- Medical Devices

- Medical Footwear Market

Medical Footwear Market Size, Share, Trends, Growth, Regional Forecast 2026 to 2033

Medical Footwear Market by Product (Medical Shoes & Boots, Medical Sandals, Others), End-user (Men, Women), Application (Diabetic Footwear, Arthritis Footwear, Buions & Hallux Valgus Footwear, Others), Sales Channel, and Regional Analysis 2026 - 2033

Medical Footwear Market Share and Trends Analysis

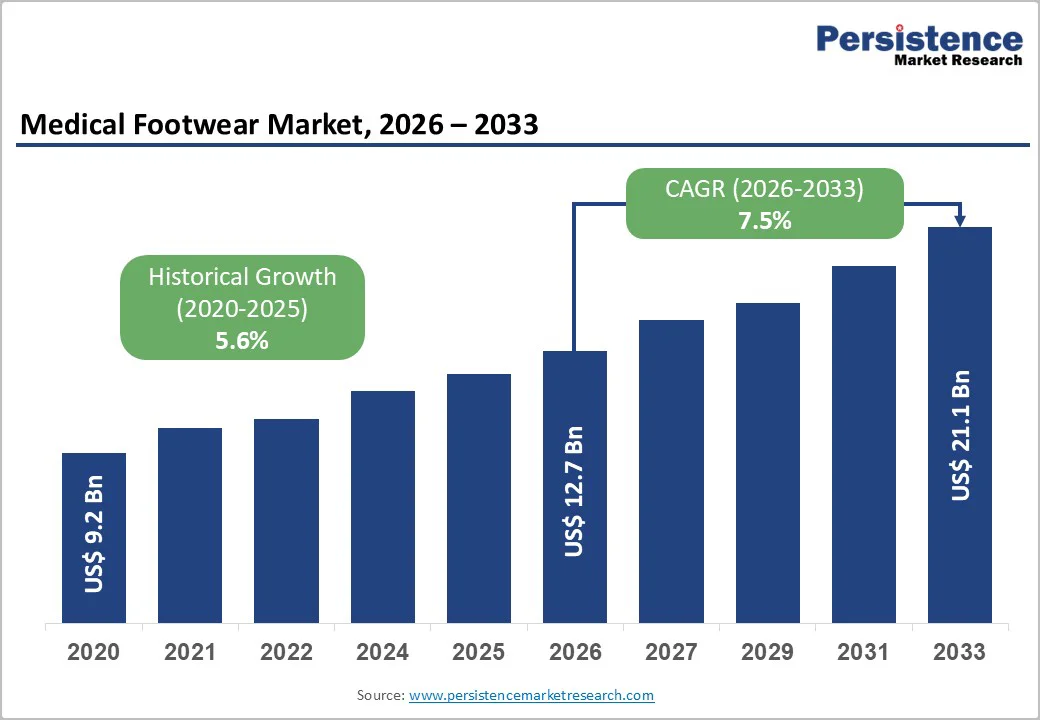

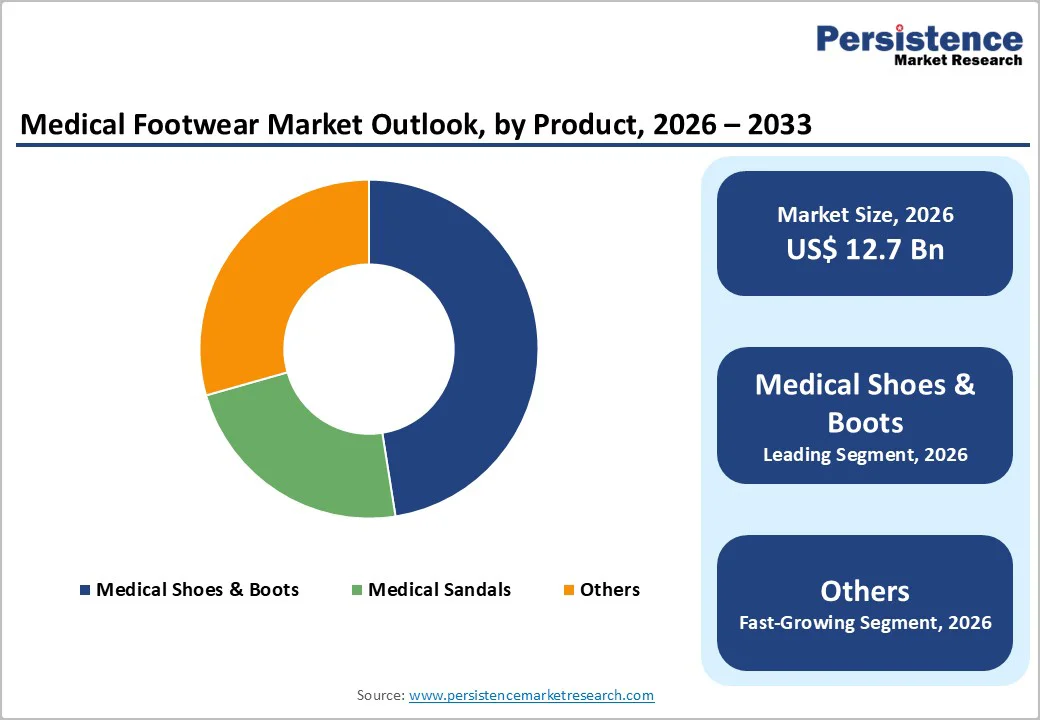

The global medical footwear market size is valued at US$12.7 billion in 2026 and is projected to reach US$21.1 billion by 2033, growing at a CAGR of 7.5% between 2026 and 2033.

This sustained expansion is primarily driven by accelerating diabetes prevalence affecting around 700 million individuals globally by 2045, aging population demographics (65+ cohort expanding 3.1% annually), and heightened clinical awareness of preventive foot care across developed healthcare systems.

Technological integration including smart insoles with pressure monitoring capabilities, 3D-printed customized orthotics, and bio-based antimicrobial materials enhance product efficacy and user compliance.

Key Industry Highlights:

- Product Segment Leadership: Medical shoes & boots command 48% market share while others (slippers, post-operative footwear) category represent fastest-growing category at 7.8% CAGR driven by affordability tiers and post-operative applications.

- End-User Dynamics: Male consumers lead with 58% market share while female segments expand at 7.6% CAGR reflecting rising workforce participation and pregnancy-related medical footwear demand in developing markets.

- Application Distribution: Diabetic footwear maintains 46% market share; miscellaneous applications (plantar fasciitis, general orthopedic support, etc.) category expand fastest at 8.0% CAGR capturing consumer-driven demand.

- Sales Channel Transformation: Specialty stores hold 41% market share while e-commerce platforms accelerate at 10.6% CAGR, indicating structural market shift toward digital distribution particularly in emerging markets.

