- Oil & Gas

- Floating Storage & Regasification Unit Market

Floating Storage & Regasification Unit Market Size, Share, and Growth Forecast 2026 - 2033

Floating Storage & Regasification Unit Market by Construction Type (New Build FSRUs, Converted FSRUs), Storage Capacity (< 150,000 m³, 150,000 - 180,000 m³, > 180,000 m³), Deployment Type (Fixed Mooring, Multi-Point Mooring, Near-shore), End-user (Power Generation Utilities, Oil & Gas Companies, Industrial Consumers, Transport & Marine Operators, Commercial, Others), Regional Analysis, 2026 - 2033

Floating Storage & Regasification Unit Market Size and Trend Analysis

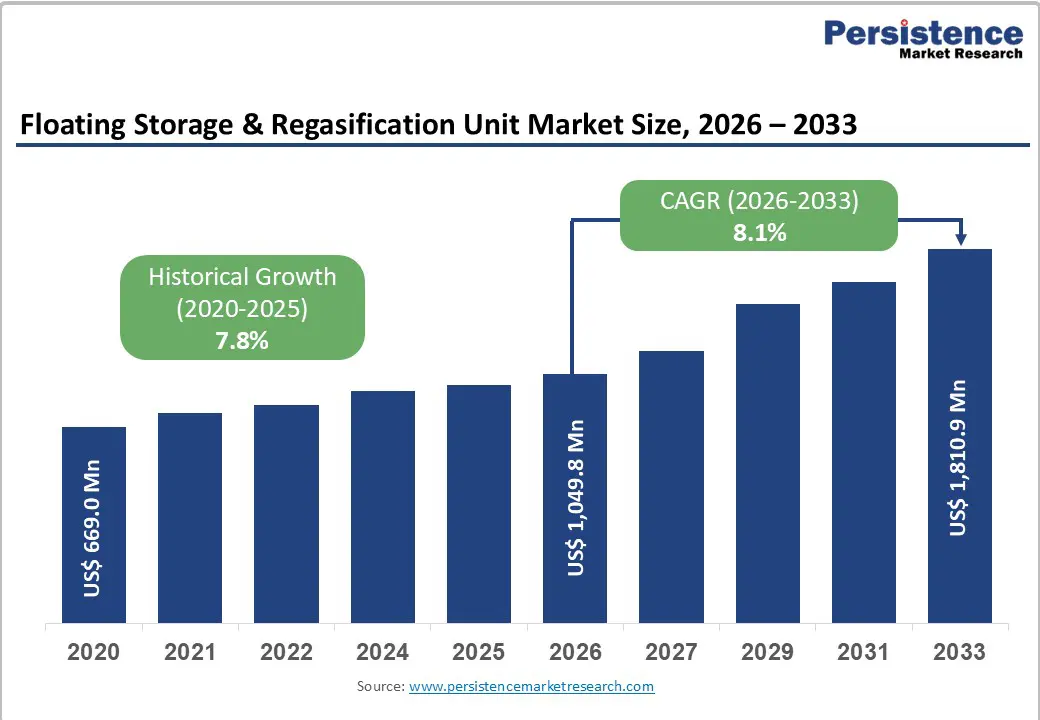

The global floating storage & regasification unit market is expected to reach US$ 1,049.8 million in 2026 and is projected to reach US$ 1,810.9 million by 2033, growing at a CAGR of 8.1% over 2026-2033.

Market expansion is driven by rising global demand for liquefied natural gas (LNG), with FSRUs providing flexible regasification infrastructure when onshore terminals face delays. Surging LNG imports in emerging economies, cost advantages of floating units over fixed terminals, and historical growth at 7.8% CAGR from 2020 to 2025 highlight the impact of the energy transition. Decarbonization policies and energy security need further boost in adoption.

