- Medical Devices

- Patient Positioning Equipment Market

Patient Positioning Equipment Market Size, Share, Growth, and Regional Forecast, 2025 - 2033

Patient Positioning Equipment Market by Product (Surgical Tables, Examination Tables, Stretcher Chair, Dental Chair), by End-user (Hospitals, Clinics, Ambulatory Surgical Centers), by Regional Analysis, from 2026 - 2033

Patient Positioning Equipment Market Share and Trends Analysis

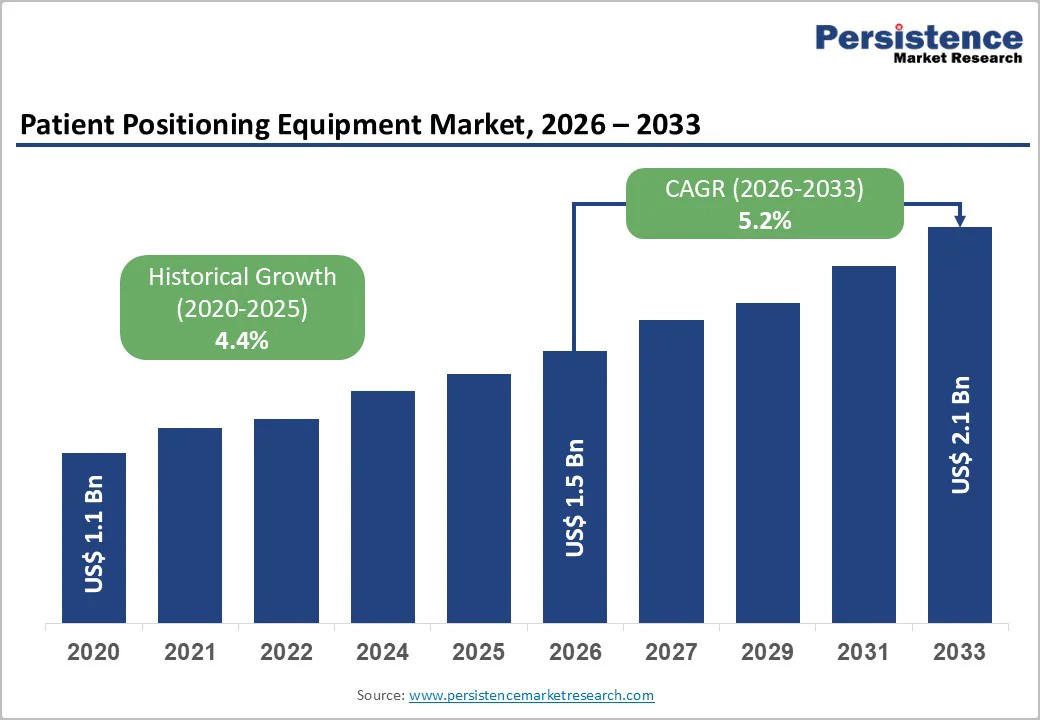

The global patient positioning equipment market size is estimated to grow from US$ 1.5 billion in 2026 and projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 5.2% during the forecast period from 2026 to 2033.

The rise in demand for surgical tables, examination tables, stretcher chairs, and dental chairs across hospitals, clinics, and outpatient care facilities collectively contributes to the market growth. Rise in surgical procedures, expanding healthcare infrastructure, and a focus on patient safety and comfort are fueling the adoption of advanced positioning systems.

