- Healthcare Services

- Small Molecule CMO/CDMO Market

Small Molecule CMO/CDMO Market Size, Share, and Growth Forecast, 2026 - 2033

Small Molecule CMO/CDMO Market by Product Type (Active Pharmaceutical Ingredients (API), Finished Drug Products (FDP)), Drug Type (Innovators, Generics), Therapeutic Area (Oncology, Neurology/CNS), Stage Type, and Regional Analysis for 2026 - 2033

Small Molecule CMO/CDMO Market Size and Trends Analysis

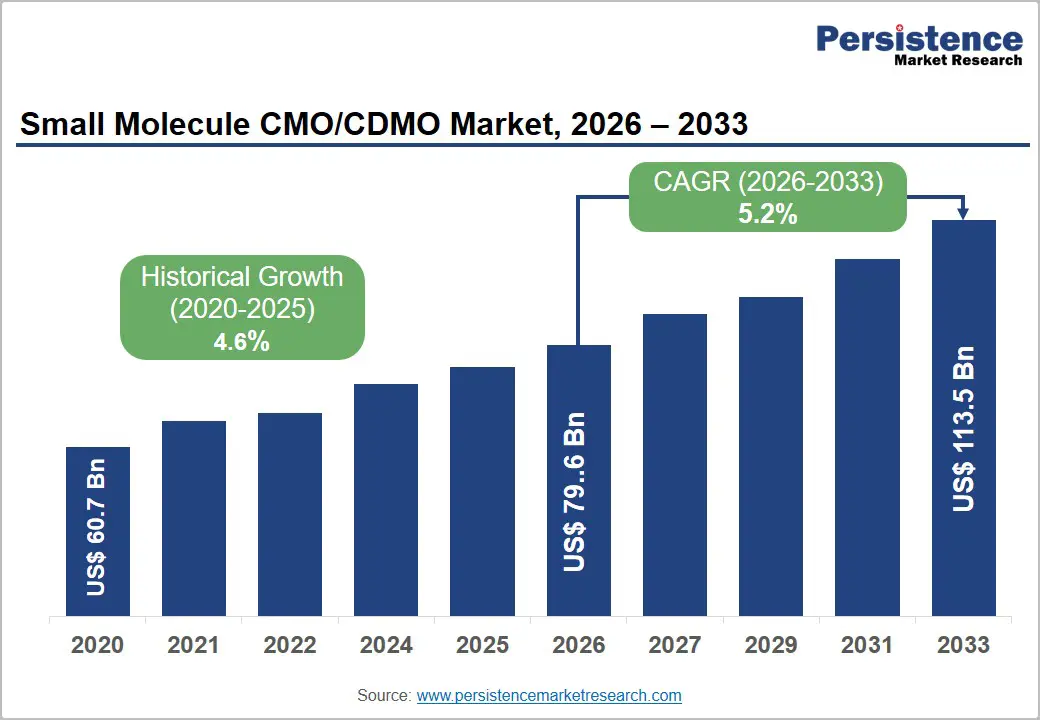

The global small molecule CMO/CDMO market size is likely to be valued at US$79.6 billion in 2026, and is expected to reach US$113.5 billion by 2033, growing at a CAGR of 5.2% during the forecast period from 2026 to 2033, driven by the pharmaceutical industry's increasing reliance on outsourcing for small molecule active pharmaceutical ingredient (API) production, formulation development, and commercial-scale manufacturing.

By partnering with specialized contract manufacturing and development organizations, pharmaceutical companies can enhance operational efficiency, reduce capital expenditure requirements, gain access to advanced technical capabilities, and accelerate product development and commercialization timelines.

Key Industry Highlights:

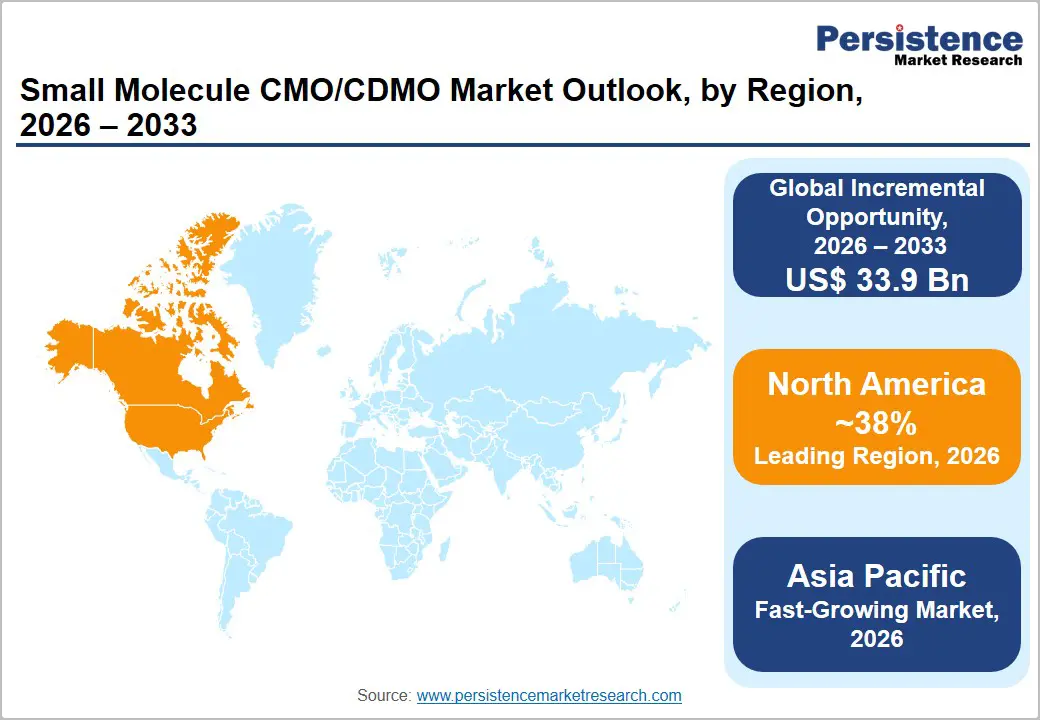

- Dominant Region: North America is expected to lead the small molecule CMO/CDMO market with approximately 38% revenue share in 2026, driven by the world's largest pharmaceutical R&D investment base, the concentrated presence of major full-service CDMO platforms including Thermo Fisher Scientific, Catalent, and Cambrex, and the FDA's established cGMP regulatory framework governing small molecule manufacturing compliance.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing regional market, driven by India and China's cost-competitive small molecule API manufacturing capabilities, expanding CDMO infrastructure investment, growing domestic pharmaceutical R&D pipelines, and increasing global pharmaceutical outsourcing to Asian manufacturing partners.

- Leading Product Type: Active pharmaceutical ingredients (API) are expected to dominate with approximately 58% share in 2026, reflecting the large commercial market for outsourced small molecule API synthesis across both innovator and generic pharmaceutical markets and the essential drug substance manufacturing role served by API CDMOs.

- Dominant Drug Type: Generic drugs are estimated to lead with approximately 55% of drug type revenue in 2026, reflecting the enormous global generic pharmaceutical market's demand for outsourced API synthesis and finished drug product manufacturing from qualified small molecule CMO partners.

- According to studies, the worldwide sales of oncology medicine are expected to reach US$470 billion by 2028, with over 40% of newly developed medications focusing on this area in 2023.

DRO Analysis

Driver - Pharmaceutical Outsourcing Model Deepening and CDMO Strategic Consolidation

The pharmaceutical industry's accelerating structural shift toward comprehensive outsourcing of small molecule manufacturing driven by the imperative to reduce capital expenditure on manufacturing infrastructure, increase operational cost flexibility, and focus internal resources on core competencies of drug discovery, clinical development, regulatory affairs, and commercial strategy is creating structural and growing demand for small molecule CDMO services that is independent of individual product cycles and represents a fundamental reorientation of pharmaceutical manufacturing operations.

The explosive growth of virtual and asset-light pharmaceutical and biotechnology company models, particularly within the innovative drug development sector where hundreds of venture capital-backed biotech companies maintain small management and scientific teams while outsourcing all manufacturing operations to CDMO partners, has created a large and commercially significant new client segment that relies entirely on small molecule CDMOs for API synthesis, clinical trial material manufacturing, and commercial supply.

