- Specialty & Fine Chemicals

- Rubber Processing Chemicals Market

Rubber Processing Chemicals Market Size, Share, and Growth Forecast, 2025 - 2032

Rubber Processing Chemicals Market By Product Type (Anti-degradants, Accelerators, Flame Retardants), Application (Tire and Related Products, Automotive Components), End-user (Tire, Non-tire), and Regional Analysis for 2025 - 2032

Rubber Processing Chemicals Market Size and Trends Analysis

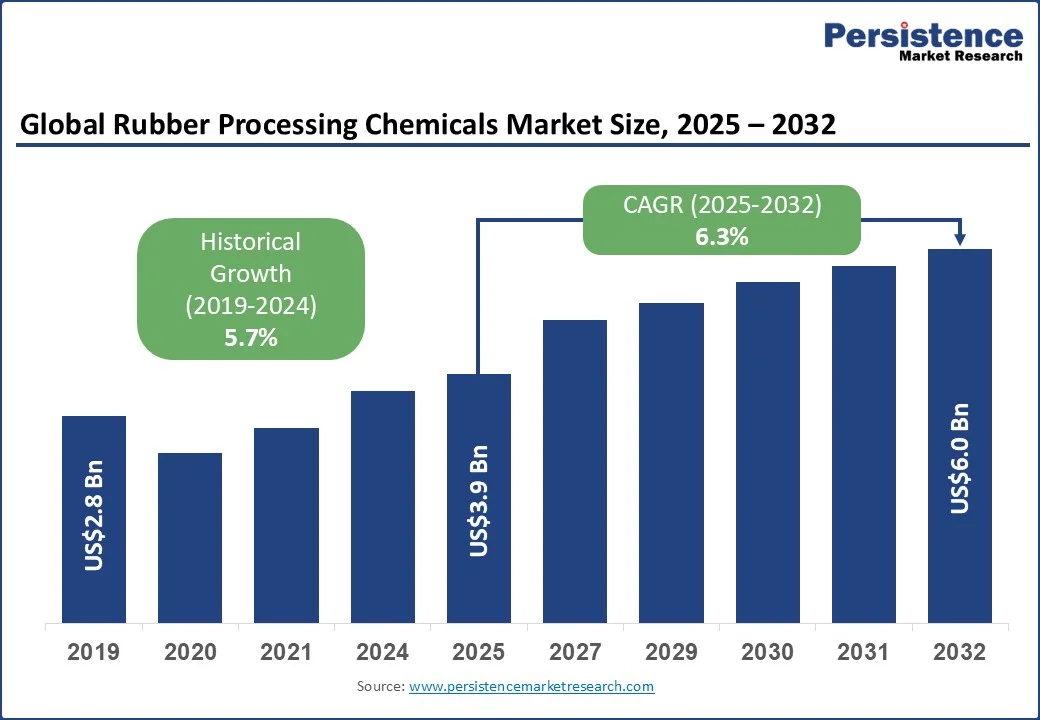

The global rubber processing chemicals market size is likely to be valued at US$3.9 Bn in 2025 and is estimated to reach US$6.0 Bn in 2032, growing at a CAGR of 6.3% during the forecast period 2025-2032, due to the rising demand for high-performance tires, the shift toward Electric Vehicles (EVs), and expanding applications in construction.