Key Industry Highlights

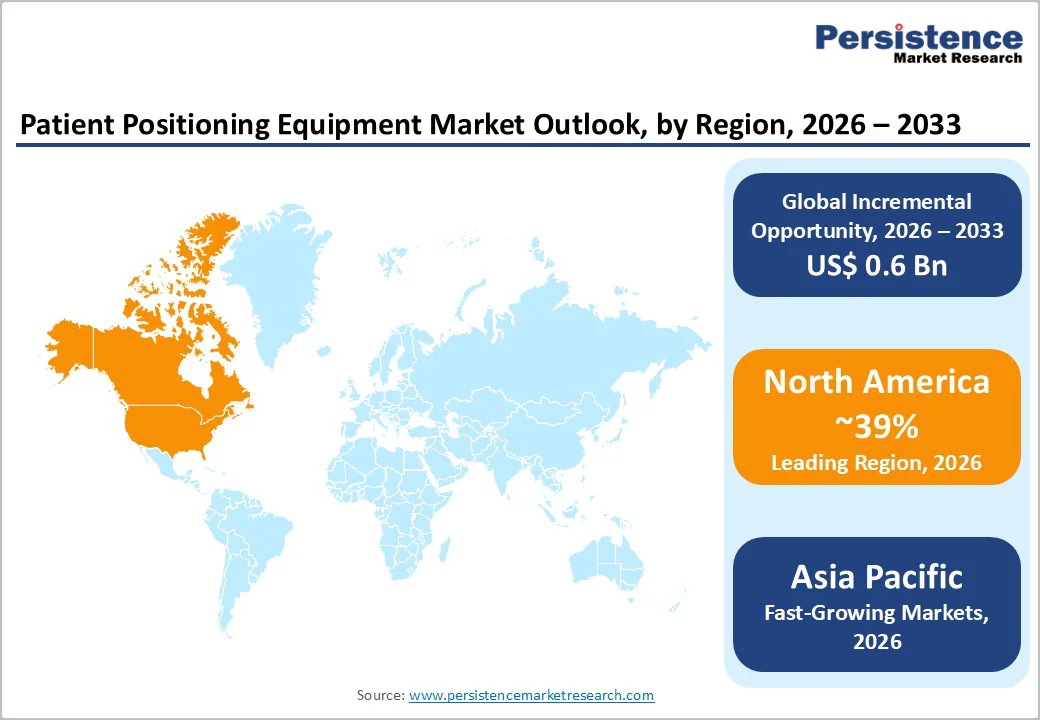

- Leading Region: North America dominates the patient positioning equipment market, driven by sophisticated OR infrastructure, advanced regulatory standards, and high adoption of powered surgical tables and exam chairs.

- Fastest Growing Region: Asia Pacific emerges fastest in growth, owing to rapid healthcare infrastructure development, rising surgery rates, and robust adoption in newly constructed hospitals and surgical centers.

