- Healthcare Services

- Outpatient Clinics Market

Outpatient Clinics Market Size, Share, and Growth Forecast, 2026-2033

Outpatient Clinics Market by Service Type (Primary Care, Specialty Care, Diagnostics, Minor Procedures, Rehab, Mental Health), Facility Type (Standalone Clinics, Hospital-Affiliated, Ambulatory Surgical Centers (ASCs), Urgent Care, Community Health Centers), Technology (Telehealth, Remote Monitoring, EHR & Scheduling, AI Diagnostics), and Regional Analysis for 2026-2033

Outpatient Clinics Market Share and Trends Analysis

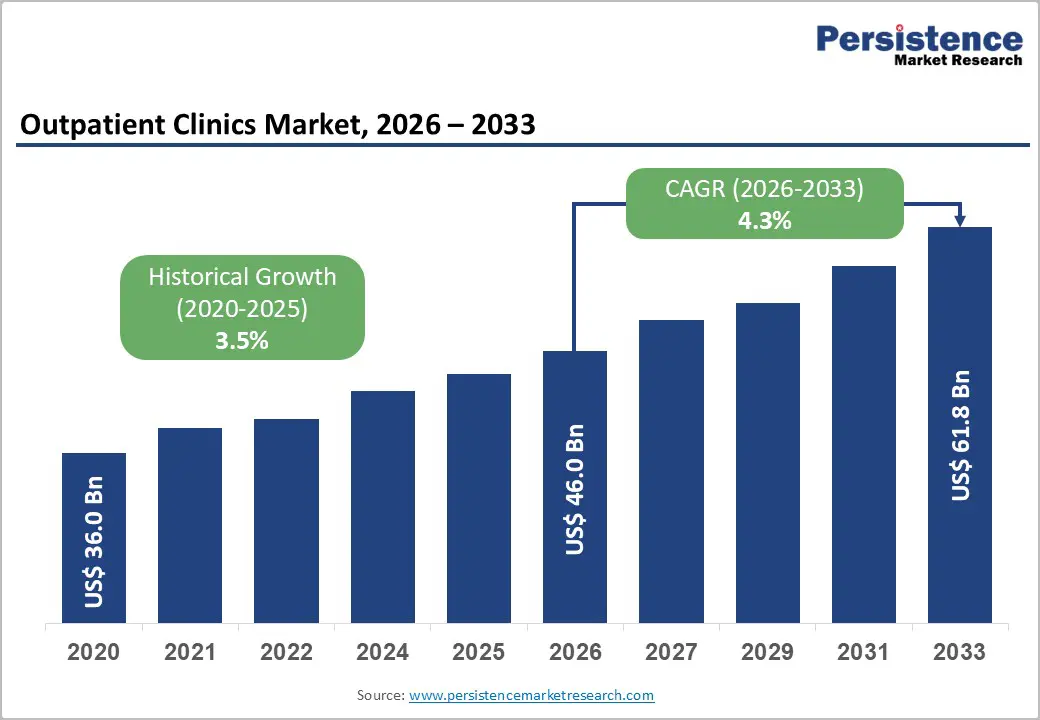

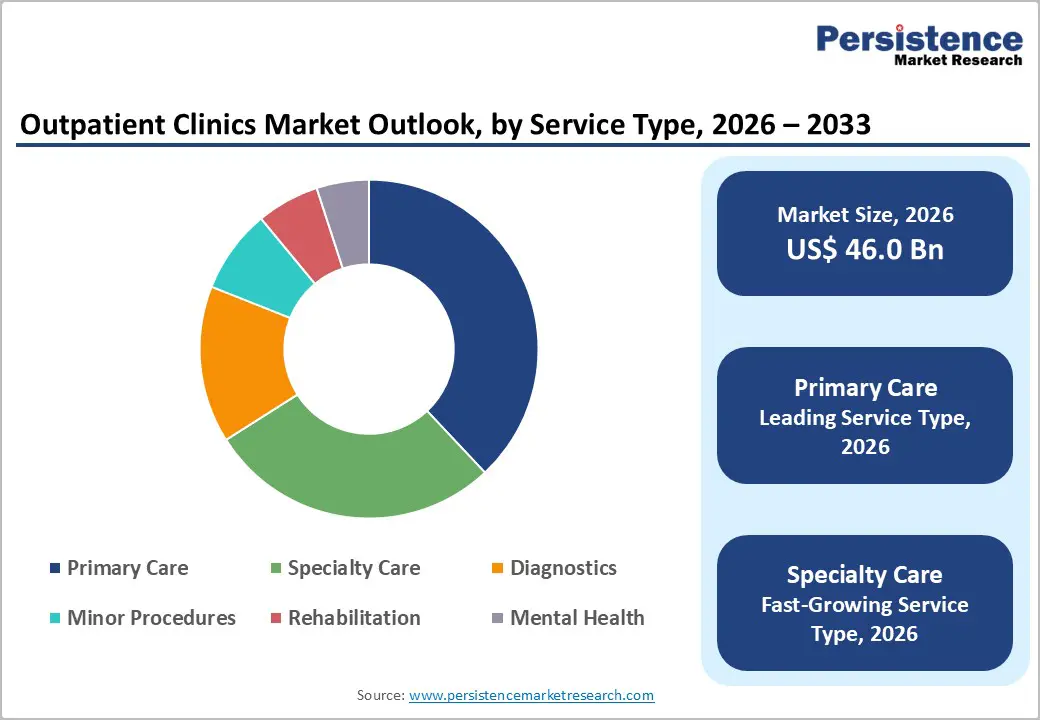

The global outpatient clinics market size is likely to be valued at US$ 46.0 billion in 2026, and is projected to reach US$ 61.8 billion by 2033, growing at a CAGR of 4.3% during the forecast period 2026–2033.

This growth is driven by a rising demand for cost-effective healthcare delivery, as patients and payers increasingly seek accessible and efficient alternatives to inpatient care. Demographic shifts toward aging populations amplify the need for continuous monitoring and management of chronic conditions, including diabetes, cardiovascular diseases, and musculoskeletal disorders. Simultaneously, healthcare providers are actively adopting digital technologies, such as telehealth, remote patient monitoring, and AI-enabled diagnostics, to enhance care accessibility and streamline clinical workflows. The increasing prevalence of chronic diseases has prompted outpatient clinics to diversify services, while healthcare systems emphasize ambulatory care to reduce hospital congestion, lower treatment costs, and improve overall operational efficiency.

Key Industry Highlights

- Dominant Service Type: Primary care services are expected to command around 38% of revenue in 2026, while specialty care services are likely to grow the fastest at a 5.8% CAGR through 2033, driven by high chronic disease prevalence.

- Leading Facility Type: Standalone clinics are expected to lead with approximately 41% share in 2026, while ambulatory surgical centers (ASCs) are likely to be the fastest-growing during 2026–2033, reflecting increasing adoption of outpatient procedures.

- Dominant Technology: Telehealth solutions are anticipated to lead with an estimated 33% share in 2026, while AI diagnostics are slated to record the highest 2026-2033 CAGR, aided by predictive analytics and clinical workflow integration.

