- Medical Devices

- Trauma Care Centers Market

Trauma Care Centers Market Size, Share, and Growth Forecast, 2025 - 2032

Trauma Care Centers Market By Facility Type (In-house, Standalone), Trauma Type (Falls, Traffic-related Injuries, Stab/Wound/Cut, Burn Injury, Brain Injury), Service Type (In-patient, Outpatient, Rehabilitation), and Regional Analysis for 2025 - 2032

Trauma Care Centers Market Size and Trends Analysis

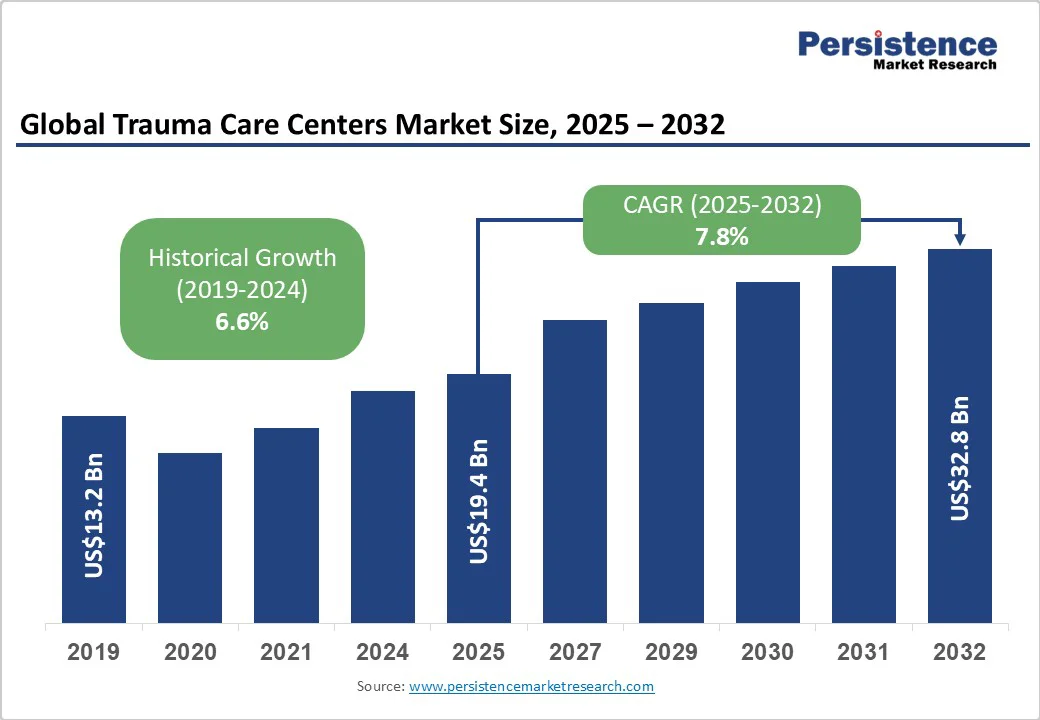

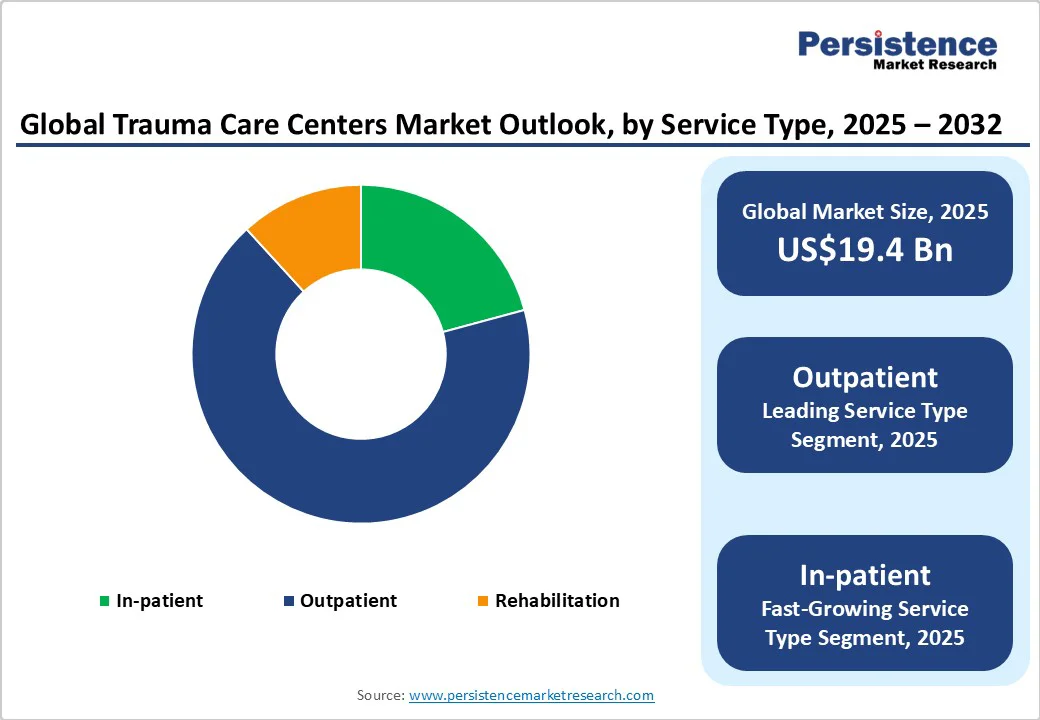

The global trauma care centers market size is likely to be valued at US$19.4 billion in 2025 and is estimated to reach US$32.8 billion in 2032, growing at a CAGR of 7.8% during the forecast period of 2025 -2032, driven by the rising demand for specialized emergency services. Increasing road traffic accidents also create a high demand for coordinated trauma intervention.

Key Industry Highlights:

- Leading Facility Type: In-house facilities hold a nearly 75.6% share in 2025, as they provide immediate access to multiple specialties under one roof.

- Dominant Trauma Type: Falls, approximately 46.8% of the trauma care centers market share in 2025, since these often result in fractures or head trauma requiring urgent treatment.

- Key Service Type: Outpatient services accounted for approximately 67.4% of the market share in 2025, as they enable quick care for minor injuries without requiring hospital admissions.

