- Medical Devices

- Cardiovascular Stents Market

Cardiovascular Stents Market Size, Share, and Growth Forecast 2026 – 2033

Cardiovascular Stents Market by Product Type (Coronary Stents, Peripheral Vascular Stents, Carotid Artery Stents, Aortic Stent Grafts – EVAR/TEVAR, Others), Stent Type (Drug-Eluting Stents, Bare-Metal Stents, Bioresorbable/Bioabsorbable Stents, Dual-Therapy Stents, Covered Stents/Stent Grafts), Coating Technology (Polymer-Based Coatings, Polymer-Free Coatings, Bioactive Coatings, Antithrombotic Coatings), Mode of Delivery (Balloon-Expandable Stents, Self-Expanding Stents), End- User (Hospitals, Cardiac Catheterization Laboratories, Ambulatory Surgical Centers, Specialty Cardiology Centers), and Regional Analysis, 2026–2033

Cardiovascular Stents Market Size and Trend Analysis

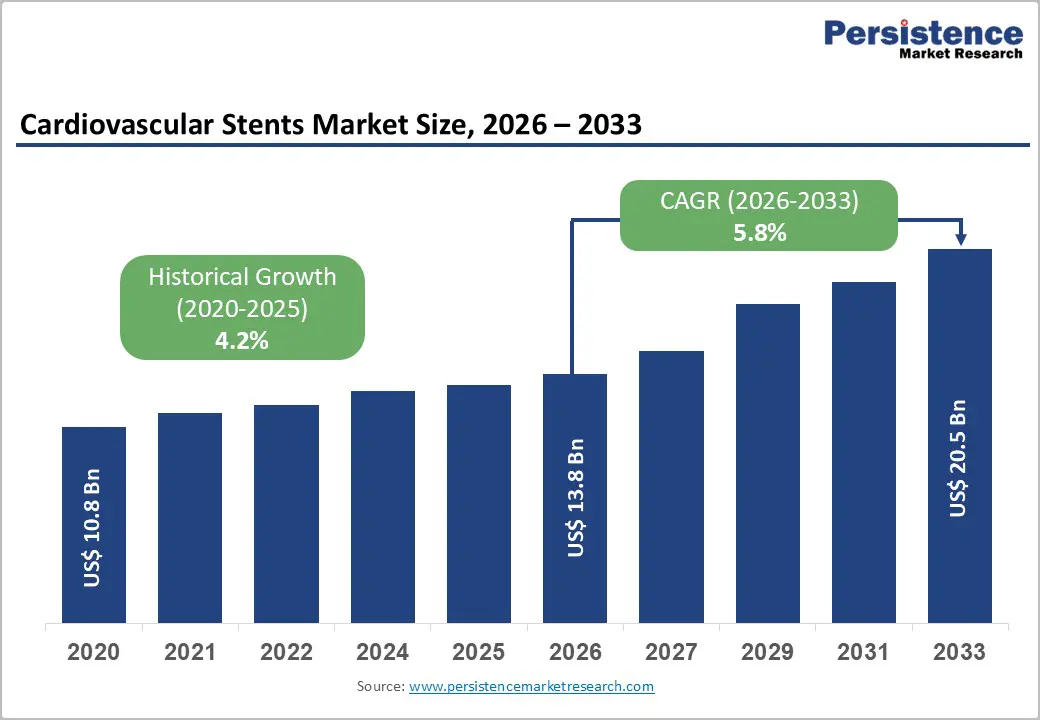

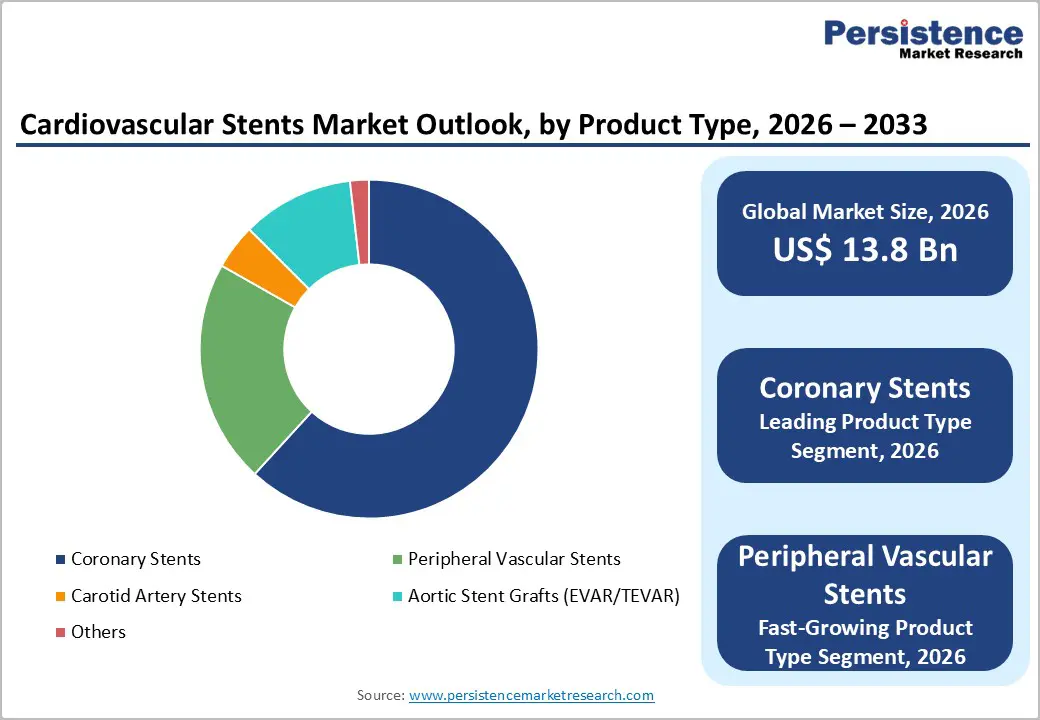

The global cardiovascular stents market size is expected to be valued at US$ 13.8 billion in 2026 and projected to reach US$ 20.5 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033. It is expanding and driven by a rise in global burden of cardiovascular disease the leading cause of mortality worldwide, expanding procedural access in Asia Pacific and Latin America, and continuous innovation in drug-eluting stent (DES) platforms with polymer-free and bioresorbable coating technologies. The World Heart