Key Industry Highlights

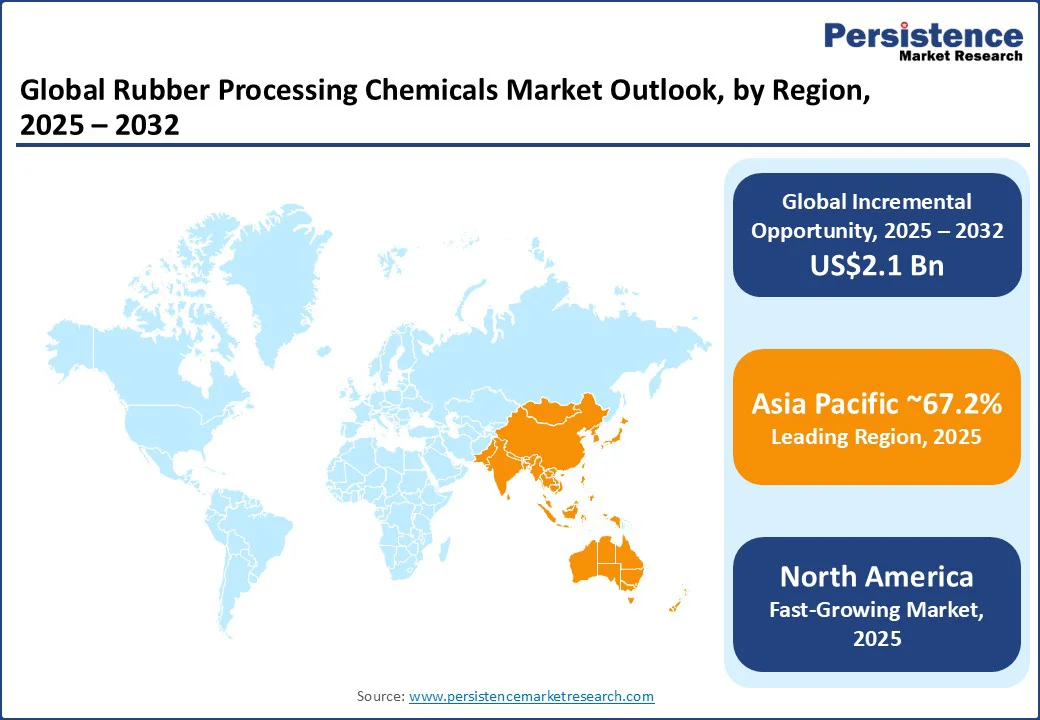

- Leading Region: Asia Pacific, with about 67.2% share in 2025, owing to high demand for tires and industrial rubber products across India and China.

- Fastest-growing Region: North America, owing to stringent environmental regulations and the presence of a mature automotive industry.

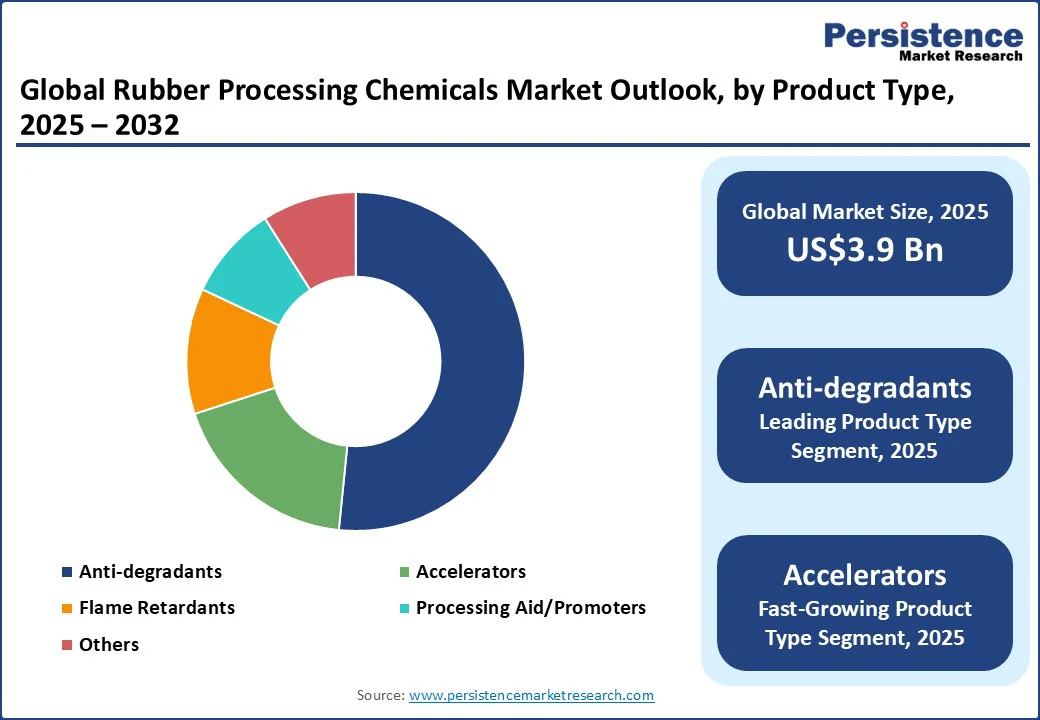

- Leading Product Type: Anti-degradants hold nearly 51.6% of the share in 2025, pushed by their ability to protect rubber from heat, ozone, and oxidative damage.

- Dominant Application: Automotive components, approximately 32.8% of the rubber processing chemicals market share in 2025, backed by the requirement for high durability and flexibility in tires, hoses, seals, and belts.

