- Bulk Chemicals

- Europe Silicone Market

Europe Silicone Market Size, Share, and Growth Forecast, 2026 - 2033

Europe Silicone Market by Product Type (Elastomer, Fluids, Resins, and Gels), Industry (Construction, Transportation, Electronics, Healthcare, Consumer Products, Industrial, and Others), and Regional Analysis for 2026 - 2033

Europe Silicone Market Size and Trends Analysis

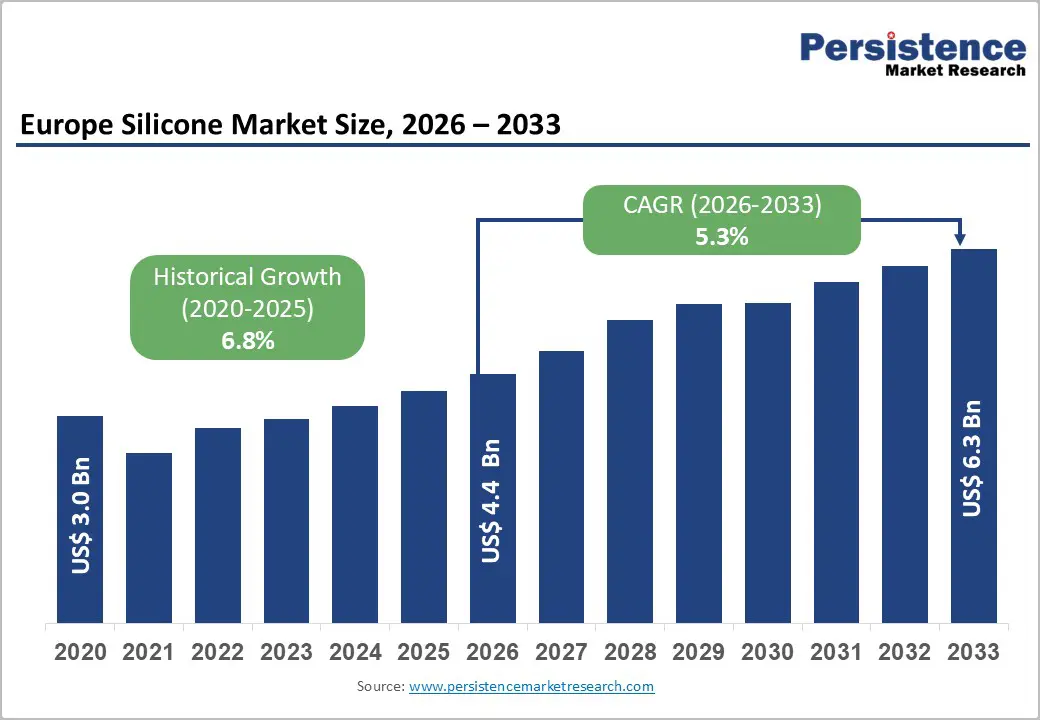

The Europe silicone market size was valued at US$ 4.4 billion in 2026 and is projected to reach US$ 6.3 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. The market reflects a strong structural demand in construction, transportation, electronics, and healthcare.

Segments such as elastomer-based products, construction applications, and Germany as the lead country anchor current revenues, while fluids, transportation uses, and France exhibit above-average growth momentum. Market growth is characterized by broad-based industrial demand across construction sealants, automotive gaskets and thermal materials, electrical insulation, and personal care formulations. Rising investment in building energy efficiency, vehicle electrification, and advanced electronics is shifting the product mix toward higher-value elastomers and specialty fluids, supporting margin resilience despite cyclical headwinds. Simultaneously, tightening environmental and chemical regulations under EU frameworks such as REACH are encouraging innovation in low-VOC, bio-based and carbon-reduced silicone solutions, reinforcing the strategic role of leading European producers.

