- Sensors & Controls

- Biometric Sensors Market

Biometric Sensors Market Size, Share, and Growth Forecast 2026 - 2033

Biometric Sensors Market by sensor type (Optical sensors, Electric field sensors, Thermal sensors, Capacitive sensors, Ultrasound sensors, Image sensors, Others), Scan Type (Finger scan, Facial scan, Hand scan, Voice scan, Vein scan, Iris scan), Application (Public security, Payment & Fintech, Access control, Office & Notebook, Others), End-user (Government & Defence, Educational hubs, Healthcare & Life sciences Others), by regional analysis, 2026 - 2033

Biometric Sensors Market Size and Trend Analysis

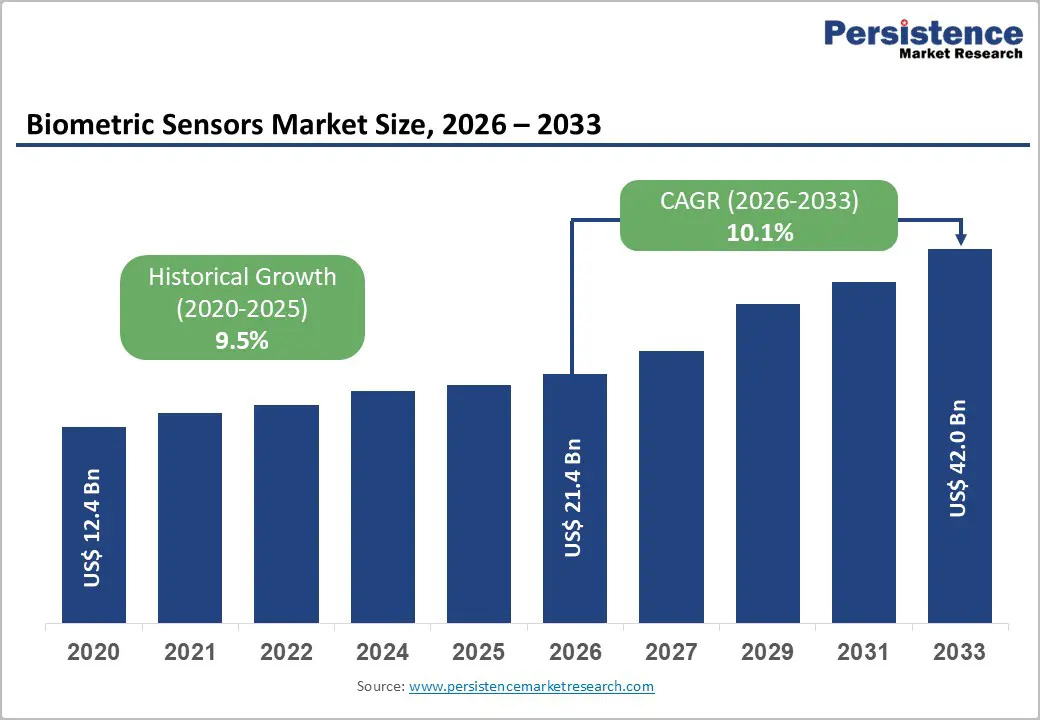

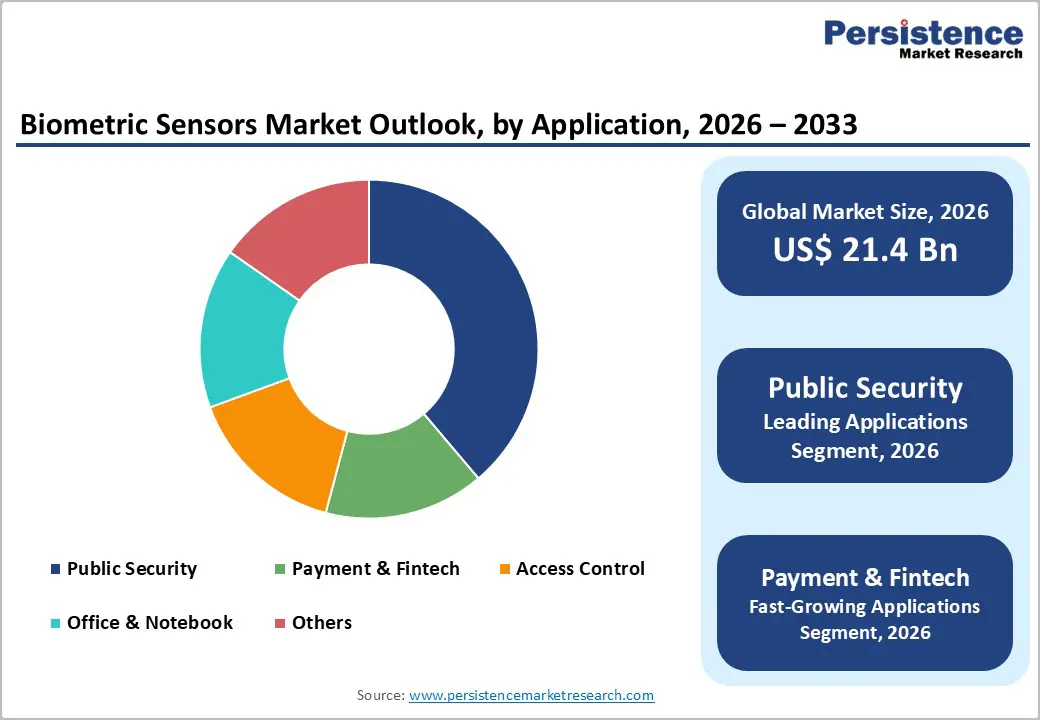

The global biometric sensors market size is likely to be valued at US$ 21.4 billion in 2026 and projected to reach US$ 42.0 billion by 2033, growing at a CAGR of 10.1% between 2026 and 2033.

The industry is experiencing transformative growth driven by escalating security concerns, widespread government initiatives promoting national identification systems, and the integration of advanced authentication technologies into consumer electronics.

Organizations and governments are increasingly prioritizing identity-verification solutions as a result of a sharp rise in data breaches. According to the 2023 Annual Data Breach Report by the Identity Theft Resource Center (ITRC), reported U.S. data compromises surged to 3,205 in 2023 from 1,801 in 2022.

Key Industry Highlights:

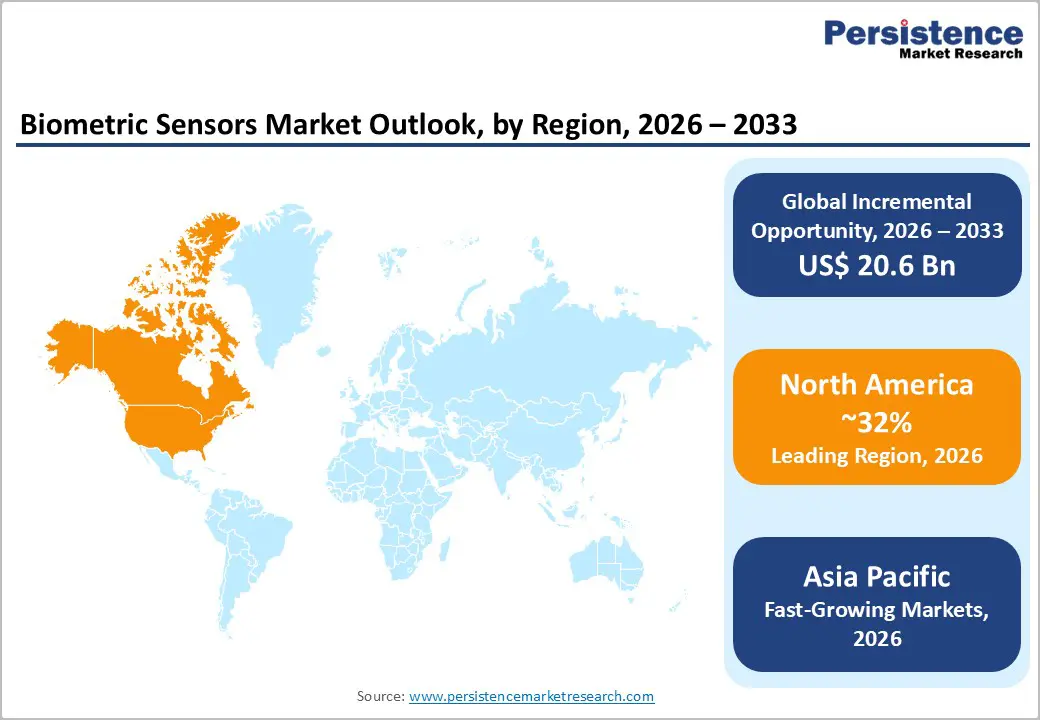

- Leading Region: North America leads the biometric sensors market in 2025, with a 32% share, driven by advanced infrastructure, strong regulatory frameworks, broad adoption across financial and consumer electronics, and significant government security investments.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expanding at a 22.43% CAGR driven by large-scale national ID programs, extensive surveillance networks, smart city initiatives, and rapid smartphone-enabled biometric integration.

- Dominant Segment: Facial scanning is the dominant and fastest-growing biometric modality, propelled by widespread smartphone use, security deployments, travel screening systems, retail verification, and rising adoption of thermal facial recognition.

- Fastest Growing Segment: Payment & Fintech is the fastest-growing application segment, as mobile authentication, digital KYC, biometric ATMs, and wallet integrations deliver seamless yet secure financial transactions.

- Key Opportunity: Government initiatives and regulatory mandates create major growth opportunities, with national ID expansions, border control modernization, and law enforcement integration driving demand for scalable biometric authentication systems.

| Key Insights | Details |

|---|---|

| Biometric Sensors Market Size (2026E) | US$ 21.4 billion |

| Market Value Forecast (2033F) | US$ 42.0 billion |

| Projected Growth CAGR (2026 - 2033) | 10.1% |

| Historical Market Growth (2020 - 2025) | 9.5% |

Market Dynamics

Drivers - Rising Security Threats and Identity Theft Concerns

The growing incidence of identity theft and cybersecurity breaches has become a primary catalyst for the adoption of biometric sensors across enterprises and government agencies worldwide.

With 13.5% of all digital account openings worldwide suspected to involve fraudulent activity, organizations are actively transitioning from traditional password-based authentication to biometric solutions that leverage unique physiological characteristics. 54% of customers across 18 nations reported experiencing multiple fraud attempts between September and December 2023, highlighting the urgency of implementing robust authentication mechanisms.

Biometric sensors provide multi-factor authentication capabilities that significantly reduce unauthorized access risks, offering organizations a non-transferable and auditable identity verification method that addresses critical security, authentication, non-repudiation, and data integrity requirements simultaneously.

Government Initiatives and Regulatory Mandates

Government-led biometric identification programs have emerged as transformative drivers of market expansion, particularly across developing economies and regions prioritizing national security infrastructure.

India’s Aadhaar initiative has enrolled over 1.3 billion citizens, creating the world’s largest biometric database managed by the Unique Identification Authority of India, thereby establishing standardized protocols for biometric authentication in government services and e-governance projects.

The European Union’s Entry/Exit System (EES), which commenced operational deployment on October 12, 2025, mandates biometric registration, including fingerprints and facial images for non-EU travelers, with full implementation expected by April 10, 2026.

These large-scale government programs necessitate reliable, scalable biometric sensor technologies, driving procurement of fingerprint scanners, facial recognition cameras, and iris-scanning systems for border control, national identification, and public security applications.