Federation (WHF) estimates that cardiovascular disease causes over 20 million deaths annually, with coronary artery disease accounting for the majority, generating relentless demand for percutaneous coronary intervention (PCI) and peripheral vascular procedures. Simultaneously, the aging global population, the rising tide of metabolic risk factors including obesity, diabetes, and hypertension, and improving catheterization laboratory infrastructure across emerging markets are collectively amplifying the global stent procedure volume pipeline.

Key Market Highlights

- Leading Region – North America: North America commanded approximately 47% of global cardiovascular stents market share in 2025, driven by 720,000 annual U.S. PCI procedures, CMS DRG reimbursement stability, and Abbott, Boston Scientific, Medtronic product leadership under FDA PMA-validated DES platforms.

- Fastest Growing Market– Asia Pacific: Asia Pacific is fast-growing, driven by China's 2 million+ annual PCIs, MicroPort/Lepu Medical domestic DES, India's PM-JAY cardiac access expansion, and Japan MHLW reimbursement for ultrathin DES/IVUS-guided PCI.

- Dominant Segment – Coronary Stents: Coronary stents held approximately 62% market share in 2025, anchored by DES representing 90%+ of coronary implantations globally, ESC/ACC Class I DES endorsement, and Abbott XIENCE®/Boston Scientific SYNERGY™ platform dominance.