Key Industry-Highlights:

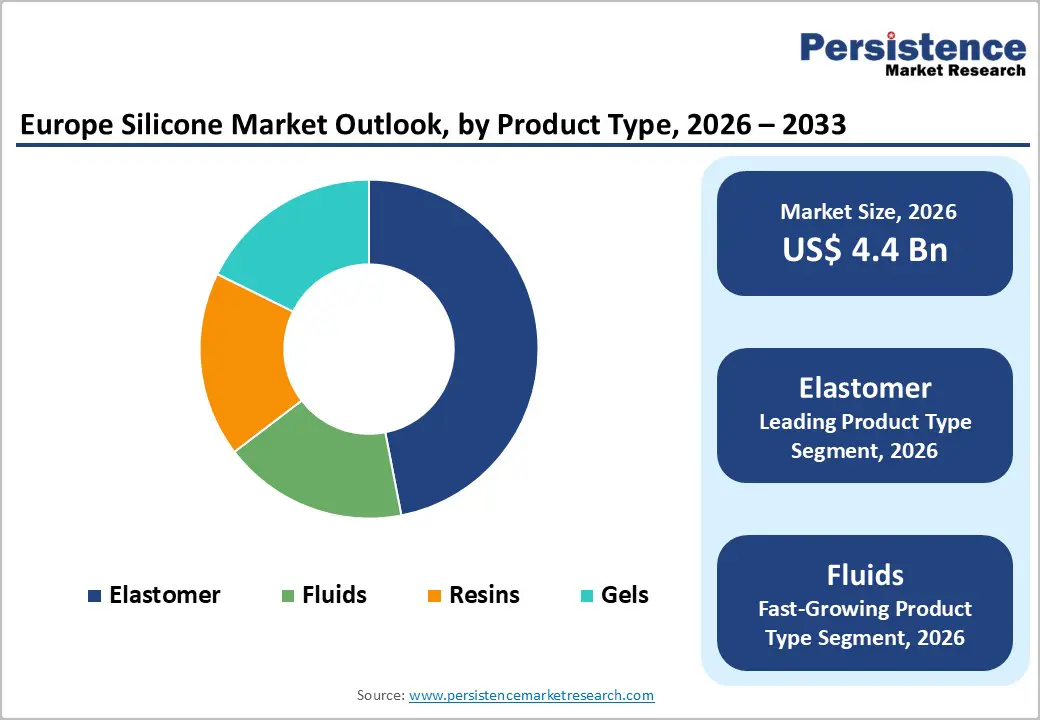

- Leading Product Type: Elastomers hold over 44% revenue share in 2026, supported by broad use in automotive, construction and healthcare; Europe’s silicone rubber segment alone is forecast to reach USD 3.29 Bn by 2035 (5.5% CAGR).

- Fast-growing Product Type: Silicone fluids are the fastest-growing product type (around a 6.3% CAGR), benefiting from specialty applications in industrial processes, coatings, lubricants, and personal care, and are reinforced by capacity expansions in Germany.

- Leading End-user: By end-user, construction exceeds 35% of demand, while transportation grows at about 6.6% CAGR, driven by EV adoption and higher electronics content per vehicle.

