- Medical Devices

- Advanced Computed Tomography Scanners Market

Advanced Computed Tomography Scanners Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Advanced Computed Tomography Scanners Market by Product Type (Cone Beam CT Scanners, Spectral Imaging Based CT Scanners, Low Dose CT Scanners, Portable CT Scanners), by End-user (Hospitals, Ambulatory Surgical Centers, Diagnostics Centers, Others), and Regional Analysis from 2026 to 2033

Advacned Computed Tomography Scanners Market Share and Trends Analysis

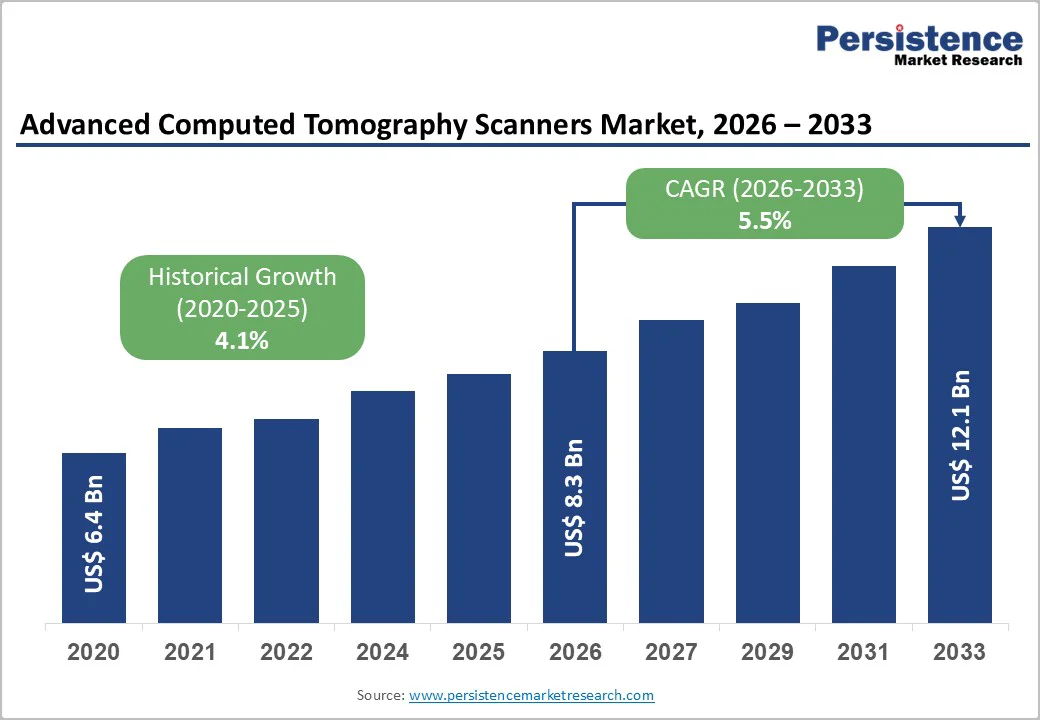

The global advanced computed tomography scanners market size is estimated to grow from US$8.3 billion in 2026 to US$12.1 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033.

As healthcare providers have switched to high-resolution, low-dose, and AI-enhanced imaging systems for faster and more accurate diagnosis, the need for advanced imaging has doubled.

The demand is driven by rising cancer, cardiovascular, and trauma cases, as well as the expansion of advanced imaging services in hospitals and diagnostic centers. Newer technologies such as spectral CT, photon-counting detectors, and portable CT units are improving image quality, reducing radiation exposure, and expanding use in emergency and critical care settings.

Key Industry Highlights:

- Spectral and photon-counting CT technologies are gaining momentum due to superior tissue characterization, reduced noise, and enhanced lesion detection.

- AI integration is transforming CT workflows by enabling automated image reconstruction, organ segmentation, and real-time anomaly detection. AI-driven optimization reduces scan times, minimizes artifacts, and supports faster reporting.

- Portable and mobile CT scanners are seeing increased adoption in ICUs, operating rooms, and emergency departments.

