- Automotive Components & Materials

- Vehicle Recycling Market

Vehicle Recycling Market Size, Share, and Growth Forecast, 2025 - 2032

Vehicle Recycling Market by Vehicle Type (Passenger Cars, Commercial Vehicles), Material (Iron & Steel, Aluminum, Non-ferrous Metals, Others), Process (Manual Dismantling, Shredding, Others), End-use (Materials, Reusable Parts, Construction, Others), and Regional Analysis for 2025 - 2032

Vehicle Recycling Market Share and Trends Analysis

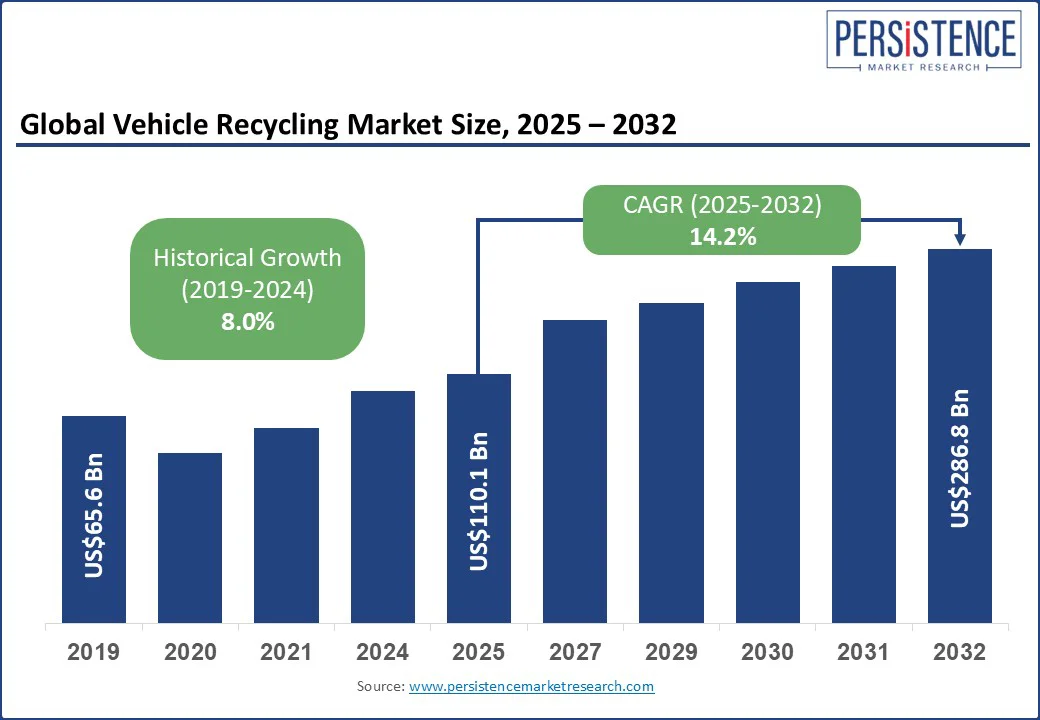

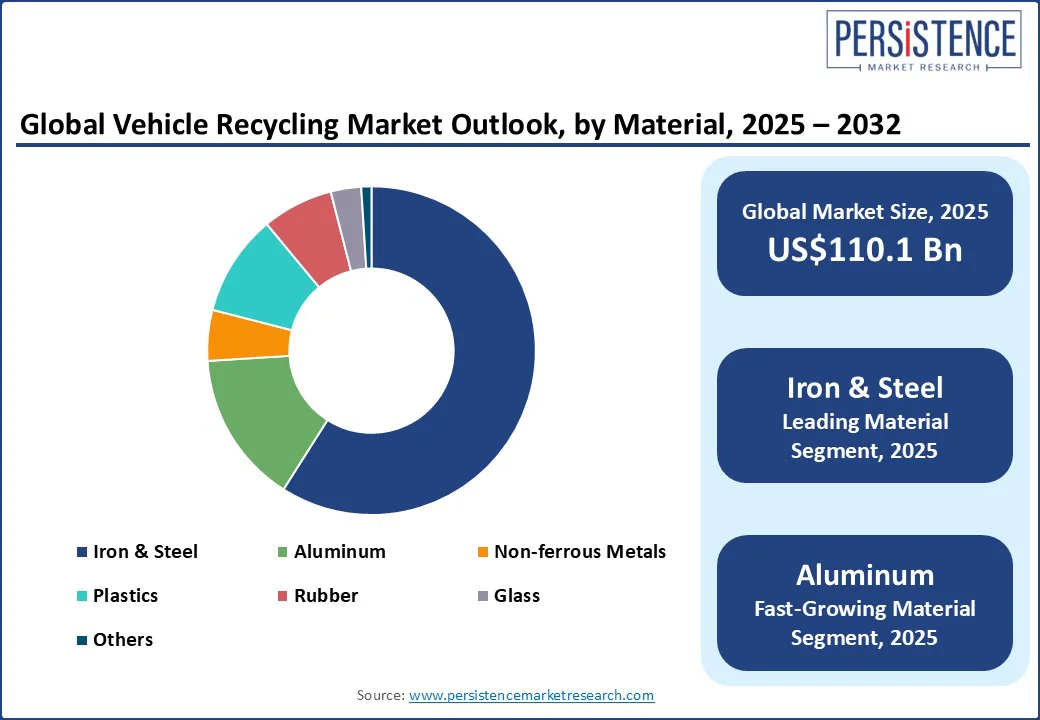

The global vehicle recycling market size is likely to value at US$ 110.1 Bn in 2025 to US$ 286.8 Bn by 2032, growing at a CAGR of 14.2% during the forecast period from 2025 to 2032.

The integration of AI-driven dismantling systems and sensor-based sorting technologies is improving material recovery rates while lowering operational costs, thereby benefiting market growth. Rising end-of-life vehicle (ELV) volumes, increasingly stringent sustainability mandates, and a surging demand for recycled materials across the automotive and manufacturing sectors drive the market growth.