Restraints - Privacy Concerns and Stringent Data Protection Regulations

The processing and storage of biometric data present significant privacy challenges, particularly in regions with strict data protection frameworks such as the European Union. The General Data Protection Regulation (GDPR) classifies biometric data as a special category of personal data under Article 9, restricting processing activities to specifically authorized use cases with explicit informed consent from data subjects.

Organizations implementing biometric systems must navigate complex compliance requirements, including encrypted data storage, access controls, regular security audits, and transparent data usage policies.

These regulatory constraints increase implementation costs and operational complexity, particularly for small and medium-sized enterprises lacking specialized compliance infrastructure, thereby limiting market penetration in heavily regulated jurisdictions and slowing adoption timelines for new applications.

Vulnerability to Spoofing Attacks and Presentation Attack Exploitation

Biometric sensor systems remain susceptible to sophisticated presentation attacks that use artificial replicas, including fabricated fingerprints made from silicone or gelatin, three-dimensional-printed facial masks, and high-resolution video recordings.

Research indicates that more than 80% of tested fingerprint scanners can be compromised by spoofed fingerprints made from materials such as gelatin or silicone. That biometric spoofing attacks have increased by 50% since 2022.

The development and proliferation of advanced attack methods, including deepfakes that employ artificial intelligence-generated facial representations, necessitate continuous technological advancement in liveness detection algorithms, anti-spoofing measures, and multi-modal biometric fusion approaches.

Organizations hesitant to deploy biometric sensors due to historical security vulnerabilities represent a significant market restraint, particularly in high-security applications requiring exceptional accuracy and fraud-resistance standards.

Opportunity - Integration of Artificial Intelligence and Machine Learning in Biometric Authentication

The convergence of artificial intelligence and biometric sensor technologies presents substantial growth opportunities through enhanced accuracy, adaptive learning, and advanced threat detection.

AI-based multimodal systems integrating facial recognition, fingerprint recognition, and voice recognition have demonstrated an 80% reduction in error rate compared to single-modality solutions, making them increasingly attractive for high-security financial and healthcare applications.

Machine learning algorithms enable continuous system refinement through pattern recognition, behavioral analysis, and demographic diversity adaptation, improving performance across culturally diverse user populations while reducing false acceptance and false rejection rates.

Financial institutions, healthcare providers, and government agencies are investing extensively in AI-powered biometric platforms supporting real-time decision-making, predictive analytics, and sophisticated presentation attack detection, creating substantial commercial opportunities for technology vendors offering cloud-based biometric-as-a-service platforms with advanced algorithmic capabilities.

Expansion into Emerging Technologies and Adjacent Markets

The proliferation of biometric integration across emerging application domains, including automotive cabin monitoring, Internet of Things devices, smart city infrastructure, and wearable electronics, represents a significant growth frontier.

Rheinmetall Dermalog and Infineon launched biometric tools specifically for driver monitoring in 2024, while automotive manufacturers increasingly embed iris and facial recognition systems for personalized cabin features and secure vehicle access.

Integrated Biometrics released the smallest multimodal biometric device in November 2024, demonstrating market momentum toward miniaturized sensors compatible with diverse form factors and industrial applications. Healthcare sector adoption is accelerating, driven by patient identification requirements, medical record security, and contactless verification in clinical environments.

These expanding use cases create substantial revenue opportunities for biometric sensor manufacturers, software developers, and systems integrators operating across consumer electronics, enterprise infrastructure, and government modernization initiatives.

Category-wise Analysis

Sensor Type Insights

Optical sensors remain the leading technology in the biometric sensors market, capturing an estimated 52.8% share in 2025 due to their widespread adoption in smartphones, laptops, and commercial access control systems. Their dominance is supported by high-resolution imaging, cost-efficient production, and seamless integration into compact consumer electronics.

Optical fingerprint sensors also benefit from mature supply chains and proven reliability, making them the preferred choice for large-scale deployments in both consumer and enterprise environments. Their scalability, durability, and ability to support high-volume authentication workloads continue to reinforce their position as the backbone of mainstream biometric identification.

