- Executive Summary

- Global Trace Oxygen Analyzer Market Snapshot 2025 and 2032

- Market Opportunity Assessment, 2025 - 2032, US$ Mn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Chemical Industry Overview

- Global Pharmaceutical Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2019 - 2032

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Trace Oxygen Analyzer Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Global Trace Oxygen Analyzer Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Units) Analysis by Product Type, 2019-2024

- Current Market Size (US$ Mn) and Volume (Units) Forecast, by Product Type, 2025 - 2032

- Process Analyzers

- Portable Analyzers

- Benchtop Analyzers

- Rack-Mounted Systems

- Market Attractiveness Analysis: Product Type

- Global Trace Oxygen Analyzer Market Outlook: Measurement Range

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Units) Analysis by Measurement Range, 2019-2024

- Current Market Size (US$ Mn) and Volume (Units) Forecast, by Measurement Range, 2025 - 2032

- Parts-per-Billion (ppb) Range Analyzers

- Parts-per-Million (ppm) Range Analyzers

- Percent-Level Range Analyzers

- Market Attractiveness Analysis: Measurement Range

- Global Trace Oxygen Analyzer Market Outlook: Technology

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Units) Analysis by Technology, 2019-2024

- Current Market Size (US$ Mn) and Volume (Units) Forecast, by Technology, 2025 - 2032

- Electrochemical Sensors

- Zirconia Sensors

- Paramagnetic Sensors

- Fluorescence Quenching Sensors

- Coulometric Sensors

- Mass Spectrometry-based Analyzers

- Market Attractiveness Analysis: Technology

- Global Trace Oxygen Analyzer Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Units) Analysis by Application, 2019-2024

- Current Market Size (US$ Mn) and Volume (Units) Forecast, by Application, 2025 - 2032

- Semiconductor & Electronics Manufacturing

- Pharmaceutical & Biotechnology

- Food & Beverage Industry

- Chemical & Petrochemical

- Industrial Gases & Gas Purity Monitoring

- Healthcare & Medical Applications

- Research & Laboratories

- Market Attractiveness Analysis: Application

- Global Trace Oxygen Analyzer Market Outlook: End User

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Units) Analysis by End User, 2019-2024

- Current Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2025 - 2032

- Industrial Process Operators

- Research Laboratories & Institutions

- OEMs (Original Equipment Manufacturers)

- System Integrators

- Calibration & Service Providers

- Market Attractiveness Analysis: End User

- Global Trace Oxygen Analyzer Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) and Volume (Units) Analysis by Region, 2019-2024

- Current Market Size (US$ Mn) and Volume (Units) Forecast, by Region, 2025 - 2032

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Trace Oxygen Analyzer Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2025 - 2032

- U.S.

- Canada

- North America Market Size (US$ Mn) and Volume (Units) Forecast, by Product Type, 2025 - 2032

- Process Analyzers

- Portable Analyzers

- Benchtop Analyzers

- Rack-Mounted Systems

- North America Market Size (US$ Mn) and Volume (Units) Forecast, by Measurement Range, 2025 - 2032

- Parts-per-Billion (ppb) Range Analyzers

- Parts-per-Million (ppm) Range Analyzers

- Percent-Level Range Analyzers

- North America Market Size (US$ Mn) and Volume (Units) Forecast, by Technology, 2025 - 2032

- Electrochemical Sensors

- Zirconia Sensors

- Paramagnetic Sensors

- Fluorescence Quenching Sensors

- Coulometric Sensors

- Mass Spectrometry-based Analyzers

- North America Market Size (US$ Mn) and Volume (Units) Forecast, by Application, 2025 - 2032

- Semiconductor & Electronics Manufacturing

- Pharmaceutical & Biotechnology

- Food & Beverage Industry

- Chemical & Petrochemical

- Industrial Gases & Gas Purity Monitoring

- Healthcare & Medical Applications

- Research & Laboratories

- North America Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2025 - 2032

- Industrial Process Operators

- Research Laboratories & Institutions

- OEMs (Original Equipment Manufacturers)

- System Integrators

- Calibration & Service Providers

- Europe Trace Oxygen Analyzer Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2025 - 2032

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Mn) and Volume (Units) Forecast, by Product Type, 2025 - 2032

