- Healthcare Services

- U.S. CMO/CDMO Market

U.S. CMO/CDMO Market Trends, Size, Share, and Growth Forecast, 2025 - 2032

U.S. CMO/CDMO Market By Services (Drug Discovery and Development, API Manufacturing, Finished Dosage Formulation Development, Packaging/Distribution), Scale of Operation (Preclinical, Clinical, Commercial), Organization Size, Therapeutic Area, and Analysis for 2025 - 2032

U.S. CMO/CDMO Market Size and Trends Analysis

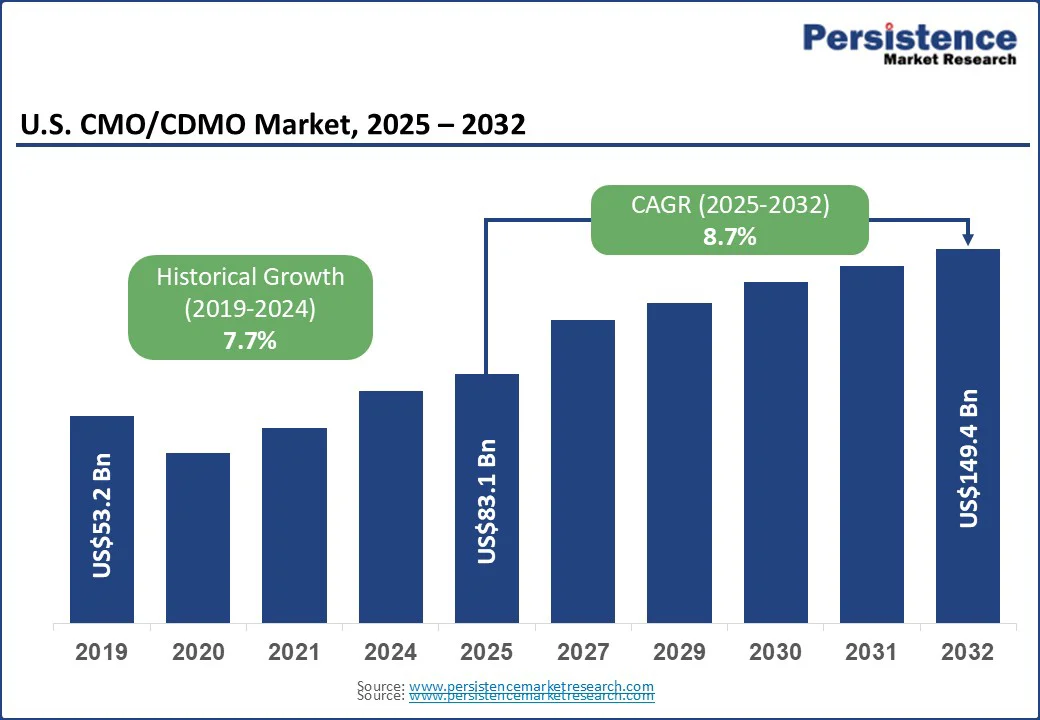

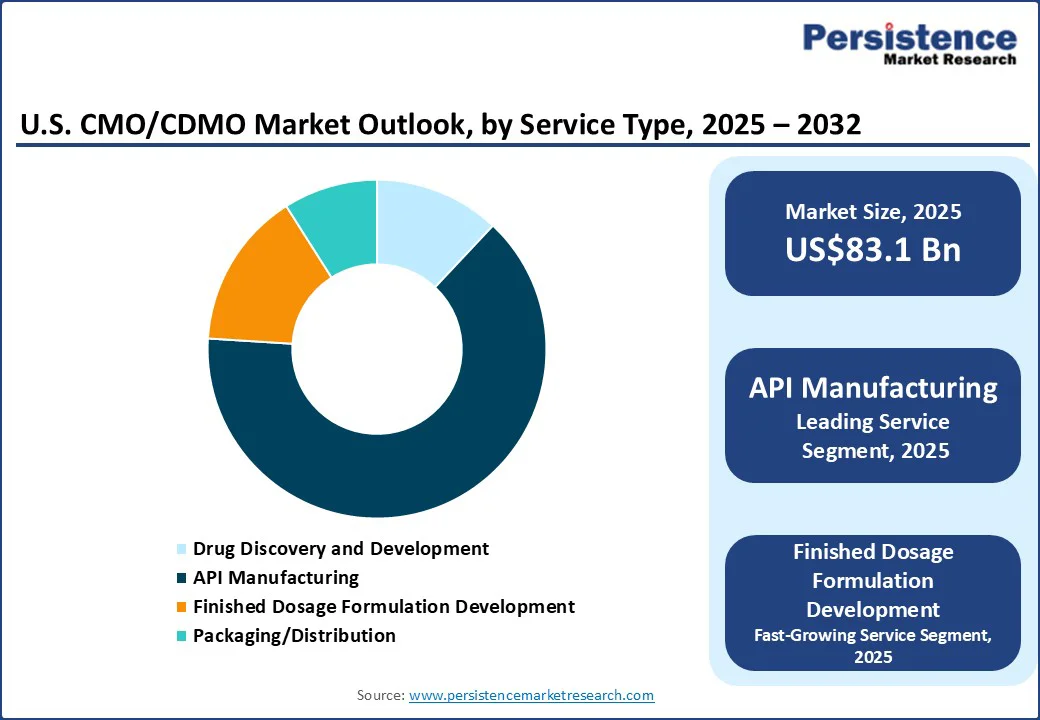

The U.S. CMO/CDMO market size is likely to be valued at US$83.1 Bn in 2025 and is expected to reach US$149.4 Bn by 2032, growing at a CAGR of 8.7% during the forecast period from 2025 to 2032, driven by the expanding demand for a wide range of services, including API manufacturing, formulation development, packaging, and labeling, across both pharmaceutical and biopharmaceutical sectors.

Key Industry Highlights:

- Leading Service Type: API manufacturing services dominate within the U.S. CMO/CDMO market, as APIs for small molecules continue to drive large batch-production, and long-term supply contracts for many pharma clients based in the U.S.

- Dominant Therapeutic Area: Oncology is the dominant therapeutic area in the U.S. CMO/CDMO market, due to the growing shift toward targeted biologics and cell-based therapies, an expanding clinical pipeline, and high R&D investments in the oncology space.

- Emerging Opportunity: The rapid expansion of emerging biopharma companies, particularly small and mid-sized firms developing niche and advanced therapies, is creating substantial growth opportunities for CDMOs.

