- Specialty & Fine Chemicals

- Isoprene Rubber Latex Market

Isoprene Rubber Latex Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Isoprene Rubber Latex Market by Grade (Medical, Industrial, Food), Application (Medical Gloves, Catheters & Balloon Devices, Condoms), Industry (Healthcare & Medical, Personal Care & Hygiene, Industrial Manufacturing) and Regional Analysis 2025 - 2032

Isoprene Rubber Latex Market Share and Trends Analysis

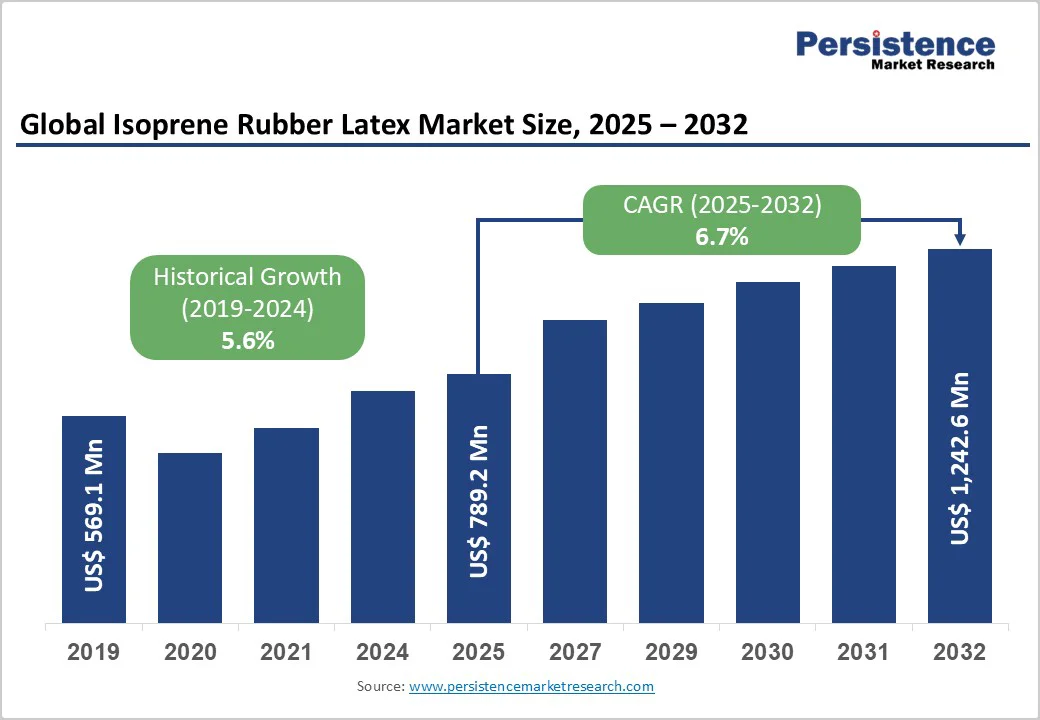

The global isoprene rubber latex market is likely to be valued at US$789.2 million in 2025 and is projected to reach US$1,242.6 million by 2032, growing at a CAGR of 6.7% between 2025 and 2032.

The market is poised for sustained growth driven by rising demand in healthcare applications, where synthetic alternatives to natural latex offer allergy-free solutions amid increasing global health standards.

In addition, advancements in polymerization technologies have enhanced product durability and biocompatibility, enabling broader adoption in medical devices.

Key Market highlights:

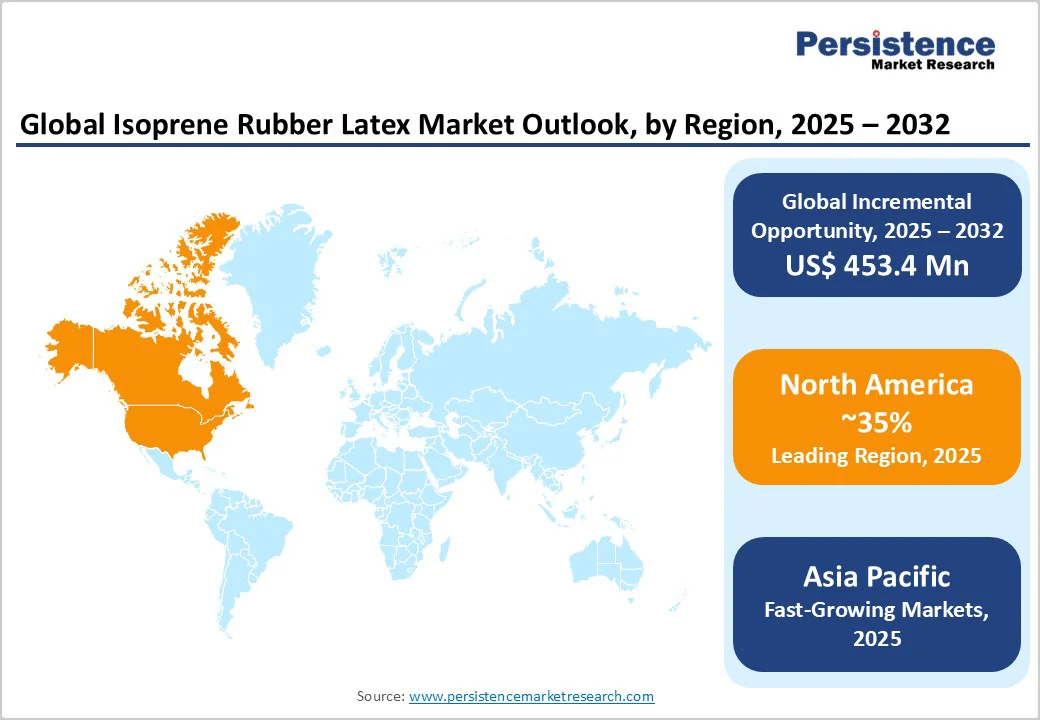

- Regional Leader: North America leads as the dominant region, driven by U.S. regulatory support and innovation in hypoallergenic medical applications, capturing a significant share through advanced healthcare infrastructure.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, fueled by China's manufacturing prowess and ASEAN's low-cost production, with rapid industrialization boosting demand in gloves and devices.

- Leading Segment: Medical grade stands as the dominant segment in grades, holding a 60% share due to its essential role in allergy-free healthcare products amid global standards.

- Fastest Growing Segment: Medical gloves represent the fastest-growing application segment, propelled by post-pandemic hygiene needs and annual volume increases of 12-15% in key markets.

- Growth Opportunities: Expansion in bio-based technologies offers a key market opportunity, aligned with policies such as the EU Green Deal, potentially increasing adoption by 25% in sustainable applications.

| Key Insights | Details |

|---|---|

| Isoprene Rubber Latex Size (2025E) | US$789.2 Mn |

| Market Value Forecast (2032F) | US$ 1,242.6 Mn |

| Projected Growth CAGR (2025-2032) | 6.7% |

| Historical Market Growth (2019-2024) | 5.6% |

Market Dynamics

Driver- Rising Demand in the Healthcare Sector for Allergy-Free Alternatives

The increasing prevalence of latex allergies has significantly boosted the adoption of isoprene rubber latex as a synthetic substitute in medical products. According to the World Health Organization (WHO), approximately 1-6% of the global population suffers from latex allergies, prompting healthcare providers to shift toward hypoallergenic materials.

This transition is particularly evident in the production of surgical gloves and catheters, where isoprene rubber latex provides superior elasticity and puncture resistance without triggering allergic reactions. In the Medical Gloves Market, this demand has led to strengthened supply chains, with manufacturers reporting up to 20% year-over-year increases in hospital orders.

Furthermore, post-pandemic hygiene protocols have amplified glove usage, with global consumption estimated at over 300 billion units annually by the U.S. Food and Drug Administration (FDA). These factors collectively drive market growth by ensuring safer, more reliable medical supplies, reducing infection risks, and aligning with stringent health regulations worldwide.

Advancements in Sustainable Manufacturing Processes

Technological innovations in bio-based production methods are propelling the isoprene rubber latex market forward by addressing environmental concerns. The U.S. Environmental Protection Agency (EPA) notes that bio-derived isoprene can reduce carbon emissions by up to 30% compared to petrochemical alternatives, appealing to eco-conscious industries.