Vehicle recycling occupies a central position in the circular economy, enabling the recovery and reuse of valuable materials such as steel, aluminum, plastics, and critical battery components from ELVs. By minimizing landfill waste and reducing the need for virgin raw materials, the recycling of vehicles not only mitigates environmental harm but also contributes to carbon footprint reduction across the automotive value chain.

The accelerated retirement of internal combustion engine (ICE) vehicles due to electrification policies is a key development supporting this market growth. By 2030, over 80 million ICE vehicles are expected to be phased out in the European Union (EU) and the U.S. alone, unlocking vast quantities of recyclable materials.

Key Industry Highlights:

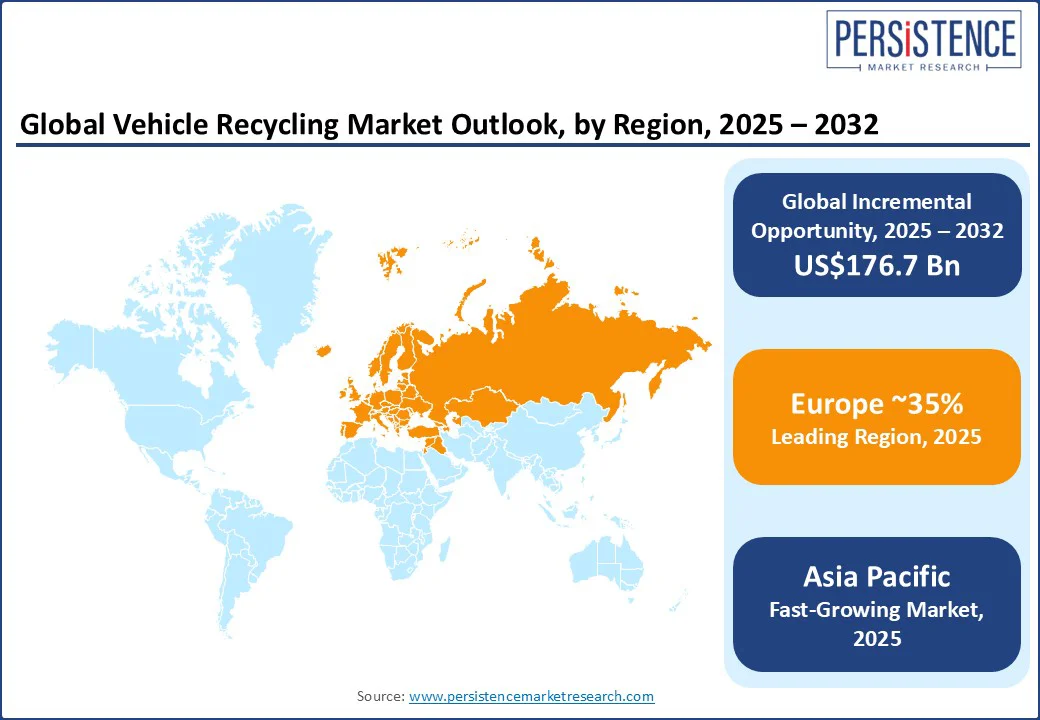

- Leading Region: Europe is expected to hold an estimated 35% of the market share by 2025 due to the rigorous recycling and sustainability mandates of the EU.