- Process Analyzers

- Portable Analyzers

- Benchtop Analyzers

- Rack-Mounted Systems

- Europe Market Size (US$ Mn) and Volume (Units) Forecast, by Measurement Range, 2025 - 2032

- Parts-per-Billion (ppb) Range Analyzers

- Parts-per-Million (ppm) Range Analyzers

- Percent-Level Range Analyzers

- Europe Market Size (US$ Mn) and Volume (Units) Forecast, by Technology, 2025 - 2032

- Electrochemical Sensors

- Zirconia Sensors

- Paramagnetic Sensors

- Fluorescence Quenching Sensors

- Coulometric Sensors

- Mass Spectrometry-based Analyzers

- Europe Market Size (US$ Mn) and Volume (Units) Forecast, by Application, 2025 - 2032

- Semiconductor & Electronics Manufacturing

- Pharmaceutical & Biotechnology

- Food & Beverage Industry

- Chemical & Petrochemical

- Industrial Gases & Gas Purity Monitoring

- Healthcare & Medical Applications

- Research & Laboratories

- Europe Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2025 - 2032

- Industrial Process Operators

- Research Laboratories & Institutions

- OEMs (Original Equipment Manufacturers)

- System Integrators

- Calibration & Service Providers

- East Asia Trace Oxygen Analyzer Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2025 - 2032

- China

- Japan

- South Korea

- East Asia Market Size (US$ Mn) and Volume (Units) Forecast, by Product Type, 2025 - 2032

- Process Analyzers

- Portable Analyzers

- Benchtop Analyzers

- Rack-Mounted Systems

- East Asia Market Size (US$ Mn) and Volume (Units) Forecast, by Measurement Range, 2025 - 2032

- Parts-per-Billion (ppb) Range Analyzers

- Parts-per-Million (ppm) Range Analyzers

- Percent-Level Range Analyzers

- East Asia Market Size (US$ Mn) and Volume (Units) Forecast, by Technology, 2025 - 2032

- Electrochemical Sensors

- Zirconia Sensors

- Paramagnetic Sensors

- Fluorescence Quenching Sensors

- Coulometric Sensors

- Mass Spectrometry-based Analyzers

- East Asia Market Size (US$ Mn) and Volume (Units) Forecast, by Application, 2025 - 2032

- Semiconductor & Electronics Manufacturing

- Pharmaceutical & Biotechnology

- Food & Beverage Industry

- Chemical & Petrochemical

- Industrial Gases & Gas Purity Monitoring

- Healthcare & Medical Applications

- Research & Laboratories

- East Asia Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2025 - 2032

- Industrial Process Operators

- Research Laboratories & Institutions

- OEMs (Original Equipment Manufacturers)

- System Integrators

- Calibration & Service Providers

- South Asia & Oceania Trace Oxygen Analyzer Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2025 - 2032

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Mn) and Volume (Units) Forecast, by Product Type, 2025 - 2032

- Process Analyzers

- Portable Analyzers

- Benchtop Analyzers

- Rack-Mounted Systems

- South Asia & Oceania Market Size (US$ Mn) and Volume (Units) Forecast, by Measurement Range, 2025 - 2032

- Parts-per-Billion (ppb) Range Analyzers

- Parts-per-Million (ppm) Range Analyzers

- Percent-Level Range Analyzers

- South Asia & Oceania Market Size (US$ Mn) and Volume (Units) Forecast, by Technology, 2025 - 2032

- Electrochemical Sensors

- Zirconia Sensors

- Paramagnetic Sensors

- Fluorescence Quenching Sensors

- Coulometric Sensors

- Mass Spectrometry-based Analyzers

- South Asia & Oceania Market Size (US$ Mn) and Volume (Units) Forecast, by Application, 2025 - 2032

- Semiconductor & Electronics Manufacturing

- Pharmaceutical & Biotechnology

- Food & Beverage Industry

- Chemical & Petrochemical

- Industrial Gases & Gas Purity Monitoring

- Healthcare & Medical Applications

- Research & Laboratories

- South Asia & Oceania Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2025 - 2032

- Industrial Process Operators

- Research Laboratories & Institutions

- OEMs (Original Equipment Manufacturers)

- System Integrators

- Calibration & Service Providers

- Latin America Trace Oxygen Analyzer Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2025 - 2032

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Mn) and Volume (Units) Forecast, by Product Type, 2025 - 2032