- Fastest Growing Segment – Peripheral Vascular Stents: Peripheral vascular stents are fastest-growing, targeting 200 million+ global PAD patients per SVS, with Boston Scientific Eluvia™ Asia Pacific launch, Shockwave Medical IVL adjunct adoption, and EVAR/TEVAR procedural volume growth driving market expansion.

- Key Opportunity – Asia Pacific CVD Surge: China's 2M+ annual PCIs, India's PM-JAY 500M+ beneficiaries, and Japan's premium DES reimbursement collectively represent a high-growth demand corridor making Asia Pacific the key battleground for capturing the US$ 6.7 billion incremental market opportunity.

Market Dynamics

Drivers – Rise in Global Cardiovascular Disease Burden Driving Unprecedented PCI Procedure Volumes

Cardiovascular disease (CVD) remains the world's leading cause of death, generating an enormous and growing procedural demand base for coronary and peripheral stents. The World Health Organization (WHO) estimates that CVD accounts for approximately 32% of all global deaths, with ischemic heart disease responsible for over 9 million deaths annually. The American Heart Association (AHA) 2024 Heart Disease and Stroke Statistics Update reports that approximately 720,000 percutaneous coronary interventions (PCIs) are performed annually in the U.S. alone. The European Society of Cardiology (ESC) has documented growing PCI volumes across Europe, with drug-eluting stents now representing over 90% of coronary stent implantations in all major markets, generating high-value per-procedure stent revenue from Abbott's XIENCE® series, Boston Scientific's SYNERGY™, and Medtronic's Resolute Onyx™.

Aging Global Population and Rising Metabolic Risk Factors Expanding Peripheral Vascular Stent Demand

The global aging demographic combined with escalating metabolic risk factor burdens including obesity, type 2 diabetes, and hypertension is generating structural growth in peripheral artery disease (PAD) and lower extremity vascular disease requiring peripheral vascular stent interventions. The Society for Vascular Surgery (SVS) estimates that PAD affects over 200 million people globally, with prevalence rising steeply in aging populations. Diabetic peripheral arterial disease is a particular driver, with the International Diabetes Federation (IDF) projecting 783 million people with diabetes by 2045. The expansion of endovascular aneurysm repair (EVAR) and transcatheter endovascular thoracic aortic repair (TEVAR) as minimally invasive alternatives to open surgery is further driving aortic stent graft adoption, with Medtronic's Endurant™ and Cook Medical's Zenith® series experiencing growing procedural volumes.

Restraints - In-Stent Restenosis and Late Stent Thrombosis Risks Constraining DES Adoption in Certain Populations

Despite substantial advances in drug-eluting stent technology, in-stent restenosis (ISR) and late stent thrombosis remain clinically significant concerns that constrain stent adoption in specific high-risk patient subgroups. Published data in JACC: Cardiovascular Interventions indicates that ISR occurs in 5–10% of DES cases at one year, requiring repeat revascularization. The mandatory requirement for dual antiplatelet therapy (DAPT) following DES implantation typically 6–12 months duration creates bleeding risk complications in elderly and anticoagulated patients, influencing physician preference for shorter-DAPT alternatives and limiting stent adoption in specific patient populations.

Stringent FDA and CE MDR Regulatory Pathways Increasing Device Approval Timelines and Costs

The global cardiovascular stent market faces significant regulatory headwinds from increasingly stringent device approval requirements. The implementation of EU MDR 2017/745 has substantially extended European market access timelines and increased clinical data requirements for stent approval with notified body certification costs rising significantly. In the U.S., FDA PMA (Premarket Approval) pathways for novel DES platforms require extensive randomized clinical trial data, extending development-to-market timelines by 3–5 years and limiting the speed at which innovative stent platforms can reach physicians and patients globally.

Opportunities - Peripheral Vascular Stents: Fastest-Growing Product Segment Driven by PAD and Endovascular Expansion

Peripheral vascular stents represent the fastest-growing product type within the cardiovascular stents market, driven by the 200 million+ global PAD patients, expanding endovascular treatment adoption over open vascular surgery, and growing EVAR and TEVAR procedure volumes for aortic aneurysm management.

