- Hardware & Software IT Services

- Patient Throughput and Capacity Management Market

Patient Throughput and Capacity Management Market Size, Share, and Growth Forecast, 2026 - 2033

Patient Throughput and Capacity Management Market by Component Type (Software, Services.), Application (Patient Flow Management, Capacity & Bed Management, ED & OR Throughput Optimization, Command Center & Operational Analytics, Misc.) , Deployment Mode (Cloud, On-Premises, Hybrid), End User (Hospitals, Ambulatory & Outpatient Centers, Integrated Delivery Networks (IDNs), Government/Defense Healthcare Facilities, Misc) and Regional Analysis for 2026 - 2033

Patient Throughput and Capacity Management Market Size and Trends Analysis

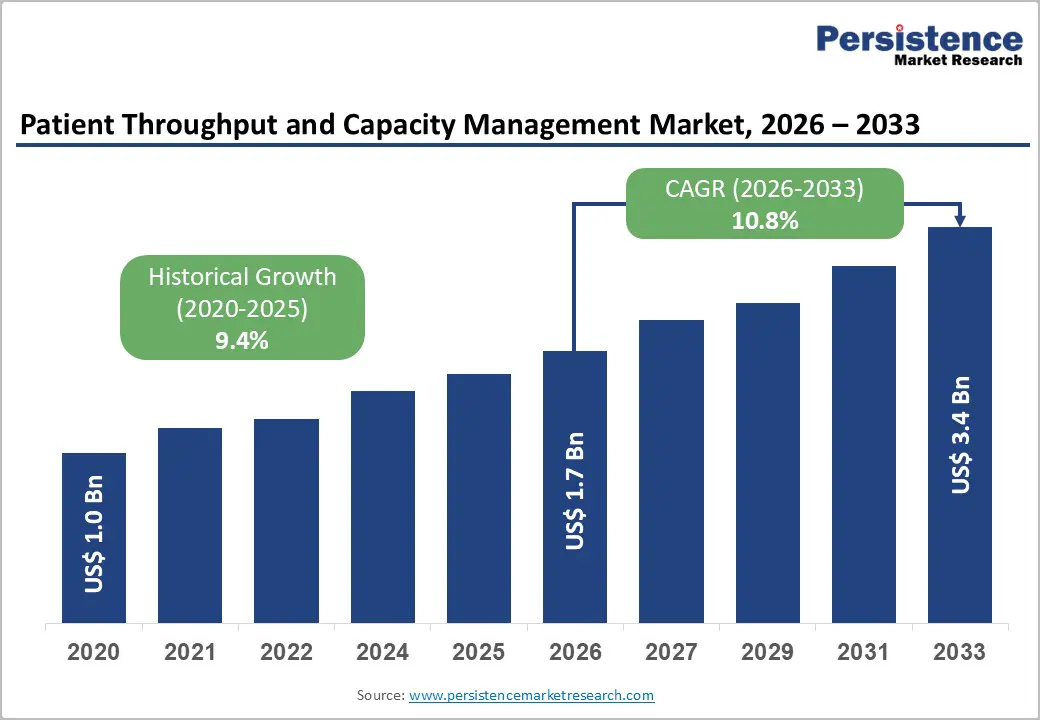

The Global Patient Throughput and Capacity Management Market size was valued at US$ 1.7 billion in 2026 and is projected to reach US$ 3.4 billion by 2033, growing at a CAGR of 10.8% between 2026 and 2033. The market's expansion reflects a critical healthcare imperative: optimizing patient movement from admission through discharge while managing constrained institutional resources.

Healthcare providers face mounting pressures from aging populations, escalating chronic disease prevalence, and persistent workforce shortages that necessitate sophisticated operational management solutions. The adoption of digital technologies particularly artificial intelligence and real-time location systems enables hospitals and health systems to improve operational efficiency, reduce patient wait times, and enhance resource utilization across care settings.