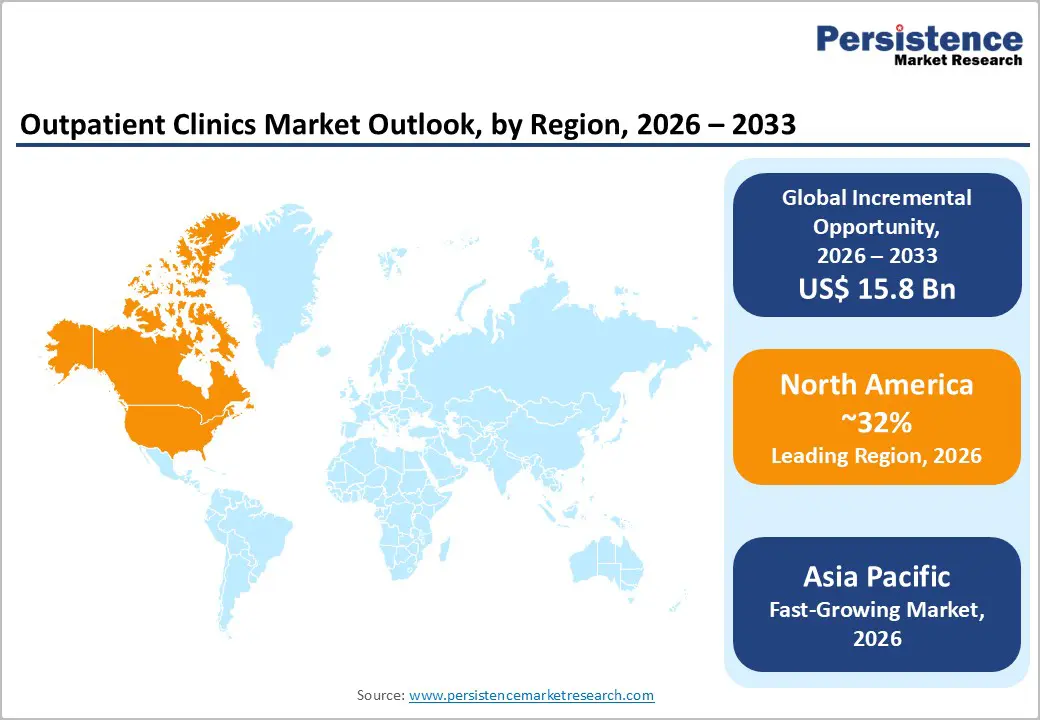

- Regional Leadership: North America is poised to dominate with an estimated 32% share in 2026, led by advanced healthcare infrastructure and wide insurance coverage.

- Emerging Market Growth: The Asia Pacific market is expected to grow at a 5.9% CAGR through 2033, driven by expanding healthcare access and telehealth adoption.

- Competitive Environment: Strategic acquisitions, AI integration, digital health partnerships, and outpatient network expansions targeting both developed and emerging markets are the prime focus areas of top players.

| Key Insights | Details |

|---|---|

|

Outpatient Clinics Market Size (2026E) |

US$ 46.0 Bn |

|

Market Value Forecast (2033F) |

US$ 61.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Aging Populations and Rising Chronic Disease Burden

The global population is aging at an unprecedented pace, with people aged 65+ increasingly seeking continuous and preventive care. Outpatient clinics provide accessible chronic disease management, early diagnostics, follow-up care, and routine interventions that reduce hospital admissions and lower overall system costs. Chronic conditions such as cardiovascular, metabolic, and musculoskeletal disorders require consistent monitoring and long-term care coordination, making outpatient settings indispensable for evolving healthcare needs. This persistent demand played a key role in sustaining the market’s historical growth and remains a foundation for continued growth through 2033.

Public health systems are reinforcing outpatient models to support chronic disease care outside hospitals. Several European health authorities are formalizing digital-front-door and outpatient-first strategies that prioritize telehealth, electronic health records (EHRs), and remote monitoring as gateways to care. These strategies are intended to relieve inpatient pressure and expand preventive care capacity, especially for populations managing long-term conditions. Such policy orientations underscore healthcare systems’ strategic shift toward outpatient care to serve aging populations efficiently while maintaining continuity and quality of care.

Digital Healthcare Integration and Value-Based Care Adoption

Outpatient clinics are increasingly adopting digital healthcare technologies such as telehealth, remote monitoring, interoperable EHR systems, and AI-enabled diagnostics. These tools allow clinics to extend patient reach, streamline workflows, and enhance chronic disease management through real-time data tracking. Telehealth has become a core channel for consultations, follow-ups, and monitoring, reducing system strain while improving patient engagement. Clinics can now deliver care more efficiently, lower operational costs, and maintain continuous oversight for patients with long-term conditions. These innovations are essential for meeting rising outpatient demand. Digital integration also improves coordination with hospitals, pharmacies, and other care providers.

Recent policy developments have reinforced this digital transition. In the U.S., Medicare telehealth flexibilities were extended through 2027, under the Consolidated Appropriations Act, maintaining expanded reimbursement and geographic waivers for virtual visits. Europe has implemented digital health data exchange frameworks to standardize patient information sharing and enhance interoperability. These regulatory measures incentivize clinics to adopt technology while supporting value-based care models linking reimbursement to quality outcomes. These trends enable outpatient clinics to deliver data-driven, patient-centered services while improving efficiency, care quality, and long-term cost savings.

Regulatory and Licensing Complexities

Outpatient clinics operate within strict and varied regulatory frameworks that govern licensing, patient privacy, and reimbursement compliance. Laws such as the Health Insurance Portability and Accountability Act (HIPAA) in the U.S. and the General Data Protection Regulation (GDPR) in Europe enforce rigorous standards for data handling, storage, and reporting. These requirements increase administrative overhead and slow down clinic setup or expansion. Multidisciplinary and cross-jurisdiction practices face additional hurdles, as providers must navigate different rules across states or countries. The complexity of these regulations can limit investment opportunities and reduce operational flexibility, posing a structural restraint on outpatient market growth.

