- Inks, Coatings, Adhesives & Sealants (ICAS)

- Silicone Sealants Market

Silicone Sealants Market Size, Share, and Growth Forecast, 2025 - 2032

Silicone Sealants Market By Cure Chemistry (RTV Neutral-Cure, Acetoxy-Cure, Others), Application (Construction, Automotive, Others), Product Form and Regional Analysis for 2025 - 2032

Silicone Sealants Market Size and Trends Analysis

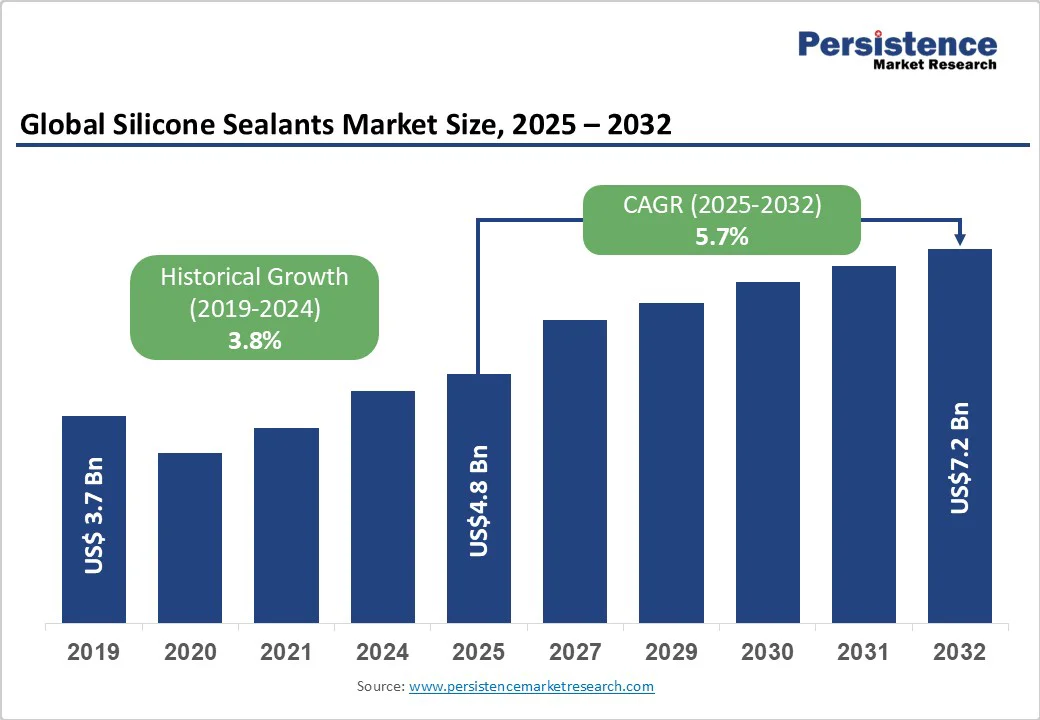

The global silicone sealants market size is likely to be valued at US$4.8 Bn in 2025 and is expected to reach US$7.2 Bn by 2032, growing at a CAGR of 5.7% during the forecast period from 2025 to 2032, driven by increased demand in construction, automotive, and electronics applications, combined with the rising shift toward energy-efficient and low-VOC products.

Advancements in formulation chemistry and automated cartridge filling enhance efficiency and scalability. The market remains moderately consolidated, led by global players such as Dow, Wacker, Shin-Etsu, Momentive, and Elkem, while regional formulators in Asia and Europe gain ground in niche construction segments.