The Society for Vascular Surgery (SVS) clinical practice guidelines increasingly endorse endovascular-first strategies for iliac, femoropopliteal, and infrapopliteal disease, driving stent procedure volumes. Next-generation drug-coated balloon (DCB) and drug-eluting peripheral stent systems including Medtronic's IN.PACT Admiral® and Boston Scientific's Eluvia™ have demonstrated superior outcomes versus bare peripheral stents in the femoropopliteal segment. Shockwave Medical's intravascular lithotripsy (IVL) technology, used in conjunction with peripheral stenting for heavily calcified lesions, is creating new adjunctive procedural revenue opportunities in a previously difficult-to-treat patient population.

Asia Pacific: Fastest-Growing Regional Market Powered by Healthcare Infrastructure Investment and CVD Surge

Asia Pacific represents the most significant geographic growth opportunity for cardiovascular stent manufacturers, driven by an escalating cardiovascular disease burden, rapidly expanding catheterization laboratory infrastructure, and growing procedural reimbursement across China, India, Japan, and Southeast Asia.

China conducts over 2 million PCIs annually, per Chinese Society of Cardiology (CSC) data, the second-highest volume globally after the U.S., with domestic manufacturers including MicroPort Scientific Corporation and Lepu Medical Technology gaining significant market share through NMPA-approved DES platforms. India's Ayushman Bharat PM-JAY scheme is expanding access to cardiac interventions for 500+ million beneficiaries, while Japan's MHLW reimbursement for next-generation bioresorbable scaffold and polymer-free DES technologies is driving premium stent adoption at Japanese tertiary cardiac centers.

Category-wise Analysis

Product Type Insights

Coronary stents dominated the cardiovascular stents market, commanding approximately 62% of the total share in 2026. The market leadership of coronary stents directly reflects the global prevalence of coronary artery disease (CAD) as the most common manifestation of cardiovascular disease, requiring percutaneous coronary intervention (PCI) with stent implantation as the standard revascularization procedure. The AHA 2024 Statistics Update documents approximately 720,000 annual PCI procedures in the U.S., each typically implanting 1–2 coronary stents per procedure.

The ESC/EACTS Guidelines on Myocardial Revascularization classify DES as a Class I recommendation for virtually all PCI indications, ensuring consistent high-volume stent implantation by interventional cardiologists globally. Abbott's XIENCE® Skypoint and Boston Scientific's SYNERGY™ EES platforms maintain leading coronary DES market positions across North America, Europe, and the Asia Pacific.

Stent Type Insights

Drug-eluting stents (DES) dominated the stent type segment, representing approximately 78% of total cardiovascular stent market revenue in 2026. DES's overwhelming market leadership reflects its clinical superiority over bare-metal stents (BMS) in reducing in-stent restenosis rates, with landmark trials including SPIRIT and ENDEAVOR demonstrating a 50–70% reduction in TVR (target vessel revascularization) compared to BMS.

The ESC and ACC/AHA guidelines endorse DES as the preferred stent in virtually all elective PCI scenarios, and their usage now exceeds 90% of all coronary stent implantations in developed markets. Current generation DES platforms featuring ultrathin strut designs (60–80 µm), biodegradable polymer coatings, and highly lipophilic antiproliferative drugs (everolimus, zotarolimus) have further reduced procedural complications, reinforcing DES market dominance.

End-user Insights

Hospitals constituted the dominant end-user segment of the cardiovascular stents market, accounting for approximately 67% of total end-user demand in 2025. Hospital-based cardiac catheterization laboratories (cath labs) are the primary setting for coronary and peripheral vascular stent implantation procedures, requiring integrated cath lab infrastructure, cardiac surgery backup, intensive care capability, and specialist interventional cardiology or vascular surgery teams that are almost exclusively concentrated in hospital settings.