Key Industry Highlights:

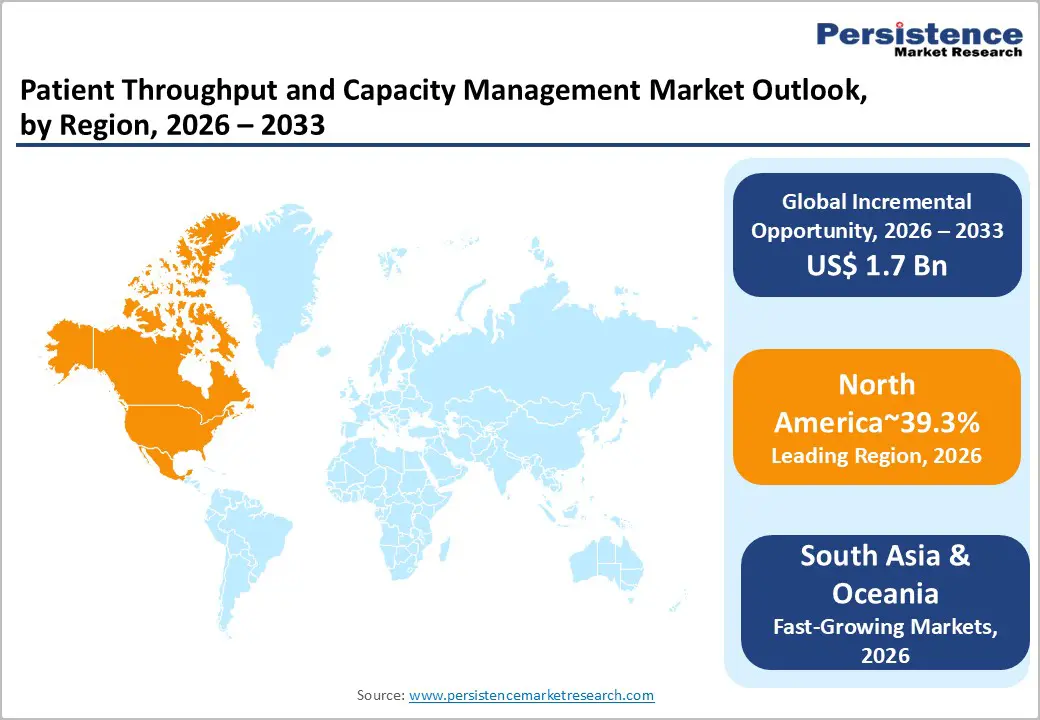

- Regional Leadership: North America leads the global Patient Throughput and Capacity Management Market with 39.3% share, driven by advanced healthcare IT infrastructure, early technology adoption, and value-based care initiatives incentivizing operational efficiency.

- Strong European Presence: Europe accounts for 26% of the market, fueled by workforce shortages, aging populations, stringent data protection regulations, and post-pandemic healthcare system optimization programs.

- Emerging Asia-Pacific Opportunities: East Asia represents 18–20% of the market, driven by rapidly aging populations, government-backed digital healthcare initiatives, infrastructure expansion, and adoption of cloud-based patient flow solutions in China, India, and Japan.

- Leading Solution Segment: Software dominates with 61.5% market share, providing real-time bed management, patient flow visualization, staff scheduling optimization, and operational analytics across hospital departments.

- Fastest-Growing Segment: Services are the fastest-growing component, reflecting high demand for consulting, integration, training, and ongoing operational support to ensure effective technology deployment.

| Key Insights | Details |

|---|---|

|

Patient Throughput and Capacity Management Market Size (2026E) |

US$ 1.7 Bn |

|

Market Value Forecast (2033F) |

US$ 3.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.4% |

Market Dynamics

Growth Drivers

Healthcare Workforce Constraints and Operational Necessity

The global healthcare sector faces an unprecedented workforce crisis that fundamentally drives adoption of Patient Throughput and Capacity Management solutions. The European Union confronts an estimated shortfall of 1.2 million doctors, nurses, and midwives, compounded by aging medical professionals and declining youth interest in healthcare careers. In the United States, physician shortages are projected to reach 86,000 by 2036, with the American Hospital Association anticipating approximately 100,000 critical healthcare worker shortages by 2028. These structural labor gaps force healthcare institutions to maximize the productivity of existing clinical and administrative staff through sophisticated operational systems

Patient Throughput and Capacity Management technology addresses this constraint by automating non-clinical coordination tasks, optimizing scheduling efficiency, and eliminating operational bottlenecks that consume staff time without adding clinical value. Organizations implementing these solutions report reducing patient wait times by approximately 30 percent through predictive analytics and real-time resource allocation. The ability to process patients more efficiently with existing workforce levels has become a strategic imperative, directly justifying technology investments that were previously considered discretionary.