- Fastest-growing Region: Asia Pacific is set to register the highest CAGR of around 14% through 2032 on the back of strong vehicle scrappage policies being implemented in China, India, and Japan.

- Leading Material Segment: Iron & steel is expected to dominate in 2025 with a share of nearly 60%, driven by its high recovery rate and extensive demand in secondary steel production.

- Dominant Process: Manual dismantling will remain the dominant process in 2025 with a 58% share due to its cost-effectiveness in labor-intensive economies and higher salvage yield for resalable components.

- Investment plans: Growing focus on extended producer responsibility (EPR) and ELV regulations is pushing original equipment manufacturers (OEMs) and recyclers to invest in circular strategies and improve traceability across the value chain.

|

Global Market Attribute |

Key Insights |

|

Vehicle Recycling Market Size (2025E) |

US$110.1 Bn |

|

Market Value Forecast (2032F) |

US$286.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

14.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.0% |

Market Dynamics

Driver - Upsurge in EV Adoption Globally to Promote Structural Shifts in the Market

The rapid shift to EVs and government plans to phase out petrol and diesel cars are accelerating the scrapping of old vehicles, boosting the vehicle recycling market. According to the International Energy Agency (IEA), global EV stock surpassed 45 million in 2024, up from just 11 million in 2020, directly displacing ICE vehicles and expanding the vehicle recycling funnel. For instance, in 2022, the European Commission (EC) is planning to place a ban on the sale of all petrol and diesel cars from 2035.

California declared in 2020 that 100% of all in-state sales of new passenger cars and trucks will be zero-emission from 2035. As these ICE bans start taking effect, millions of legacy vehicles will approach end-of-life status in a few years, creating a historic surge in recyclable materials. This change will create a major shift in how vehicles are dismantled. Companies such as Redwood Materials and Ecobat have proactively begun partnering with OEMs to build reverse logistics networks that facilitate efficient collection and recycling of EV components, heralding the future of sustainable automotive materials management.

Restraint - Deep Presence of Informal Recycling Ecosystems to Temper Market Spirits

Even as the formal market for vehicle recycling gathers momentum, the predominance of informal and unregulated recycling operations, particularly in emerging economies, has consistently undermined material recovery efficiency, traceability, and environmental compliance. In countries such as India, Brazil, and parts of Southeast Asia, over 70% of ELVs are dismantled in off-the-grid scrapyards lacking standardized depollution protocols, resulting in a widespread pilferage of recoverable metals and leakage of hazardous fluids, compromising circular economy goals.

According to a 2023 UN Environment Programme (UNEP) report, the absence of formal ELV recycling frameworks in over 90 developing countries is delaying investment in advanced shredding systems, battery recycling infrastructure, and AI-based material sorting technologies. The continued existence of this parallel system also discourages participation from OEMs in extended producer responsibility (EPR) schemes, hindering the development of closed-loop supply chains for recycled automotive components.

Opportunity - Circularity of EV Batteries to Produce High-Value Profit Opportunities in Vehicle Recycling

The most lucrative opportunity is the high-margin recovery and repurposing of critical raw materials from end-of-life EV batteries. This high-value space is only set to explode as OEMs and governments pivot toward closed-loop supply chains to mitigate mineral scarcity and geopolitical risk. With EV battery demand expected to surpass 4,500 GWh by 2030, as per the IEA, recyclers are strategically investing in advanced hydrometallurgical and direct regeneration technologies to extract lithium, nickel, cobalt, and graphite.