Key Industry highlights:

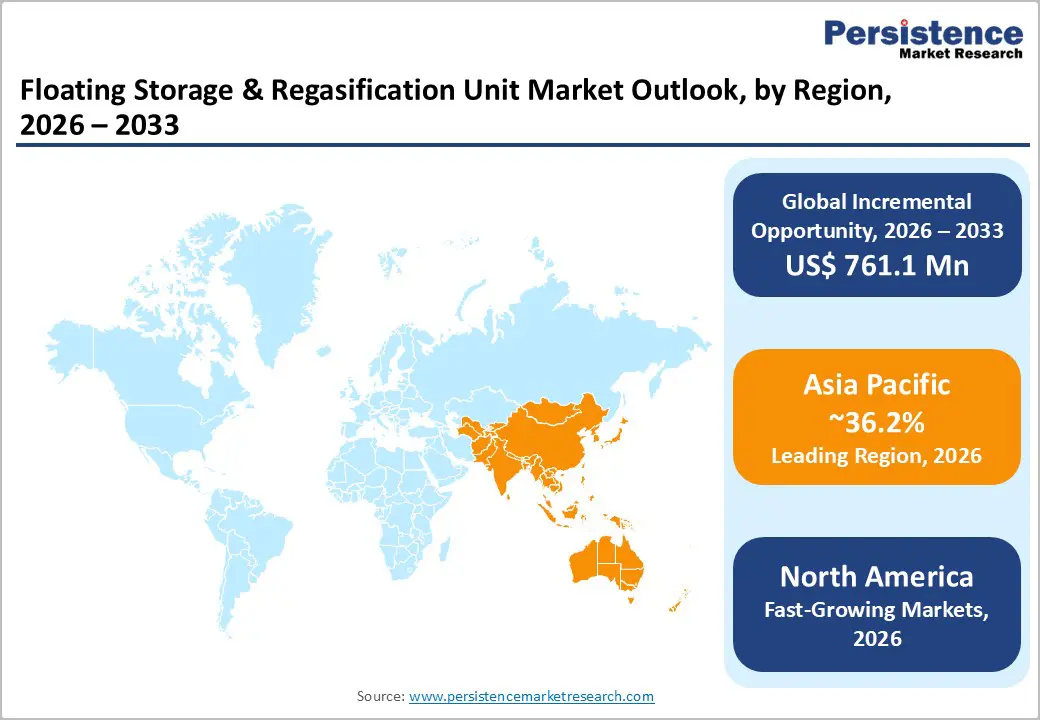

- Leading Region: Asia Pacific leads with 36.2% share in 2025, driven by LNG import growth in China and India.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with ~9% CAGR, supported by manufacturing advantages and policy incentives.

- Leading Construction Type: Converted FSRUs dominate with 65% share in 2025, favored for cost-efficiency and rapid deployment.

- Leading Storage Capacity: The 150,000-180,000 m³ segment holds 60% share in 2025, balancing capacity and operational efficiency for mid-scale imports.

- Key Opportunity: Near-shore hybrid FSRUs are rising in adoption, supporting power projects with a 35% increase in awards.

| Key Insights | Details |

|---|---|

| Floating Storage & Regasification Unit Size (2026E) | US$ 1,049.8 million |

| Market Value Forecast (2033F) | US$ 1,810.9 million |

| Projected Growth CAGR (2026 - 2033) | 8.1% |

| Historical Market Growth (2020 - 2025) | 7.8% |

Market Dynamics

Drivers - Rising Global Demand for Liquefied Natural Gas Accelerates FSRU Adoption

The surging global consumption of LNG is driving demand for Floating Storage & Regasification Units (FSRUs), as countries look for rapid regasification solutions amid ongoing energy transitions. LNG trade volumes reached unprecedented levels in 2024, with Asia-Pacific imports alone surpassing 200 million tonnes, highlighting the crucial role of FSRUs in quickly meeting growing energy needs.

Converted FSRUs offer a cost-effective alternative, providing 30-50% lower capital expenditures compared to traditional onshore terminals. Utilities and governments can efficiently address peak demand periods and enhance energy supply security. At the same time, flexible deployment allows operators to respond quickly to fluctuating market conditions and global LNG trade patterns.

Cost-Effectiveness and Operational Flexibility of FSRUs Propel Market Growth

FSRUs offer significant economic advantages through mobility and shorter construction timelines, making them highly attractive for LNG importers. Deployment of a floating terminal typically takes 18-24 months, compared to 4-5 years for land-based facilities, allowing companies to quickly enter new markets and respond to rising energy demands.

This flexibility also enables operators to capitalize on volatile gas prices and shifting demand patterns. Approximately 80% of new regasification projects in import-dependent regions now favor FSRUs, reflecting their ability to reduce financial risk, optimize operational efficiency, and support the growing transition toward cleaner energy sources.