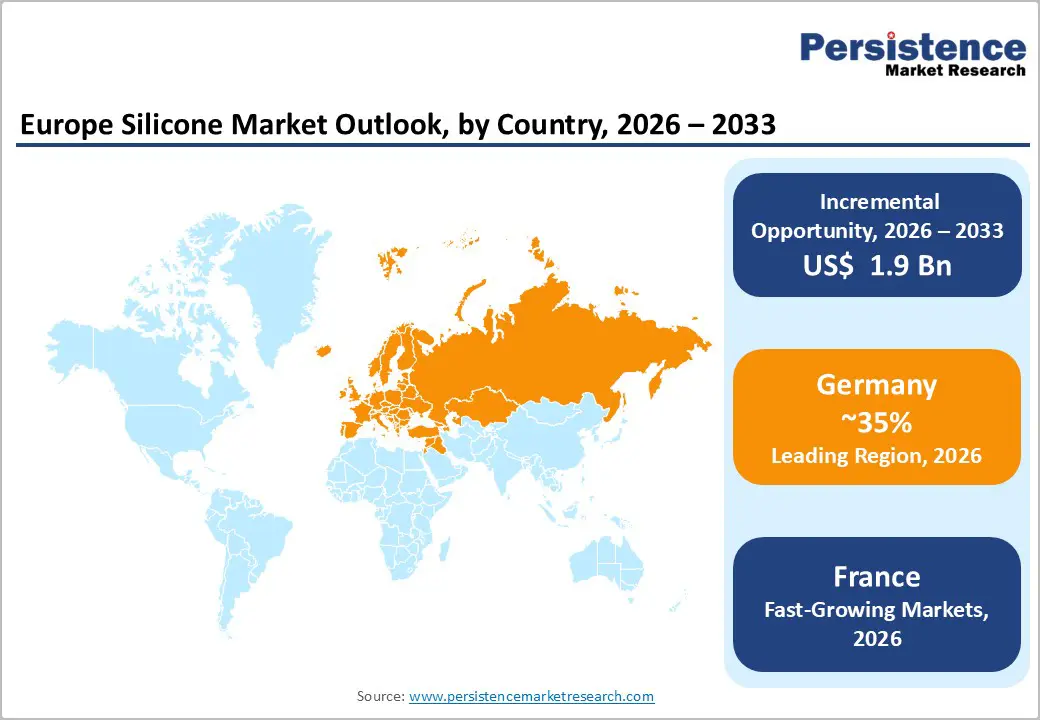

- Country Analysis: Germany is Europe’s largest silicone market, accounting for 9.6% of global revenues in 2022 and serving as the continent’s leading consumer and producer by volume. France is among the fastest-growing markets, with an estimated CAGR of about 6.5% supported by construction, automotive, and premium cosmetics.

- Development Analysis: Major strategic developments since 2023 include Wacker’s new Karlovy Vary plant, Dow’s carbon-neutral elastomer blends, and Wacker’s expanded silicone capex and healthcare acquisition, all reinforcing a shift toward specialty, sustainability-aligned silicones.

| Key Insights | Details |

|---|---|

| Europe Silicone Market Size (2026E) | US$ 4.4 Bn |

| Market Value Forecast (2033F) | US$ 6.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.8% |

Market Dynamics

Drivers - EU Green Transition Accelerates Silicon-Intensive Construction Activity

The European Green Deal and the EU's Renovation Wave Strategy targeting the retrofit of 35 million buildings by 2030 are generating substantial demand for high-performance silicone sealants, adhesives, and insulation materials. The European Commission estimates that buildings account for approximately 40% of the EU's total energy consumption. Silicone-based weatherproofing and glazing technologies are critical enablers of energy efficiency in building envelopes. According to Eurostat, construction output across the EU-27 expanded by 3.2% in 2023. Regulatory frameworks such as the Energy Performance of Buildings Directive (EPBD), revised in 2024, mandate near-zero energy standards for all new constructions directly amplifying silicone content per building. This macrostructural driver is expected to sustain above-average demand through 2030 and beyond.

Electric Vehicle Expansion Elevates Silicon Demand in Transportation

Europe's electric vehicle (EV) transition is a high-growth structural catalyst for silicon demand. The European Automobile Manufacturers' Association (ACEA) reports that EV registrations in Europe exceeded 3.2 million units in 2023, with battery electric vehicles accounting for 14.6% of total new car sales. Silicone elastomers and gels are essential in EV battery management systems, providing thermal insulation, vibration damping, and moisture sealing. The EU's 2035 ban on new internal combustion engine vehicle sales under the revised CO- Regulation for Cars and Vans (Regulation EU 2023/851) creates an irreversible demand trajectory. Each EV platform uses substantially more silicone per unit compared to conventional vehicles, making this segment a primary volume multiplier for the European silicone market through 2033.

Healthcare Sector Demand Driven by Aging Demographics and Regulatory Standards

Europe's demographic profile, with approximately 21% of the population aged 65 or older (Eurostat, 2023), projected to reach 29% by 2050, underpins sustained demand for medical-grade silicone across implants, catheters, wound care, and pharmaceutical packaging. The EU Medical Device Regulation (MDR, Regulation EU 2017/745), now fully in force, demands biocompatible, high-purity silicone materials that meet stringent safety standards, effectively raising entry barriers while rewarding established high-quality suppliers. The European medical devices market is valued at approximately €130 billion annually (MedTech Europe). Silicone's unique combination of biocompatibility, flexibility, and chemical inertness makes it the material of choice in advanced medical applications. This sector is expected to contribute meaningfully to premium silicone demand through 2033.

