- Telecommunications

- U.S. Fintech Market

U.S. Fintech Market Size, Share, Trends, and Growth Forecast, 2025 - 2032

U.S. Fintech Market by Service Type (Payment, Lending, Banking, Insurance, RegTech, Wealth Management and Investment, Personal Finance / Financial Planning, and Others), Technology (AI & ML, Blockchain, Robotic Process Automation (RPA), API, and Others), Deployment Mode, and End-user Analysis for 2025 - 2032

U.S. Fintech Market Size and Trends

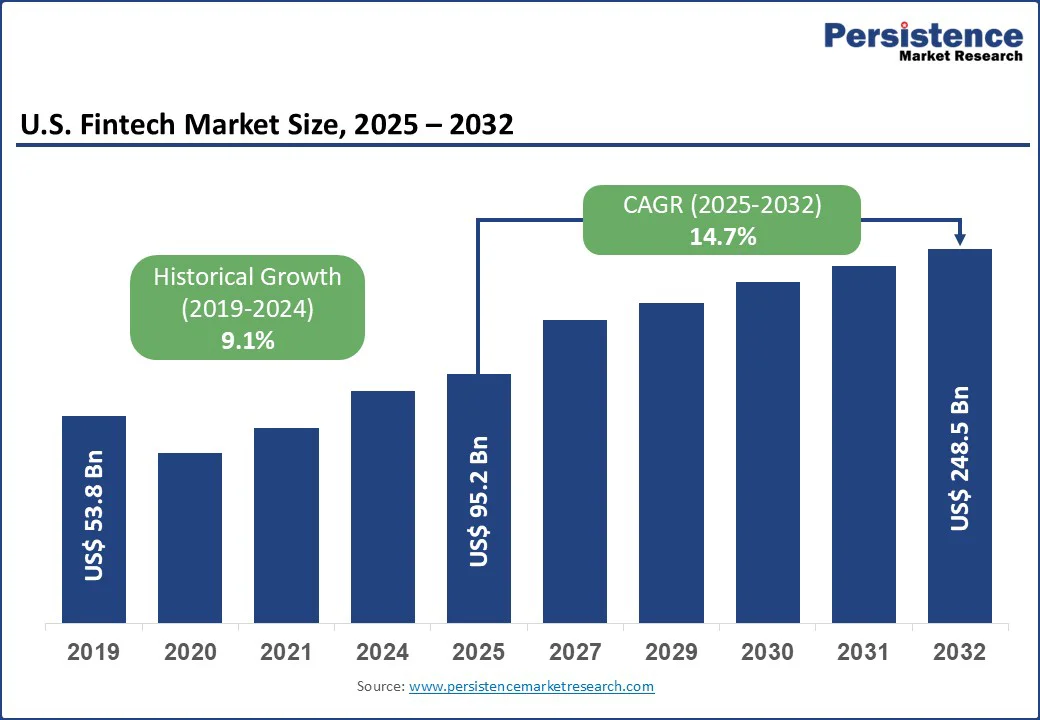

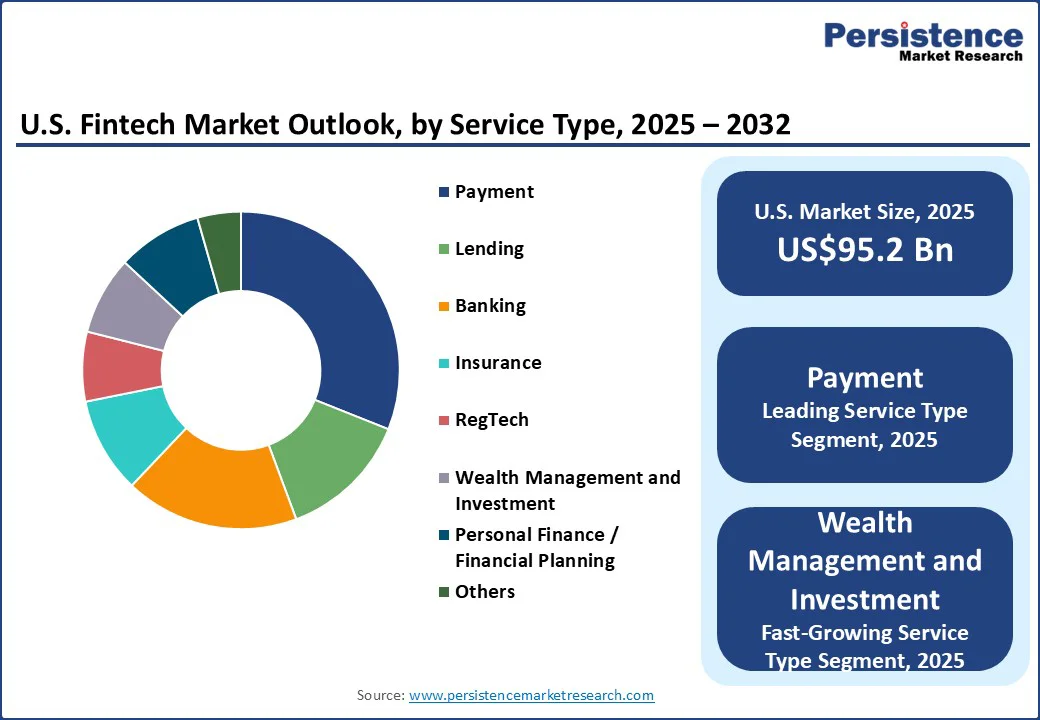

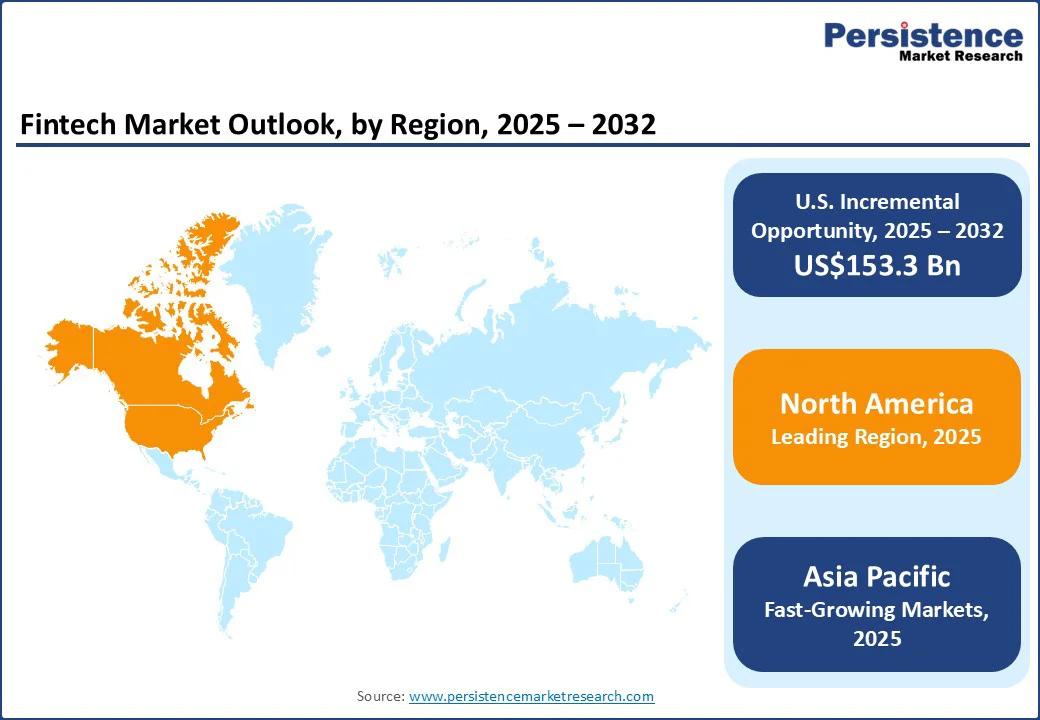

The U.S. fintech market size is likely to be valued at US$95.2 Bn in 2025 and is expected to reach US$248.5 Bn by 2032, growing at a CAGR of 14.7% during the forecast period from 2025 to 2032.