Restraints - High Initial Capital Expenditure and Elevated Operational Costs Limit FSRU Adoption

The substantial upfront investment required for FSRUs acts as a major restraint, particularly for smaller or emerging LNG markets. New-build FSRU units often exceed US$ 300 million each, posing significant financial barriers and limiting the ability of some nations and private operators to deploy floating regasification infrastructure.

Harsh marine environments contribute to elevated maintenance and operational expenses, increasing annual costs by 20-30%, according to DNV reports. These financial pressures reduce scalability and deter rapid fleet expansion, particularly in regions with unpredictable LNG demand or where cost-sensitive project economics are critical, thereby slowing overall market penetration.

Stringent Regulatory and Environmental Challenges Hinder FSRU Deployments

FSRU projects face complex regulatory hurdles and environmental compliance requirements that can slow market growth. International Maritime Organization (IMO) methane emission standards and local environmental mandates necessitate costly technology upgrades, such as advanced vaporizers and emission control systems, adding both time and expense to projects.

Approval and permitting processes often extend project timelines by 12-18 months, particularly in sensitive coastal zones. These delays impact operational efficiency and discourage rapid deployment, making it challenging for developers to meet growing LNG demand, while also increasing the financial and logistical risks associated with new FSRU installations.

Opportunity - Rapid Expansion of FSRU Storage Capacity in Emerging Markets Offers Significant Growth Potential

The fastest-growing FSRU segment, with storage capacities of 150,000-180,000 m³, presents substantial market opportunities, accounting for approximately 84% of value share toward the latter part of the forecast period, according to Persistence Market Research. Emerging economies are increasingly adopting floating regasification infrastructure to meet rising LNG demand.

Countries such as India and Bangladesh are planning multiple FSRU installations to support LNG imports, with floating units expected to contribute around 20% of total gas supply. This trend underscores the potential for accelerated investment, increased fleet deployment, and regional energy security, positioning emerging markets as key drivers of global FSRU growth over the coming decade.

Hybrid LNG-to-Power Projects Drive FSRU Integration and Value Addition

Near-shore FSRU deployments are enabling hybrid LNG-to-power solutions, combining regasification with electricity generation. The number of hybrid project awards has risen by approximately 35%, reflecting growing interest in integrated energy infrastructure that maximizes operational efficiency and asset utilization.

Europe and Asia lead these developments, leveraging carbon capture and storage technologies to ensure compliance with stringent decarbonization regulations, particularly under EU mandates. These projects not only expand LNG consumption opportunities but also create long-term value for investors, enhance energy reliability, and strengthen the role of FSRUs in sustainable power generation strategies.

Category-wise Analysis

Construction Type Insights

Converted FSRUs lead the market with a 65% share in 2025, driven by cost-efficiency and rapid availability from existing LNG carrier fleets. Persistence Market Research emphasizes their dominance due to 30-50% lower capital costs compared to new-build units, allowing operators to respond quickly to demand spikes. Their proven reliability across diverse marine conditions makes them the preferred choice for most regions.

The fastest-growing segment is new-build FSRUs, driven by increasing demand for specialized, high-capacity floating terminals. These units are designed with optimized storage and regasification systems, advanced safety technologies, and higher efficiency, catering to long-term strategic LNG import projects and regions requiring purpose-built solutions for expanding energy infrastructure.

Storage Capacity Insights

The 150,000-180,000 m³ storage capacity segment dominates with a 60% share in 2025, balancing large-scale LNG handling with maneuverability for major ports. It provides optimal economics for mid-scale LNG imports and is projected to capture 84% of long-term market value. Asia-Pacific hubs handling 5-7 MTPA flows particularly favor this capacity range for operational efficiency.

The fastest-growing storage segment lies above 180,000 m³, responding to rising LNG import volumes and mega-scale energy projects. These high-capacity units allow operators to store and regasify larger LNG volumes, reduce the frequency of shipments, and serve high-demand industrial zones or national gas grids efficiently, meeting future energy consumption needs.

Deployment Type Insights

Multi-Point Mooring (MPM) dominates with a 55% share in 2025, offering stability in deep waters via buoy systems. Bluewater MPM solutions enable weathervaning for safe offloading and reduce downtime by approximately 70% in offshore locations. The configuration is preferred in 80% of new projects, particularly where port congestion is a challenge, ensuring smooth LNG operations in diverse marine environments.