Restraint - Regulatory Complexity, cGMP Compliance Burden

The small molecule CMO/CDMO market operates within one of the most stringent and continuously evolving regulatory compliance environments in manufacturing, with FDA cGMP regulations (21 CFR Parts 210/211), EMA Good Manufacturing Practice guidelines, ICH Q10 pharmaceutical quality system requirements, and national regulatory authority cGMP standards across all major pharmaceutical markets imposing comprehensive quality management, facility qualification, process validation, analytical method validation, and documentation requirements that represent significant and growing operational compliance investment for small molecule CDMO providers.

FDA warning letters, import alerts, and consent decrees directed at small molecule manufacturing facilities, particularly API manufacturing sites in India and China, create substantial market disruption for CDMOs and their pharmaceutical clients, with remediation programs potentially requiring years and significant capital investment to resolve regulatory compliance deficiencies identified during FDA surveillance or pre-approval inspections.

Opportunity- Continuous Manufacturing Technology Adoption and Process Innovation

The progressive pharmaceutical industry adoption of continuous manufacturing technology for small molecule API synthesis and drug product processing, actively promoted by the FDA's Emerging Technology Program and endorsed by the ICH Q13 continuous manufacturing guidance, represents a transformational commercial opportunity for technologically advanced small molecule CDMOs investing early in continuous flow chemistry, continuous crystallization, and continuous tablet compression capabilities that offer significant operational advantages over conventional batch manufacturing.

Flow chemistry technology for API synthesis, enabling safer handling of hazardous reaction intermediates, improved reaction selectivity, reduced solvent volumes, and streamlined process scale-up through continuous reaction parameter optimization, is gaining growing adoption among advanced small molecule CDMOs seeking to differentiate their synthesis chemistry capabilities through process technology innovation.

Category-wise Analysis

Product Type Insights

Active pharmaceutical ingredients (API) are expected to dominate product type, commanding approximately 58% of global revenue in 2026. Their market leadership reflects the API segment’s critical role in the small molecule pharmaceutical value chain, driven by high-value multi-step chemical synthesis processes and advanced technical expertise requirements.

Finished drug products (FDP) are likely to be the fastest-growing product type segment, fueled by growing demand for integrated CDMO partnerships offering end-to-end API-to-finished product manufacturing, which is driving market growth by reducing supply chain complexity and ensuring single-partner accountability.

Drug Type Insights

Generic drugs are projected to represent the dominant drug type segment, capturing approximately 55% of small molecule CMO/CDMO market revenue in 2026, due to the large global scale of generic pharmaceutical production and the heavy reliance on outsourced API synthesis and drug manufacturing by generic drug companies.

Innovator drugs are likely to be the fastest-growing drug type segment, driven by the rising pharmaceutical R&D investment, expanding small molecule drug pipelines, and increasing reliance on CDMO partnerships for clinical and commercial manufacturing.

Therapeutic Area Insights

Oncology is the dominant therapeutic area, commanding approximately 35% of small molecule CMO/CDMO market revenue in 2026. Oncology leads the market due to strong pharmaceutical investment in cancer therapeutics, creating high demand for small molecule oncology API synthesis, HPAPI manufacturing, and oncology drug formulation services through CDMO partnerships.

The neurology/CNS segment is expected to be the fastest-growing therapeutic area segment, driven by renewed pharmaceutical investment in CNS drug development and the rising global burden of neurological and psychiatric disorders, increasing demand for small molecule CNS therapies.