Restraint - Feedstock Price Volatility Compresses Silicone Producer Margins

Europe's silicone production is materially dependent on metallurgical silicon and chloromethane as primary feedstocks, both of which are exposed to global commodity price cycles. Silicon metal prices surged by over 40% in 2021-2022 amid energy constraints and supply chain disruptions, before moderating in 2023. The EU's Carbon Border Adjustment Mechanism (CBAM), which is phasing in from 2026, is expected to introduce additional cost pressures on energy-intensive chemical production, including silicone intermediate manufacturing. These structural cost headwinds risk compressing EBITDA margins for European producers, particularly smaller operators, and may constrain capital investment in capacity expansion. The inability to fully pass cost increases downstream in competitive markets is a significant structural restraint.

Regulatory Complexity and REACH Compliance Costs Create Market Friction

The European Chemicals Agency (ECHA) has placed certain cyclic siloxanes, notably D4 and D5, under REACH restrictions due to environmental persistence concerns, impacting specific personal care and industrial applications. Compliance with REACH, CLP, and evolving PFAS-related restrictions requires significant investment in product reformulation, toxicological testing, and regulatory documentation. For mid-sized silicone formulators, compliance costs can represent 3-6% of revenue annually. These regulatory hurdles pose barriers to new entrants and may temporarily constrain the breadth of product portfolios for incumbent manufacturers, slowing innovation cycles in affected application areas.

Opportunities - Healthcare, medical devices and specialty life-science applications

Medical-grade silicones benefit from favourable demographic and technology trends, including ageing populations, higher chronic-disease prevalence, and wider adoption of implantable and wearable devices. Fact.MR notes that healthcare is one of the fastest-growing end-use sectors for silicone rubber in Europe, driven by catheters, tubing, implants, and advanced wound-care solutions. Wacker’s 2024 acquisition of Bio Med Sciences, a US coater of silicone-coated healthcare products, is explicitly framed as a move to expand its medical and healthcare silicone portfolio, with global implications including Europe. The high regulatory and technical barriers in this segment support above-average margins and long-term supply contracts, making it a priority opportunity cluster for leading European silicone suppliers.

Digitalization of Electronics Manufacturing Fuels Specialty Silicone Demand

Europe's semiconductor ambitions under the European Chips Act, targeting 20% of global chip production by 2030, alongside growth in 5G infrastructure, industrial IoT, and advanced consumer electronics, are creating expanding markets for specialty silicone in thermal interface materials, conformal coatings, and electronic-grade encapsulants. The global electronics silicone segment is projected to register above-market growth rates driven by miniaturization trends that demand superior thermal management. European OEMs and Tier-1 suppliers increasingly specify silicone solutions over traditional materials for reliability in extreme operating conditions. This technology convergence offers producers with application engineering capabilities a differentiated value proposition and premium margin potential through 2033.

Category-wise Analysis

Product Type Insights

Elastomer Dominance Persists While Specialty Fluids Outpace Growth

Silicone elastomers command the largest revenue share in Europe silicone market, accounting for above 44% of total market revenue in 2026. Their dominance stems from unmatched versatility across temperature extremes (−60°C to +200°C), excellent electrical insulation, weathering resistance, and biocompatibility. Elastomers are the material of choice in sealing, gasketing, and bonding applications across construction (window profiles, expansion joints), automotive (powertrain seals, EV battery housings), and medical devices (implants, catheters). The ongoing energy renovation of Europe's building stock and the structural shift toward EV platforms, both supported by EU regulatory mandates, are reinforcing demand for high-performance elastomers. Major producers have invested in liquid silicone rubber (LSR) capacity expansions to serve healthcare and automotive injection molding applications, further consolidating elastomers' leadership position through 2033.