- Major imaging companies are launching next-generation CT platforms featuring improved detector technology, smart workflow automation, and expanded clinical applications.

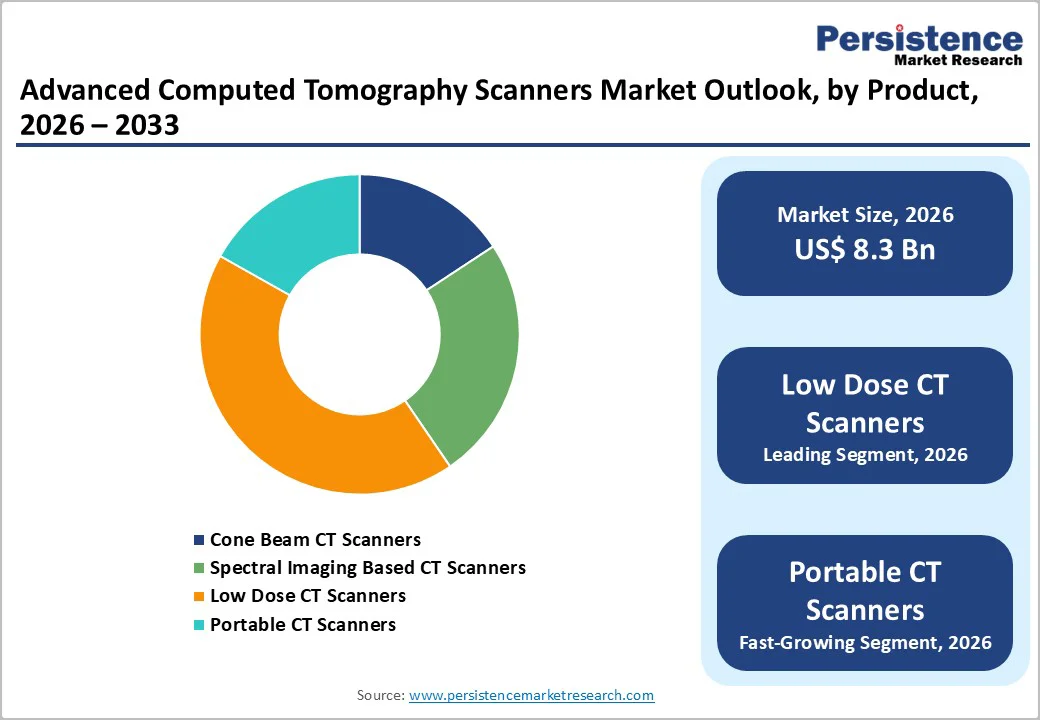

- Leading Product Type: Low-dose CT scanners are widely used across hospitals and diagnostic centers for routine imaging, cancer screening, trauma evaluation, and cardiology.

| Key Insights | Details |

|---|---|

| Advanced Computed Tomography Scanners Market Size (2026E) | US$8.3 Bn |

| Market Value Forecast (2033F) | US$12.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.1% |

Market Dynamics

Driver - Growth of Hybrid Imaging in Oncology

The growth of hybrid imaging in oncology is becoming a major driver for advanced CT adoption, as cancer centers increasingly rely on integrated CT-PET and CT-SPECT platforms for comprehensive tumor assessment. These hybrid systems combine metabolic and anatomical information in a single scan, enabling highly precise staging, early detection of micro-lesions, and more accurate treatment-response monitoring.

Advanced CT modules within hybrid systems provide superior spatial resolution, faster acquisition, and low-dose imaging, supporting repeated follow-ups throughout the patient’s treatment journey.

As oncology care shifts toward personalized and targeted therapies, clinicians require deeper insights into tumor behavior and treatment efficacy, pushing hospitals to upgrade to next-generation hybrid-ready CT platforms that enhance diagnostic confidence and improve patient outcomes.

Restraints - Radiation Exposure Concerns

Despite significant advancements in low-dose CT technology, concerns about cumulative radiation exposure remain a major restraint on the adoption of advanced CT scanners. Repeated imaging, particularly for patients undergoing chronic disease monitoring, cancer follow-ups, or multi-phase studies, can lead to increased lifetime radiation doses.