Scan Type Insights

Facial scan technology is projected to register the fastest growth among biometric modalities, driven by rapid advancements in computer vision and 3D sensing. Its non-contact verification process, coupled with high accuracy in diverse lighting and environmental conditions, has accelerated adoption across smartphones, law enforcement systems, and airport passenger screening programs.

Facial recognition’s ability to authenticate users seamlessly without physical interaction positions it as a core technology for smart city surveillance, retail age verification, and public security deployments. Its expanding use in mobile applications and cloud-based identity platforms continues to solidify facial scan as the most dynamic modality in the market.

Application Insights

Payment & Fintech applications are experiencing the fastest growth in the biometric sensors market as financial platforms increasingly integrate fingerprint and facial authentication for secure digital transactions. Mobile banking, e-commerce, and digital wallet ecosystems rely on biometric verification for KYC processing, fraud mitigation, and frictionless user approval flows.

Markets such as India are accelerating this shift by enabling biometric-approved UPI payments, reducing authentication time while maintaining regulatory compliance. With biometric banking adoption exceeding 85% in select European countries, fintech providers are scaling biometric-enabled solutions to enhance trust, strengthen cybersecurity, and support the transition toward fully digital financial ecosystems.

End-user Insights

Government & Defence remains the dominant end-user segment, driven by national ID programs, border control modernization, and law enforcement applications requiring high-precision identity verification across large populations. Governments deploy multimodal biometrics, particularly facial and iris recognition, for criminal investigations, traveler screening, citizen enrollment, and public safety monitoring.

Facial recognition systems implemented across more than 20 U.S. airports illustrate the scale of adoption, supporting faster processing for millions of passengers annually. As digital identity frameworks and security infrastructure expand globally, government agencies continue investing in scalable biometric platforms to strengthen national security, streamline citizen services, and enhance cross-border identity management systems.

Regional Insights

North America Biometric Sensors Market Trends

North America remains the leading market for biometric sensors, accounting for roughly 32% of global share in 2023, supported by its advanced digital infrastructure, heavy R&D spending, and strong regulatory emphasis on data security.

The United States drives regional adoption through extensive government programs, including the deployment of facial recognition across more than 20 airports and the integration of biometric verification in federal systems such as the FBI’s Next Generation Identification platform. State-level privacy regulations-most notably Illinois’ BIPA, along with laws in Texas and Washington-continue shaping product design and compliance standards for biometric vendors.

The region’s mature fintech ecosystem further accelerates adoption, with biometric-enabled mobile banking and payment solutions becoming standard features in consumer devices, supported by innovations such as Qualcomm’s 3D Sonic Gen 2 fingerprint sensors.

Healthcare adoption is expanding rapidly as providers implement biometric systems for patient identification and medical record security, positioning North America as a sustained growth market for advanced, high-assurance authentication technologies.

Europe Biometric Sensors Market Trends

Europe is witnessing strong momentum in biometric sensor adoption, driven by technological modernization, stringent data protection regulations, and coordinated EU-level security initiatives. The upcoming implementation of the European Entry/Exit System (EES)-operational between October 2025 and April 2026-marks a major shift for regional border management by mandating fingerprint and facial biometrics for all non-EU travelers across 29 Schengen states.

Countries such as Germany, France, the United Kingdom, and Spain are accelerating deployment across financial services, digital identity programs, and public security infrastructures. Biometric payments grew by 45% in Europe during 2023, reflecting rising consumer preference for seamless and secure authentication.

However, regulatory frameworks such as GDPR, Article 9 restrictions on sensitive data, and the forthcoming EU AI Act obligations introduce heightened compliance requirements, particularly for high-risk AI facial recognition systems. As a result, Europe increasingly favors privacy-centric biometric solutions emphasizing ethical design, data minimization, and transparent algorithmic governance, creating opportunities for compliance-driven technology providers.