Silicone fluids represent the fastest-growing product category within Europe silicone market, projected to expand at a CAGR of 6.3% through 2033. Demand growth is propelled by expanding applications in personal care (as silicone fluids face selective REACH restrictions, reformulated variants are gaining traction), industrial lubricants, textile coating, and thermal management fluids for EV battery cooling systems. The shift from mineral oil-based to silicone-based dielectric cooling fluids in data centers and EV battery systems, driven by superior thermal stability and non-flammability, is an emerging high-volume application. Silicone fluids' ability to deliver performance in applications where competing materials fall short of regulatory and performance requirements is structurally underpinning their above-market growth rate in Europe.

Industry Insights

Europe silicone market is structurally anchored by the construction sector while experiencing its fastest expansion within transportation applications. Construction remains the dominant end-use industry, contributing over 35% of total silicone revenues in Europe in 2026. This leadership reflects silicone’s critical role in structural glazing, façade bonding, weather sealing, expansion joints, and building-envelope protection systems. Across residential, commercial, and infrastructure projects, large volumes of silicone-based sealants, elastomers, and coatings are deployed to enhance durability, insulation performance, and long-term structural integrity. EU-driven renovation initiatives and increasingly stringent energy-efficiency regulations continue to reinforce demand for high-performance materials. Silicones provide extended service life, superior weather resistance, and reduced maintenance costs, key advantages in total cost-of-ownership assessments, making them a preferred solution in sustainable and certified green building projects. As developers prioritize lifecycle efficiency, premium silicone systems increasingly displace lower-performance alternatives, solidifying construction as the market’s volume-intensive backbone.

Simultaneously, transportation represents the fastest-growing end-use segment, projected to expand at a CAGR of approximately 6.6% between 2026 and 2033. Rising vehicle electrification and increasing electronics integration are accelerating silicone demand in thermal management, battery insulation, sealing systems, vibration damping, and lightweighting applications. Automotive and aerospace manufacturers rely on silicone materials for high-temperature elastomers, encapsulants, and advanced sealing solutions that can withstand chemical exposure and mechanical stress. Europe’s stringent CO-emission targets and safety standards further drive the shift toward advanced materials, particularly in electric and hybrid vehicles. The combination of regulatory pressure, electrification trends, and technical performance requirements positions transportation as the strategic growth engine complementing construction’s stable revenue dominance in the European silicone market.

Regional Insights and Trends

Germany Anchors European Silicone Market Leadership

Germany holds the leading position in the European silicone market with above 35% revenue share in 2026, attributable to its position as Europe's largest manufacturing economy and the concentration of key silicone end-use industries including automotive, chemicals, electronics, and construction. Germany's GDP of approximately €3.9 trillion (Destatis, 2023) and its industrial output index despite 2023 contraction pressures underscore the depth of its chemical processing ecosystem. Wacker Chemie AG, headquartered in Munich, is a globally significant silicone producer and contributes to both domestic supply and export capacity across Europe.

The German automotive sector contributing approximately 5% of GDP and employing 786,000 workers directly (VDA, 2023) is undergoing a profound structural shift toward electrification, with Volkswagen Group, BMW, and Mercedes-Benz committing to predominantly electric or hybrid portfolios by 2030. This transition directly drives premium-grade silicone demand in battery management systems, thermal interface materials, and high-voltage sealing applications. Germany's construction market, governed by the German Building Energy Act (GEG 2023), mandates near-zero energy standards for new buildings and incentivizes renovation further sustaining construction-segment silicone demand. The German government's commitment to carbon neutrality by 2045 and the ongoing KfW federal bank renovation loan programs are channeling approximately €18 billion annually into energy-efficient building measures, supporting silicone-intensive retrofitting activity. Germany's well-established chemicals distribution infrastructure and proximity to key downstream industrial clusters position it as the anchor market for European silicone producers through 2033.

France’s Reindustrialization and Renewables Accelerate Market Growth.