Pediatric and geriatric populations are especially vulnerable due to heightened sensitivity to ionizing radiation. These safety concerns prompt stricter clinical guidelines, limit the frequency of scans, and influence physicians’ imaging choices.

As a result, hospitals and diagnostic centers may hesitate to fully adopt or invest in high-end multi-slice or spectral CT systems, despite their diagnostic advantages. Patient awareness and regulatory emphasis on minimizing radiation further reinforce this restraint, affecting market growth globally.

Opportunity - Portable and Point-of-Care CT

The Portable and Point-of-Care CT segment is gaining significant traction as hospitals and healthcare providers prioritize rapid, bedside imaging solutions. Mobile CT scanners enable clinicians to perform high-quality scans directly in ICUs, emergency rooms, and operating theaters, eliminating the need to transport critically ill or immobile patients.

This not only reduces the risk of complications during patient transfer but also accelerates diagnosis and treatment decisions. The convenience and flexibility of portable CT systems make them particularly valuable for trauma care centers, neurology, and intra-operative imaging, while also creating growth opportunities in field hospitals and remote or underserved healthcare settings.

Category-wise Analysis

By Product Type, the low-dose CT scanners segment leads the Market.

Low-dose CT scanners hold the highest market share because they are widely used across hospitals, diagnostic imaging centers, and government-supported screening programs. Their ability to deliver high-quality images while minimizing radiation exposure makes them suitable for routine diagnostics, lung cancer screening, cardiac assessments, and trauma evaluation.

Unlike spectral CT, CBCT, or portable CT scanners, which serve niche or specialized applications, low-dose CT systems address a broad spectrum of clinical needs. Their relatively lower cost, large installed base, and regulatory support for low-radiation imaging further contribute to widespread adoption, making them the dominant segment in the advanced CT scanner market.

By End-user, the Hospitals Segment Leads the Market

Hospitals account for the largest market share in the advanced CT scanners market because they serve as primary hubs for multi-specialty healthcare and have high patient volumes. They require advanced imaging systems for a wide range of applications, including oncology, cardiology, neurology, trauma, and emergency care.

Hospitals typically have the necessary infrastructure, trained radiologists, and financial resources to invest in high-end, multi-slice, low-dose, spectral, or hybrid CT scanners, unlike smaller diagnostic centers or ambulatory surgical centers. Their focus on comprehensive patient care, continuous imaging services, and critical care diagnostics ensures that hospitals remain the dominant end-user segment, driving the largest share of CT scanner installations globally.