Demographic Pressures and Chronic Disease Demand

Global demographic shifts toward older populations are fundamentally altering healthcare demand patterns and capacity requirements. Approximately one-third of the European Union's population will exceed 65 years of age by 2050, a structural shift that permanently increases demand for hospital-based and long-term care services. Within this demographic cohort, average hospital length of stay has increased by 15 percent from 2010 to 2024, rising from 5.4 days to 6.2 days, driven by the complexity of managing multiple comorbidities and delayed discharge arrangements. The prevalence of chronic conditions, including cardiovascular disease, diabetes, and neurodegenerative disorders necessitates ongoing medical attention and specialized interventions.

Patient Throughput and Capacity Management solutions address these demand challenges through predictive analytics that forecast patient volumes across disease categories, optimizing bed allocation and staffing deployment in anticipation of demand fluctuations. India's healthcare sector, supporting 7.5 million workers and experiencing substantial government investment through initiatives such as Ayushman Bharat and Tele-MANAS, exemplifies the convergence of demographic demand and policy support driving technology adoption across diverse economic contexts. The ability to accommodate higher patient volumes without proportional infrastructure expansion directly enables healthcare systems to respond to aging populations while managing capital constraints.

Technological Convergence and Real-Time Operational Intelligence

Advances in artificial intelligence, machine learning, and real-time location systems (RTLS) technology have fundamentally transformed the feasibility and value proposition of Patient Throughput and Capacity Management solutions. RTLS systems, deploying RFID, Wi-Fi, and infrared technologies, enable real-time tracking of patients, staff, and clinical assets throughout healthcare facilities, capturing operational data previously unavailable for analysis. Machine learning models trained in historical admission patterns, discharge trends, and seasonal illness variations can now forecast future capacity needs with high statistical accuracy, enabling hospitals to make proactive rather than reactive operational decisions.

The November 2025 launch of Decision IQ by TeleTracking Technologies represents a significant technological inflection point, introducing the first AI-driven "computational twin" that simulates capacity scenarios and provides real-time proactive guidance to eliminate hospital bottlenecks.

King Faisal Specialist Hospital achieved median inpatient wait time reduction from 13 plus hours in 2023 to 3.2 hours in mid-2025 through deployment of an AI-enabled Patient Flow & Capacity Command Centre using real-time operational monitoring and predictive analytics. These deployments validate that technological maturity has reached sufficient sophistication to justify enterprise-scale implementation, accelerating market adoption across healthcare systems globally.

Market Restraining Factors

Implementation of Complexity and Legacy System Integration Challenges

Hospital and health system IT environments typically comprise multiple Electronic Health Record (EHR) platforms, departmental systems, and legacy infrastructure deployed over decades, creating substantial technical integration barriers for new Patient Throughput and Capacity Management solutions. Effective deployment requires real-time data exchange with EHR systems, admission-discharge-transfer (ADT) platforms, and department-specific scheduling applications, each operating under distinct data governance frameworks and security protocols.

Organizations implementing new capacity management platforms frequently require 6–18-month integration cycles, substantial IT resource allocation, and organizational change management efforts to achieve full operational capability. These implementation demands create financial barriers for smaller health systems and resource-constrained providers, particularly in developing healthcare markets where IT infrastructure investment remains limited.

Key Market Opportunities

Artificial Intelligence and Predictive Analytics Convergence

The integration of advanced artificial intelligence and machine learning capabilities into Patient Throughput and Capacity Management solutions represents a substantial market opportunity for technology providers. Contemporary AI systems can now predict patient admissions with high accuracy by analyzing historical admission patterns, identify patients ready for discharge before clinical teams recognize discharge criteria, and optimize operating room scheduling to maximize surgical throughput while maintaining clinical safety standards.

Research published by the National Institutes of Health demonstrates that AI discharge prediction tools can significantly reduce discharge delays by a common operational bottleneck by identifying patients ready for discharge and their discharge barriers, enabling proactive interventions by clinical teams.

The market continues to attract significant innovation investment focused on expanding AI capabilities to support appointment scheduling optimization, emergency department admission prediction, and ward transfer anticipation. Healthcare organizations implement these advanced analytics reports around 25 percent relative reductions in hospital readmissions and corresponding improvements in operational efficiency metrics. As AI algorithm accuracy continues to improve through expanded training datasets and methodological refinement, the value proposition for organizations not yet deployed these technologies continues to strengthen, supporting accelerated adoption rates across healthcare systems worldwide.