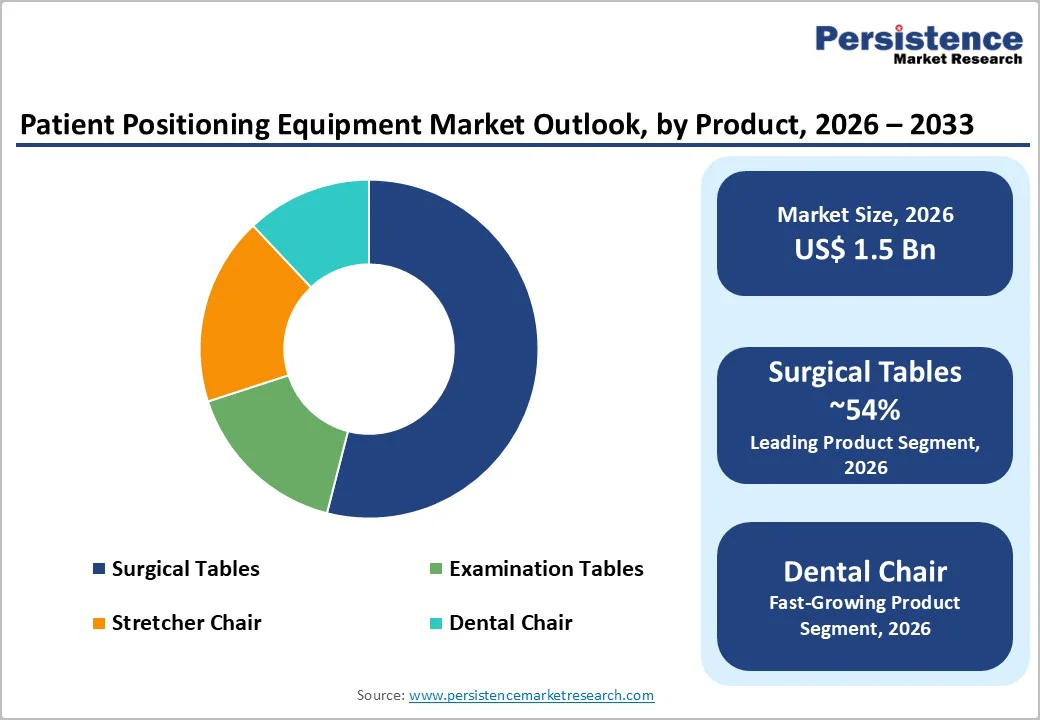

- Dominant Segment: Surgical tables accounted for about 54% of market share in 2025, reflecting their central role in all types of surgical settings globally, particularly in OR modernization projects.

- Fastest Growing Opportunity: Ambulatory Surgical Centers represent the fastest-growing end-user category as outpatient surgery volumes rise, demanding agile, easy-to-clean, and multi-position compatible positioning equipment.

| Key Insights | Details |

|---|---|

|

Patient Positioning Equipment Market Size (2026E) |

US$ 1.5 Bn |

|

Market Value Forecast (2033F) |

US$ 2.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.2% |

|

Historical Market Growth (CAGR 2020 to 2024) |

4.4% |

Market Dynamics

Driver - Surge in Surgical Procedures and Minimally Invasive Interventions

The global patient positioning equipment market is significantly driven by the steady rise in surgical procedures, encompassing advanced orthopedic, cardiovascular, and minimally invasive interventions. Hospital and national health statistics indicate that elective and trauma surgeries have grown by over 20% in key economies since 2020, fueled by aging populations and the adoption of innovative surgical technologies. Minimally invasive surgeries demand precise and stable patient positioning to provide optimal access and visibility for surgeons, prompting hospitals and ambulatory surgical centers (ASCs) to invest in motorized surgical tables, modular supports, and ergonomic positioning aids. Such equipment enhances surgical precision, reduces procedure times, and contributes to better clinical outcomes.

In addition, stringent regulatory requirements for patient safety and compliance in operating rooms have reinforced the need for high-precision positioning solutions. The combination of rising procedural volumes, evolving surgical techniques, and an emphasis on patient safety continues to accelerate adoption of advanced positioning equipment across hospitals, specialty clinics, and surgical centers worldwide, highlighting this segment as a key growth driver in the medical equipment market.

Restraints - High Capital and Maintenance Costs

The widespread adoption of advanced patient positioning equipment is constrained by high upfront costs and ongoing maintenance expenses. Devices such as motorized surgical tables, modular OR systems, and multi-functional positioning aids require substantial capital investment, which can be prohibitive for smaller hospitals and budget-limited clinics. The procurement process often depends on long-term investment planning, reimbursement considerations, and anticipated return on investment, limiting immediate adoption. Beyond initial purchase, maintenance, periodic calibration, and technical servicing add to the total cost of ownership, sometimes discouraging facilities from frequent upgrades or the acquisition of specialized models intended for low-volume surgical procedures.

These financial challenges may result in reliance on conventional or manual positioning methods, particularly in emerging markets or resource-constrained settings. Consequently, the high-cost barrier continues to act as a significant restraint, affecting the market penetration of technologically advanced patient positioning equipment despite its clinical and operational advantages.

