabling deployment through operational expense structures.

Category-wise Analysis

Product Type Insights

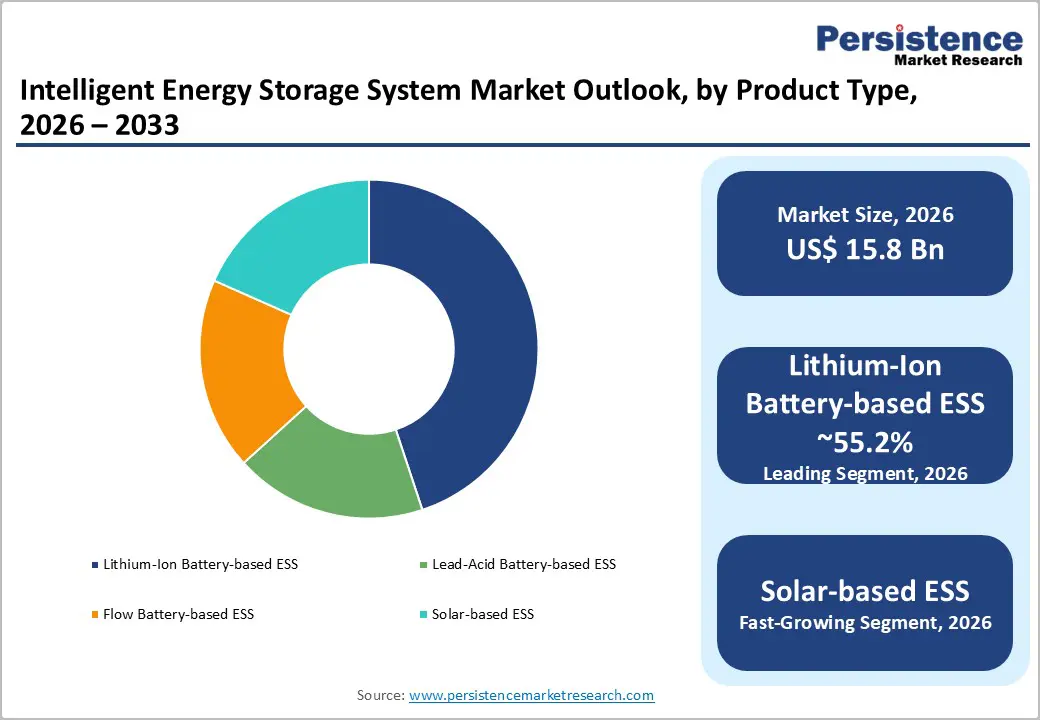

Lithium-ion battery-based energy storage systems maintain a commanding share of 55.2% within the Intelligent Energy Storage System Market, driven by superior performance characteristics, continuous cost reduction, and manufacturing maturity. Lithium iron phosphate (LFP) chemistry has emerged as the dominant technology for stationary applications, accounting for over 99 percent of newly deployed grid-scale capacity and 80 percent plus of residential and commercial systems. LFP chemistry advantages extended cycle life, enhanced safet, and cost competitiveness have established technological superiority relative to older nickel-based chemistries (NCA, NMC).

The 2024 Annual Technology Baseline (ATB) documents continued cost reductions across all LFP duration categories, with declining $/kWh metrics projected through 2050 across conservative, moderate, and advanced innovation scenarios. Lithium-ion systems continue advancing in energy density, charging speed, and safety features.

Recent developments include Johnson Controls' Lithium-Ion Risk Prevention System, providing integrated safety solutions with rapid off-gas detection and automatic battery stack shutdown to prevent thermal runaway. ABB's BESS-as-a-Service offering and strategic partnership with Grid Beyond integrate advanced hardware, software, and AI-driven lifecycle management to maximise asset value and operational efficiency.

Solar-based energy storage systems comprising integrated photovoltaic generation with battery storage and intelligent controls represent the fastest-growing product category within the Intelligent Energy Storage System Market. These systems address residential and commercial customer needs for maximised self-consumption, peak demand management, and grid independence. ABB's partnership with Humless exemplified this integration, delivering the solar industry's first intelligent all-in-one ESS capable of AC/DC coupling, load shaving, and time-of-use optimization.