- Process Analyzers

- Portable Analyzers

- Benchtop Analyzers

- Rack-Mounted Systems

- Latin America Market Size (US$ Mn) and Volume (Units) Forecast, by Measurement Range, 2025 - 2032

- Parts-per-Billion (ppb) Range Analyzers

- Parts-per-Million (ppm) Range Analyzers

- Percent-Level Range Analyzers

- Latin America Market Size (US$ Mn) and Volume (Units) Forecast, by Technology, 2025 - 2032

- Electrochemical Sensors

- Zirconia Sensors

- Paramagnetic Sensors

- Fluorescence Quenching Sensors

- Coulometric Sensors

- Mass Spectrometry-based Analyzers

- Latin America Market Size (US$ Mn) and Volume (Units) Forecast, by Application, 2025 - 2032

- Semiconductor & Electronics Manufacturing

- Pharmaceutical & Biotechnology

- Food & Beverage Industry

- Chemical & Petrochemical

- Industrial Gases & Gas Purity Monitoring

- Healthcare & Medical Applications

- Research & Laboratories

- Latin America Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2025 - 2032

- Industrial Process Operators

- Research Laboratories & Institutions

- OEMs (Original Equipment Manufacturers)

- System Integrators

- Calibration & Service Providers

- Middle East & Africa Trace Oxygen Analyzer Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2025 - 2032

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Mn) and Volume (Units) Forecast, by Product Type, 2025 - 2032

- Process Analyzers

- Portable Analyzers

- Benchtop Analyzers

- Rack-Mounted Systems

- Middle East & Africa Market Size (US$ Mn) and Volume (Units) Forecast, by Measurement Range, 2025 - 2032

- Parts-per-Billion (ppb) Range Analyzers

- Parts-per-Million (ppm) Range Analyzers

- Percent-Level Range Analyzers

- Middle East & Africa Market Size (US$ Mn) and Volume (Units) Forecast, by Technology, 2025 - 2032

- Electrochemical Sensors

- Zirconia Sensors

- Paramagnetic Sensors

- Fluorescence Quenching Sensors

- Coulometric Sensors

- Mass Spectrometry-based Analyzers

- Middle East & Africa Market Size (US$ Mn) and Volume (Units) Forecast, by Application, 2025 - 2032

- Semiconductor & Electronics Manufacturing

- Pharmaceutical & Biotechnology

- Food & Beverage Industry

- Chemical & Petrochemical

- Industrial Gases & Gas Purity Monitoring

- Healthcare & Medical Applications

- Research & Laboratories

- Middle East & Africa Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2025 - 2032

- Industrial Process Operators

- Research Laboratories & Institutions

- OEMs (Original Equipment Manufacturers)

- System Integrators

- Calibration & Service Providers

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Emerson Electric Co

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Nova Analytical Systems

- Advanced Micro Instruments Inc

- Thermo Fisher Scientific

- Setra Systems

- Parker Hannifin

- Siemens

- ABB

- Ametek

- Honeywell

- Endress+Hauser

- Metrohm

- Yokogawa Electric Corporation

- Teledyne Technologies Incorporated

- Horiba, Ltd

- Emerson Electric Co

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Industrial Machinery

- Trace Oxygen Analyzer Market

Trace Oxygen Analyzer Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Trace Oxygen Analyzer Market by Product Type (Process Analyzers, Portable Analyzers, Benchtop Analyzers, Rack-Mounted System), Measurement Range (Parts-per-Billion (ppb) Range Analyzers, Parts-per-Million (ppm) Range Analyzers, Percent-Level Range Analyzers, Technology, Application, End-user, Regional Analysis, 2025 - 2032

Key Market Highlights:

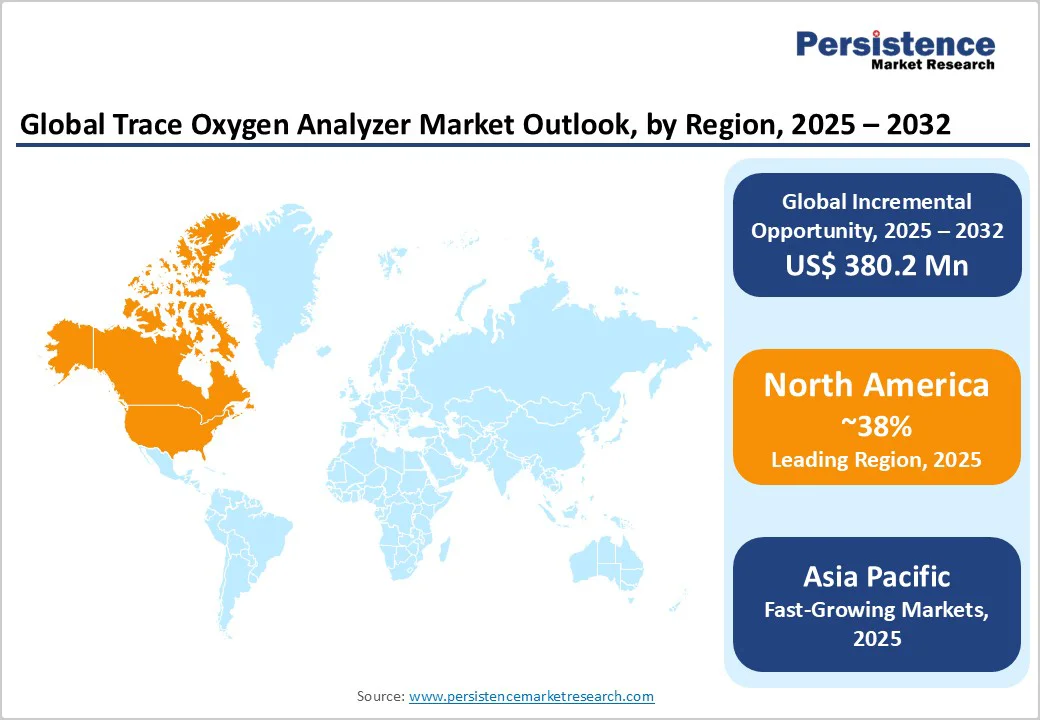

- North America leads the global market with 38% share, driven by advanced semiconductor manufacturing and stringent FDA pharmaceutical regulations.

- Asia Pacific emerges as the fastest-growing region with 7.2% CAGR, fueled by China's semiconductor expansion and India's pharmaceutical industry growth.

- Electrochemical sensors dominate technology adoption with 35% market share due to cost-effectiveness and ambient temperature operation capabilities.

- Semiconductor manufacturing represents the fastest-growing application with 8.1% CAGR, driven by advanced process node requirements and yield optimization needs.

- IoT integration presents the key market opportunity with $150 million potential by 2032 through smart manufacturing and predictive maintenance adoption.