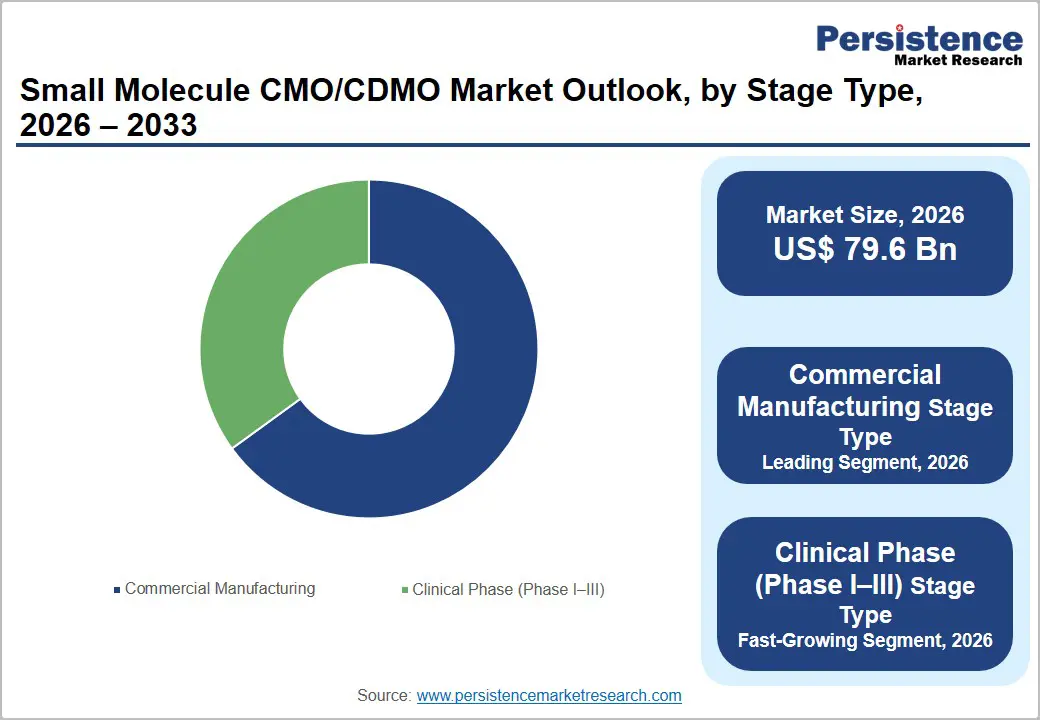

Stage Type Insights

Commercial manufacturing is expected to dominate, capturing approximately 65% of small molecule CMO/CDMO market revenue in 2026, propelled by large-scale, long-term manufacturing contracts for marketed pharmaceutical products, generating significant recurring revenue for CDMO partners.

Clinical phase manufacturing (Phase I-III) is likely to be the fastest-growing segment, driven by the expanding pharmaceutical clinical trial pipeline and increasing demand for GMP-compliant manufacturing, formulation development, and clinical supply services from CDMOs that support faster drug development.

Regional Insights

North America Small Molecule CMO/CDMO Market Trends

North America is projected to dominate the small molecule CMO/CDMO market, holding approximately 38% of the total revenue in 2026, representing the largest regional market globally. The region's market leadership reflects the U.S.'s dominant position as the global pharmaceutical and biotechnology R&D investment hub, the concentrated presence of major full-service CDMO platforms with North American principal facilities, and the FDA's well-established cGMP regulatory framework, creating strong demand for FDA-registered and inspected small molecule manufacturing partners.

U.S. Small Molecule CMO/CDMO Market Insights

The U.S. is anticipated to be the world's largest market and commanding approximately 85% of the regional market share in 2026, anchored by the country's commanding position in global pharmaceutical R&D investment, the concentrated presence of major pharmaceutical innovators including Pfizer, Bristol-Myers Squibb, AbbVie, and Eli Lilly with substantial small molecule outsourcing programs, and the well-developed U.S. CDMO ecosystem spanning full-service integrated platforms to specialized niche API synthesis providers.

Canada Small Molecule CMO/CDMO Market Insights

Canada's market is expected to hold 15% of the regional share in 2026, benefiting from the country's pharmaceutical manufacturing sector's established GMP compliance capabilities, Health Canada regulatory framework harmonized with ICH guidelines, and growing pharmaceutical and biotechnology R&D cluster development in Toronto, Montreal, and Vancouver, generating increasing small molecule clinical manufacturing outsourcing demand.

Europe Small Molecule CMO/CDMO Market Trends

Europe is estimated to be the second-largest regional small molecule CMO/CDMO market, accounting for approximately 30% of global revenue share in 2026, supported by Europe's large established pharmaceutical manufacturing infrastructure, the strong regional presence of full-service European CDMO platforms including Lonza, Recipharm, Siegfried Holding, and Euroapi, and the substantial small molecule outsourcing demand from major European pharmaceutical innovators including Roche, Novartis, AstraZeneca, Sanofi, and Bayer.

U.K. Small Molecule CMO/CDMO Market Trends

The U.K. is likely to be the leading Europe market, accounting for approximately 30% of regional revenue share in 2026, driven by the country's strong pharmaceutical manufacturing heritage, the MHRA's rigorous GMP inspection program maintaining high manufacturing quality standards, and significant outsourcing demand from major U.K.-associated pharmaceutical companies including AstraZeneca and GlaxoSmithKline.