France represents the fastest-growing national market within Europe, projected to expand at a CAGR of 6.5% through 2033, reflecting the convergence of accelerating industrial reindustrialization policy, an ambitious renewable energy buildout, and substantial construction renovation activity. France's GDP of approximately €2.8 trillion (INSEE, 2023) and its position as the EU's second-largest economy provide a deep demand base across construction, transportation, and emerging technology sectors.

The French government's 'France 2030' investment plan, committing €54 billion across strategic industrial sectors including clean energy, automotive electrification, and advanced manufacturing, is creating structural demand for specialty silicone materials in targeted applications. France's renewable energy ambitions are particularly relevant. The National Energy and Climate Plan (NECP) targets 40% of electricity from renewables by 2030, necessitating substantial solar PV and offshore wind deployment. Silicone encapsulants and sealants are critical to both technologies. Airbus and the French aerospace supply chain centered in Toulouse represent a premium demand segment for high-specification silicone adhesives and coatings. The MaPrimeRénov' renovation subsidy scheme, which disbursed €3.1 billion to French households in 2023 (ANAH), directly supports demand for silicone sealants and insulation products in the residential construction segment. France's above-average silicone market growth rate relative to European peers reflects this multi-sector policy catalyst alignment.

Competitive Landscape

The Europe silicone market exhibits a moderately consolidated structure at the upstream production level, with three to four global producers led by Wacker Chemie, Shin-Etsu Chemical, Elkem, and Momentive controlling the majority of base silicone polymer capacity. The downstream formulation and specialty application segment is more fragmented, with numerous regional compounders, adhesive manufacturers, and specialty chemical formulators competing on application expertise. The top five players collectively account for an estimated 55-65% of European market revenue. This structure creates a tiered competitive landscape where scale advantages are critical in commodity silicone production, while application engineering and regulatory compliance capabilities are the primary differentiators in specialty segments.

Key Industry Developments:

- In 2024, WACKER Plans New Production Site for Silicone Specialties in the Czech Republic. Wacker Chemie AG plans to further expand its silicone specialties business and is reorganizing its production operations in Europe.

- In 2024, Wacker Chemie AG announced targeted capacity investments in liquid silicone rubber (LSR) production at its Burghausen, Germany, facility, specifically to serve the growing EV battery and medical device sectors. The investment part of Wacker's capital expenditure program targeting approximately €350 million in 2024 reflects strategic prioritization of high-margin specialty silicone segments over commodity fluids.

- In late 2023, Elkem ASA (Oslo-headquartered) entered a strategic R&D partnership with a European chemical recycling technology firm to develop scalable silicone recovery and recycling processes. Aligned with EU Circular Economy Action Plan requirements and corporate Scope 3 emissions targets, this initiative aims to establish Europe's first commercial-scale silicone depolymerization and reformulation capability by 2026

- In 2024, Shin-Etsu Chemical expanded its European specialty silicone distribution footprint, establishing new technical service and application laboratories in Germany and the Netherlands.

Companies Covered in Europe Silicone Market

- AB Specialty Silicones

- ACSIC Ingredients

- Shin-Etsu Chemical Co Ltd

- Wacker Chemie AG

- Illinois Tool Works Inc

- Evonik Industries AG

- CK Hutchison Holdings Ltd

- Kemira Oyj

- Dow Inc

- Elkem ASA Ordinary Shares

- SilColours

- Momentive Performance Materials Inc.

- Other Market Players

Frequently Asked Questions

The Silicone market is estimated to be valued at US$ 4.4 Bn in 2026.

The key demand driver for the Silicone market in Europe is the increasing demand from major end-use industries, particularly construction, automotive, electronics, and industrial applications with construction and industrial growth being especially significant.

In 2026, Germany will dominate the market with an exceeding 35% revenue share in the Europe Silicone market.

Among product types, elastomer has the highest preference, capturing beyond 44% of the market revenue share in 2026, surpassing other product types.

AB Specialty Silicones, ACSIC Ingredients, Shin-Etsu Chemical Co Ltd, Wacker Chemie AG, Illinois Tool Works Inc, Evonik Industries AG, and CK Hutchison Holdings Ltd. There are a few leading players in the European Silicon market.