| Key Insights | Details |

|---|---|

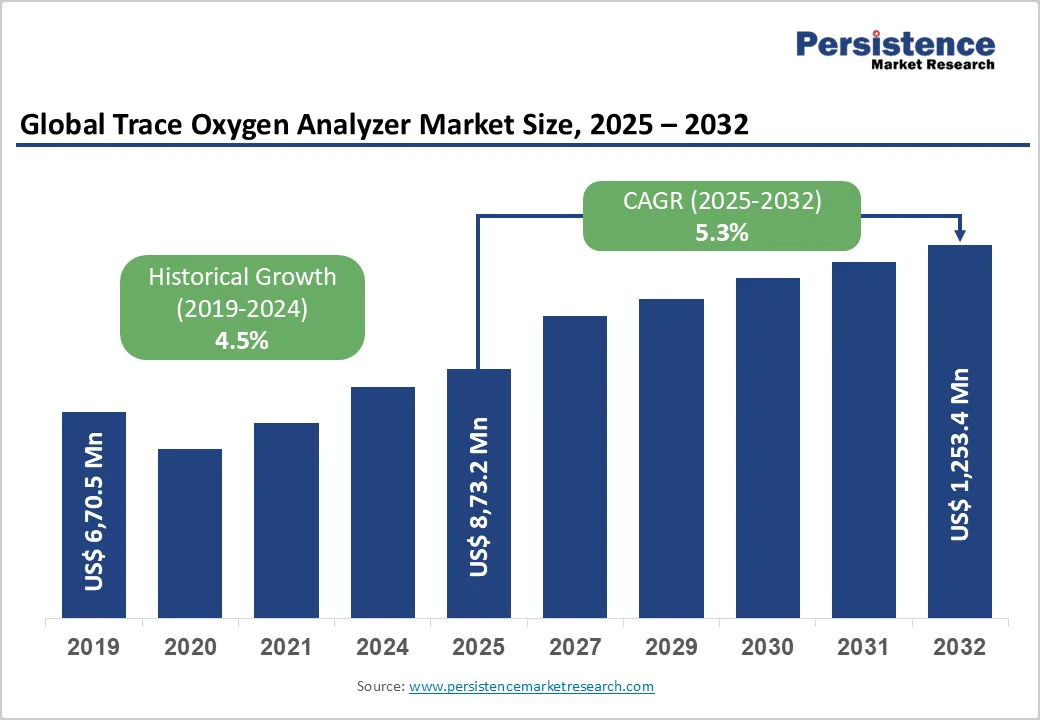

| Trace Oxygen Analyzer Market Size (2025E) | US$ 873.2 million |

| Market Value Forecast (2032F) | US$ 1,253.4 million |

| Projected Growth CAGR (2025 - 2032) | 5.3% |

| Historical Market Growth (2019 - 2024) | 4.5% |

Market Dynamics

Drivers - Stringent Regulatory Requirements in Pharmaceutical Manufacturing

The pharmaceutical industry's adherence to FDA 21 CFR Part 211 and EU GMP Annex 1 guidelines mandates ultra-pure environments with precise oxygen monitoring in cleanrooms and sterile manufacturing facilities. FDA regulations require compressed air quality to meet or exceed cleanroom classification standards, where oxygen contamination monitoring is critical for maintaining ISO 5 (Class 100) and ISO 7 (Class 10,000) environments.

The European Medicines Agency (EMA) enforces similar requirements under the EU Guidelines for Good Manufacturing Practice, requiring continuous trace oxygen analysis in critical areas where sterilized drug products are exposed. These regulatory frameworks drive consistent demand for trace oxygen analyzers capable of ppb-level detection, ensuring pharmaceutical product integrity and patient safety.

Semiconductor Manufacturing Precision Requirements

The semiconductor industry demands ultra-high purity environments where even ppb-level oxygen contamination can compromise wafer yield and circuit integrity. China's semiconductor production capacity increased by 18% in 2024, with facilities requiring trace oxygen analyzers for chemical vapor deposition, plasma etching, and wafer processing operations.

Taiwan's advanced semiconductor manufacturing contributes 63% of global chip production, where trace oxygen analyzers are essential for monitoring nitrogen purging systems, glove boxes, and process chambers. The industry's transition to 3nm and smaller process nodes intensifies contamination sensitivity, driving demand for analyzers with detection limits below 50 ppb to maintain optimal production yields.

Restraints - High Initial Investment and Maintenance Costs

Advanced trace oxygen analyzers using laser-based and optical fluorescence technologies require a significant capital investment of $15,000 to $50,000 per unit, creating barriers for small and medium-sized enterprises.

Electrochemical sensors require replacement every 12-24 months at a cost of $500-$2,000, while zirconia sensors require specialized maintenance and calibration procedures. These recurring operational expenses challenge budget-conscious facilities, particularly in emerging markets where cost sensitivity limits the adoption of premium analytical equipment.

Technical Complexity and Skill Requirements

Zirconia-based trace oxygen analyzers operate at 600-800°C temperatures, requiring specialized expertise for installation, calibration, and maintenance procedures. Mass spectrometry-based analyzers demand highly trained technicians for optimal operation, limiting widespread deployment in facilities lacking analytical chemistry expertise.

Complex calibration protocols and potential cross-interference from sulfur compounds in zirconia sensors create operational challenges, necessitating continuous technical support and specialized training programs.

Opportunities - Expanding Food and Beverage Modified Atmosphere Packaging

The global Modified Atmosphere Packaging (MAP) market, valued at $4.2 billion in 2024, is driving increased demand for trace oxygen analyzers to monitor packaging atmospheres and extend product shelf life. European food safety regulations mandate oxygen monitoring in MAP applications, where levels must remain below 2% to prevent spoilage and maintain product quality.

Asia-Pacific beverage industries are adopting headspace analyzers to monitor oxygen levels in PET bottles, as China's beverage production grows 8.5% annually. Rising consumer demand for premium packaged foods and stringent USDA and EFSA food safety standards create substantial opportunities for portable trace oxygen analyzers in quality control applications.