Key Industry Highlights

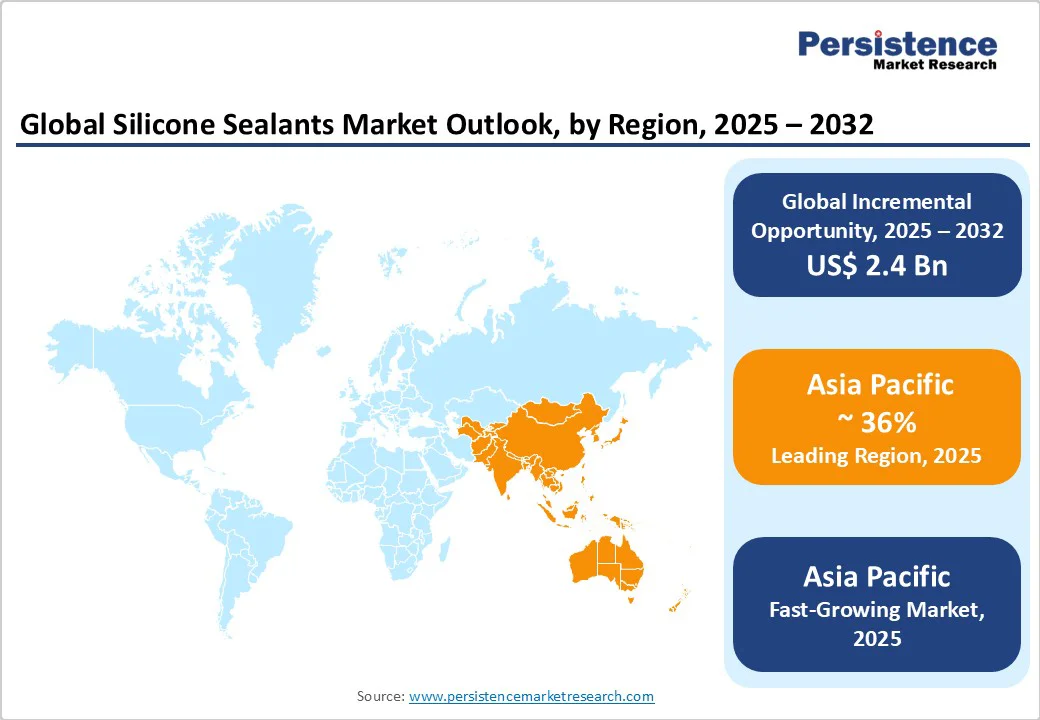

- Leading Region: Asia Pacific, accounting for approximately 36% of market share in 2025, driven by construction, electronics, and industrial manufacturing.

- Fastest-Growing Region: Asia Pacific, projected 7% CAGR through 2032, fueled by urbanization, EV manufacturing, and renewable-energy applications.

- Investment Plans: Expansion of regional manufacturing and R&D facilities, including Sika’s Pune plant (India, 2024), Dow’s Zhangjiagang expansion (China, 2023), and Wacker’s Nanjing silicone facility (China, 2023).

- Dominant Cure Chemistry: RTV neutral-cure silicones, holding around 38% market share, widely used in construction, glazing, and sanitary applications.