Germany Small Molecule CMO/CDMO Market Trends

Germany is expected to lead with over 20% of the regional market share in 2026, supported by the country's world-class chemical synthesis and pharmaceutical manufacturing heritage, the headquarters presence of major German pharmaceutical companies generating substantial outsourcing demand, and Germany's strong fine chemicals and specialty synthesis manufacturing ecosystem. Euroapi, formed from Sanofi's API manufacturing business, maintains significant European API manufacturing operations, including German-based synthesis capabilities serving global pharmaceutical clients.

Asia Pacific Small Molecule CMO/CDMO Market Trends

Asia Pacific is likely to be the fastest-growing regional market, powered by India's dominant global position in generic API manufacturing, China's rapidly expanding integrated CDMO capabilities through WuXi AppTec and domestic competitors, growing domestic pharmaceutical R&D investment generating new CDMO service demand, and the pharmaceutical industry's sustained use of cost-competitive Asian manufacturing partners for both API synthesis and drug product manufacturing.

China Small Molecule CMO/CDMO Market Trends

China is expected to dominate the Asia Pacific market, commanding a 35% share in 2026, led by major players such as WuXi AppTec, Asymchem, Pharmaron, and ChemPartner. Growth is supported by integrated API manufacturing, drug development services, and strong global pharmaceutical partnerships. China's NMPA regulatory authority's progressive ICH harmonization is improving the international acceptance of Chinese CDMO-manufactured API and drug product data in global regulatory submissions, supporting Chinese CDMO market expansion beyond domestic pharmaceutical clients into regulated global pharmaceutical outsourcing markets.

India Small Molecule CMO/CDMO Market Trends

India is expected to hold 25% of the regional market share in 2026, and it represents the world's dominant generic API manufacturing hub and a critically important small molecule CMO market, with the country's established pharmaceutical manufacturing ecosystem encompassing hundreds of U.S. FDA and EMA-approved API and finished product manufacturing facilities providing cost-competitive, quality-compliant small molecule manufacturing services to global pharmaceutical markets.

Competitive Landscape

The global small molecule CMO/CDMO market is characterized by a competitive landscape ranging from large, fully integrated global CDMO platforms with comprehensive API-to-drug product manufacturing capabilities across multi-regional facility networks to specialized regional CMOs with focused API synthesis, process development, or drug product manufacturing expertise serving specific pharmaceutical market segments.

Lonza Group occupies a pre-eminent position among global integrated small molecule CDMOs through its comprehensive chemical synthesis, API manufacturing, and drug product capabilities delivered across its global manufacturing network in North America, Europe, and Asia. Thermo Fisher Scientific's Pharma Services Group, operating the Patheon CDMO platform across more than 30 manufacturing sites globally, offers end-to-end small molecule development-to-commercial manufacturing services under a single preferred partner framework increasingly adopted by major pharmaceutical innovators.

Key Industry Developments:

- In October 2024, Symbiosis Pharmaceutical Services invested US$1.57 million in a new manufacturing facility at Castle Business Park in Stirling, Scotland, doubling the local CMO's production capacity.

- In September 2024, SK Pharmteco planned to build a US$260 million small molecule and peptide production facility in Sejong, South Korea, employing 300+ people and broadening its manufacturing network.

Companies Covered in Small Molecule CMO/CDMO Market

- Lonza

- Thermo Fisher Scientific

- Catalent

- WuXi AppTec

- Piramal Pharma Solutions

- Cambrex

- Recipharm

- Siegfried Holding

- Euroapi

Frequently Asked Questions

The global small molecule CMO/CDMO market is projected to reach US$79.6 billion in 2026.

Growing pharmaceutical outsourcing and the rise of virtual biotech companies are driving strong demand for small molecule CDMO services for API synthesis, clinical manufacturing, and commercial supply.

The small molecule CMO/CDMO market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Adoption of continuous manufacturing and flow chemistry technologies is creating growth opportunities for advanced small molecule CDMOs through improved efficiency, safety, and process innovation.

Key players include Lonza, Thermo Fisher Scientific, Catalent, WuXi AppTec, Piramal Pharma Solutions, Cambrex, Recipharm, Siegfried Holding, and Euroapi.