Opportunity - Integration of Digital Technologies and Imaging

The integration of digital technologies and imaging solutions into patient positioning equipment presents a significant growth opportunity in the market. Innovations such as real-time pressure mapping, remote-controlled adjustments, pre-configured surgical presets, and seamless compatibility with imaging systems like C-arms are increasingly in demand. Hospitals upgrading to digital operating rooms require equipment that can interface with hospital information systems, enabling data-driven management of patient safety metrics and procedural outcomes. The adoption of smart sensors and AI-powered positioning guidance enhances precision during complex surgical procedures, reducing risks of tissue injury and improving overall workflow efficiency.

Modular platforms compatible with electronic health records allow for standardized documentation of patient positioning, supporting regulatory compliance and quality assurance initiatives. Additionally, advancements in digital connectivity facilitate telemonitoring, remote troubleshooting, and predictive maintenance, lowering operational downtime. Manufacturers investing in these integrated technologies can differentiate their products, capturing a growing share of hospitals seeking modernized, efficient, and patient-centric perioperative solutions. As the healthcare sector increasingly emphasizes precision, safety, and personalization in surgical care, digital-enabled patient positioning equipment represents a high-potential segment for market expansion.

Category-wise Analysis

By Product Type, Surgical Tables Dominates the Market

Surgical tables are the leading segment in the patient positioning equipment market, accounting for approximately 54% of global market share in 2025. Their dominance stems from their critical role in operating rooms across all surgical specialties, including orthopedic, cardiovascular, neurosurgical, and minimally invasive procedures. Modern surgical tables offer advanced features such as motorized height and tilt adjustments, programmable positioning memory, and full compatibility with imaging systems like C-arms, allowing precise intraoperative access and enhanced surgical accuracy.

Hospitals and ambulatory surgical centers (ASCs) increasingly prefer modular, multi-position, and electrically powered tables that can be configured for diverse procedures, improving both patient comfort and surgical ergonomics. The versatility of these tables ensures that they accommodate various patient body types, procedural requirements, and positioning accessories. Additionally, the growing focus on minimally invasive surgeries and complex interventions further reinforces demand for sophisticated surgical tables. Continuous technological innovation, combined with hospital investment in operating room modernization, ensures that surgical tables remain the backbone of patient positioning solutions, maintaining their market leadership over other equipment such as examination tables, stretcher chairs, and dental chairs.

By End-user, Hospitals Leads the Market

Hospitals represent the largest end-user segment in the patient positioning equipment market, holding around 48% of the market share in 2025. They perform the majority of inpatient and complex surgical procedures, necessitating advanced and reliable patient positioning solutions to comply with stringent safety, accreditation, and regulatory standards. Large hospital chains, academic medical centers, and tertiary care institutions often establish benchmarks for technology adoption, regularly updating surgical tables, examination tables, stretcher chairs, and accessory systems to align with evolving clinical requirements. The need to accommodate diverse surgical specialties, high patient throughput, and multidisciplinary operating teams’ drives the replacement cycle of positioning equipment, further reinforcing hospital dominance. Moreover, hospitals focus on integrating motorized, modular, and image-compatible tables to optimize surgical workflow, enhance patient safety, and support minimally invasive procedures. Combined with growing investments in operating room infrastructure and modernization initiatives, these factors ensure sustained demand from hospitals, making them the principal consumers of patient positioning solutions globally. The steady adoption of advanced equipment within hospitals continues to shape market growth and drive innovation.

Region-wise Insights

North America Patient Positioning Equipment Market Trends

North America leads the global patient positioning equipment market with about 39% share in 2025, propelled by advanced OR infrastructure, high surgical procedure rates, and early adoption of smart operating room technologies. The U.S. commands the largest regional market, supported by reimbursement policies favoring capital investment in surgical and examination platforms. Regulatory bodies such as the FDA enforce rigorous device standards and promote ergonomic safety, leading hospitals to invest in technologically advanced positioning solutions from trusted manufacturers such as Hill-Rom (Baxter), Stryker Corporation, and STERIS plc.