The fastest-growing deployment type is near-shore or jetty-mounted FSRUs, which are easier to connect to pipelines and shore infrastructure. These installations are gaining traction in emerging LNG import markets, providing cost-effective, rapid deployment options and supporting integrated LNG-to-power and industrial gas supply projects in coastal regions.

End-user Insights

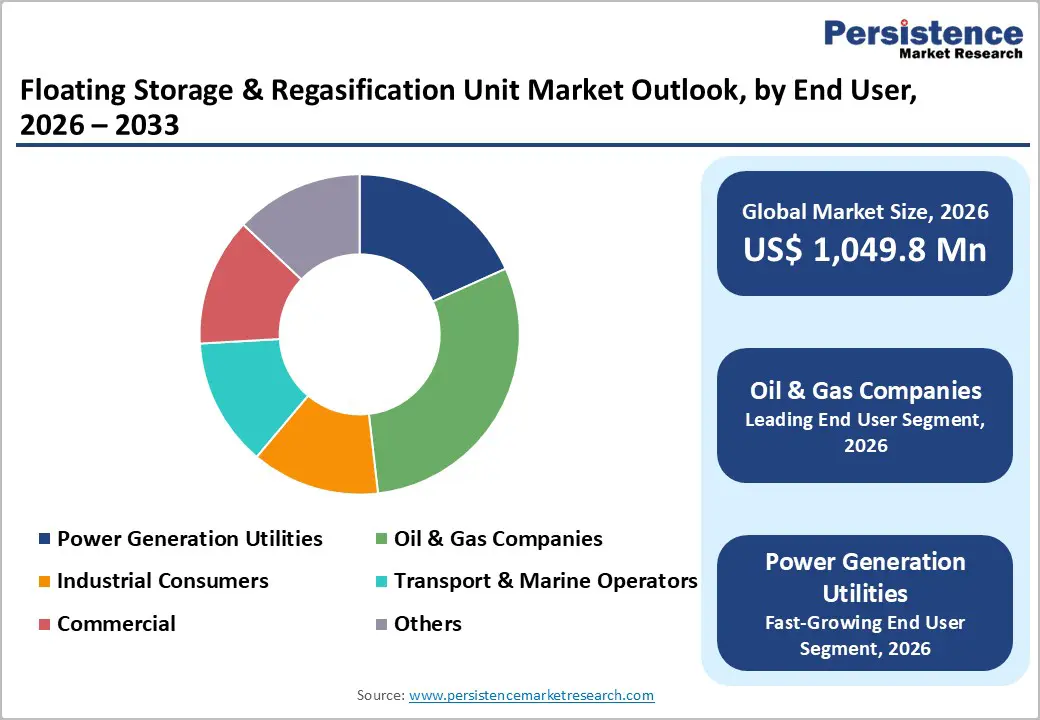

Oil & gas companies lead with a 45% share in 2025, driving FSRU adoption for offshore processing and storage. They contribute around 45.6% of hydrocarbons revenue, leveraging FSRUs’ mobility to establish flexible LNG export hubs and efficiently support global trading operations. Their operational experience also ensures optimal utilization and reliability in complex offshore environments. The fastest-growing end-user segment is power generation and utilities. Increasing LNG-to-power projects, peak-shaving needs, and industrial energy requirements are prompting these users to adopt FSRUs for reliable, scalable, and short-term deployment solutions, particularly in emerging markets and coastal regions aiming to transition to cleaner energy sources.

Regional Insights

North America Floating Storage & Regasification Unit Market Trends

North America is a key FSRU market, with the U.S. leading deployment through Gulf Coast export terminals supplying small-scale LNG to Caribbean markets. FERC regulations support peak-shaving operations, and the DOE has approved over 10 projects since 2024. Innovation in LNG bunkering and flexible floating infrastructure strengthens the region’s strategic energy position.

FSRUs in North America account for approximately 32.8% of the global market share, reflecting their critical role in meeting domestic and regional LNG demand. Growing focus on energy security and operational flexibility continues to attract investments, particularly for rapid-response import and export solutions, making floating regasification infrastructure a core component of North American LNG strategy.