Recent developments illustrate these challenges. In June 2025, the government of Pennsylvania implemented multistate health care licensure compacts, allowing qualified doctors, nurses, and therapists to practice across several states under uniform standards. While this reform eases mobility for compact participants, it also highlights the fragmented licensing landscape in jurisdictions not covered by the compacts. Providers outside the compact still face time-consuming approvals, which restrict workforce mobility and slow the scaling of outpatient clinics. This example demonstrates that even with targeted policy changes, regulatory complexity remains a key market restraint.

Workforce Shortages and Infrastructure Costs

Outpatient providers continue to face significant workforce shortages, particularly for specialized clinicians, nurses, and diagnostic technicians, who are essential to delivering routine and advanced services. These shortages increase staffing costs, extend appointment wait times, and constrain service capacity, especially in high-demand specialty areas. Burnout and turnover further intensify recruitment challenges, as clinics compete with hospitals and larger systems for a limited pool of qualified professionals. Clinics also face elevated infrastructure costs for digital systems, diagnostic tools, and staffing overhead, which can delay expansion and reduce operational flexibility.

In the U.K., a 93% decline in overseas nurses arriving to work due to changes in immigration and visa conditions was widely reported, exposing the fragility of staffing models that depend on international recruitment and highlighting the potential for deeper service bottlenecks. Such systemic strains reflect broader shortages of clinical roles worldwide, underscoring that workforce constraints, coupled with capital requirements for training, equipment, and digital infrastructure, remain significant constraints on outpatient clinic performance and scale.

Expansion into Emerging Economies and Digital Healthcare Adoption

Emerging markets in the Asia Pacific, especially China and Southeast Asian countries, offer strong growth opportunities driven by expanding healthcare access and rising demand for outpatient services. Governments are incorporating preventive care and digital platforms into national health agendas, aiming to improve service delivery far beyond traditional hospital settings. Outpatient clinics that establish a presence in these regions can capture significant patient volumes and diversify revenue streams as demand shifts away from inpatient care. Clinics can also leverage local public-private partnerships to optimize infrastructure utilization and gain early market advantages over competitors.

Countries such as Vietnam have approved national health programs for 2026 that include free screenings and EHR systems, enabling broader data integration and continuity of care. Additionally, healthcare providers are extending operations internationally, with major providers exploring partnerships and outpatient initiatives in nations such as Iraq, Tanzania, and Indonesia, reflecting a global approach to outpatient service expansion. These movements highlight real momentum in international healthcare infrastructure, digital adoption, and patient-centered service models that outpatient clinics can strategically leverage.

Technology Integration and Strategic Partnerships

Integration of AI-enabled diagnostics, predictive analytics, and clinical decision support systems presents outpatient clinics with a strategic opportunity to enhance care quality, operational efficiency, and patient outcomes. Advanced technologies can accelerate diagnostic processes, personalize treatment plans, and improve chronic disease outcomes, thereby strengthening patient satisfaction and clinical performance. Clinics that adopt these digital innovations can differentiate services, attract new patient segments, and potentially access new reimbursement pathways tied to outcomes rather than volume. Broader adoption also allows clinics to build scalable, data-driven care models that improve long-term sustainability.

Government actions in 2025–2026 are reinforcing this trend. In the United States, the Centers for Medicare & Medicaid Services (CMS) launched the ACCESS pilot to expand technology-supported chronic care delivery, incentivizing providers to adopt digital tools to manage conditions such as hypertension and diabetes. Expanded telehealth flexibilities through early 2026 also continue to enable remote care delivery, reinforcing technology as a core part of outpatient services. These initiatives, coupled with increasing investments in AI-enabled diagnostics across Europe and Asia Pacific, underline the structural shift toward tech-enabled outpatient care that reduces hospital load, enhances patient access, and positions early adopters for long-term competitive advantage.

Category-wise Analysis

Service Type Insights

Primary care is expected to remain the leading service type, accounting for approximately 38% of the outpatient clinics market revenue share in 2026, driven by routine health screenings, preventive care, and chronic disease management. Its broad patient base ensures stable revenue and strong referral pathways into specialty services. Clinics benefit from policies emphasizing cost-effective, community-based care and continuity of patient management. In late 2025, the U.S. CMS proposed shifting more payment value toward primary care and freestanding outpatient clinics in the 2026 payment rule, rebalancing incentives away from hospital outpatient departments and supporting sustained growth.