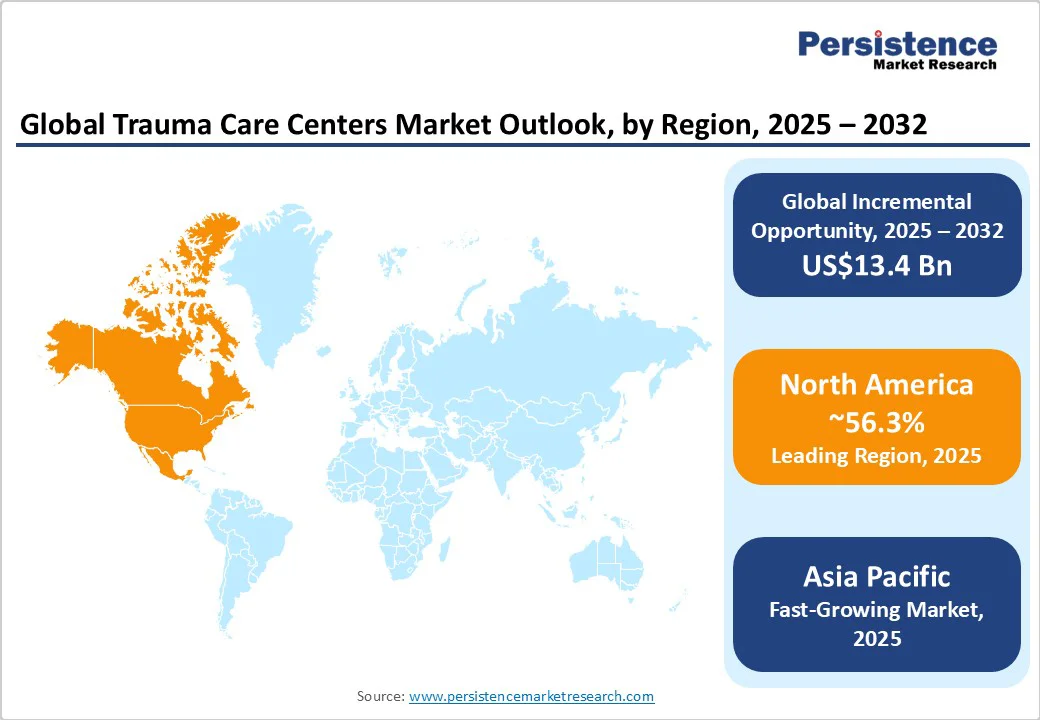

- Leading Region: North America, with about 56.3% share in 2025, backed by the widespread adoption of technology-driven care.

- Fastest-growing Region: Asia Pacific to register around 9.4% CAGR through 2032, owing to rising road accidents across India and China.

| Key Insights | Details |

|---|---|

| Trauma Care Centers Market Size (2025E) | US$19.4 Bn |

| Market Value Forecast (2032F) | US$32.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Number of Casualties Driven by Road Traffic Accidents

The need for trauma care centers is driven by the increasing frequency of road traffic accidents across both developed and developing countries. Urbanization, high vehicle ownership, and congested roads have led to a surge in high-impact collisions involving cars, motorcycles, and commercial vehicles.

Globally, road traffic injuries are a leading cause of death, particularly for young people, with over 1.35 million fatalities annually. Road traffic accidents often result in complex injuries, including fractures, head trauma, and internal bleeding, which require immediate, coordinated medical intervention.

Increase in Violence-related Trauma Cases

Another key factor fueling the trauma care centers market is the rising number of injuries stemming from violent incidents, including assaults, armed conflicts, and domestic violence. These cases frequently involve multiple organ injuries, penetrating wounds, or severe soft tissue damage, demanding immediate and highly specialized medical attention.

Hospitals in urban centers of North America and Europe have reported an increase in gunshot and stabbing cases, specifically among young adults. This has led to the establishment of trauma units with dedicated surgical teams, critical care beds, and quick blood transfusion facilities.

Barrier Analysis - Limited Government Funding and Support

One of the key challenges hindering market growth is the lack of financial backing from state and federal governments. Multiple public hospitals struggle to maintain fully equipped trauma units due to budget constraints, which affects staffing, technology upgrades, and facility expansion.

In the U.S., rural trauma centers often rely heavily on government subsidies, and any reduction in funding can lead to reduced service hours or even temporary closures. Similarly, in parts of the Asia Pacific and Eastern Europe, a lack of consistent governmental investment slows the establishment of new centers, limiting access to urgent care in underserved areas.

High Cost of Resources and Infrastructure

Trauma care centers require substantial investment in specialized personnel, innovative equipment, and advanced infrastructure, which can limit market growth. Recruiting trained trauma surgeons, anesthesiologists, critical care nurses, and emergency medical staff is expensive and competitive, mainly in regions facing workforce shortages.

Building hybrid operating rooms, fully-equipped ICUs, and rapid diagnostic imaging units further demands high capital expenditure. These high operational and setup costs make it challenging for small hospitals to establish fully functional trauma centers.

Opportunity Analysis - Improved Pre-hospital Care through Telemedicine

A significant opportunity exists in enhancing pre-hospital care through the use of telemedicine and rapid transport systems. Real-time consultation between paramedics and trauma specialists enables emergency teams to initiate treatment even before the patient arrives at the hospital, thereby reducing delays and improving survival rates.

Air ambulances, high-speed ground transport, and mobile diagnostic tools complement these digital interventions, enabling quick triage and decision-making. For instance, in Australia, the Royal Flying Doctor Service has integrated telemedicine links with regional trauma centers, allowing clinicians to guide paramedics in remote areas.

Integrated Systems for Managing Severe Injuries

Another growth opportunity comes from establishing comprehensive systems that not only address acute trauma but also support long-term recovery. Trauma centers that combine surgical intervention, intensive care, physiotherapy, and rehabilitation services provide a complete care pathway for patients with complex injuries.