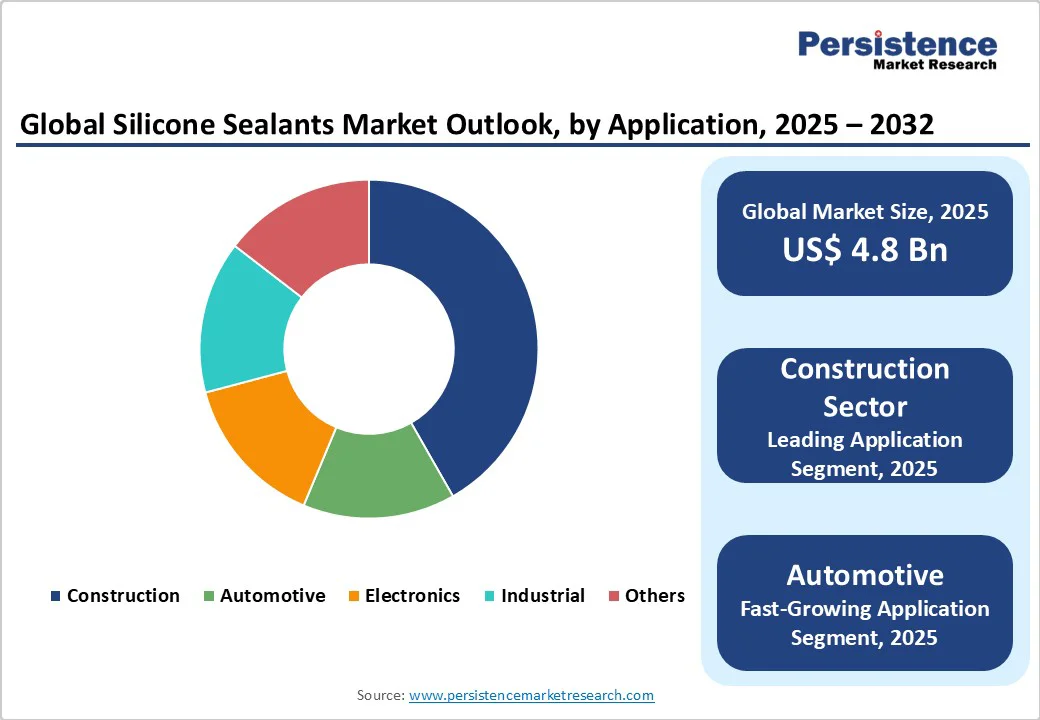

- Leading Application: Construction sector, contributing approximately 43% of the total revenue, with applications in façades, curtain walls, and energy-efficient building envelopes.

| Key Insights | Details |

|---|---|

| Silicone Sealants Market Size (2025E) | US$4.8 Bn |

| Market Value Forecast (2032F) | US$7.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Surge in Construction And Retrofit Activity

Global construction growth, particularly in urban housing and commercial retrofitting, remains the largest driver for silicone sealants. These sealants are critical in façade systems, insulating glass units, and structural glazing, offering durability, UV stability, and resistance to extreme temperature variations.

Construction applications account for over one-third of total demand, and the growing focus on green-building certifications is accelerating the use of neutral-cure and low-emission formulations. This steady expansion supports high baseline consumption and ensures consistent long-term procurement contracts for established manufacturers.

Electrification and Demand for High-Performance Materials

The transition toward electric vehicles, renewable energy, and consumer electronics is reshaping the silicone sealant landscape. High-temperature, dielectric, and thermally conductive silicones are increasingly preferred for battery pack assembly, power module sealing, and photovoltaic (PV) systems.

Manufacturers are investing in specialty formulations with higher purity and performance characteristics, commanding premium prices. The electronics and EV sectors are projected to grow at nearly double the overall market rate, creating a significant value-addition opportunity for producers capable of meeting stringent OEM specifications.

Sustainability and Regulatory Alignment

Tighter environmental regulations in North America and Europe, coupled with stricter indoor air quality standards, have accelerated the development of low-VOC, neutral-cure, and solvent-free silicone sealants. Governments and construction authorities increasingly mandate products certified under programs such as LEED and BREEAM.

The trend toward environmentally responsible materials is pushing manufacturers to invest in greener chemistry and transparent product declarations. Companies achieving regulatory compliance and certification enjoy enhanced brand preference and improved access to large institutional contracts.

Barrier Analysis - Volatility in Raw Material Prices

Silicone sealants depend on intermediates such as siloxanes and chlorosilanes, derived from energy-intensive manufacturing processes. Fluctuations in energy prices and supply-chain bottlenecks can significantly affect margins. Feedstock price surges of up to 30 % in certain quarters have been observed historically, directly impacting production costs and profitability. The market’s dependence on a few global suppliers creates additional vulnerability. Companies are responding through backward integration, strategic partnerships, and cost-pass-through mechanisms to stabilize operations.

Lengthy Product Qualification Cycles

In sectors such as automotive electronics and PV modules, new silicone formulations must undergo extended validation and certification processes lasting up to two years. This delays market entry for smaller or emerging players and reinforces the dominance of established suppliers with accredited laboratories and testing capabilities. High qualification costs limit the ability of smaller firms to innovate rapidly. The challenge emphasizes the need for collaborative testing programs and faster approval frameworks to accelerate commercialization.

Opportunity Analysis - Expansion in EV and Electronics Sealants

The electrification trend across transportation and energy systems is opening strong growth potential for specialty silicone sealants with superior dielectric strength and thermal resistance. The EV and power electronics subsegment is projected to grow between 8 % and 12 % CAGR, surpassing overall market performance.

These advanced sealants ensure durability and safety in high-temperature or high-voltage environments. Companies focusing on customized formulations and co-development with OEMs are expected to capture premium, long-term supply contracts and higher margins.

Asia Pacific Manufacturing and Local Formulation Advantage

Asia Pacific has become the largest and fastest-growing regional market, driven by rapid urbanization, industrialization, and government infrastructure spending in countries such as China, India, and Indonesia. Establishing regional manufacturing plants and cartridge-filling facilities significantly reduces lead times and shipping costs.

The region accounts for 30 %-40 % of global consumption, with domestic formulators increasingly competitive on cost and customization. Multinational companies expanding their local presence are achieving faster market access and improved profitability.