Cloud-Based Deployment and Scalability Solutions

Cloud-based deployment models represent an emerging opportunity within the Patient Throughput and Capacity Management market, particularly for healthcare organizations seeking cost-effective solutions that avoid substantial capital infrastructure investment. Cloud deployment reduces initial costs by 25-40 percent relative to on-premise deployment over 3–5-year periods, eliminates the requirement for dedicated IT staff to maintain local infrastructure, and enables rapid feature updates deployed by solution providers.

Cloud architecture provides inherent scalability, enabling healthcare organizations to adjust computational resources in response to demand fluctuations without requiring advance hardware procurement and deployment cycles.

The October 2024 launch of Capacity IQ by TeleTracking Technologies, a SaaS version of its established Capacity Management Suite exemplifies this market opportunity. Smaller health systems and community hospitals lacking dedicated IT infrastructure and capital budgets can now access enterprise-grade Patient Throughput and Capacity Management capabilities through cloud-based platforms with significantly lower total cost of ownership.

Regional healthcare markets in Asia-Pacific and Latin America represent opportunities for cloud deployment models, as these regions simultaneously experience healthcare infrastructure expansion, limited capital availability for on-premises IT systems, and regulatory environments increasingly supporting cloud healthcare solutions. The SaaS delivery model enables solution providers to address geographically dispersed markets and diverse organizational sizes more efficiently.

Category-wise Analysis

Middleware Type Insights

The Software component segment demonstrates dominant market positioning with 61.5% market share in 2026, reflecting the fundamental requirement for digital platforms to support Patient Throughput and Capacity Management operations. Healthcare software solutions addressing patient throughput integrate multiple operational functions including bed management, patient flow visualization, staff scheduling optimization, and real-time capacity reporting into unified platforms accessible across hospital departments. Software platforms serve as the operational backbone enabling healthcare organizations to transform raw data from electronic health records and hospital information systems into actionable intelligence for clinical and administrative decision-making.

Major healthcare information technology companies including Epic Systems, Cerner (acquired by Oracle), Allscripts, and McKesson have integrated Patient Throughput and Capacity Management capabilities directly into comprehensive healthcare IT platforms. These integrated solutions reduce implementation complexity by leveraging existing EHR data and system infrastructure already deployed within healthcare organizations. The dominance of software reflects the essential role that digital platforms play in contemporary healthcare operations, where patient flow optimization depends fundamentally upon real-time visibility into bed availability, staff allocation, and operational bottlenecks across geographically distributed facilities.

The Services component emerges as the fastest-growing segment within the Patient Throughput and Capacity Management market, reflecting the increasing recognition that technology implementation success depends critically upon consulting, integration, training, and ongoing operational support services.