- Key Trend: Outsourcing manufacturing and development services to CDMOs offers significant cost advantages to U.S. biopharma companies by eliminating the need for upfront capital expenditure (CAPEX) on GMP-compliant facilities and reducing the risk of idle manufacturing capacity.

| Key Insights | Details |

|---|---|

|

U.S. CMO/CDMO Market Size (2025E) |

US$83.1 Bn |

|

Market Value Forecast (2032F) |

US$149.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

CDMOs Driving Cost Efficiency and Faster Commercialization in the U.S. Biopharma Sector

Outsourcing manufacturing and development services to CDMOs provides U.S. biopharma firms with tangible cost advantages by eliminating the need for upfront capital investment in GMP-compliant facilities and reducing the risk of underutilized capacity. Partnerships with CDMOs are enabling faster commercialization of niche and orphan therapies as they handle key processes and reduce operational and logistical burden for pharma.

Growing demand for API and sterile injectables has further led to mid-sized biotech firms outsourcing these services and increasing their overall capacity, thereby reducing overall time-to-clinic and cash burn. The CDMO channel has become a key lever for cost containment and financial flexibility across the U.S. pharma portfolios.

Advanced Therapies Driving U.S. CMO/CDMO Market Expansion and Facility Investments

The rapid proliferation of advanced therapy modalities such as cell, gene, viral vectors, and mRNA, requiring specialized bioprocessing and fill-finish capabilities, is significantly driving the U.S. CMO/CDMO market. These modalities require manufacturing in a closed-system environment, alongside suites for viral-vector handling, cryogenic logistics, and custom-made potency assays, encouraging biopharma companies to partner with CDMOs that already possess accredited facilities.