Application Insights

Grid-scale energy storage holding a share of 42.2% represents the dominant application within the Intelligent Energy Storage System Market, driven by utility-scale renewable integration requirements and wholesale electricity market participation. The 42.2 percent market share reflects substantial capital deployment toward utility-scale battery storage projects, which provide essential grid services including frequency regulation, peak shaving, energy shifting, and renewable firming. In 2024, grid-scale installations reached 12,314 MW of power and 37,143 MWh of energy capacity globally, representing 33 percent and 34 percent year-over-year growth, respectively.

The United States deployed 4.9 GW of utility-scale capacity in Q2 2025 alone, sufficient to supply electricity to 3.7 million homes, with leading states including Texas, California, and Arizona each adding over 1 GW. Grid-scale applications benefit from regulatory tailwinds, including investment tax credits, renewable energy mandates, and market mechanisms recognising storage value provision for grid stability services. The economic profile of grid-scale systems has matured, enabling profitable deployment through energy arbitrage and ancillary services revenue without subsidy support in favourable markets.

Industrial energy storage applications are experiencing accelerated growth within the Intelligent Energy Storage System Market, driven by manufacturing cost reduction objectives, peak demand charge management, and renewable energy integration in energy-intensive facilities. Industrial applications leverage energy storage to reduce demand charges, which can constitute 30-50 percent of electricity costs for industrial users, enable time-shifting of production to off-peak pricing periods, and support on-site renewable generation utilisation.

Regional Insights and Trends

North America Market Trend

North America commands a significant share of 25.3% in the global Intelligent Energy Storage System Market, supported by mature regulatory frameworks, substantial renewable energy expansion, and favourable investment tax credit structures. The United States represents the largest North American market, where 2024 demonstrated record energy storage deployment: utility-scale capacity reached 26 GW, with 10.4 GW of new installations bringing battery storage to represent 2 percent of total utility-scale generating capacity.

The trajectory accelerated further in Q2 2025, setting new quarterly installation records and prompting multiple utilities to upgrade capacity procurement forecasts upward. The Inflation Reduction Act (IRA) of 2022, sustained through the One Big Beautiful Bill Act (OBBA), provides investment tax credits (ITC) of up to 50 percent for grid-scale storage projects beginning construction by 2032, provided foreign content thresholds are met. This regulatory certainty has stimulated substantial project pipeline development, particularly in high-renewable-penetration regions including Texas, California, and the Southwest Power Pool region.

Residential energy storage expanded 132 percent year-over-year in Q2 2025, driven by high attachment rates in distributed solar installations, larger-capacity systems, and premium pricing justified by grid reliability concerns in specific states. The regional market faces supply chain challenges following the implementation of Foreign Entity of Concern (FEOC) restrictions, which constrain battery cell sourcing from China and necessitate reliance on emerging U.S. manufacturing capacity that remains insufficient to meet current demand.

Domestic battery cell production is expanding but remains below the 16.5 GW five-year buildout threshold, creating potential growth constraints post-2027, absent accelerated domestic manufacturing capacity expansion.

East Asia Market Trend

East Asia dominates the global Intelligent Energy Storage System market with 40.1% share, driven predominantly by China's massive grid modernisation initiative and expanding renewable energy targets. China's government announced plans to deploy over 30 GW of energy storage by 2025, representing the world's largest deployment pipeline. November 2025 data indicated that cumulative user-side storage installations for the first eleven months of 2025 reached 39.5 GW, marking 28% year-over-year growth despite monthly deployment volatility.

Lithium iron phosphate (LFP) batteries accounted for over 99% of installed capacity, reflecting overwhelming market preference for this chemistry in both utility-scale and distributed applications. Regional dynamics within East Asia reveal substantial heterogeneity: Fujian province emerged as the leading center, contributing more than half of newly commissioned capacity, driven by the concentration of energy-intensive industries and well-developed local lithium battery supply chains incorporating power conversion systems, battery management systems, and energy management software.