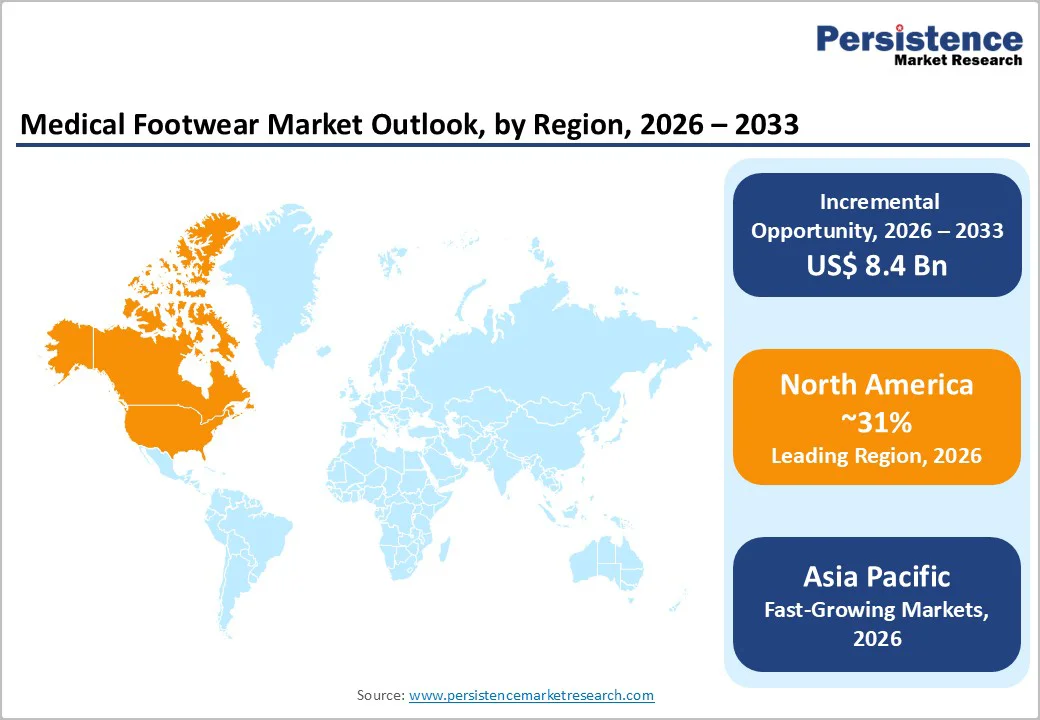

- Regional Growth Leaders: North America maintains 31% market share at 7.2% CAGR; Asia Pacific emerges fastest at 8% CAGR driven by India's diabetes population and China manufacturing advantages.

- Strategic Market Developments: Orthofeet smart boot launch, and Skechers diabetic footwear expansion (May 2025) signal mainstream brand expansion into medical footwear, potentially capturing ~8-12 Mn additional lifestyle-conscious consumers.

| Key Insights | Details |

|---|---|

| Medical Footwear Market Size (2026E) | US$ 12.7 billion |

| Market Value Forecast (2033F) | US$ 21.1 billion |

| Projected Growth CAGR (2026 - 2033) | 7.5% |

| Historical Market Growth (2020 - 2025) | 5.6% |

Market Dynamics Analysis

Drivers - Rise in Prevalence of Diabetes and Chronic Foot Pathologies

Global diabetes prevalence reached around 463 million adults in 2024 with projections accelerating to 700 million by 2045, representing 50% decade-on-decade growth according to the International Diabetes Federation.

Diabetic neuropathy affects approximately 50% of diabetes-diagnosed populations, creating corresponding demand for specialized preventive footwear. The CDC's National Diabetes Statistics Report (2023) documented 37.3 million Americans with diabetes, with ~90% experiencing some form of foot complication during disease progression.

Diabetic foot ulcers represent the leading non-traumatic lower limb amputation etiology globally, affecting around 30% of hospitalized diabetic patients. Medical-grade footwear reduces ulceration risk by 60-70% through pressure-offloading mechanisms and reinforced structural integrity compared to conventional footwear.

Beyond diabetes, arthritis prevalence increased to around 60Mn U.S. adults, with ~20-24% experiencing foot-specific symptoms requiring orthopedic support infrastructure. These escalating chronic disease burdens create institutional demand drivers encompassing clinical prevention protocols and patient compliance incentives.

Healthcare System Integration and Insurance Reimbursement Expansion

Medicare coverage for therapeutic diabetic shoes (established 1993) has evolved to encompass multi-insole customization with podiatrist-prescribed fitting protocols, expanding reimbursable product scope to US$200-350 per pair annually for eligible beneficiaries. In 2024, ~78% of Medicare Advantage plans incorporated diabetic footwear coverage, increasing from 54% in 2018, representing significant expansion over six years.

European Union regulatory harmonization (CE-marked medical device standardization across 27 member states) enabled seamless cross-border distribution and pan-European insurance recognition. The UK National Health Service (NHS) prescribing protocols designated therapeutic footwear as first-line intervention for Type 2 diabetics with neuropathic complications, generating institutional procurement volumes reaching around 2.4Mn units annually.

Private insurance penetration in Asia Pacific (specifically Singapore, Australia, and New Zealand) expanded coverage to 35Mn beneficiaries, previously accessing medical footwear through out-of-pocket channels. These systemic healthcare integration pathways create predictable demand streams independent of consumer discretionary spending, establishing stable revenue foundations for manufacturers aligned with clinical guideline requirements.

Market Restraints

High Production Costs and Customization Complexity

Custom orthotics manufacturing using hand-crafted components and individualized insole fitting requires 6-8 clinical hours per patient, creating substantial labor burdens even before material and overhead allocation. Specialized machinery for 3D scanning and printing adds significant fixed-cost barriers, while imported raw materials face notable shipping premiums and supply-chain exposure.

Smaller manufacturers lack the economies of scale enjoyed by multinational competitors, resulting in higher per-unit costs. Regulatory compliance obligations, including FDA and CE processes, impose recurring administrative and documentation demands that disproportionately strain emerging-market producers.

Additionally, increasing expectations for traceability, digital record management, and clinician-validated design standards further elevate operational pressures across the industry.