Several CDMO firms are also upgrading their facilities in the U.S. to expand manufacturing capacities. In June 2025, Piramal Pharma Solutions announced a US$90 Mn investment in its Lexington and Riverview sites to expand capabilities in sterile injectables and antibody-drug conjugates (ADCs) through its integrated CDMO offering.

Rising Operational Costs and Supply Chain Complexity

The biotech sector requires highly specialized talent due to its complexity and technical demands. In the U.S., a shortage of qualified personnel and inflationary input costs associated with consumables and cold chain logistics are increasing the operational expenses. Constructing and validating new GMP suites is costly and time-consuming, extending CAPEX payback periods.

Additionally, risks associated with the supply chain, such as dependence on a limited supplier or raw material shortages, further increase operational risks, forcing CDMOs to hold higher safety stocks, tying up capital. Rising costs thus force CDMOs to carefully balance capacity investment and margins while managing operational risks.

Emerging Biopharma & Demand for Drug Discovery/Bioprocessing

There are over 5,000 pharma and biotech companies in the U.S., creating sustained demand for CDMO services across various processes, particularly in oncology, immunology, and rare diseases. The rapid growth of emerging biopharma companies, including small- and mid-sized firms focused on niche and advanced therapy modalities, is creating significant opportunities in the CDMO market. These companies often lack specialized capabilities and infrastructure to carry out end-to-end processes, such as drug discovery, development, and in-house bioprocessing.

Increasing clinical trial pipeline and R&D activity, coupled with shorter timelines to clinic and commercialization pressures, are fueling demand for outsourced capabilities to manage process development, high-throughput analytics, cell-therapy scale-up, regulatory compliance, and quality assurance. CDMOs provide these integrated services, acting as strategic partners that enable emerging biopharma firms to accelerate innovation, reduce capital expenditure, and bring novel therapies to market faster, creating a significant growth and revenue opportunity for CMOs/CDMOs in the U.S. market.

Category-wise Analysis

Service Type Insights

API manufacturing services dominate within the U.S. CMO/CDMO market as APIs for small molecules continue to drive large batch production, and long-term supply contracts for many pharma clients based in the U.S. Manufacturers outsource API chemistry to CDMOs to access advanced manufacturing capabilities without capitalizing on fixed assets. Being a high-volume and low-risk revenue base for CDMOs, API manufacturing remains the backbone of the U.S. contract-manufacturing landscape.

Therapeutic Area Insights

Oncology is the dominant therapeutic area in the U.S. CMO/CDMO market due to the growing shift toward targeted biologics and cell-based therapies, an expanding clinical pipeline, and high R&D investment in the oncology space. CDMOs are uniquely positioned to offer essential guidance and assistance throughout the complex transition from drug development to commercial manufacturing. Increasing demand for rapid and safe delivery of new cancer therapies, coupled with urgent clinical timelines, is driving pharma companies to invest more in CDMO partnerships to accelerate product delivery.

U.S. CMO/CDMO Market Trends

Expansion of Capacity through M&A and New Facilities

Large CDMO firms in the U.S. are expanding their capacity through both strategic acquisitions and large-scale facility upgrades. Development of specialized suites such as single-use bioreactors, sterile injectable lines, and viral vector suites, etc., together with the acquisition of niche providers by these big CDMOs, is filling the technology gaps.

Mergers and acquisitions are accelerating the time-to-market for new capabilities, consolidating demand for outsourced CDMO services across novel modalities and commercial-scale production. In December 2024, Novo Holdings A/S acquired leading CDMO firm, Catalent, Inc., to integrate Catalent’s fill-finish manufacturing facilities and boost production of Novo Nordisk’s diabetes and weight-loss drugs. In July 2025, ESTEVE CDMO acquired Regis Technologies, a CDMO firm based in the U.S., to expand its CDMO services for small-molecule API in the U.S.