This is supported by developments from organizations such as the National Institute of Standards and Technology (NIST), which note improvements in fermentation-derived isoprene, enhancing yield efficiency to 50-60%. Such progress not only lowers production costs but also meets growing regulatory demands for sustainable materials in consumer goods and adhesives.

In industrial applications, this has resulted in a 15% increase in adoption rates, as per industry reports, fostering long-term market expansion through reduced dependency on volatile fossil fuels and promoting circular economy practices.

Restraint - Volatility in Raw Material Prices and Supply Chain Disruptions

Fluctuating prices of isoprene monomers, driven by petrochemical market instabilities, pose a significant barrier to the isoprene rubber latex market. Data from the U.S. Geological Survey indicates that natural rubber prices dropped from US$ 1.64 per kg in 2018 to US$ 1.41 per kg in 2019, intensifying competition and squeezing margins for synthetic latex producers.

This volatility is exacerbated by supply chain disruptions, such as those seen during global events, leading to delays in monomer availability and increased costs by up to 25%.

In the Condoms Market, where consistent quality is crucial, these issues have caused production halts, affecting market reliability. Environmental regulations from bodies like the EPA, which reported 22 Mn pounds of toxic releases from rubber facilities in 2019, further complicate operations, raising compliance expenses and deterring investments, ultimately hindering overall market growth.

Competition from Natural Rubber and Other Synthetics

Intense competition from natural rubber and alternative synthetics, such as nitrile limits the expansion of isoprene rubber latex. The U.S. Bureau of Labor Statistics notes a 1.2% decline in rubber manufacturing employment from 2018 to 2019, reflecting shifts toward cheaper natural options amid economic pressures. Natural rubber's lower cost and established supply chains make it preferable in non-medical applications, capturing up to 60% of the adhesives market share.

Furthermore, synthetics like nitrile offer better chemical resistance, drawing demand from industrial sectors and reducing isoprene's penetration. In the Peripherally Inserted Central Catheters industry, this competition has led to slower adoption rates, with manufacturers facing pricing pressures that erode profitability and innovation incentives, thereby restraining market potential.

Opportunities - Expansion in Emerging Medical Device Segments

The fastest-growing segment in medical devices, particularly catheters and balloon devices, presents substantial opportunities for isoprene rubber latex manufacturers. With minimally invasive procedures rising by 10-15% annually, as reported by the World Health Organization (WHO), demand for biocompatible materials is surging.

Recent developments, such as DEHP-free regulations by the FDA, favor isoprene latex for its non-toxic properties in balloon catheters, potentially increasing market share by 20% in this area. Companies can capitalize by investing in R&D for ultra-clean grades meeting USP standards, targeting vaccine-related applications like vial stoppers amid global health initiatives. This aligns with policies promoting advanced healthcare in developing regions, generating significant demand and revenue potential through 2032.

Adoption of Bio-Based Technologies and Policies

Government policies favoring sustainable materials open doors for bio-based isoprene rubber latex in industrial and consumer goods. The European Union's Green Deal aims to reduce emissions by 55% by 2030, incentivizing bio-derived rubbers with subsidies and tax breaks.

Innovations in fermentation processes, as noted by IFPEN, have improved yields to 70%, enabling cost-effective production. This is particularly promising in adhesives and sealants, where eco-friendly alternatives could capture 25% more market share. Firms focusing on these technologies can leverage emerging business models like partnerships with biotech firms, tapping into high-demand end-users and driving long-term growth.