Industrial Internet of Things (IoT) Integration Trends

The convergence of Industry 4.0 and trace oxygen analysis presents significant growth opportunities through IoT-enabled real-time monitoring systems. Smart manufacturing initiatives in Germany's chemical industry are integrating trace oxygen analyzers with predictive maintenance algorithms, reducing downtime by 25% and optimizing process efficiency.

North American petrochemical facilities are deploying wireless sensor networks with trace oxygen analyzers for continuous emissions monitoring and safety compliance. The growing adoption of cloud-based data analytics and remote diagnostics capabilities enables proactive maintenance scheduling and enhances analyzer performance, creating new revenue streams for technology providers.

Category-wise Insights

Product Type Analysis

Process Analyzers dominate the Trace Oxygen Analyzer Market with approximately 42% market share, driven by their continuous monitoring capabilities in critical industrial applications. These fixed-installation systems provide 24/7 real-time oxygen measurement in semiconductor fabrication, pharmaceutical cleanrooms, and petrochemical processes where consistent monitoring is essential for safety and quality control.

Process analyzers offer superior accuracy with detection limits down to 10 ppb and integrate seamlessly with distributed control systems (DCS) for automated process optimization. Their robust design enables operation in harsh industrial environments with minimal maintenance requirements, making them preferred for applications requiring uninterrupted oxygen monitoring and regulatory compliance documentation.

Measurement Range Analysis

Parts-per-million (ppm) Range Analyzers capture the largest market share at approximately 38%, reflecting widespread demand for mid-range sensitivity applications across diverse industries. These analyzers serve critical functions in industrial gas purity verification, heat treatment atmospheres, and gas storage monitoring, where oxygen levels between 1-1000 ppm must be precisely controlled.

Food packaging applications use ppm-range analyzers for modified-atmosphere packaging validation, ensuring oxygen levels remain below 500 ppm to prevent product deterioration. Their balanced combination of sensitivity, cost-effectiveness, and operational simplicity makes them suitable for routine quality control in chemical manufacturing, metal processing, and laboratory research environments.

Technology Analysis

Electrochemical Sensors lead the market with approximately 35% share due to their cost-effectiveness, compact design, and suitability for ambient temperature applications. These sensors provide excellent sensitivity for trace-level detection with lifespans of 12-24 months and simple replacement procedures, making them ideal for portable analyzers and safety monitoring systems.

Electrochemical technology dominates in pharmaceutical cleanrooms, glove box monitoring, and confined-space safety applications, where fast response times and reliability are paramount. Their ability to operate without external heating and minimal power consumption makes them preferred for battery-operated devices and applications requiring explosion-proof certification in hazardous environments.

Application Analysis

Semiconductor & Electronics Manufacturing is the fastest-growing application segment, with approximately 28% market share, driven by rising global chip production and stringent purity requirements. Taiwan's semiconductor industry, producing 63% of global chips, relies heavily on trace oxygen analyzers for wafer processing, cleanroom monitoring, and process gas purity verification.

South Korea's memory chip production facilities utilize these analyzers for chemical vapor deposition and plasma etching processes, where sub-ppm oxygen levels are critical for yield optimization. The industry's transition to advanced 5nm and 3nm process technologies intensifies contamination sensitivity, driving demand for analyzers with ppb-level detection capabilities and real-time monitoring functionality.

End User Analysis

Industrial Process Operators constitute the largest end-user segment, with approximately 33% market share, encompassing chemical, petrochemical, and power generation facilities that require continuous oxygen monitoring for safety and efficiency.

These operators deploy trace oxygen analyzers for combustion optimization, inert gas blanketing, and pipeline leak detection, where precise oxygen control is essential to preventing explosions and maintaining process efficiency.

Oil refineries use these systems to monitor flue gas oxygen content to optimize fuel-to-air ratios and reduce emissions, while chemical plants use them to control reactor atmospheres and ensure product quality in oxygen-sensitive manufacturing processes.

Regional Insights

North America Trace Oxygen Analyzer Market Trends

North America maintains market leadership driven by advanced semiconductor manufacturing and stringent pharmaceutical regulatory standards. The United States semiconductor industry, supported by the CHIPS and Science Act with $52 billion in federal funding, is expanding domestic chip production capabilities, driving increased demand for trace oxygen analyzers in cleanroom environments and process monitoring.