Specialty care is the fastest-growing service type, projected at a 5.8% CAGR from 2026 to 2033, fueled by procedure migration from hospitals and rising chronic illness prevalence. Specialty clinics, including cardiology, orthopedics, and oncology, leverage advanced equipment, multidisciplinary teams, and digital scheduling systems to enhance efficiency and patient outcomes. In early 2026, HCA Healthcare expanded its outpatient specialty network, emphasizing ambulatory surgical operations and advanced diagnostics, demonstrating real-world growth and confirming strong market momentum for specialty outpatient services.

Facility Type Insights

Standalone outpatient clinics are likely to dominate with an estimated 41% market share in 2026, driven by operational flexibility, patient-centric care, and rapid adoption of digital healthcare technologies. By maintaining independence from hospital systems, these clinics are customizing service delivery, integrating cloud-based EHR systems, scheduling platforms, and telehealth solutions to improve efficiency, patient engagement, and continuity of care. CMS reforms in 2025–2026, promoting office-based outpatient care, are further encouraging investment in digital infrastructure and expanding community access. Over the coming years, standalone clinics are expected to achieve operational scalability, optimize workflows, and strengthen their role as key drivers of cost-effective, accessible, and high-quality outpatient healthcare.

Ambulatory Surgical Centers are poised to be the fastest-growing facility type, with a 6.2% CAGR through 2033, as they deliver cost-efficient, same-day surgical procedures through streamlined operations and advanced technology. ASCs are enhancing patient convenience and procedural efficiency, particularly for orthopedic, ophthalmology, and minor surgical interventions. In December 2025, Medicare expanded prior authorization for certain ASC procedures, acknowledging rising procedural volumes and clinical significance. These facilities are investing in minimally invasive techniques, digital scheduling, and postoperative care platforms, enabling operational scalability and improved patient outcomes. Over time, ASCs will strengthen their position in outpatient surgical care and attract the attention of both private and public payers.

Regional Insights

North America Outpatient Clinics Market Trends

North America is expected to hold an approximate 32% outpatient clinics market share in 2026, propelled by advanced healthcare infrastructure, high insurance coverage, and patient preference for ambulatory care. The United States drives much of this demand through policies that encourage care delivery outside hospital settings, with providers increasingly focusing on chronic disease management, preventive services, and community-based care. Technology adoption, including telehealth, remote patient monitoring, AI diagnostics, and interoperable electronic health records, is widespread across large health systems and independent clinic networks. Site-neutral payment reforms finalized by the U.S. CMS are reducing cost disparities between hospital outpatient departments and other outpatient sites, making outpatient care more financially attractive for providers and patients alike.

Public investment is also shaping growth in underserved communities. In late 2025, the federal Rural Health Transformation (RHT) Program secured US$ 50 billion to strengthen rural health services across all 50 states, including support for clinics, facilities, and workforce expansion, which will expand outpatient access and infrastructure in hard-to-reach areas. This long-term funding is expected to improve care continuity for chronic conditions and increase clinic sustainability. Cross-border activity continues as Canadian and Mexican providers explore alliances with U.S. outpatient networks, reflecting North America’s strategic importance for future expansion. Given these structural drivers, North America is positioned to sustain robust growth and reinforce its leadership position through 2033.

Europe Outpatient Clinics Market Trends

Europe holds a substantial portion of the outpatient clinics market share, supported by universal healthcare systems, preventive care models, and policy frameworks that prioritize community-oriented service delivery. Countries such as Germany, the U.K., France, and Spain are increasing outpatient utilization to reduce pressure on hospitals and improve population health outcomes. For example, national digital health strategies across the European Union (EU) are rolling out unified electronic booking and digital patient ID systems, enabling millions of outpatient appointments to be scheduled efficiently and securely. Member states are also piloting AI applications in diagnostics and screening to enhance early detection and optimize clinical workflows.