Key Industry Highlights:

- Dominant Service Type: Payment, over 35% share due to the increasing demand for faster, secure, and seamless transaction processing. Businesses and consumers prefer digital payment solutions that enhance convenience, reduce fraud, and support real-time financial operations.

- Leading Technology: API, holding more than 32% market share in 2025, as they facilitate real-time data exchange, improve transaction speed, and enhance customer experience.

- Dominant End-user: Banks, with over 40% share, due to their extensive customer base, established trust, and regulatory expertise. They are increasingly integrating advanced digital solutions to enhance operational efficiency and customer experience.

- Key Growth Driver: Seven in ten U.S. consumers used mobile payments in 2024, with mobile transactions rising to 32% of all costs. At the same time, fraud losses surged to $12.5 billion, up 25% from 2023, highlighting both massive adoption and the urgent need for secure fintech solutions.

| U.S. Fintech Market Attribute | Key Insights |

|---|---|

| Fintech Market Size (2025E) | US$95.2 Bn |

| Market Value Forecast (2032F) | US$248.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 14.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 9.1% |

The market growth is driven by increasing demand for faster, more secure, and convenient digital financial services, as businesses and consumers seek quicker transaction processing, improved risk management, and enhanced financial insights.

Advancements in AI, blockchain, and cloud computing are enabling innovative solutions, while regulatory support and initiatives for financial inclusion further fuel market expansion. As competition intensifies, firms are focusing on technology-driven differentiation and strategic partnerships to capture market share.

Market Dynamics

Driver- Consumer Demand for Convenience and Policies Encouraging Transparency

Consumers’ increasing demand for accessible, user-friendly, and on-demand financial services has fueled the rise of digital wallets, peer-to-peer platforms, and mobile banking apps. Features such as instant transfers, real-time alerts, and personalized advice offered by solutions like Venmo and Cash App are transforming expectations.

According to the Diary of Consumer Payment Choice (2024), consumers made an average of 48 payments per month, two more than in 2023, with mobile phone payments making up 23% of all transactions, 11% of in-person non-bill payments, and 45% of remote payments.

This digital shift, coupled with regulatory momentum, creates a pressing need for LegalTech solutions to ensure compliance, transparency, and data security. The Consumer Financial Protection Bureau (CFPB) has finalized rules enabling consumers to share financial data securely with third-party apps. At the same time, initiatives like tech sprints promote innovation and fair lending practices.

Antitrust action, such as the U.S. Department of Justice lawsuit against Visa for monopolizing the debit card market, underscores heightened legal scrutiny. Adoption of open banking payments remains limited, with only 11% of U.S. adults making such transactions in 2024, according to a study on Consumer Sentiment About Open Banking Payments, underscoring the role of LegalTech in building trust and enabling a competitive financial ecosystem.

Restraint- Data Protection and Compliance Challenges

Rising data breaches remain a major challenge, compromising sensitive information such as credit card details and personal identification data. These incidents often originate from phishing attacks, malware, and API vulnerabilities, leading to financial losses, legal consequences, and loss of customer trust.

According to the Federal Trade Commission, consumers reported losses of over US$12.5 billion to fraud in 2024, up 25% from 2023, with government imposter scams alone surging to $789 million. The growing reliance on third-party vendors further magnifies risks, as the SecurityScorecard Report shows that 42% of breaches in top fintech companies originated from third-party vendors.

Compliance with stringent regulations also adds to operational burdens. Laws such as the Gramm-Leach-Bliley Act (GLBA) mandate safeguarding nonpublic personal data, while the California Consumer Privacy Act (CCPA) grants consumers extensive rights over their personal information.

Meeting these requirements entails high operational costs for implementing safeguards, conducting audits, and training employees. Non-compliance results in hefty fines and reputational damage, with smaller firms particularly vulnerable as the financial and administrative burden diverts focus away from innovation and core business activities.

Opportunity- Strengthening Legal Oversight in Embedded Finance, Open Banking & WealthTech

The rapid rise of embedded finance in platforms like e-commerce, ride-hailing, and SaaS is creating significant opportunity. For instance, Shopify Pay makes checkout four times faster and boosts conversion rates by 1.7, but this also creates legal complexities around consumer protection, liability, and partnership contracts.