End User Insights

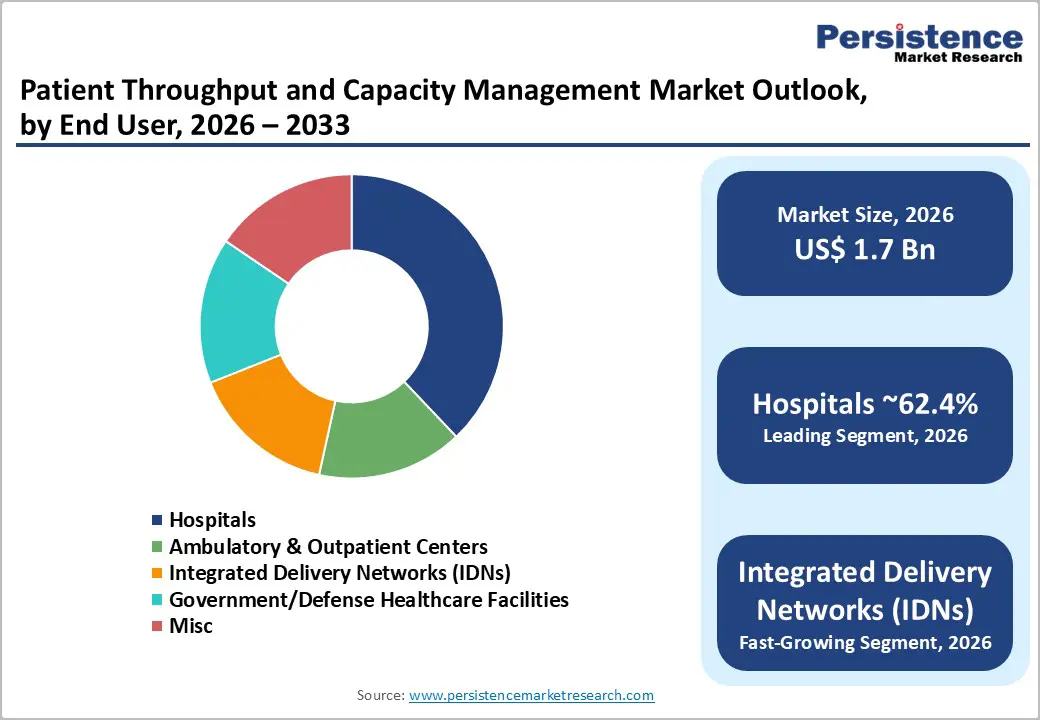

Hospitals represent the dominant end-user segment with 62.4% market share in 2026, reflecting the complexity of hospital operations and the acute operational challenges that patient throughput management addresses. Large teaching hospitals, regional medical centers, and community hospitals all confront substantial daily operational challenges balancing emergency department volumes, surgical schedules, medical/surgical bed availability, and staff allocation across multiple clinical departments and specialized care units.

Hospital operations involve continuous coordination across emergency departments, operating rooms, medical/surgical units, intensive care units, and discharge planning functions each with distinct patient volume patterns, length-of-stay characteristics, and resource requirements.

Integrated Delivery Networks (IDNs) comprising hospitals, ambulatory surgical centers, physician practices, and outpatient clinics operating under unified governance and shared health information systems represent the fastest-growing end-user segment for Patient Throughput and Capacity Management solutions. IDN structures create operational opportunities for system-level patient throughput optimization that cannot be achieved by independent hospitals, as IDN management can coordinate patient movement across multiple facility types and care settings to optimize overall system efficiency rather than individual facility metrics.

Regional Insights and Trends

North America Market Trend

North America commands the largest global market share at 39.3%, reflecting advanced healthcare infrastructure, early technology adoption, and substantial healthcare IT investment within the United States and Canada. The U.S. healthcare system, while fragmented across thousands of independent hospitals and health systems, prioritizes operational efficiency driven by Medicare quality reporting requirements and value-based purchasing programs that directly link reimbursement to operational performance metrics.

The Hospital Price Transparency Rule and Centers for Medicare & Medicaid Services (CMS) quality initiatives have created direct financial incentives for hospitals to reduce length of stay, minimize emergency department boarding times, and optimize bed utilization operational goals directly addressed by Patient Throughput and Capacity Management solutions.

Healthcare IT maturity within North America enables rapid deployment of sophisticated platform capabilities, as most hospitals and health systems have already implemented comprehensive electronic health record systems that serve as foundational data sources for capacity management platforms.

East Asia Market Trend

East Asia represents a strategically important emerging market within Patient Throughput and Capacity Management, driven by rapid healthcare infrastructure expansion, increasing patient volumes, and substantial government investment in healthcare digital transformation initiatives. China, India, and Japan collectively represent the largest healthcare markets within the region, with distinct market characteristics and growth drivers.

East Asia's demographic trajectory with rapidly aging populations throughout Japan and South Korea, and aging acceleration anticipated across China over coming decades creates long-term structural demand for healthcare capacity management solutions. Healthcare systems throughout East Asia are simultaneously experiencing physician and nursing shortages similar to global patterns, strengthening the business case for technology solutions that optimize productivity of available clinical staff. Cloud-based Patient Throughput and Capacity Management platforms represent particularly suitable deployment models for East Asian healthcare markets, as they avoid substantial capital infrastructure investment while providing access to technology capabilities that North American and European providers have already validated.

Europe Market Trend

Europe's Patient Throughput and Capacity Management market, comprising 26% of global market share, reflects mature healthcare systems navigating post-pandemic recovery, workforce crisis management, and regulatory compliance requirements around data protection and healthcare quality standards. The European Union healthcare system faces a documented shortage of 1.2 million healthcare professionals including doctors, nurses, and midwives, with particular acuity in Central and Eastern European countries experiencing health worker migration to Western European nations and North America.