In the U.K., government-backed digital transformation plans are redefining outpatient care delivery, with proposals for an enhanced patient-centric health app that enables self-referrals, appointment bookings, and access to unified medical records. While this “doctor in your pocket” initiative aims to modernize service access and relieve hospital load, health leaders acknowledge ongoing workforce and funding challenges that may impact rollout timelines. Europe’s regulatory harmonization, public funding mechanisms, and commitment to digital health innovation underpin a stable and steadily expanding outpatient market, while engagement with data interoperability and AI promises to improve care delivery and patient outcomes across regional systems.

Asia Pacific Outpatient Clinics Market Trends

Is Asia Pacific poised to become the fastest-growing regional market for outpatient clinics, with a CAGR of approximately 5.9% from 2026 to 2033, led by China, India, and the ASEAN block? Growth is driven by expanding healthcare access, rising incomes, demographic transitions, and rapid technology adoption. In China, outpatient services are benefiting from policy priorities that expand community health services and integrate digital health platforms, while in India, the growing middle class and increasing insurance penetration are driving demand for affordable outpatient care. ASEAN members are attracting investment in telemedicine, digital diagnostics, and scalable care models addressing rapid urbanization and population growth.

Apollo Hospitals announced expansion plans in Iraq, Tanzania, and Indonesia, focusing on outpatient care, teleconsultation, and digital health technologies for international markets. This reflects the real-world globalization of outpatient care expertise emerging from Asia Pacific providers and highlights the region’s influence in shaping care delivery beyond domestic borders. Public–private partnerships are also emerging to boost digital infrastructure, telehealth platforms, and rural clinic networks. Regulatory reforms in India are simplifying clinic licensing and supporting the adoption of digital clinical solutions, creating a favorable environment for both domestic and multinational outpatient care expansion. These trends are expected to drive above-average market growth and position Asia Pacific as a critical engine of global outpatient clinic demand.

Competitive Landscape

The global outpatient clinics market structure is moderately consolidated, with top players such as HCA Healthcare, Fresenius Medical Care, Apollo Hospitals, and Tenet Healthcare holding a significant share in 2026. These providers leverage large healthcare networks, integrated care pathways, and strong payer relationships. They are investing in telehealth, EHR, remote monitoring, and AI diagnostics to improve efficiency and patient outcomes. Their scale and digital capabilities allow them to lead in service quality and operational performance.

Regional and niche competitors, including Kaiser Permanente, Ramsay Health Care, and IHH Healthcare, focus on specialized services and targeted geographies. High regulatory compliance, licensing requirements, and infrastructure costs limit new entrants. Technology adoption allows telemedicine startups and software-focused providers to integrate into the outpatient ecosystem. Market consolidation is expected to rise as leading networks acquire smaller clinics and partner with digital health firms to enhance care coordination.

Key Industry Developments

- In November 2025, GE HealthCare acquired Intelerad for US$ 2.3 billion to expand into outpatient imaging, integrating AI-enabled workflows and cloud-based PACS solutions. This deal strengthens recurring revenue and efficiency in ambulatory diagnostics.

- In July 2025, Nordic Capital invested an undisclosed majority stake valued over US$ 500 million in Arcadia Solutions to grow its AI-powered analytics for outpatient and value-based care. The deal enhances predictive insights and clinical decision support tools globally.

- In May 2025, Fortis Healthcare opened a super specialty outpatient department (OPD) clinic to deliver advanced, multidisciplinary consultations and improve access to specialized care without hospital admission. The facility is enhancing patient convenience by integrating expert consultations, diagnostics, and treatment planning within an outpatient setting.

Companies Covered in Outpatient Clinics Market

- Mayo Clinic

- Johns Hopkins Medicine

- MD Anderson Cancer Center

- Cleveland Clinic

- DaVita Inc.

- Fresenius Medical Care

- Kaiser Permanente Inc.

- Tenet Healthcare Corporation

- Community Health Systems

- Apollo Hospitals Enterprise Ltd.

- Universal Health Services

- Mount Sinai Health System

- Narayana Health

- Ramsay Health Care

- Mediclinic International

Frequently Asked Questions

The global outpatient clinics market is projected to reach US$ 46.0 billion in 2026.

Surging chronic disease prevalence, aging populations, and adoption of digital health technologies are driving the market.

The market is poised to witness a CAGR of 4.3% from 2026 to 2033.

Expanding into emerging economies and integrating AI diagnostics and telehealth offer significant opportunities.

HCA Healthcare, Fresenius Medical Care, Apollo Hospitals, and Tenet Healthcare are some of the leading players in the market.