Asia Pacific Biometric Sensors Trends

Asia Pacific is the fastest-growing region in the biometric sensors market, projected to grow at a 12.8% CAGR from 2026 to 2033, driven by large-scale national identification programs, rapid industrial modernization, and widespread smartphone adoption.

China leads regional deployment, supported by an extensive biometric surveillance network exceeding one billion facial recognition cameras and smart city ecosystems integrating biometrics across policing, retail, and transportation.

India’s Aadhaar program, with over 1.3 billion enrollments, anchors the region’s digital identity infrastructure and drives biometric adoption in government services, financial inclusion initiatives, and public welfare delivery. Japan continues to advance biometric integration in smart transportation and banking systems, while South Korea accelerates adoption across defense and cashless payment environments.

The region’s expanding consumer base, growing fintech sector, and strong manufacturing capabilities create significant opportunities for biometric sensor suppliers. Government-backed digital transformation programs further reinforce Asia Pacific’s position as the most dynamic and scalable market for next-generation biometric technologies.

Competitive Landscape

The global biometric sensors market features a moderately concentrated structure, with a small group of established technology leaders holding substantial share through proprietary sensor innovations, integrated biometric platforms, and strong global distribution.

Competition is shaped by continuous investment in R&D, development of multimodal authentication systems, and expansion into cloud-based identity verification ecosystems. Market leaders increasingly focus on acquiring niche technology developers, enhancing AI-driven sensing capabilities, and strengthening compliance with emerging data protection regulations.

While specialized vendors are gaining traction in areas such as iris, vein, and thermal recognition, large integrated providers retain dominance through end-to-end product portfolios and long-term ecosystem commitments.

The competitive landscape is further defined by advances in presentation attack detection, algorithmic accuracy, and privacy-preserving design, which have become critical differentiators in regulated sectors including government, financial services, healthcare, and enterprise security. As demand for high-assurance digital identity solutions accelerates, competition is expected to intensify around scalability, interoperability, and ethical biometric deployment.

Key Market Developments:

- October, 2025: EU’s Entry/Exit System (EES) commences operational deployment, capturing fingerprint and facial biometric data from non-EU travelers across Schengen participating countries, establishing standardized protocols for border security and digital identity verification with full implementation expected by April 2026.

- January 2025: Fingerprint Cards licenses its iris recognition technology to Smart Eye for up to SEK 50 million, enabling joint development of advanced automotive and enterprise biometric solutions integrating identity authentication with driver-monitoring systems.

Companies Covered in Biometric Sensors Market

- IDEMIA

- 3M

- BioID

- HID Global Corporation

- Fujitsu

- IDEX Biometrics ASA

- IrisGuard Ltd

- NEC Corporation

- NEXT Biometrics

- Synaptics Incorporated

- Thales

- Fulcrum Biometrics LLC

- Precise Biometrics AB

- Qualcomm Technologies

- Fingerprint Cards AB

- Goodix Technology

- Suprema Inc.

- Aware Inc.

- Invixium

Frequently Asked Questions

The biometric sensors market will grow from US$ 21.4 billion in 2026 to US$ 42.0 billion by 2033 at a 10.1% CAGR, driven by security needs and rising biometric integration across major industries.

Key drivers include rising identity fraud, increasing data breaches, large-scale government ID programs, and high biometric adoption in smartphones and BFSI services.

Facial scan sensors are the fastest-growing segment, fueled by smartphone usage, law enforcement, airport screening, retail verification, and expanding contactless authentication.

North America leads the market with the largest share due to strong infrastructure, privacy regulations, government deployments, and high enterprise and consumer adoption.

Payments and fintech authentication offer the top opportunity, supported by digital KYC, biometric ATM access, mobile wallet growth, and rising contactless financial transactions.

Major leaders include Thales, Synaptics, Fingerprint Cards, NEC, and IDEMIA, supported by strong portfolios, large patent bases, and advanced sensor innovation.