Category-wise Analysis

Cure Chemistry Type Insights

Continuous advancements in formulation chemistry and automated cartridge-filling technologies are transforming the silicone sealants industry by improving production efficiency, product consistency, and scalability. These innovations allow manufacturers to develop high-performance formulations with enhanced adhesion, durability, and resistance to environmental stress.

Automation has also reduced production time and waste, optimizing material utilization and lowering operational costs. As a result, companies can better meet the rising demand for sustainable and high-strength sealants across construction, automotive, and industrial applications. Moreover, the integration of smart manufacturing systems and precision dosing equipment supports tighter quality control, ensuring superior end-product reliability.

The global silicone sealants market exhibits moderate consolidation, with a few multinational producers, such as Dow, Wacker, Shin-Etsu, Momentive, and Elkem, dominating supply chains and setting technological benchmarks. These key players leverage their R&D capabilities and vertical integration to deliver innovative solutions tailored to regional performance standards and sustainability goals.

Meanwhile, regional formulators in Asia and Europe are expanding their presence in specialized and local construction segments, focusing on customized solutions, cost competitiveness, and flexible distribution networks. This evolving market landscape balances global scale with local expertise, fostering innovation and responsiveness to diverse industry needs.

Application Insights

The construction sector accounts for about 43% of global silicone sealant revenue, driven by applications in weatherproofing, structural adhesion, and insulation across curtain walls, windows, joints, and façades. Their elasticity, UV stability, and moisture resistance make them vital for sustainable construction.

Growing emphasis on energy-efficient, green buildings under LEED (U.S.) and BREEAM (Europe) standards fuels demand for low-VOC, neutral-cure formulations. Products such as Sika’s Sikasil® SG-550 and Wacker’s Elastosil® 895, certified for environmental performance, are widely used in modern high-rise and façade applications.

The automotive industry is emerging as the fastest-growing application segment. In the automotive sector, sealants are used for EV battery housing, lighting assemblies, and ADAS sensor modules. Major OEMs such as Tesla, Toyota, and BMW rely on silicone-based materials to enhance component longevity and prevent thermal degradation. Elkem’s Bluesil™ and Dow’s DOWSIL™ EA-7100 adhesives are examples designed for high-thermal-cycling and low-pressure molding processes in EV manufacturing.

Regional Insights

North America Silicone Sealants Market Trends - Infrastructure Spending, Energy Retrofits & EV Boom Fuel Demand

North America maintains a strong position in the global silicone sealants market. Growth is underpinned by extensive infrastructure investment, robust residential and commercial renovation cycles, and expanding clean-energy initiatives. The United States remains the primary driver, supported by demand in glazing, curtain walls, weatherproofing, HVAC systems, and renewable-energy applications.

Regulatory support remains a key market catalyst. EPA’s VOC reduction programs, combined with state-level initiatives in California and New York, have accelerated the shift toward low-VOC and solvent-free formulations.

The U.S. Department of Energy’s Weatherization Assistance Program and federal infrastructure funding under the Infrastructure Investment and Jobs Act (IIJA) are spurring energy-efficiency retrofits, further boosting silicone sealant consumption in building envelopes and insulation systems.

The region’s growing EV and battery-manufacturing ecosystem, with major plants from Tesla, Ford, and General Motors, is driving demand for thermally stable, electrically insulating sealants in module assembly and battery protection.

Europe Silicone Sealants Market Trends - Sustainability Regulations & Green Innovation Drive Market Evolution

Europe remains one of the most innovation-intensive and regulation-driven regions in the silicone sealants industry. Key markets include Germany, the U.K., France, Italy, and Spain, each exhibiting unique growth dynamics driven by urban regeneration, energy-efficient building design, and manufacturing modernization. The European market’s defining characteristic is its focus on sustainability and safety compliance.

Regulatory frameworks such as REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals) and the EU Construction Products Regulation (CPR) have pushed producers toward solvent-free, low-VOC, and bio-based formulations. This transition aligns with the European Green Deal and the continent’s 2050 carbon-neutral target, ensuring silicone sealants play a crucial role in high-performance building envelopes and long-life façade systems.