Europe Floating Storage & Regasification Unit Market Trends

Europe has significantly increased FSRU adoption following the Ukraine crisis, with Germany and the U.K. deploying multiple units and chartering over 10 by 2025. Harmonization of EU regulations through the TEN-E program supports cross-border LNG infrastructure, while France and Spain add capacity to handle 20 bcm/year. Sustainability and energy transition goals are major growth drivers.

The European FSRU market is projected to grow at a CAGR of 8.2%, driven by the need for flexible LNG import capacity to diversify supplies. Regional initiatives focus on low-carbon operations, integrating floating terminals with carbon capture and hybrid LNG-to-power projects, positioning Europe as a high-demand, technologically advanced FSRU market.

Asia Pacific Floating Storage & Regasification Unit Market Trends

Asia Pacific dominates the global FSRU market, accounting for approximately 36.2% share in 2025, fueled by rapid LNG demand in China and India. India’s Jaigarh terminal is operational, supporting domestic energy needs, while ASEAN countries leverage FSRUs to reduce infrastructure costs by up to 20%. Strategic deployment in manufacturing and power sectors drives adoption across the region.

The region benefits from large-scale LNG imports, cost-efficient floating solutions, and rapid deployment capabilities. FSRUs enable governments to meet growing industrial, residential, and power-sector demand, providing flexibility for expanding LNG infrastructure and reinforcing Asia Pacific’s position as the world’s leading market for floating regasification units.

Competitive Landscape

The FSRU market is highly consolidated, with leading players focusing on strategic fleet management that combines converted and new-build units. Companies prioritize innovation and R&D, developing solutions for decarbonization, including advanced carbon capture systems, while expanding their presence through charter contracts and new project deployments. Key differentiators include cutting-edge mooring technologies that enable successful redeployment of units across different regions. Emerging FSRU models increasingly integrate hybrid power solutions, enhancing operational efficiency, flexibility, and sustainability. This focus on technological advancement and adaptable infrastructure strengthens competitive positioning and ensures long-term growth in the global FSRU market.

Key Developments:

- In June 2024, Höegh LNG deployed the Hoegh Galleon FSRU in Egypt for EGAS, strengthening LNG supply security amid a surge in imports. The deployment enabled rapid regasification capacity and supported the nation’s energy stability and infrastructure expansion.

- In May 2025, Egypt received a second FSRU from Höegh LNG, increasing import capacity by 4 bcm/year. This addition enhanced gas supply reliability, facilitated consistent energy distribution, and strengthened Egypt’s position in regional LNG trade, addressing growing domestic demand efficiently.

- In 2024, India commissioned the Jaigarh FSRU by H-Energy to supply key LNG imports. The unit improved operational flexibility, accelerated LNG distribution to domestic markets, and supported India’s ongoing energy transition and growing industrial and power-sector requirements.

Companies Covered in Floating Storage & Regasification Unit Market

- Höegh LNG Holdings Ltd.

- Excelerate Energy Inc.

- Golar LNG Limited

- BW Gas Limited

- Exmar NV

- Samsung Heavy Industries Co., Ltd.

- Hyundai Heavy Industries Co., Ltd.

- Daewoo Shipbuilding & Marine Engineering Ocean

- Hudong-Zhonghua Shipbuilding

- Keppel Offshore & Marine

- Seatrium

- Mitsui O.S.K. Lines

- Kawasaki Heavy Industries, Ltd.

- Maran Gas Maritime

- New Fortress Energy

Frequently Asked Questions

The global FSRU market is expected to reach US$ 1,049.8 million in 2026, reflecting rising LNG trade and growing demand for flexible regasification infrastructure worldwide.

Market growth is propelled by increasing global LNG demand and the cost-effectiveness of FSRUs, which offer faster deployment and lower capital expenditure compared to traditional onshore terminals.

Asia Pacific leads with 36.2% share in 2025, driven by high LNG import volumes in China, India, and ASEAN nations, along with supportive policies and expanding energy infrastructure.

Near-shore hybrid LNG-to-power projects are a major growth opportunity, with a 35% increase in project awards, enabling efficient energy distribution and integration with local power and industrial needs.

Leading firms include Höegh LNG, Excelerate Energy, Golar LNG, BW LNG.