This integrated approach improves patient outcomes, reduces readmission rates, and enhances hospital reputation. For example, Ganga Hospital in India has developed an end-to-end trauma program that includes critical care, orthopedic surgery, and post-discharge rehabilitation.

Category-wise Analysis

Facility Type Insights

In-house facilities are predicted to account for approximately 75.6% of the share in 2025 as they provide immediate access to a wide range of specialties such as neurosurgery, orthopedics, and cardiology under one roof. This integration speeds up decision-making and reduces transfer delays, which is crucial in the ‘golden hour’ following an injury. For example, Apollo Hospitals in India have built trauma units into their main hospitals, ensuring that patients can easily transition from emergency to surgery to intensive care without leaving the facility.

Standalone trauma centers are expanding because they provide dedicated resources and focus exclusively on trauma cases, avoiding competition with other hospital departments for operating rooms, imaging, or ICU beds. This specialization often results in quick triage and consistent care pathways.

In the Asia Pacific, hospitals such as Bangkok Hospital’s award-winning trauma center have proven that standalone models can attract international patients and recognition by delivering specialized trauma protocols, 24/7 air ambulance services, and hybrid operating theaters.

Trauma Type Insights

Falls are poised to remain at the forefront with a share of about 46.8% in 2025 as they affect all age groups, from children to the elderly, and can occur in everyday environments such as homes, workplaces, and public spaces.

Aging populations in Europe, North America, and parts of the Asia Pacific are specifically vulnerable, with osteoporosis and balance issues increasing risk. For instance, in the U.K., recent NHS data show that falls account for a significant portion of emergency admissions among adults over 65, highlighting how demographic shifts are driving this trend.

Traffic-related injuries are expected to be the fastest-growing segment through 2032, primarily due to increased vehicle ownership and high traffic density, particularly in India, China, and Southeast Asia. The combination of more motorcycles and two-wheelers, along with inconsistent traffic safety enforcement, contributes to high accident rates. In the U.S., even with improved vehicle safety, traffic-related trauma remains a leading cause of emergency visits among young adults.

Service Type Insights

Outpatient services are expected to hold nearly 67.4% of the market share in 2025, as they allow patients with minor injuries or post-surgery follow-ups to receive care without hospital admission, thereby saving time and reducing costs. Quick consultations, imaging, and rehabilitation can be managed in an outpatient setting. For example, in the U.S., several Level II trauma centers now operate outpatient fracture clinics and wound care units that handle high patient volumes.

Inpatient services are gaining momentum, backed by the increasing complexity and severity of cases, specifically from traffic accidents, falls among the elderly, and industrial injuries. Hospitals are investing in dedicated trauma wards, hybrid operating rooms, and ICU-equipped floors to handle multi-system injuries. Bangkok Hospital in Thailand has expanded its inpatient trauma facilities, delivering 24/7 critical care with specialized teams.

Regional Insights

North America Trauma Care Centers Market Trends

In 2025, North America is predicted to account for approximately 56.3% of the share. In the U.S., the largest cities are well covered with Level I and II trauma centers, ensuring that urban patients usually reach care within an hour. Programs such as the Trauma Quality Improvement Program help hospitals benchmark outcomes, making survival rates more consistent across leading centers. The major gap is in rural regions.

Several counties still lack trauma centers, leading to long transfer times that worsen outcomes. By contrast, some cities have too many centers competing for the same patient pool, which reduces case volume per hospital and can weaken training and specialist availability. There is also a staffing challenge. Trauma surgeons, neurosurgeons, and critical care nurses are in short supply. This shortage makes it difficult for small or newly designated centers to run at full capacity.

Asia Pacific Trauma Care Centers Market Trends

In the foreseeable future, the Asia Pacific will likely register a CAGR of nearly 9.4% as trauma care is improving consistently across India, Japan, and Thailand. Japan already has well-established trauma hospitals, while India is adding trauma facilities inside large multispecialty hospitals as well as building standalone trauma centers. Thailand’s Bangkok Hospital has earned awards for its trauma services, including the delivery of hybrid operating theaters, rapid response teams, and even air ambulance transfers.