- New Additive Launch: LANXESS launched a rubber additive named Vulkanox HS Scopeblue to improve the sustainability and durability of tires. The new product is designed to protect tires from oxidative and thermal degradation.

|

Key Insights |

Details |

|

Rubber Processing Chemicals Market Size (2025E) |

US$3.9 Bn |

|

Market Value Forecast (2032F) |

US$6.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.7% |

Market Behavior and Trends Analysis

EV Adoption Bolsters Demand for Novel LRR Tire Formulations

The increasing focus on fuel efficiency and emission reduction in the automotive industry is pushing the demand for Low Rolling Resistance (LRR) tires. It is further spurring the consumption of rubber processing chemicals. These tires require specialized formulations of accelerators, antioxidants, and silane coupling agents to improve tread wear, reduce heat build-up, and improve grip without compromising durability. For instance, tire makers such as Continental have been actively integrating silica-silane technology into their LRR tire lines to lower carbon emissions from passenger and commercial vehicles.

The shift requires novel chemical inputs during compounding, making rubber processing chemicals essential to meet evolving performance standards and regulatory targets. As EV adoption rises, the demand for low rolling resistance (LRR) tires with optimized efficiency increases, driving chemical demand due to the higher torque and weight stress EVs place on tires compared to conventional vehicles.

Restrictions on Key Anti-degradants Lead to Supply Uncertainty

Environmental and safety regulations, such as REACH in Europe and EPA rules in the U.S., are compelling chemical manufacturers to reformulate or phase out certain widely used rubber processing chemicals. For example, the EU recently restricted the use of 6PPD due to concerns about toxic runoff affecting aquatic life. As 6PPD remains one of the most effective anti-degradants for tire performance, its restriction is creating uncertainty for manufacturers, who now face significant R&D costs to develop safe alternatives before scaling production.

The compliance process adds significant cost and potential delays. Every new formulation requires extensive toxicology testing, lifecycle impact assessments, and regulatory approvals, which can take years. Small-scale players often struggle with these expenses, leading to fewer firms in the market and reduced competitive supply. This regulatory drag often slows development and keeps demand for rubber processing chemicals from increasing at the pace it could if fewer compliance hurdles existed.

High-performance Additives Such as Nano-silica Create New Niches

New mixing technologies are creating opportunities for rubber processing chemical manufacturers as they enable precise dispersion of additives. This helps in improving the durability and performance of rubber products. Novel internal mixers and twin-screw extruders, for example, are allowing tire makers to evenly distribute accelerators and anti-degradants. This precision is important for EV tires, which require better abrasion resistance and lower rolling resistance. Companies that can manufacture chemicals specifically for these novel mixing lines are finding new demand from automotive OEMs and specialty rubber producers.

High-performance additives are also creating new niches. Nano-silica and bio-based antioxidants are being blended into rubber compounds to replace traditional options without compromising strength. Tire companies have already started joining hands with chemical suppliers to explore sustainable additives that balance performance with environmental compliance. This shift allows chemical companies to position themselves not just as suppliers, but as innovation partners who can co-develop customized solutions.

Category-wise Analysis

Product Type Insights

By product type, the market is segregated into anti-degradants, accelerators, flame retardants, processing aid/promoters, and others. Among these, anti-degradants are poised to hold around 51.6% of the market share in 2025, as they protect rubber from environmental damage, which is a key reason rubber products fail. Rubber components used in tires, hoses, seals, and belts are constantly exposed to oxygen, ozone, heat, and sunlight. This causes cracks, stiffness, and loss of flexibility. Anti-degradants help slow down this process, making products last longer and perform better.

Accelerators are expected to record a steady CAGR in the forecast period due to their ability to make the vulcanization process fast and efficient, which saves energy and production time. Without them, rubber curing takes a long time and requires high temperatures, which increases costs. Accelerators allow manufacturers to produce large volumes of tires and industrial rubber goods quickly while keeping energy use under control. Additionally, they are essential for improving the performance of modern rubber products. Accelerators help achieve the right balance of elasticity, strength, and heat resistance in rubber compounds.

Application Insights

Based on application, the market is divided into tire and related products, automotive components, footwear products, industrial rubber products, and others. Out of these, automotive components are predicted to account for nearly 32.8% of the share in 2025 as vehicles demand rubber parts that can withstand harsh conditions. Tires, seals, gaskets, hoses, and belts usually face constant stress from heat, pressure, fuel, oil, and road contact. Without processing chemicals, these parts would crack, harden, or wear out quickly. The chemicals also help extend product life, improve performance, and keep vehicles safe on the road.