Germany continues to lead in production and export, with firms such as Wacker Chemie AG and Sika AG driving product innovation. Wacker’s 2024 launch of GENIOSIL® XB series hybrid silicone sealants, designed to combine mechanical strength with environmental compliance, reflects the region’s sustainability-driven R&D approach. Similarly, Henkel’s 2023 investment in its Düsseldorf Innovation Center has enhanced testing and formulation capabilities for silicone and hybrid adhesives tailored for industrial and construction applications.

Asia Pacific Silicone Sealants Market Trends - High Growth Led by Construction, Electronics & Local Manufacturing Scale

The Asia Pacific (APAC) region represents the largest and fastest-growing silicone sealants market, accounting for approximately 36% of global consumption in 2025 and projected to reach nearly 45% by 2032. The region’s expansion is driven by rapid industrialization, urban infrastructure investment, and manufacturing scalability. China dominates both production and consumption, supported by its expansive construction and electronics sectors.

Major local producers such as Huitian New Materials, Guangzhou Baiyun Chemical Industry, and Chengdu Guibao Science & Technology are expanding manufacturing capacity to serve domestic and export markets. In 2024, Huitian announced a new 30,000-ton per-year RTV silicone facility in Hubei province to meet growing demand from renewable-energy and electronics customers.

Japan and South Korea remain leaders in high-performance silicone applications, particularly in electronics, automotive, and semiconductor manufacturing. Companies such as Shin-Etsu Chemical Co. Ltd. and KCC Corporation continue to innovate in thermally conductive and optically clear silicone sealants for EVs, displays, and solar modules.

Asia Pacific offers cost-efficient raw material access, skilled labor, and well-established supply networks, which have made it a preferred base for both global and domestic producers. Continued demand from infrastructure megaprojects, solar power installations, and EV supply-chain expansion is expected to sustain this trajectory.

Dow’s 2023 capacity expansion in Zhangjiagang, China, is to enhance silicone intermediates supply for sealants and elastomers. Elkem ASA’s new R&D center in Shanghai (2024) focuses on silicone innovations for electronics and construction markets. Wacker’s 2023 launch of a silicone plant in Nanjing, aimed at supporting regional demand for industrial and construction sealants.

Competitive Landscape

The global silicone sealants market is moderately consolidated. Global chemical producers dominate high-performance and specialty segments due to strong R&D capabilities, backward integration into siloxane intermediates, and established global supply networks.

Regional manufacturers compete in standard construction and consumer channels, often leveraging pricing and local distribution. Market concentration is higher in electronics and automotive applications, while construction sealants remain more fragmented.

Competitive differentiation primarily relies on product innovation, sustainability certifications, and customer technical service. Market leaders are pursuing innovation-driven specialization, targeting growth in EV, renewable energy, and advanced electronics.

Strategies emphasize sustainability credentials, localized production, and co-development partnerships with OEMs. Competitive success increasingly depends on integrating formulation expertise with agile regional supply chains.

Companies Covered in Silicone Sealants Market

- Dow Inc.

- Wacker Chemie AG

- Momentive Performance Materials Inc.

- Sika AG

- Elkem ASA

- 3M Company

- Henkel AG & Co. KGaA

- Shin-Etsu Chemical Co., Ltd.

- Evonik Industries AG

- H.B. Fuller Company

- BASF SE

- RPM International Inc.

- General Electric (GE)

- Tremco Incorporated

- Arkema S.A.

- ITW Performance Polymers

- KCC Corporation

- Avery Dennison Corporation

- McCoy Soudal Sealants Adhesives & Foams Pvt. Ltd.

- Dow Corning Corporation

Frequently Asked Questions

The silicone sealants market size is estimated at US$4.8 Billion in 2025, driven by steady construction recovery, infrastructure development, and growing adoption in automotive and electronics applications.

By 2032, the market is projected to reach US$7.2 Billion, reflecting sustained industrial expansion, technological innovation, and wider usage of high-performance, eco-compliant materials.

Key trends include the adoption of low-VOC and neutral-cure formulations, growing use in EVs and renewable-energy systems, increased automation in dispensing, and expanding R&D and manufacturing capacities in Asia Pacific, reshaping global supply dynamics.

The construction segment leads the market, contributing around 45% of total revenue, supported by façade systems, glazing applications, and large-scale renovation projects worldwide.

The silicone sealants market is expected to grow at a CAGR of 5.7% from 2025 to 2032.

Major players include Dow Inc., Wacker Chemie AG, Momentive Performance Materials Inc., Sika AG, and Elkem ASA.