Regulatory Complexity and Clinical Evidence Requirements

FDA classification of medical footwear as Class II medical devices mandates 510(k) substantial equivalence demonstrations referencing predicate products, requiring 12-18-month approval timelines and significant development investment. The European Union Medical Device Regulation (MDR) introduced enhanced clinical documentation standards, post-market surveillance obligations, and periodic safety updates that impose recurring compliance costs.

Comparative clinical trials establishing efficacy versus conventional footwear require multisite cohorts of approximately 200-500 participants with 12-24-month follow-up periods and considerable research commitments.

Insurance reimbursement justification demands health-economic modeling demonstrating acceptable cost-effectiveness thresholds, limiting addressable markets to patients with more severe pathologies. These regulatory burdens increasingly concentrate market share among established multinationals with robust regulatory infrastructure.

Opportunity- Smart Footwear and Health Monitoring Integration

Connected medical footwear incorporating biometric sensors represents a substantial addressable market by 2033, while currently capturing only 3-5% of total medical footwear units. Wearable technology convergence enabling seamless smartphone integration via Bluetooth, creates recurring software subscription revenue streams.

Remote patient monitoring capabilities enable telemedicine-facilitated clinical oversight reducing in-office consultation frequencies by 40-50%, creating payer-attractive cost reduction narratives. Integration with enterprise wellness programs and occupational health services creates B2B2C distribution channels. FDA guidance supporting software-enabled medical device ecosystems accelerates regulatory approval timelines for sensor-integrated footwear platforms.

Preventive Care Reimbursement and Corporate Wellness Expansion

Corporate wellness spending is rising significantly, creating strong opportunities for footwear-based ergonomic and preventive health programs to gain deeper market penetration. Employee populations with occupational foot strain (manufacturing, retail, and healthcare workers totaling 450M individuals globally) represent addressable market for workplace-subsidized medical footwear programs.

Insurance carriers recognizing around US$2,000-4,500 annual cost reductions per prevented diabetic foot ulcer event are expanding wellness program coverage to include preventive footwear. Self-insured employer populations are unilaterally funding medical footwear initiatives without regulatory approval requirements.

Occupational safety and health administration (OSHA) guidance emphasizing ergonomic footwear in hazardous-duty environments creates institutional procurement pathways for specialized industrial medical footwear addressing prominent market opportunity.

Category-wise Analysis

Product Type Insights

Medical shoes and boots command 48% market share, across clinical applications. Structured shoe architecture provides ankle stability, arch support, and pressure-offloading insole integration unattainable through sandal or slipper form factors. Diabetic shoe designs incorporating rocker-bottom soles, reinforced toe boxes, and seamless interior construction reduce ulceration risk by 60-70% compared to conventional footwear.

Premium medical shoes priced around US$180-350 achieve 38-42% gross margins, substantially exceeding slipper segment economics. Specialized applications including post-operative recovery shoes and arthritis-specific designs with reduced flexion requirements drive category diversification.

The Others category encompassing therapeutic slippers, post-operative recovery shoes, and specialized flip-flops expands at 7.8% CAGR, capitalizing on consumer preference for accessible, affordable medical footwear options.

Post-operative flip-flops designed for immediate post-surgical use (following bunion, flat-foot corrections) create consumable replacement cycles. Antimicrobial-treated slippers for hospitalized patients address healthcare-associated infection prevention, generating institutional B2B procurement channels.

End-user Insights

Male consumers capture 58% market share, reflecting epidemiological patterns of higher diabetes prevalence among male populations (particularly ages 55-75). Occupational foot strain drivers (manufacturing, construction, commercial transportation sectors) concentrate within male-dominated employment categories, amplifying medical footwear demand.

Male consumers demonstrate higher purchasing power in developed markets (North America, Western Europe) where income differentials favor premium product selection. Professional footwear requirements necessitate aesthetic design integration balancing clinical functionality with workplace appearance standards, driving category premium pricing acceptance.

Female end-user segments expand at 7.6% CAGR, driven by increasing female workforce participation in developed economies and rising female-specific chronic disease incidence.

Gestational diabetes affecting 14-18% of pregnancies creates post-partum medical footwear demand among reproductive-age cohorts. Female-specific design requirements historically underserved by male-dominated product portfolios create design differentiation opportunities. Obstetric complications including gestational arthritis and postpartum edema create expanded therapeutic footwear applications.