Category-wise Insights

Grade Analysis

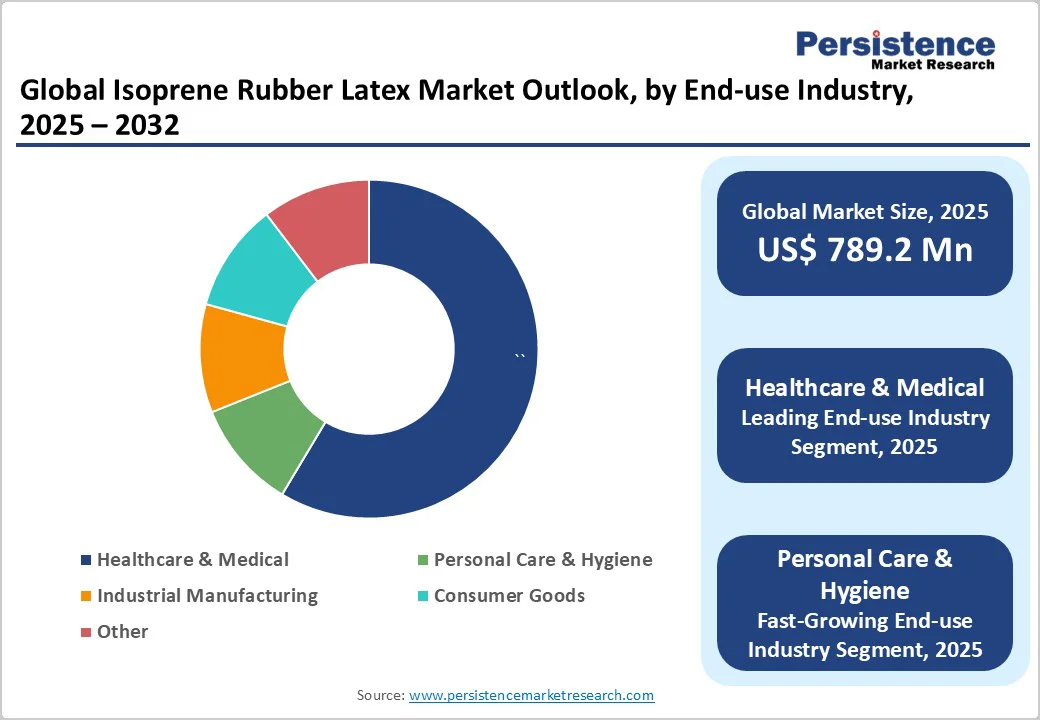

The medical grade segment leads the isoprene rubber latex market, holding approximately 60% market share due to its critical role in hypoallergenic medical applications.

This dominance is justified by data from the World Health Organization (WHO), which reports that latex allergies affect up to 6% of healthcare workers, driving the shift to synthetic options like medical-grade isoprene for gloves and devices. Its superior biocompatibility and low protein content, as per FDA standards, ensure safety in surgical environments, reducing infection risks.

In the Medical Gloves Market, this grade's adoption has surged, supported by 300 billion global glove usages annually, emphasizing its necessity for high-purity, non-allergenic materials that meet stringent regulatory requirements and enhance patient outcomes.

Application Analysis

Medical gloves emerge as the leading segment in applications, commanding about 70% market share, driven by escalating hygiene standards in healthcare. Justification stems from U.S. Food and Drug Administration (FDA) reports indicating over 300 billion gloves used globally in 2020, with isoprene latex favored for its elasticity and allergy-free properties.

In the Medical Gloves Market, this segment benefits from post-pandemic protocols, where powder-free variants have experienced 12-15% annual volume increases among producers. Its puncture resistance and tactile sensitivity make it ideal for examinations and surgeries, outperforming alternatives in high-demand settings and solidifying its position through consistent innovation in manufacturing.

Industry Analysis

The healthcare and medical Industry dominates with roughly 65% market share, attributed to the essential use in protective equipment amid rising infection control needs. This is supported by World Health Organization (WHO) statistics showing 1 in 10 patients affected by healthcare-associated infections, necessitating reliable barriers like isoprene latex in gloves and catheters.

In the Peripherally Inserted Central Catheters Market, its biocompatibility has led to increased adoption, with procedures growing by 10-15% yearly. Regulatory frameworks from bodies like the FDA further reinforce this leadership by mandating hypoallergenic materials, ensuring sustained demand in hospitals and clinics worldwide.

Regional Insights

North America Isoprene Rubber Latex Trends

The U.S. leads North America's isoprene rubber latex market through innovation in medical applications, supported by robust regulatory frameworks. The FDA's emphasis on hypoallergenic materials has driven adoption in gloves and devices, with recent tariffs on Chinese imports redirecting 80% of orders to domestic suppliers as of 2025. This fosters an ecosystem of R&D, exemplified by advancements in bio-based latex reducing emissions by 30%, per EPA data.