FDA regulations under 21 CFR Part 210 and Part 211 mandate precise oxygen monitoring in pharmaceutical manufacturing, with compressed air quality requirements matching cleanroom classifications. The region's robust innovation ecosystem fosters development of advanced analyzer technologies, with companies like Emerson Electric and Honeywell investing in IoT-enabled monitoring solutions and laser-based detection systems.

Europe Trace Oxygen Analyzer Market Trends

Europe demonstrates strong market growth driven by pharmaceutical manufacturing excellence and environmental compliance initiatives. Germany's chemical industry, the largest in Europe, utilizes trace oxygen analyzers for process optimization and emissions monitoring, with BASF and Bayer implementing advanced monitoring systems across their manufacturing facilities.

UK pharmaceutical companies comply with MHRA guidelines aligned with EU GMP Annex 1, requiring continuous oxygen monitoring in sterile manufacturing environments. France's aerospace industry employs trace oxygen analyzers for high-temperature testing and material processing applications, while Netherlands food processing facilities adopt these systems for modified atmosphere packaging validation.

Asia Pacific Trace Oxygen Analyzer Market Trends

Asia Pacific represents the fastest-growing regional market, driven by rapid industrialization and expanding semiconductor manufacturing capacity. China's semiconductor production increased 18% in 2024, with SMIC and domestic foundries requiring trace oxygen analyzers for advanced process nodes and cleanroom monitoring.

Taiwan's semiconductor dominance, which accounts for 63% of global chip production through TSMC and other foundries, creates substantial demand for ultra-high-purity monitoring systems. Japan's precision manufacturing sector, including companies such as Sony and Panasonic, uses trace oxygen analyzers for electronic component production and quality control.

Competitive Landscape

The global Trace Oxygen Analyzer Market exhibits a moderately consolidated structure with leading companies maintaining 35-40% combined market share through technological differentiation and strategic partnerships. Market leaders are investing in R&D for laser-based and optical sensor technologies to achieve ppb-level detection capabilities and enhanced reliability.

Key competitive strategies include vertical integration with sensor manufacturing, development of IoT connectivity, and industry-specific solution customization for semiconductor, pharmaceutical, and petrochemical applications. Companies are expanding through strategic acquisitions of specialized sensor manufacturers and establishing regional partnerships to strengthen market presence in high-growth Asia-Pacific markets.

Key Market Developments:

- October 2024: Advanced Micro Instruments Inc. launched their new GPR-2800 series portable trace oxygen analyzer featuring enhanced electrochemical sensor technology with 10 ppb detection capability and IoT connectivity for remote monitoring applications.

- August 2024: Emerson Electric Co. announced a partnership with TSMC to deploy X-STREAM Enhanced continuous gas analyzers across semiconductor fabrication facilities, enabling real-time trace oxygen monitoring for advanced process nodes.

- June, 2024: Nova Analytical Systems introduced their Model 4100 trace oxygen analyzer with proprietary fluorescence quenching technology, offering 5 ppb detection limit and enhanced stability for pharmaceutical cleanroom applications.

Companies Covered in Trace Oxygen Analyzer Market

- Emerson Electric Co

- Nova Analytical Systems

- Advanced Micro Instruments Inc

- Thermo Fisher Scientific

- Setra Systems

- Parker Hannifin

- Siemens

- ABB

- Ametek

- Honeywell

- Endress+Hauser

- Metrohm

- Yokogawa Electric Corporation

- Teledyne Technologies Incorporated

- Horiba, Ltd

Frequently Asked Questions

The global Trace Oxygen Analyzer Market is projected to reach US$ 1,253.4 million by 2032, growing from US$ 873.2 million in 2025 at a CAGR of 5.3%.

Major demand drivers include stringent pharmaceutical regulations, semiconductor contamination control, and food packaging atmosphere monitoring.

Electrochemical sensors lead the market with around 35% share due to their cost-effectiveness and versatility.

Asia Pacific shows the fastest growth at 7.2% CAGR, driven by industrial and semiconductor expansion.

IoT-enabled smart monitoring and predictive maintenance offer a $150 million opportunity by 2032.

Key market players include Emerson, Nova Analytical, AMI, Thermo Fisher, Honeywell, Siemens, ABB, and Yokogawa.