LegalTech firms can enable automated compliance checks, digital contracting, and regulatory monitoring, ensuring fintech platform collaborations operate securely and within legal frameworks while enhancing customer trust.

The move toward open banking is another catalyst, with the CFPB’s October 22, 2024, Personal Financial Data Rights rule mandating free consumer data portability. Secure APIs are replacing risky screen-scraping, opening avenues for account aggregation, automated lending, and pay-by-bank flows, but also increasing the need for legal oversight in data-sharing, risk management, and consumer rights enforcement.

The rise of AI-driven WealthTech platforms that expand access to private equity, hedge funds, and real estate investments brings heightened compliance and investor-protection needs. As fintech broadens into retirement planning, lending, and insurance, LegalTech is uniquely positioned to support contract automation, regulatory adherence, and dispute resolution, making it a key enabler.

Fintech Market Key Trends

Digital Wallet Adoption and Neobank Growth

The rapid adoption of digital wallets and contactless payments is reshaping consumer behavior, pushing merchants, banks, and fintechs to integrate wallet-friendly acceptance, tokenization, and real-time settlement. The Federal Reserve’s 2024 Survey and Diary of Consumer Payment Choice reports that seven in ten consumers used a mobile phone for payments at least once in the prior year, with mobile’s share rising from 28% to 32% of all payments.

This surge necessitates clear frameworks for liability, chargebacks, tokenization, and instant settlement, areas where LegalTech solutions aid institutions in interpreting regulatory requirements and updating digital payment contracts accordingly.

The U.S. Treasury highlights that cash usage fell from 31% in 2017 to just 16% in 2023, underscoring the long-term shift toward electronic and mobile-first banking. Neobanks, which operate branch-free, rely on digital platforms, APIs, and real-time rails to meet demand for instant payments, budgeting tools, and cross-border transfers, especially among millennials and Gen Z, according to the Federal Reserve, 2024.

SMEs are also adopting neobank services such as payroll and invoicing, which rely on API-driven integration. These shifts expand the volume of digital agreements, compliance checks, and data-sharing arrangements, making LegalTech essential for managing regulatory adherence in an increasingly digital financial environment.

Category-wise Analysis

By Service Type, Payment Enables Faster, Secure, and Convenient Transactions

Based on the service type, the market is divided into payment, lending, banking, insurance, RegTech, wealth management & investment, personal finance/financial planning, and others. Payment is expected to account for more than 35% share in 2025, due to the growing demand for faster, secure, and convenient transactions.

The rise of e-commerce, digital wallets, and contactless payments has accelerated the shift from cash and traditional banking. Businesses and consumers increasingly prefer real-time payments, peer-to-peer transfers, and integrated payment gateways. Regulatory support and innovations like tokenization and fraud prevention are driving widespread adoption, making payment services the core of fintech growth.

For instance, in July 2023, the Federal Reserve introduced the FedNow Service to facilitate instant payments, underscoring the emphasis on real-time payment solutions.

Wealth management and investment services are expected to grow at the highest rate due to increasing adoption of digital platforms for personalized investment advice, robo-advisors, and automated project portfolio management. Rising disposable incomes and greater retail investor participation are driving demand for accessible, low-cost investment solutions. Integration of AI and analytics enables smarter decision-making, while millennials and Gen Z prefer mobile-first, seamless financial experiences.

By Technology, APIs Drive Interoperability and Enhanced Customer Experience

In terms of technology, the market is segregated into AI & ML, blockchain, robotic process automation (RPA), API, and others. Out of these, the API (application programming interface) is expected to account for more than a 32% share in 2025, as it enables seamless integration across financial systems, supporting faster, more secure, and personalized services.

The demand for real-time data sharing, automation, and interoperability drives API adoption, while services like embedded finance, digital wallets, and automated payments benefit from it. Regulatory support, including PSD2-like initiatives, further accelerates API usage, reducing operational costs and enhancing customer experience.

For instance, the CFPB’s new open banking rules require banks with assets exceeding $850 million to provide consumer financial data access via APIs, making secure data sharing mandatory.

AI & ML are expected to grow at a significant rate due to their ability to enhance decision-making, automate processes, and personalize financial services. Banks and fintech firms are increasingly using AI-driven analytics for credit scoring, fraud detection, and risk management, reducing operational costs and improving efficiency.