Battery recycling companies are already securing long-term contracts and grants from governments and automakers to supply recycled battery-grade materials. For example, in May 2025, Poland’s Ministry of Economic Development and Technology offered a grant worth US$320 Mn to Ascend Elements for setting up a lithium-ion battery recycling facility in the country. As the average EV battery retains 70-80% of its energy storage capacity post-vehicle use, second-life applications in stationary storage also present attractive revenue streams for market players.

Category-wise Analysis

Material Insights

By material, the iron & steel segment is expected to account for nearly 60% of the revenue share in 2025, owing to the ubiquity of these materials in vehicle architecture and their established, highly efficient industrial recovery infrastructure. Recyclers regularly leverage high-volume shredding, magnetic separation, and bulk steel-baling systems that yield seamless reintegration into heavy industry supply chains. For instance, mature recycling hubs across North America and Western Europe consistently deliver under-20% processing margins due to economies of scale in ferrous metal recovery. This high-volume scrap ecosystem virtually guarantees stable revenue flows and makes iron & steel recycling the bedrock of the secondary metals space.

Aluminum recycling, on the other hand, is exhibiting rapid momentum, with this segment set to register the highest CAGR through 2032. Aluminum is both light and valuable, making it ideal for helping automakers meet rules to reduce vehicle weight and cut carbon emissions. Industry reports show recycled aluminum uses only 5% of the energy compared to making new aluminum and cuts carbon emissions by up to 95%. New rules, such as the EU’s targets for using more recycled plastics and metals in cars, have made aluminum recycling more profitable. This has led companies such as Novelis to invest heavily; it is even planning a U.S. IPO that could value it at up to US$12.6 Bn. Automotive OEMs, especially in the EV segment, are increasingly securing recycled aluminum to meet both weight targets and corporate sustainability commitments.

Process Insights

Among processes, manual dismantling is anticipated to lead the market with an approximate 58% share in 2025, on account of its unmatched flexibility in recovering high-value components and maximizing part reuse. In developing markets such as India and Brazil, where labor is available in abundance and is cheap, and the resale demand for used parts is high, manual dismantling enables recyclers to extract premium vehicle components that command lucrative aftermarket prices. Moreover, the manual process ensures compliance with environmental norms by safely draining fluids and segregating hazardous elements such as batteries and airbags. As the EU and other regulatory bodies across countries enforce stricter directives on ELV treatment and circular economy principles, the role of manual dismantling is becoming indispensable.

Battery recycling is unleashing explosive growth within the vehicle recycling market as the proliferation of EVs has catalyzed the demand for closed-loop critical minerals such as lithium, cobalt, and nickel. Battery recycling technologies will grow rapidly from 2025 to 2032 as more EVs retire, the EU enforces stricter recycled content rules, and OEMs shift their strategies toward sustainable supply chains. Companies are also scaling hydrometallurgical techniques and black mass refinement, opening up high-value recovery streams.

Regional Insights

Europe Vehicle Recycling Market Trends

Europe is expected to command an estimated 35% of the vehicle recycling market share by 2025. The primary reason cementing its top position is that the region is home to some of the world’s most rigorous recycling and sustainability mandates. The EU’s End-of-Life Vehicles Directive is the force majeure that is compelling automakers and recyclers to recover up to 95% of vehicle materials, institutionalizing best practices across the region.

Germany, France, and the Netherlands have capitalized on this momentum, deploying cutting-edge automation and material separation technologies across licensed dismantling centers. Furthermore, the integration of recycled aluminum, copper, and rare earths into new vehicle production lines has resulted in a self-sustaining loop that aligns with both environmental, social, and governance (ESG) compliance and resource efficiency. The maturity of the supply chain for ELV processing and an unrelenting focus on carbon-neutral manufacturing have justified Europe’s leadership in the vehicle circular economy landscape.

Asia Pacific Vehicle Recycling Market Trends

Asia Pacific, the fastest-growing vehicle recycling market with a projected 14% CAGR through 2032, offers major growth opportunities for both global and local recycling companies. China’s national scrappage programs, Japan’s longstanding auto recycling expertise, and India’s evolving ELV policy framework are converging to push the possibilities of the market here.

According to the International Council on Clean Transportation (ICCT), China scrapped and replaced over 6 million vehicles in 2024. In India, the Ministry of Road Transport and Highways launched the Voluntary Vehicle Modernization Program or Vehicle Scrapping Policy in 2024 to create an ecosystem for phasing out unfit polluting vehicles across the country through a network of Registered Vehicle Scrapping Facilities (RVSFs) and Automated Testing Stations (ATSs). Meanwhile, EV adoption across the region is generating a new stream of end-of-life batteries, prompting investments in lithium recovery and urban mining hubs.