European healthcare systems are implementing Patient Throughput and Capacity Management solutions as operational responses to workforce constraints, with emphasis on technologies that optimize productivity of remaining healthcare professionals and reduce administrative burden consuming clinical time.

The National Health Service in the United Kingdom launched the Urgent and Emergency Care Services Recovery Plan in March 2024, explicitly identifying digital tools supporting real-time operational decision-making as strategic priorities for improving healthcare system performance and patient outcomes. European healthcare providers increasingly adopt cloud-based patient flow management platforms that reduce local IT infrastructure requirements and operational burden on constrained IT departments

European regulatory frameworks particularly GDPR data protection requirements and healthcare-specific regulations around medical data handling create specific compliance requirements for Patient Throughput and Capacity Management platform providers. European healthcare organizations frequently prefer platform implementations providing maximum data control and security, sometimes favoring on-premises deployments despite higher operational costs.

Competitive Landscape

The Global Patient Throughput and Capacity Management Market is moderately fragmented with pockets of consolidation, characterized by the presence of both large healthcare IT incumbents and specialized solution providers. Leading players such as TeleTracking Technologies, Epic Systems, Cerner (Oracle Health), McKesson, Allscripts, GE Healthcare, and Philips Healthcare hold significant influence, offering integrated platforms for patient flow, bed management, and operational analytics.

Niche providers like STANLEY Healthcare, CenTrak, and Care Logistics further add to the competitive diversity, particularly in realtime location and workflow optimization solutions. Market competition is driven by technological innovation, AI based predictive analytics, cloud adoption, and strategic partnerships. While many vendors offer overlapping solutions, the top-tier players dominate key contracts and large hospital networks, making the market fragmented but leaning toward consolidation around major healthcare IT platforms.

Key Industry Developments

- On November 20, 2025, TeleTracking Technologies launched Decision IQ®, an AI-powered patient throughput solution designed to optimize capacity and improve system-wide patient flow. The platform is being piloted at University of Louisville Health, where it addresses capacity constraints by using predictive analytics, discharge simulation, and real-time operational insights. This marks a significant advancement in the Patient Throughput and Capacity Management market, enabling proactive decision-making, reduced bottlenecks, and improved care coordination across departments.

- On December 30, 2025, King Faisal Specialist Hospital & Research Centre (KFSHRC) in Riyadh reported major gains in emergency department and inpatient throughput, reducing median wait time for an inpatient bed from 13 plus hours in 2023 to ~3.2 hours in mid-2025. The improvement stemmed from a system-wide process redesigned by an AI-enabled Patient Flow & Capacity Command Centre that monitors real-time bottlenecks and drives proactive operational decisions. These measures expanded effective inpatient capacity, streamlined admissions and discharges, and strengthened accountability, marking a notable advancement in the Patient Throughput and Capacity Management market.

Companies Covered in Patient Throughput and Capacity Management Market

- Epic Systems Corporation

- STANLEY Healthcare

- McKesson Corporation

- CERNER CORPORATION

- TeleTracking Technologies, Inc.

- Awarepoint Corporation

- Allscripts

- Care Logistics LLC

- Central Logic

- Sonitor Technologies, Inc.

Frequently Asked Questions

The global Patient Throughput and Capacity Management Market is projected to be valued at US$ 1.7 Bn in 2026.

The Software segment is expected to account for approximately 61.5% of the Global Patient Throughput and Capacity Management Market by Component Type in 2026.

The market is expected to witness a CAGR of 10.8% from 2026 to 2033.

The Patient Throughput and Capacity Management market is driven by healthcare workforce shortages, increasing demand from aging populations and chronic diseases, and technological advancements like AI, predictive analytics, and real-time operational intelligence that optimize patient flow, reduce wait times, and improve resource utilization.

The Patient Throughput and Capacity Management market offers significant opportunities through AI and predictive analytics for admission forecasting, discharge optimization, and OR scheduling, as well as cloud-based, scalable deployment models that reduce costs and enable broader access, particularly in Asia-Pacific and Latin America.

Key players in the Patient Throughput and Capacity Management Market include TeleTracking Technologies, Epic Systems, Cerner (Oracle Health), McKesson, Allscripts, GE Healthcare, and Philips Healthcare.