Machine learning models enable predictive insights for investments and customer behavior, fostering smarter, faster financial solutions. For instance, in fiscal year 2024, AI-driven fraud detection tools, including machine learning, enabled the U.S. Treasury Department to prevent and recover over $4 billion, highlighting their effectiveness in combating financial fraud.

By End-use, Banks Lead with Streamlined Operations and Fintech Collaboration

Based on the end user, the market is divided into banks, financial institutions, investment firms, non-banking financial companies, and others. Banks are expected to account for more than 40% share in 2025, as they increasingly integrate advanced digital solutions to enhance customer experience, streamline operations, and reduce costs.

Their extensive customer base and regulatory expertise enable the adoption of technologies like AI, blockchain, and real-time payments. Leveraging regulatory familiarity, banks offer secure fintech services while ensuring compliance with data privacy and anti-fraud measures.

For instance, the Federal Reserve, FDIC, and OCC issued a joint statement in July 2024 outlining potential risks and risk management practices related to arrangements between banks and third parties to deliver bank products and services, highlighting the increasing collaboration between banks and fintechs.

Non-banking financial companies (NBFCs) are expected to grow at a significant rate due to their flexibility and ability to serve niche financial needs that traditional banks often cannot. It also capitalizes on underserved segments, such as gig workers, SMEs, and digitally native customers, who prefer quick, seamless digital transactions.

Their lighter regulatory burden compared to banks allows them to innovate rapidly and scale operations efficiently. According to the Federal Reserve System, between 1990 and 2024, credit lines extended by banks to non-bank financial institutions grew from $0.08 trillion to $0.6 trillion, reflecting a structural shift in bank engagement with NBFIs.

By 2024, credit lines to NBFIs accounted for approximately 3% of U.S. GDP, indicating significant systemic exposure and highlighting the growing role of NBFIs in the financial system.

Competitive Landscape

The U.S. Fintech market is fragmented, with numerous players offering a range of digital financial solutions. Companies are driving innovation through AI and blockchain to deliver faster and more secure services. They are forming strategic partnerships to expand their reach and executing mergers and acquisitions to scale operations and enter new segments. Competitive pricing, user-friendly digital interfaces, and strict regulatory compliance are helping them build market trust.

Key Industry Developments:

- In August 2025, ClarityPay joined the American Fintech Council (AFC), offering merchants flexible installment payment options at checkout. The platform helps businesses manage risk, set terms, and maintain control over customer experience.

- In June 2025, PayPal plans to expand its PYUSD stablecoin to the Stellar blockchain, pending regulatory approval, joining Ethereum and Solana. Leveraging Stellar’s fast, low-cost infrastructure, PYUSD could be used for global payments, remittances, and everyday transactions. PayPal also aims to support small businesses with near-instant working capital through its “PayFi” financing model.

- In April 2025, Affirm launched AdaptAI, an AI-powered promotions platform for merchants. It enables personalized offers like exclusive APR rates, special repayment terms, and cash savings delivered to consumers via the Affirm App and Card. Merchants can now provide real-time, targeted promotions optimized for each customer’s shopping habits at checkout.

Companies Covered in U.S. Fintech Market

- PayPal

- Block Inc.

- Affirm, Inc.

- Upstart Network, Inc.

- Social Finance, LLC

- Stripe Inc.

- Chime Financial, Inc.

- Plaid Inc.

- Brex Payments LLC

- Mercury

- Oscar Insurance

- Avant LLC

- Others

Frequently Asked Questions

The U.S. fintech market is projected to be valued at US$95.2 Bn in 2025.

Growing demand for faster, secure, and convenient digital financial services, supported by mobile banking, digital payments, is the key driver of the fintech market.

The U.S. fintech market is poised to witness a CAGR of 14.7% from 2025 to 2032.

Advancements in AI and open banking enable secure data sharing and personalized financial services, driving strong growth opportunities in the market.

PayPal, Block Inc., Affirm, Inc., Upstart Network, Inc., Social Finance, LLC, Stripe Inc., Chime Financial, Inc., Plaid Inc. are among the leading key players.