Innovation hubs in states like Illinois, where the Latex Glove Ban Act effective 2024 promotes synthetics, enhance market dynamics. Overall, these trends position North America for steady growth, balancing regulatory compliance with technological progress in healthcare.

Europe Isoprene Rubber Latex Trends

Germany, the U.K., France, and Spain drive Europe's market with strong performance in sustainable manufacturing and regulatory harmonization. Germany's automotive and medical sectors leverage isoprene for adhesives, supported by EU Green Deal policies aiming for 55% emission cuts by 2030. Recent news from IFPEN highlights fermentation tech yielding 70% efficiency, boosting eco-friendly adoption.

Harmonized regulations across the region, like REACH standards, ensure uniform quality, with France and Spain seeing 15% rises in medical device production. This cohesive framework enhances competitiveness, focusing on innovation and environmental compliance for long-term market stability.

Asia Pacific Isoprene Rubber Latex Trends

China, Japan, India, and ASEAN nations fuel Asia Pacific's growth through manufacturing advantages and expanding healthcare. China's dominance stems from facilities like Cariflex Pte Ltd's Singapore plant, inaugurated in May 2025 with USD 355 Mn investment, catering to medical demands. ASEAN's low-cost production sees glove volumes up 12-15% annually, per Malaysian reports.

Japan and India benefit from tech integrations, with India's hygiene awareness driving condom and glove usage in the Condoms Market. These dynamics, combined with rapid industrialization, position the region as a high-growth hub.

Competitive Landscape

The isoprene rubber latex market is moderately consolidated, with key players such as petrochemical giants holding significant shares through vertical integration. Companies employ expansion strategies, such as capacity boosts in Asia, and R&D for bio-based grades to counter volatility.

Market leaders differentiate via proprietary catalysts for ultra-clean latex, meeting medical standards. Emerging trends include sustainable business models, like partnerships for fermentation tech, enhancing supply security, and eco-compliance.

Key Market Developments:

- May, 2025: Cariflex Pte Ltd inaugurated the world's largest polyisoprene latex facility in Singapore, investing USD 355 Mn to meet surging medical demand.

- January, 2023: The Illinois General Assembly enacted the Latex Glove Ban Act, promoting synthetics like isoprene to reduce allergies in healthcare settings.

Top Companies in Isoprene Rubber Latex

- KURARAY CO., LTD. (Japan): As a leader in polymerization tech, KURARAY excels with tailored medical grades, leveraging monomer access for hypoallergenic products. Its portfolio strength and global influence drive revenue, focusing on sustainable innovations.

- Zeon Corporation (Japan): With maturity in synthetics, Zeon influences the market via high-purity latex for devices. Headquartered in Tokyo, it emphasizes R&D, holding strong positions in healthcare through quality and supply reliability.

- JSR Corporation (Japan): JSR stands out for its revenue and portfolio in ultra-clean grades, impacting medical and industrial segments. Based in Tokyo, its strategic expansions ensure market maturity and innovation leadership.

Companies Covered in Isoprene Rubber Latex Market

- Cariflex Pte Ltd

- Daelim Co., Ltd.

- KURARAY CO., LTD.

- JSR Corporation

- PJSC SIBUR Holding

- Zeon Corporation

- Eni S.p.A

- Exxon Mobil Corporation

- Fushun Yikesi New Materials Co., Ltd

- Synthomer plc

- Kraton Corporation

- Top Glove Corporation Bhd

- SABIC

- TSRC Corporation

- LG Chem

Frequently Asked Questions

The global isoprene rubber latex market is projected to reach US$ 1,242.6 Mn by 2032.

Rising demand in healthcare for allergy-free alternatives drives the market, supported by increasing global glove consumption and hygiene standards.

Medical gloves lead the application segment, holding about 70% share due to their essential role in infection prevention.

North America leads, driven by U.S. regulatory frameworks and innovation in medical applications.

Adoption of bio-based technologies presents opportunities, aligned with sustainability policies for eco-friendly production growth.

Key players include KURARAY CO., LTD., Zeon Corporation, JSR Corporation, and Cariflex Pte Ltd.