Application Insights

Diabetic footwear applications command 46% market share, reflecting diabetes as primary clinical driver. Preventive footwear reducing ulceration risk and amputation incidence creates clinical evidence foundation supporting insurance reimbursement.

Medicare-covered diabetic shoes generating institutional procurement volumes of around 7-8 Mn pairs annually establish stable demand foundation. Specialized features including moisture-wicking materials reducing fungal infection risk, seamless construction minimizing blister formation, and accommodative depths addressing diabetic edema create clinical differentiation versus conventional footwear.

Miscellaneous applications including plantar fasciitis management, Achilles tendonitis recovery, post-operative wound care, and general orthopedic support expand at 8.0% CAGR, representing fastest category growth.

Plantar fasciitis affecting around 10% of adult populations (particularly ages 40-60) creates consumer-driven demand through over-the-counter direct purchasing pathways independent of clinical prescribing. Post-operative footwear applications generate recurring replacement cycles (6-month intervals) through surgical procedure volume growth.

Sales Channel Insights

Specialty retail channels including dedicated medical footwear boutiques, orthopedic shoe stores, and podiatry clinics command 41% market share. Clinical consultation capabilities within specialty environments enable customer education on foot condition management and footwear customization requirements.

Specialty retailers maintain ~45-55% gross margins through premium positioning and direct customer relationships, substantially exceeding e-commerce channel economics. Healthcare provider partnerships (podiatry clinics, orthopedic centers) drive in-store traffic through clinical referral networks. Geographic concentration in urban markets and regional medical centers limits accessibility for rural and emerging market populations.

E-commerce distribution channels expand at 10.6% CAGR, capturing market share from traditional specialty retail through cost advantages and geographic accessibility. Amazon, Alibaba, and region-specific platforms (Flipkart in India, Lazada in Southeast Asia) provide unlimited product visibility and consumer comparison capabilities.

Virtual try-on technologies and detailed sizing guides reduce product return rates to 12-18% from traditional retail baseline. E-commerce channel CAGR substantially exceeds specialty retail growth, indicating structural market shift toward digital distribution.

Regional Market Insights

North America Medical Footwear Market Share and Insights

North America commands 31% of the global market with a strong growth rate, driven primarily by the United States, where approximately 37.3 million diagnosed diabetics, extensive Medicare coverage for therapeutic footwear, and high private insurance penetration collectively reinforce regional dominance.

Medicare reimbursement framework established in 1993 generates institutional procurement of around 7 to 8 Mn pairs annually at standardized reimbursement levels of US$200-350 per pair.

The Canadian market demonstrates similar healthcare system integration with provincial health authority coverage expanding diabetic footwear access.

Regional competitive intensity concentrates among 40-50 established manufacturers including Dr. Comfort, Orthofeet, New Balance, and Propet maintaining distribution networks across specialty retail chains and healthcare facilities. Insurance reimbursement providing predictable payment streams establish North America as premium market commanding disproportionate manufacturing focus.

FDA regulatory framework establishing predictable approval pathways and standardized testing protocols creates competitive neutrality across manufacturers meeting predicate device requirements. Podiatry professional integration within clinical practice communities drives clinical adoption of evidence-based footwear recommendations.

Direct-to-consumer marketing through telehealth platforms and digital patient engagement channels increasingly bypasses traditional specialty retail infrastructure. Market consolidation trends including specialty retail chain consolidations and manufacturer acquisitions by multinational conglomerates reshape competitive dynamics.

Europe Medical Footwear Market Share and Insights

Europe maintains 27% global market share growing at 7.1% CAGR. Germany, United Kingdom, France, and Spain collectively represent 60-65% of regional market value, driven by aging populations (65+ cohort representing 21% of populations versus 17% U.S. average) and established healthcare infrastructure.

German market emphasis on engineering excellence and clinical evidence standards maintains premium product positioning. UK market demonstrates NHS integration of diabetic footwear within clinical pathways, generating institutional procurement of around 2.4Mn pairs annually.

French market characterization by strong cooperative and mutualist insurance structures expands coverage accessibility. Spanish market leadership through regional manufacturers (Piedro, specialized orthopedic producers) reflects regional competitive dynamics.

EU Medical Device Regulation (MDR) harmonization across 27 member states enables pan-European distribution without duplicative regulatory approvals. Reimbursement frameworks demonstrate heterogeneity with German statutory health insurance providing comprehensive coverage versus restrictive UK NHS protocols limiting uptake to severe pathology populations.