Shift Toward End-to-End “One-Stop-Shop” Models

Biopharma companies in the U.S. are increasingly preferring CDMOs that offer end-to-end services, including process development, analytics, commercial manufacturing, and regulatory support. This “one-stop-shop” model helps accelerate regulatory filings, reduce technology transfers, and centralize accountability. Leading CDMOs are offering single points of contact and integrated project governance agreements, driving horizontal integration within the sector and incentivizing CDMOs to invest in cross-functional teams that support the entire product lifecycle.

CDMO’s Integration with Clinical Research Functions

CDMO firms in the U.S are expanding into clinical research operations to offer hybrid CRO-CDMO services to their clients. This includes providing manufacturing, logistics, and even clinical trial support services. This convergence of services is helping pharma companies shorten IND (Investigational New Drug) timelines by coordinating batch release timelines, comparability testing, and chain-of-custody for clinical materials. For U.S. firms, the combined CRO/CDMO model represents an attractive evolution in outsourced service.

Competitive Landscape

The U.S. CDMO market is both highly competitive and strategically consolidating. The leading players are competing based on regulatory track record, technology depth in ATMPs (advanced therapy medicinal products), ADCs, or viral vector production, new manufacturing plant expansion, and increasing ability to deliver rapid scale-up. Growing mergers and acquisitions, partnerships, and capacity expansion are reshaping the landscape, positioning integrated CDMOs as preferred long-term partners for pharma and biopharma companies seeking cost efficiency, innovation, and reliable end-to-end solutions.

Key Industry Developments:

- In September 2025, Enzene Biosciences Ltd. (Pune, India–based) opened its US$50 Mn, state-of-the-art biopharmaceutical manufacturing plant on the Princeton West Innovation Campus in Hopewell. Earlier in 2024, the company announced the construction of a 54,000 ft² continuous biomanufacturing facility in New Jersey, and launched Phase I in Q3 2024 with plans for full drug-product and formulation capabilities.

- In October 2024, Lonza announced the acquisition of Genentech’s large-scale biologics manufacturing site in Vacaville, California, from Roche for US$1.2 Bn. The acquisition led to an upgrade of the total bioreactor capacity of around 330,000 liters, significantly extending manufacturing capacity for late-stage clinical and commercial products.

- In April 2024, Fujifilm expanded its U.S. Bio CDMO capacity by investing an additional US$1.2 Bn in new large-scale bioreactor facilities in North Carolina, scheduled to begin operations in 2025.

Companies Covered in U.S. CMO/CDMO Market

- Thermo Fisher Scientific Inc.

- AGC Biologics

- Curia Global, Inc.

- LGM Pharma

- Cell Culture Company, LLC

- Ascendia Pharmaceutical Solutions

- Kindeva

- Crystal Pharmatech Co., Ltd.

- Asymchem Inc.

- Pharmaceutics International, Inc.

- Catalent, Inc.

- Cambrex Corporation

- CARBOGEN AMCIS

- Lonza

- Bora Pharmaceuticals

- BioSpring

- Quotient Sciences

- Hillgene Biopharma Co., Ltd.

- CMIC HOLDINGS Co., LTD.

- Evonik

- Novartis AG

- Piramal Pharma Limited

- CordenPharma

- Recipharm AB.

Frequently Asked Questions

The U.S. CMO/CDMO market is projected to be valued at US$83.1 Bn in 2025.

Cost efficiency, complex biologics, and advanced modality outsourcing drive the U.S. CMO/CDMO market.

The U.S. CMO/CDMO market is poised to witness a CAGR of 8.7% between 2025 and 2032.

Emerging biopharma partnerships and differentiated technologies in cell, gene, and mRNA therapies present major U.S. CDMO opportunities.

Major players in the U.S. CMO/CDMO market include Thermo Fisher Scientific Inc., AGC Biologics, Catalent, Inc., Lonza, Quotient Sciences, Evonik, and Recipharm AB.