Innovation ecosystems in the U.S. foster collaboration between manufacturers, hospital procurement teams, and OR clinicians to refine features such as pressure-injury monitoring and C-arm imaging integration. Ongoing upgrades funded by federal programs and major health systems accelerate the adoption of digital and patient-centric positioning equipment in North American ORs, cementing the region’s market leadership.

Europe Patient Positioning Equipment Market Trends

Europe remains a highly developed region for patient positioning equipment, marked by strong regulatory frameworks, advanced public and private hospital networks, and robust adoption of ergonomic and safety-enhanced platforms. Top markets Germany, U.K., France, and Spain maintain consistent surgical procedure volumes and invest significantly in operation room modernization. Harmonization of medical device standards across the EU enhances equipment compatibility and procurement transparency, facilitating multi-country product launches.

European hospitals increasingly mandate solutions that meet environmental standards and pressure management guidelines established by local medical associations. Regional manufacturers and subsidiaries of global leader’s tailor offerings for national procurement requirements, resulting in a wide spectrum of basic to advanced examination and surgical positioning equipment penetrating the European marketplace.

Asia and Pacific Patient Positioning Equipment Market Trends

Asia Pacific is the fastest-growing market, fueled by vast investments in hospital infrastructure, rising healthcare expenditures, and a sharp uptick in elective surgeries across China, Japan, India, and ASEAN countries. Efforts to expand healthcare access and modernize medical facilities incorporate high-quality positioning systems in both urban and regional centers. Rapid construction of ASCs, coupled with government subsidies for technology upgrades, drives demand for multi-functional tables and ergonomic exam chairs.

Significant price sensitivity in many Asian markets encourages the adoption of value-based advanced yet affordable positioning products from global and domestic manufacturers. Additionally, the expanding private hospital sector fosters the introduction of imported and high-tech solutions, while local firms innovate lower-cost products catering to small and medium healthcare settings.

Market Competitive Landscape

The global patient positioning equipment market is moderately consolidated, led by established multinationals such as Hill-Rom (Baxter), Stryker Corporation, STERIS plc, Getinge AB, and Medtronic plc. Competition centers on technology upgrades, modular platform development, and expanding portfolios to support advanced imaging and minimally invasive procedures. Leaders emphasize partnerships with major health systems and continuous R&D investment, differentiating through integrated safety features, customizable modules, and compliance support. Smaller and regional players compete via niche product innovation and pricing flexibility tailored for high-growth emerging markets.

Key Industry Developments:

- In January 2025, Stryker Corporation launched a next generation powered surgical table equipped with advanced ergonomic features and digital memory settings, specifically designed for minimally invasive surgery suites.

- In August 2023, U.S. Surgitech, Inc. celebrated receiving a patent for its innovative SurgyPad patient positioning system.

Companies Covered in Patient Positioning Equipment Market

- Hill‑Rom (Baxter)

- Stryker Corporation

- STERIS plc

- Skytron, LLC.

- OPT SurgiSystems S.R.L.

- Medifa‑Hesse GmbH & Co. KG

- Getinge AB

- Medline Industries, LP

- Span America Medical Systems, Inc.

- Medtronic plc

- Others

Frequently Asked Questions

The global patient positioning equipment market is projected to be valued at US$ 1.3 Bn in 2026.

Major demand drivers include rising surgical procedure rates, expansion of minimally invasive techniques, and hospital modernization.

The global patient positioning equipment market is poised to witness a CAGR of 5.2% between 2026 and 2033.

Key opportunities arise from digital modular platforms, imaging-compatible systems, and workflow-optimized solutions tailored for emerging high-volume outpatient, ambulatory, and minimally invasive settings.

Leading players include Hill Rom (Baxter), Stryker Corporation, STERIS plc, Getinge AB, Medtronic plc, Medline Industries, LP, Skytron, LLC., and Span America Medical Systems, Inc.