Region-wise Insights

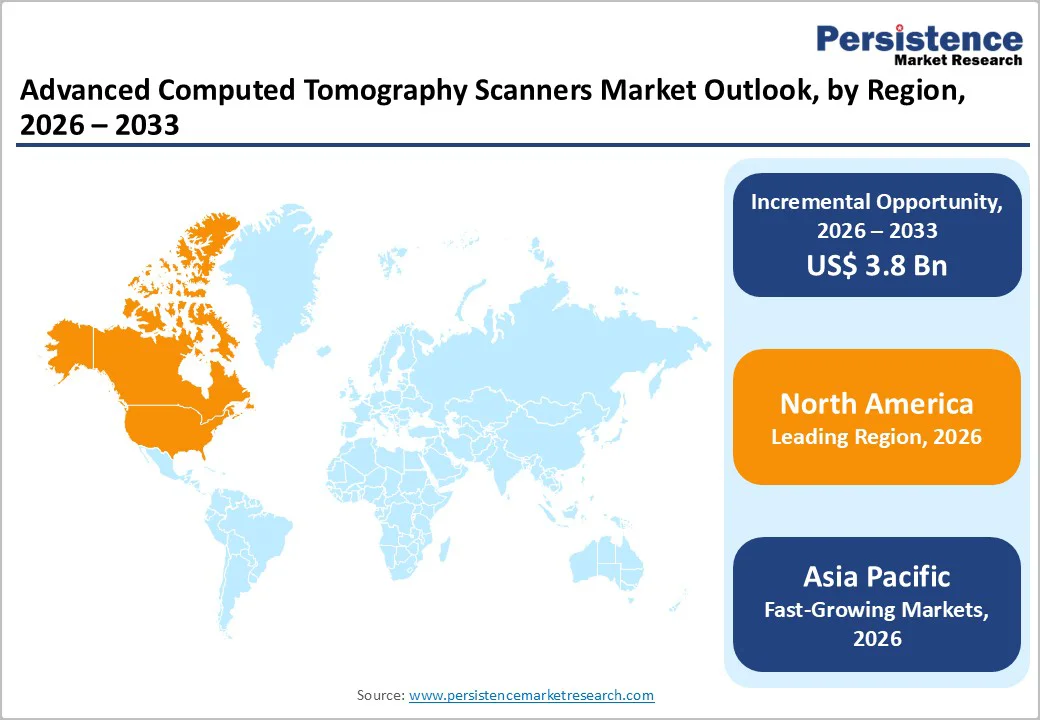

North America Advanced Computed Tomography Scanners Trends

North America leads the advanced computed tomography (CT) scanners market, driven by advanced healthcare infrastructure, high adoption of cutting-edge imaging technologies, and strong investments in hospital modernization. In the U.S., rising demand for low-dose and spectral CT scanners is fueled by lung cancer screening programs, cardiovascular diagnostics, and trauma care.

Hospitals and diagnostic centers increasingly adopt AI-enabled and high-slice CT systems to enhance image quality, reduce scan times, and improve patient outcomes. Continuous product innovation, favorable reimbursement policies, and growing awareness of early disease detection further strengthen North America’s dominance, making it the most mature and technologically advanced market globally.

Asia Pacific Advanced Computed Tomography Scanners Market Trends

The Asia Pacific advanced computed tomography (CT) scanners market is emerging rapidly due to expanding healthcare infrastructure, rising healthcare expenditure, and increasing demand for early disease diagnosis. Countries like China, India, Japan, and South Korea are investing in modern hospitals and diagnostic centers, driving the adoption of low-dose, spectral, and multi-slice CT scanners.

The rising prevalence of cancer, cardiovascular diseases, and trauma cases further fuels demand. Additionally, growing government initiatives for screening programs, increasing penetration of private healthcare, and technological collaborations with global CT manufacturers are accelerating market growth. This makes Asia Pacific a high-potential, fast-growing region in the international advanced CT scanner landscape.

Market Competitive Landscape

The Advanced Computed Tomography (CT) Scanners market is highly competitive, driven by continuous technological innovation and the introduction of high-slice, low-dose, spectral, and AI-enabled CT systems.

Companies focus on differentiating through specialized applications in oncology, cardiology, trauma, and portable imaging. Strategic partnerships, product launches, and regional expansions enhance market presence, while competitive pricing, service contracts, and subscription models influence adoption.

Key Industry Developments:

- In March 2025, GE HealthCare launched Revolution Vibe, its next-generation CT scanner designed specifically for coronary CT angiography (CCTA) and structural heart examinations.

Companies Covered in Advanced Computed Tomography Scanners Market

- Koninklijke Philips N.V.

- General Electric Company

- Siemens AG

- Carestream Health, Inc.

- Canon Inc.

- Xoran Technologies, LLC.

- Medtronic, Plc.

- iCRco, Inc.

- NeuroLogica Corp.

- Others

Frequently Asked Questions

The global advanced computed tomography scanners market is projected to be valued at US$8.3 Bn in 2026.

Increasing cases of cancer, cardiovascular diseases, neurological disorders, and trauma boost demand for accurate and early diagnosis through advanced imaging.

The global market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Growing adoption in ICUs, emergency rooms, and intra-operative settings for bedside imaging and faster clinical decision-making.

Koninklijke Philips N.V., General Electric Company, Siemens AG, Medtronic, Plc., and others.