At the same time, big gaps remain across lower- and middle-income countries. Several hospitals still lack fully designated trauma centers, and rural areas often face long delays in accessing specialized care. A survey across 15 Asia Pacific countries showed that only about 70% had at least one designated trauma center, and less than half had specialist trauma teams in place. Training and partnerships are emerging as key solutions. Ganga Hospital in India was recently named a Global Center of Excellence and is working with Johnson & Johnson MedTech to train surgeons across the region.

Europe Trauma Care Centers Market Trends

Europe is currently building more formal trauma networks. Ireland recently opened two Major Trauma Centers in Dublin and Cork as part of its National Trauma Strategy, marking a shift toward organized systems that link local trauma units with national hubs. Hospitals are also testing unique technology.

In France, an AI tool called Shockmatrix was trialed across eight university hospitals to support doctors in identifying hemorrhagic shock in trauma patients. Results showed its accuracy was close to that of human specialists, exhibiting how AI is starting to play a key role in emergency care.

Rural and cross-border access, however, remain major challenges. Multiple trauma centers are concentrated in large cities, leaving rural patients with long travel times. To address this, cross-border projects such as EGALURG (France-Spain) and Boundless Trauma Care (Central Europe) are using telemedicine and shared networks to connect small-scale hospitals with renowned trauma centers.

New facilities are also being built. In Vienna, construction is scheduled to start in 2024 on a modern Rehabilitation and Trauma Center in Meidling. It is expected to combine acute trauma services with long-term rehabilitation, a model not common in all cities.

Competitive Landscape

The global trauma care centers market is characterized by a mix of public trauma networks and private tertiary hospitals. Public systems, including the U.K.’s Major Trauma Center network, compete through national coverage and outcome reporting.

Private hospitals in markets such as India and the U.S. compete through brand reputation, speed of care, and novel facilities. Leading hospitals are investing in hybrid operating rooms, tele-triage systems, and robotic surgery to improve patient survival and throughput. Private players, such as Apollo Hospitals in India, utilize trauma-focused masterclasses and branded training programs to enhance their credibility and referral networks.

Business Strategies

Trauma care centers pursue innovation-driven strategies such as hybrid ORs, AI triage, and tele-ICU; cost leadership via integrated public trauma networks; and market expansion through cross-border hospital chains. Leaders differentiate through rapid EMS-to-surgery pathways, outcome transparency, and specialist teams. Emerging models include PPP trauma hubs and insurer-linked outcome contracts.

Key Industry Developments

- In September 2025, Saint Francis Hospital earned Level I Trauma Center verification from the American College of Surgeons. Hospitals with this designation offer round-the-clock access to trauma surgeons and specialists, as well as rehabilitation services, and participate in medical research.

- In June 2025, the Apollo Children’s Hospital established a center of excellence in pediatric orthopedics and trauma care. The facility aims to serve children who require specialized orthopedic treatment due to injuries sustained while playing sports or resulting from complex congenital conditions.

Companies Covered in Trauma Care Centers Market

- University of Alabama Hospital

- Banner Health

- Albany Med Health System

- St. Joseph’s Hospital and Medical Center

- China Medical University Hospital

- NYC Health + Hospitals/Bellevue

- Ascension St. John Hospital

- Kaiser Foundation Health Plan, Inc.

- Klinikum Stuttgart

- University Hospital Southampton NHS Foundation Trust

- Bellevue Hospital Center

Frequently Asked Questions

The trauma care centers market is projected to reach US$19.4 Bn in 2025.

Rising road traffic accidents and violence-related injuries are the key market drivers.

The trasuma care centers market is poised to witness a CAGR of 7.8% from 2025 to 2032.

Expanding pre-hospital care and the development of hybrid operating rooms are the key market opportunities.

University of Alabama Hospital, Banner Health, and Albany Med Health System are a few key market players.