North America Vehicle Recycling Market Trends

In 2025, North America is anticipated to hold a market share of about 28%, buoyed by a unique mix of public-private initiatives to promote recycling practices, policy stimulus, and a well-established industrial capacity for recycling operations. In the U.S., the Inflation Reduction Act (IRA) has triggered a storm of investments in lithium-ion battery recycling and sustainable materials recovery, aiding the shift toward domestic, closed-loop recycling ecosystems.

Industry leaders such as Redwood Materials and Li-Cycle are setting up vertically integrated facilities that fuse AI-powered dismantling, safe battery extraction, and rare metal reclamation. A high turnover of aging vehicles, especially pickup trucks and sports utility vehicles (SUVs) has ensured a steady supply of ELVs. Banking on its forward-leaning approach to building out resilient and tech-enabled automotive recycling infrastructure, North America has positioned itself as a key stakeholder in shaping the future of green vehicle disposal and sustainable mobility.

Competitive Landscape

The global vehicle recycling market landscape is undergoing unprecedented evolution, characterized by technological upgrades, policy-induced disruption, and strategic vertical integration across key value chains. Industry players are aggressively scaling operations in advanced material recovery, engaging in a wide spectrum of operations ranging from AI-powered scrap sorting and robotic dismantling to closed-loop EV battery recycling.

Market differentiation is intricately tied to capabilities in smart logistics, sustainable processing, and digital salvage platforms that streamline end-of-life vehicle recovery while enhancing traceability. The European Commission recently fined several automakers € 458 million (US$ 498 million) for colluding in ELV recycling practices, putting global players on high alert. Leading vehicle recyclers are responding by embedding circular economy strategies, aligning with OEM sustainability goals, and investing in regional facilities to localize the supply of secondary raw materials such as steel, aluminum, lithium, and rare earths.

Key Industry Developments

- In June 2025, Tata Motors opened two new vehicle scrapping facilities in Lucknow and Raipur under its Re.Wi.Re (Recycle with Respect) initiative. Together, they can dismantle up to 40,000 old vehicles each year, including two-wheelers, cars, and trucks. These high-tech, paperless facilities have dedicated stations to safely handle parts such as tires, batteries, and fluids. The move supports India’s Vehicle Scrappage Policy, promotes recycling, and helps shift toward cleaner, more efficient vehicles.

- In June 2025, the European Union introduced a new regulation on end-of-life vehicles (ELVs) to boost recycling and sustainability in the auto industry. It now covers not just cars but also trucks, motorcycles, buses, and special-purpose vehicles. The law requires that at least 25% of plastic in new vehicles comes from recycled sources. It also strengthens rules that make vehicle makers responsible for the cost of collecting and recycling old vehicles, including those without known owners.

- In May 2025, Toyoda Gosei, a top Japanese auto parts maker, developed a new recycling technology that creates high-quality plastic with 50% recycled content from end-of-life vehicles (ELVs). This recycled plastic matched the strength and durability of new plastic, making it suitable for tough interior car parts. The breakthrough, achieved in partnership with recycler Isono, used special material treatment techniques and supported "horizontal recycling", reusing plastics in the same type of auto parts.

Companies Covered in Vehicle Recycling Market

- ASM Auto Recycling Ltd.

- Copart, Inc.

- Eco-Bat Technologies Ltd.

- INDRA (India)

- Keiaisha Co., Ltd.

- Hensel Recycling Group

- LKQ Corporation

- Schnitzer Steel Industries, Inc.

- Scholz Recycling GmbH

- Sims Metal Management Limited

Frequently Asked Questions

The global vehicle recycling market is projected to reach US$ 110.1 Bn in 2025.

The rapid growth of EV adoption and government rules to phase out older vehicles amplify the market growth.

The vehicle recycling market is poised to witness a CAGR of 14.2% from 2025 to 2032.

Recovering valuable materials from old EV batteries and reusing them is a big opportunity. Car makers and governments are also focusing on recycling to reduce the risk of running out of key minerals and to avoid relying too much on certain countries.

ASM Auto Recycling Ltd., Copart, Inc., and Eco-Bat Technologies Ltd. are some of the leading market players.