Joint Commission-certified Chest Pain Centers and Primary PCI centers in the U.S. and ESC-accredited Stent for Life initiative centers in Europe mandate 24/7 PCI capability, sustaining hospital-based stent procedure volumes. CMS reimbursement for PCI procedures under DRG coding provides predictable hospital revenue for stent-based revascularization, reinforcing their dominant market position.

Regional Insights

North America Cardiovascular Stents Market Trends and Insights

North America accounted for approximately 46.8% of the global cardiovascular stents market in 2026, supported by high percutaneous coronary intervention (PCI) volumes, widespread adoption of premium drug-eluting stents, and strong reimbursement coverage across public and private healthcare systems. The region benefits from robust clinical guideline implementation, extensive catheterization laboratory networks, and continuous innovation from leading manufacturers such as Abbott Laboratories, Boston Scientific Corporation, and Medtronic plc. Increasing use of intravascular imaging and calcium-modification technologies is further supporting demand for complex coronary and peripheral stent procedures.

U.S. Cardiovascular Stents Market Trends and Insights

The U.S. represented nearly 88.4% of the North American market in 2025, equivalent to about 41.4% of global revenue. More than 700,000 PCI procedures are performed annually, supported by stable reimbursement from the Centers for Medicare & Medicaid Services and strong adoption of next-generation ultrathin-strut DES and aortic stent graft systems across high-volume cardiac centers.

Canada Cardiovascular Stents Market Trends and Insights

Canada accounted for an estimated 8.7% of the regional market in 2026 and is projected to expand at a CAGR of 6.3% through 2033. Growth is supported by provincial cardiac care programs, increasing use of minimally invasive endovascular aneurysm repair, and expanding coronary intervention capacity in tertiary hospitals across Ontario, Quebec, and British Columbia.

Europe Cardiovascular Stents Market Trends and Insights

Europe captured approximately 27.6% of the global cardiovascular stents market in 2026, driven by broad access to primary PCI, strong compliance with European Society of Cardiology guidelines, and continued uptake of polymer-free and ultrathin-strut DES technologies. The region maintains a mature interventional cardiology ecosystem supported by universal healthcare systems and active clinical research. Regulatory oversight under EU MDR is reinforcing product quality and accelerating the adoption of evidence-backed stent platforms in both coronary and peripheral applications.

Germany Cardiovascular Stents Market Trends and Insights

Germany contributed approximately 23.8% of the European market in 2026, representing around 6.6% of global revenue. The country performs over 300,000 PCI procedures annually and remains Europe’s largest cardiovascular stent market due to comprehensive statutory insurance coverage and strong demand for advanced coronary and peripheral stent systems.

United Kingdom Cardiovascular Stents Market Trends and Insights

UK held close to 14.9% of the regional market in 2026, and is expected to reach a CAGR of 5.8% by 2033. Market expansion is supported by NHS England cardiac service investments and increasing use of DES and endovascular stent grafts in tertiary referral centers.

Asia Pacific Cardiovascular Stents Market Trends and Insights

Asia Pacific accounted for approximately 19.9% of the global cardiovascular stents market in 2026 and is projected to register the fastest CAGR of 8.9%. Growth is fueled by rising coronary artery disease prevalence, rapid expansion of catheterization laboratories, and increasing adoption of domestically manufactured drug-eluting stents. Government-supported insurance programs and healthcare infrastructure investments are improving access to PCI and peripheral vascular interventions across both developed and emerging economies.

China Cardiovascular Stents Market Trends and Insights

China represented nearly 46.7% of the Asia Pacific market in 2026, equivalent to approximately 9.3% of global revenue. With more than two million PCI procedures annually, the country benefits from large-scale adoption of competitively priced DES manufactured by domestic leaders such as MicroPort Scientific Corporation and Lepu Medical Technology.