The industrial rubber products segment is a key application area as it is used in environments where durability and resistance to extreme conditions are non-negotiable. Conveyor belts in mining, hoses in oil refineries, or seals in heavy machinery face continuous exposure to heat, abrasion, chemicals, and mechanical stress. Rubber processing chemicals are essential here as they provide these products with the elasticity, toughness, and longevity required to function without frequent breakdowns. The rise of renewable energy and modern infrastructure projects is also making this application important.

Regional Insights

Asia Pacific Rubber Processing Chemicals Market Trends- Export Compliance Pressurizes Local Producers to Adopt Eco-friendly Solutions

Asia Pacific is estimated to account for approximately 67.2% of the market share in 2025, due to high demand from the tire and automotive sectors. China and India are tightening regulations around hazardous antidegradants and accelerators, especially those that generate nitrosamines or are linked to health risks. There is an increasing demand for green substitutes such as bio?based processing oils, eco-friendly accelerators, and safe anti-degradants. Local producers are under pressure both from domestic environmental laws and from export markets demanding compliance.

Global chemical companies are investing heavily in Asia Pacific to stay close to demand. Many are upgrading production lines to meet environmental standards, while less efficient plants are being shut down. A recent case is SI Group’s decision to close its alkylphenol plant in Singapore owing to changes in the antioxidant value chain and rising operating costs. Raw material volatility and supply chain disruptions remain key challenges in Asia Pacific.

North America Rubber Processing Chemicals Market Trends - Ongoing Shift toward EVs Propels Demand for Novel Chemicals

In North America, the market is being fueled by stringent environmental norms and frequent policy changes. Recently, a U.S. Congressional resolution overturned an Environmental Protection Agency (EPA) rule that was meant to limit air pollutants from tire and rubber manufacturing. This rollback reduced short-term compliance costs for manufacturers but created uncertainty for chemical suppliers, who have been investing in green solutions.

The shift toward electric vehicles is also influencing the demand for specialized chemicals. EVs put more stress on tires and rubber components due to high torque and weight. They hence require rubber processing chemicals that can improve heat resistance, durability, and rolling efficiency. This is propelling producers in the U.S. rubber processing chemicals market to focus on novel anti-degradants and accelerators designed specifically for EV applications.

Europe Rubber Processing Chemicals Market Trends - Ban on BPA in Food-contact Rubber Accelerates Reformulation

The regional market is heavily influenced by strict regulations. The European Union (EU) recently banned bisphenol A (BPA) in all rubber and plastic applications that come into contact with food, effective January 2025. This has compelled manufacturers to reformulate coatings and additives, creating opportunities for safe alternatives. The debate around per- and polyfluoroalkyl substances (PFAS) is another major issue. Instead of a blanket ban, the EU is moving toward risk-based restrictions, which has been welcomed by Germany’s rubber industry group.

Environmental norms are further influencing the market. Short-chain chlorinated paraffins used in belts and hoses have been placed under strict EU toxic-waste regulations. In addition, the EU has banned crumb rubber infill in sports pitches due to concerns about microplastics. This directly impacts recycled rubber additives that depend on this market. Owing to the rising pressure, domestic firms are investing in sustainable solutions such as bio-based accelerators. The region is becoming a hub for green chemistry development, even though companies face high energy costs.

Competitive Landscape

The global rubber processing chemicals market is characterized by strategic moves, technological developments, and regional dynamics. Leading players are embracing mergers and acquisitions, regional expansions, and product launches to strengthen their positions. A few others are focusing on improving their product portfolios and expanding their geographical presence to cater to the rising demand in emerging markets. The introduction of bio-based and sustainable products is gaining momentum. In addition, companies are investing in research and development to create products that comply with environmental norms while maintaining performance standards.

Key Industry Developments

- In September 2025, LANXESS announced the expansion of its production capacities with the addition of rubber processing promoters at its Bushy Park facility in Goose Creek. The project aims to meet the increasing demand and improve supply reliability, with new production anticipated to come online in November 2025.

- In February 2025, Gayatri Rubbers and Chemicals Limited secured work orders worth around INR 1.03 crore (approximately US$117,000) from multiple Indian railway zones and the industrial sector. These orders involve the supply of neoprene rubber, fire-retardant gasket, and rubber compound.

Companies Covered in Rubber Processing Chemicals Market

- Lanxess AG

- Solvay

- BASF SE

- AkzoNobel N.V.

- R.T. Vanderbilt Holding Company, Inc.

- Eastman Chemical Company

- Behn Meyer Holding AG

- Paul & Company

- Merchem Limited

- China Petrochemical Corporation

- Kumho Petrochemical Co.

- Others