Long-duration energy storage technologies are experiencing accelerated deployment in East Asia, with vanadium redox flow batteries and extended-duration lithium systems deployed for grid flexibility and peak-shaving applications. Technology innovation and cost reduction continue advancing rapidly within the region, supported by substantial government R&D investment and vertical integration of battery manufacturers with renewable developers.

Europe Market Trend

Europe accounts for approximately 15% of the global Intelligent Energy Storage System market. Europe's Intelligent Energy Storage System Market is experiencing robust growth supported by ambitious decarbonization targets and regulatory mandates for renewable energy integration. Europe installed nearly 12 GW of energy storage capacity in 2024, bringing cumulative installed capacity to 89 GW and marking a record year driven by both grid-scale front-of-the-meter (FTM) and behind-the-meter (BTM) deployments.

Growth has been uneven across segments: grid-scale storage expanded sharply due to grid flexibility requirements and renewable integration necessities, while behind-the-meter systems experienced moderation following the 2023 energy crisis peak and subsequent subsidy reductions. Electrochemical systems, predominantly lithium-ion batteries, represent the fastest-growing technology category, while legacy pumped-storage hydroelectricity continues to account for the largest share of cumulative installed capacity.

Competitive Landscape

The global Intelligent Energy Storage System (IESS) market is moderately consolidated, dominated by leading players such as ABB, Electrovaya, Eos Energy Enterprises, Johnson Controls, BSLBATT, and AmpereHour Energy. These companies offer a range of solutions, including grid-scale BESS, commercial and industrial ESS, and residential intelligent storage systems, often integrating AI-driven energy management and advanced battery technologies.

Market competition is driven by technology differentiation, service-based models like ABB’s BESS-as-a-Service, and proprietary platforms such as Eos Energy’s DawnOS and Electrovaya’s Infinity Technology. While a few large players control significant market share, regional and niche companies contribute to innovation, particularly in modular and scalable solutions. Strategic partnerships, joint ventures, and acquisitions are common, helping players expand deployment capabilities and enhance grid integration offerings.

Key Industry Developments

- September 9, 2025 – Electrovaya launched its next-generation Energy Storage Systems (ESS) featuring proprietary Infinity Technology, offering over 2MWh in a 20’ containerized format with enhanced safety, long cycle life, and lower lifecycle costs. Manufactured in the USA, the systems target grid support, renewable integration, microgrids, data centres, and behind-the-meter applications, while qualifying for U.S. Investment Tax Credits, reinforcing Electrovaya’s position in the growing stationary energy storage market.

- October 21, 2025 – Eos Energy partnered with Talen Energy to develop long-duration zinc-based battery energy storage systems across Pennsylvania aimed at supporting AI infrastructure and increasing grid reliability. The collaboration leverages Eos’ Z3 BESS technology and Talen’s generation assets to optimise capacity, provide scalable, safe, and U.S.-made energy storage, and accelerate clean energy adoption for utility-scale, commercial, and industrial applications.

Companies Covered in Intelligent Energy Storage System Market

- ABB

- Green Charge Networks

- Ampere Hour Energy

- NEC Energy Solutions

- CODA Energy

- Beacon Power Systems

- Green smith

- Bloom Energy

- BSLBATT

- Electrovaya

- Eos Energy Storage

- Johnson Controls

Frequently Asked Questions

The Global Intelligent Energy Storage System Market is projected to be valued at US$ 15.8 Bn in 2026.

The Industrial Energy Storage segment is expected to account for approximately 28.3% of the Global Intelligent Energy Storage System Market by Product Type in 2026.

The market is expected to witness a CAGR of 9.9% from 2026 to 2033.

The Intelligent Energy Storage System Market growth is driven by renewable energy integration and grid intermittency management, supportive government policies and regulatory mandates, and technological advancements with significant cost reductions in battery systems.

Key market opportunities in the Intelligent Energy Storage System Market lie in long-duration energy storage and grid-forming applications, behind-the-meter and distributed energy resource integration, and service-based deployment models that enable cost-effective adoption.

Key players in the Intelligent Energy Storage System Market include ABB, Electrovaya, Eos Energy Enterprises, Johnson Controls, BSLBATT, and AmpereHour Energy.