Regional insurance system variations create complex market access requirements for multinational manufacturers. Investment capital concentration supports emerging European audio brands including Scandinavian design-focused producers emphasizing aesthetic integration with clinical functionality.

Asia Pacific Medical Footwear Market Share and Insights

Asia Pacific represents fastest-growing region with 8% CAGR, currently capturing approximately 25-29% global market share and accelerating toward 30-33% by 2033.

China's ~130Mn diabetic-diagnosed population represents single largest addressable market globally, with government health initiatives creating institutional procurement pathways. India's ~95M diabetes population and 56% treatment gap (population lacking access to adequate footwear solutions) creates significant incremental opportunity through affordable product tier expansion.

Japan's aging population (29% age 65+) and advanced healthcare infrastructure drive premium product demand. Manufacturing cost advantages enable region-specific pricing strategies capturing price-sensitive consumer segments. Rapid e-commerce penetration across urban centers fundamentally reshapes distribution economics independent of traditional specialty retail infrastructure.

Asia Pacific manufacturing ecosystem including established footwear production capacity in Vietnam, Indonesia, and India enables cost-optimized supply chains capturing global volume production. Local brand proliferation (Dr. Ortho, Diabetic India, regional manufacturers) captures prominent regional market share through region-specific marketing and distribution network penetration.

Government initiatives supporting medical device manufacturing accelerate regional production capacity expansion. Cross-border e-commerce integration enables Chinese brand distribution across Southeast Asian markets, intensifying competitive dynamics.

Competitive Landscape

The global medical footwear market shows moderate consolidation, with top players holding around 32-35% and over 280 companies sharing the rest. New Balance, Dr. Comfort, and Orthofeet lead premium segments, while SAS and Mephisto add notable share. Chinese manufacturers expand rapidly via aggressive pricing. Premium markets remain concentrated, whereas budget categories and Asia Pacific markets are heavily fragmented across global consumer groups.

Strategic Developments

- In February 2025, Orthofeet launched its smart IoT-enabled boot featuring temperature and pressure sensors with real-time alerts to help prevent diabetic foot ulcers. This early move into connected medical footwear strengthens its subscription-based revenue model and supports higher reimbursement potential with an anticipated ASP uplift.

- In May 2025, 3G Capital acquired Skechers and introduced a diabetic footwear line aimed at mass-market accessibility. Leveraging Skechers’ global retail presence and low-cost manufacturing in Vietnam and China, the strategy enables competitive pricing and accelerates the brand’s entry into high-volume medical footwear segments.

Business Strategies

Market leaders rely on premium clinical differentiation supported by evidence-based design, podiatrist endorsements, and reimbursement alignment. Orthofeet and Dr. Comfort target pathology-specific needs, while New Balance leverages orthopedic heritage for pricing power.

Emerging brands use cost leadership and e-commerce. Athletic brands blend clinical and lifestyle design. Key themes include customization technology, healthcare partnerships, market expansion, and connected-product models for growth.

Companies Covered in Medical Footwear Market

- New Balance Athletics, Inc.

- Dr. Comfort LLC

- Orthofeet, Inc.

- SAS Shoes, Inc.

- Mephisto (Groupe Mephisto)

- Propet USA

- Vionic (Caleres subsidiary)

- Drew Shoe Corporation

- Apex Foot Health Industries

- DARCO International

- Duna

- Chaneco

- Kizik Technologies

- Sole

- Skechers USA, Inc.

Frequently Asked Questions

The global medical footwear market is valued at US$12.7354 Billion in 2026 and is projected to reach US$21.0917 Billion by 2033.

The medical footwear market is propelled by rising global diabetes prevalence-currently affecting over 460 million adults and projected to approach 700 million by 2045, alongside expanding healthcare reimbursement integration and advancing customization technologies.

The medical footwear market is projected to grow at a 7.47% CAGR between 2026 - 2033.

Primary market opportunities include expanding into emerging geographies, integrating smart footwear with health-monitoring capabilities, and broadening reimbursement support for preventive care solutions.

Market leadership is dominated by New Balance, Dr. Comfort, Orthofeet, SAS Shoes, and Mephisto, while emerging competitors such as Nike, Skechers, and regional manufacturers are gaining substantial share through cost-leadership strategies and strong e-commerce penetration across Asia Pacific markets.