India Cardiovascular Stents Market Trends and Insights

India accounted for about 17.5% of the regional market in 2026 and is forecast to reach a CAGR of 10.8% through 2033. Rising intervention volumes in major hospital networks and broader reimbursement under Ayushman Bharat are accelerating adoption of coronary and peripheral stent technologies across both metropolitan and tier-2 cities.

Competitive Landscape

The global cardiovascular stents market is moderately consolidated, with Abbott Laboratories, Boston Scientific Corporation, Medtronic plc, and BIOTRONIK SE & Co. KG commanding dominant positions through their respective DES and peripheral stent portfolios. Key competitive differentiators include ultrathin strut design (≤60 µm), biodegradable polymer coating technology, IVUS/OCT compatibility, and chronic total occlusion (CTO) PCI specialty platforms. MicroPort Scientific and Lepu Medical are gaining global share through competitive pricing. Emerging trends include AI-assisted PCI planning software integration, bioresorbable scaffold platform reinvestment by Abbott and Elixir Medical, and drug-coated balloon (DCB) combinations with stenting for in-stent restenosis treatment.

Key Developments:

- In January 2025, Bentley launched two additional products at the Leipzig Interventional Course, namely, the BeGraft stent graft system and the BeFlared Fenestrated Endovascular Aneurysm Repair (FEVAR) stent graft system. BeGraft is considered the world's first on-label bridging device, while BeFlared is the first dedicated indicated bridging stent for FEVAR procedures.

- In May 2024, Abbott introduced an everolimus-eluting coronary stent system called XIENCE Sierra in India. The launch came after the system bagged regulatory approval from the Central Drugs Standard Control Organization (CDSCO).

Global Cardiovascular Stents Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 10.8 Bn |

|

Current Market Value (2026) |

US$ 13.8 Bn |

|

Projected Market Value (2033) |

US$ 20.5 Bn |

|

CAGR (2026-2033) |

5.8% |

|

Leading Region |

North America, 46% share |

|

Dominant Stent Type |

Drug-Eluting Stents (DES), 76.50% share |

|

Top-ranking Product Type |

Coronary Stents, 61.8% |

|

Incremental Opportunity |

US$ 2.0 Bn |

Companies Covered in Cardiovascular Stents Market

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- BIOTRONIK SE & Co. KG

- Terumo Corporation

- MicroPort Scientific Corporation

- B. Braun SE

- Cordis

- Becton, Dickinson and Company

- Cook Medical

- Johnson & Johnson Services, Inc.

- Stryker Corporation

- Merit Medical Systems, Inc.

- Lepu Medical Technology (Beijing) Co., Ltd.

- Shockwave Medical, Inc.

- Others

Frequently Asked Questions

The global cardiovascular stents market is expected to be valued at US$ 13.8 billion in 2026, growing from US$ 10.8 billion in 2020, and projected to reach US$ 20.5 billion by 2033 at a forecast CAGR of 5.8%.

Rising prevalence of coronary and peripheral artery diseases, increasing aging population, growing volumes of minimally invasive PCI and endovascular procedures, and continued adoption of advanced drug-eluting stent technologies.

North America leads with approximately 47% global market share in 2025, supported by 720,000+ annual U.S. PCI procedures, CMS DRG reimbursement for stent procedures, FDA PMA-validated XIENCE®, SYNERGY™, and Resolute Onyx™ DES platforms, and SCAI/ACC guideline-mandated Primary PCI center infrastructure.

Expansion in emerging markets, rapid adoption of bioresorbable and polymer-free stents, increasing use of aortic and peripheral stent grafts, and integration of imaging-guided and AI-assisted interventional cardiology solutions.

Leading companies include Abbott Laboratories (XIENCE®), Boston Scientific Corporation (SYNERGY™/Eluvia™), Medtronic plc (Resolute Onyx™/Endurant™), BIOTRONIK SE & Co. KG (Orsiro Mission®), Terumo Corporation, MicroPort Scientific, Lepu Medical Technology, and Shockwave Medical, competing through ultrathin strut design, polymer-free coating technology, and peripheral vascular DES platforms.